GCC Prefabricated Buildings Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Type (Modular Buildings, Panelized Buildings, Pre-Engineered Buildings, Container Buildings), By Application (Residential, Commercial, Industrial, Healthcare, Education, Hospita ... lity), and others Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

GCC Prefabricated Buildings Market

Projected 4.95% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 6.2 Billion

Market Size (2032)

USD 8.28 Billion

Base Year

2025

Projected CAGR

4.95%

Leading Segments

By Application: Industrial

GCC Prefabricated Buildings Market Report Key Takeaways:

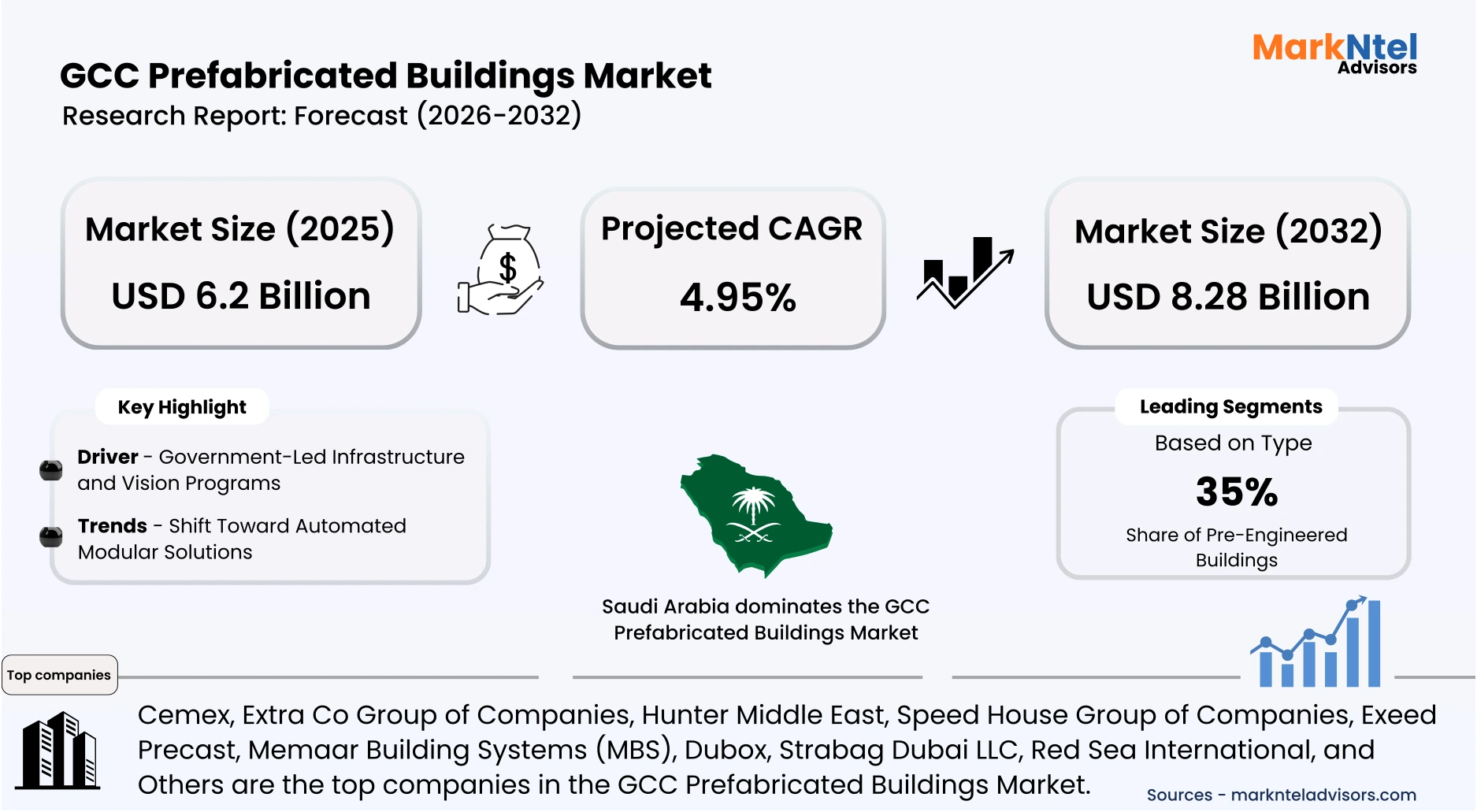

- Market size was valued at around USD 6.2 billion in 2025 and is projected to reach USD 8.28 billion by 2032. The estimated CAGR from 2026 to 2032 is around 4.95%, indicating strong growth.

- Saudi Arabia is dominating this market by accounting for more than 38% of the market share in 2025.

- By Type, the Pre-Engineered Buildings (PEB) segment represented a significant share of about 35% in the GCC Prefabricated Buildings Market in 2025.

- By Application, the Industrial segment represented a significant share of about 32% in the GCC Prefabricated Buildings Market in 2025.

- Leading Prefabricated Buildings in GCC are Cemex, Extra Co Group of Companies, Hunter Middle East, Speed House Group of Companies, Exeed Precast, Memaar Building Systems (MBS), Dubox, Strabag Dubai LLC, Red Sea International, and Others.

Market Insights & Analysis: GCC Prefabricated Buildings Market (2026-32):

The GCC Prefabricated Buildings Market size was valued at around USD 6.2 billion in 2025 and is projected to reach USD 8.28 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 4.95% during the forecast period, i.e., 2026-32.

The GCC Prefabricated Buildings Market continues to benefit from large-scale public investment programs that are accelerating construction activity across member states. Saudi Arabia’s Vision 2030 initiative has driven the launch of real estate and infrastructure projects valued at approximately USD 1.3 trillion, with the wider national construction project pipeline estimated to exceed USD 1.7 trillion, underscoring substantial long-term demand for advanced construction technologies. Additionally, Saudi Arabia maintained strong capital expenditure on infrastructure and urban development despite fiscal adjustments, reinforcing construction momentum. In parallel, the UAE’s 2025 federal budget of approximately USD 17.5 billion prioritizes infrastructure, housing, and economic development, supporting continued uptake of industrialized construction methods .

Residential demand remains a key growth pillar, particularly in Saudi Arabia, where the Housing Program under Vision 2030 aims to raise homeownership to 70%, according to official government releases. Rapid population growth across GCC states, highlighted by World Bank demographic data, continues to necessitate new housing supply, encouraging faster delivery mechanisms such as prefabrication . Industrial and logistics expansion also strengthens demand, as Saudi Arabia’s National Industrial Development and Logistics Program promotes manufacturing and warehousing capacity growth. The UAE Ministry of Industry and Advanced Technology has similarly emphasized advanced construction technologies to enhance productivity and reduce waste in industrial projects.

Institutional and commercial segments further reinforce market expansion through government-backed infrastructure plans in healthcare, education, and tourism. Saudi Arabia’s 2025 budget allocates substantial funding to health and education sectors, according to official Ministry of Finance statements, supporting new facility construction . In the UAE, national tourism strategies aim to attract increased visitor numbers by 2031, driving hotel and mixed-use developments that require efficient building systems. Regulatory measures such as Dubai’s Green Building Regulations and Saudi energy efficiency programs encourage the adoption of resource-efficient construction methods compatible with modular systems.

Looking ahead, sustained fiscal commitments and diversification strategies are expected to underpin continued growth in prefabricated construction adoption. The World Bank’s 2025 regional outlook projects stable non-oil growth across GCC economies, supported by infrastructure and private-sector investment . Ongoing smart city and industrial cluster developments across Saudi Arabia, the UAE, and Qatar provide a structural pipeline of projects suited to off-site and pre-engineered solutions. With policy alignment, demographic expansion, and efficiency-driven construction reforms converging, the GCC prefabricated buildings market is positioned for resilient and policy-supported expansion in the coming years.

GCC Prefabricated Buildings Market Recent Developments:

- 2025 : Dubai-based DuBox launched “WorkBox,” a standardized modular office solution under its new Productization strategy. Built using off-site volumetric concrete construction, the turnkey system enables delivery within seven months. The launch strengthens modular construction adoption in the GCC commercial sector and aligns with regional sustainability and industrial modernization goals.

GCC Prefabricated Buildings Market Scope:

| Category | Segments |

|---|---|

| By Type | (Modular Buildings, Panelized Buildings, Pre-Engineered Buildings, Container Buildings), |

| By Application | (Residential, Commercial, Industrial, Healthcare, Education, Hospitality), |

GCC Prefabricated Buildings Market Driver:

Government-Led Infrastructure and Vision Programs

Government-led infrastructure expansion under national transformation agendas has emerged as the most influential structural driver of this market. In 2025, Saudi Arabia’s Public Investment Fund reported assets exceeding USD 925 billion and confirmed sustained domestic investment across real estate, logistics, tourism, and industrial sectors, reinforcing long-term construction pipelines . Additionally, as per the U.S. Department of State’s 2025 Qatar Investment Climate Statement, the Qatari government allocated nearly USD 17 billion for major projects in areas like infrastructure, education, and healthcare. These sovereign-backed commitments structurally increase demand for faster and scalable construction delivery models such as modular and pre-engineered systems.

This driver materially enlarges total market volume because it increases the absolute scale of infrastructure rollout rather than influencing short-term pricing dynamics. For instance, as per the IMF (2025), sustained capital formation and public investment across Gulf economies are key growth mechanisms . As sovereign-backed entities institutionalize multi-year project pipelines, construction output expands structurally across residential, industrial, and institutional segments. Consequently, prefabricated buildings benefit from recurring, large-scale deployment requirements aligned with accelerated project execution mandates throughout the GCC.

GCC Prefabricated Buildings Market Trend:

Shift Toward Automated Modular Solutions

The shift toward standardized and productized modular solutions has emerged as the most significant structural transformation reshaping the GCC Prefabricated Buildings Market. Governments across the region are increasingly institutionalizing industrialized construction to improve productivity, reduce waste, and meet compressed project timelines under national transformation agendas. For instance, in 2025, Saudi Arabia’s Ministry of Municipal and Rural Affairs and Housing reinforced the adoption of modern construction methods to accelerate housing delivery, while the UAE’s Ministry of Industry and Advanced Technology advanced manufacturing-led construction integration under its industrial strategy framework. Complementing these efforts, Dubai Municipality launched the 70–70 Strategy for 2030, targeting 70% off-site construction and 70% factory automation, by including robotic construction strategies, thereby formalizing large-scale modular and factory-based building practices.

This policy-backed transition is restructuring industry dynamics by shifting from bespoke, project-driven construction toward repeatable, factory-engineered systems with standardized design templates and controlled manufacturing environments. Companies are expanding integrated design-manufacture-build models to secure cost predictability and schedule reliability, reflecting a move toward vertically coordinated value chains. For example, Group AMANA has scaled modular manufacturing capacity in the UAE and Saudi Arabia through DuBox and DuPod, reporting delivery timelines up to 30% faster using volumetric off-site systems . Additionally, Hong Kong-based AluHouse announced plans to establish a Saudi manufacturing facility capable of producing 30,000 prefabricated flats annually, signaling industrial-scale housing standardization .

The persistence of this trend is reinforced by labor constraints, sustainability mandates, and long-term capital formation across Gulf economies. The IMF’s 2025 regional outlook underscores continued infrastructure-led growth, which necessitates scalable and automation-driven delivery models rather than incremental efficiency improvements. As regulatory frameworks increasingly recognize modular accreditation and robotic construction technologies, industrialized building systems are transitioning from alternative solutions to mainstream procurement models. Consequently, productization is redefining competitive positioning and embedding standardized modular construction as a foundational component of the GCC’s evolving construction ecosystem.

GCC Prefabricated Buildings Market Opportunity:

Expansion of Affordable and Workforce Housing Projects

The expansion of affordable and workforce housing presents a compelling structural opportunity for new entrants in the GCC prefabricated buildings market. In 2025, the UAE signed agreements to deliver 17,000 affordable housing units for key sector workers, while Sharjah approved an additional 2,000 units, reflecting a strong government commitment to an accessible housing supply . Abu Dhabi also launched a Value Housing Programme in 2025 to boost real estate supply through public-private partnerships . These initiatives are driven by demographic expansion and rising demand for workforce accommodation across major urban centers.

This opportunity exists because housing affordability pressures and population growth are accelerating residential development targets across the region. In 2025, Saudi Arabia reported that housing rents remained a primary contributor to inflation, underscoring persistent residential demand pressures. Dubai has similarly expanded affordable housing allocations to accommodate residents across income levels . As governments seek faster delivery mechanisms to stabilize supply, prefabricated housing solutions translate policy targets directly into scalable construction demand.

The segment is particularly advantageous for new and emerging players because affordable housing projects rely on standardized layouts and repetitive unit typologies rather than bespoke architectural complexity. Modular manufacturers can compete on speed, cost control, and scalable production through off-site fabrication facilities. Compared to mega mixed-use developments dominated by established contractors, workforce housing programs offer clearer procurement frameworks and recurring volume contracts. This creates a structurally favorable entry pathway for modular firms capable of delivering high-volume, standardized residential units efficiently.

GCC Prefabricated Buildings Market Challenges:

High Capital Investment for Advanced Manufacturing Facilities

High capital investment requirements for advanced modular manufacturing facilities remain a critical structural constraint in the GCC prefabricated buildings market. Modular production plants require automated fabrication lines, robotics, precision molds, curing chambers, heavy-lift systems, and quality laboratories, all of which significantly elevate upfront capital expenditure. In 2025, GCC monetary policy remained aligned with U.S. Federal Reserve rates, keeping benchmark interest rates elevated across the region. This higher borrowing environment increases financing costs for capital-intensive factory investments. In 2025, GCC central banks maintained elevated interest rates in line with global monetary tightening, reinforcing higher financing costs for industrial expansion and manufacturing investments across the regi on.

The burden is further intensified by the need to establish production capacity within designated industrial zones to comply with localization and in-country value frameworks. Setting up volumetric modular factories requires long-term land leases, infrastructure connections, and compliance with industrial safety and environmental standards, which materially increase fixed asset commitments. In addition, most advanced automation equipment and robotics systems are imported, exposing manufacturers to currency and supply chain risks. These combined cost pressures raise the minimum viable investment threshold for new entrants. In 2025, Saudi localization and production policies continued to emphasize domestic manufacturing under in-country value programs, increasing capital commitments for companies seeking to establish factory-based operations.

This capital intensity restricts market participation primarily to well-funded conglomerates or multinational firms capable of absorbing long payback cycles. Smaller modular players face constrained access to affordable financing and higher risk exposure when committing to fixed manufacturing assets without guaranteed project pipelines. As a result, despite rising housing and industrial demand, the pace of new factory establishment remains measured, limiting rapid capacity expansion and slowing broader competitive entry across the GCC prefabricated buildings market.

GCC Prefabricated Buildings Market (2026-32) Segmentation Analysis:

The GCC Prefabricated Buildings Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the GCC level. Based on the analysis, the market has been further classified as;

Based on Type

- Modular Buildings

- Panelized Buildings

- Pre-Engineered Buildings

- Container Buildings

Pre-Engineered Buildings (PEB) dominate the GCC Prefabricated Buildings Market, accounting for approximately 35% of total market share, because they directly align with the region’s large-scale industrial, logistics, and infrastructure expansion. GCC economies are accelerating industrial diversification under national strategies such as Saudi Arabia’s industrial development programs and the UAE’s Operation 300bn initiative, which targets significant growth in the market. These initiatives require rapid deployment of factories, warehouses, and logistics hubs, where steel-based PEB structures offer faster construction timelines and scalable design flexibility compared to conventional methods.

This dominance is particularly evident in the industrial and logistics segments, which represent some of the fastest-growing construction categories across Saudi Arabia and the UAE. The expansion of economic zones, free zones, and port-linked logistics corridors increases demand for wide-span, column-free structures capable of accommodating heavy machinery and high storage volumes. PEB systems provide cost efficiency, structural durability under harsh climatic conditions, and adaptability for future expansion, making them the preferred solution for industrial developers. Additionally, steel-intensive PEB structures reduce construction time and labor dependency, supporting compressed project schedules common in GCC infrastructure rollouts. Consequently, sustained growth in industrial real estate, warehousing demand, and infrastructure development reinforces PEB’s leading position within the GCC prefabricated buildings market.

Based on the Application

- Residential

- Commercial

- Industrial

- Healthcare

- Education

- Hospitality

The Industrial segment dominates the GCC Prefabricated Buildings Market, accounting for approximately 32% of total market share, because industrial diversification and manufacturing expansion have become primary growth engines across Gulf economies. Governments are actively increasing the contribution of non-oil sectors, driving large-scale development of factories, logistics hubs, processing plants, and industrial parks. In June 2025, Saudi Arabia issued 83 new industrial licenses and opened 58 factories with investments exceeding approximately USD 760 million, reflecting tangible expansion in manufacturing capacity across the Kingdom. This acceleration in industrial activity directly translates into higher demand for pre-engineered and prefabricated industrial structures.

This dominance is particularly evident in logistics and manufacturing infrastructure, where wide-span steel buildings, warehouses, and processing facilities are required at scale. Saudi Arabia’s industrial cities and logistics corridor developments continue to expand under national diversification programs, generating recurring demand for factory shells, storage facilities, and maintenance structures. Similarly, Qatar’s USD 22.3 billion infrastructure blueprint for 2025–2029 is expected to significantly increase demand for structural steel and prefabricated components across municipal, utility, and electromechanical projects. The scale of these developments reinforces the requirement for modular and steel-based construction systems capable of supporting large industrial and logistics facilities. Additionally, Saudi Global Ports expanded King Abdulaziz Port Dammam and launched a USD 346 million logistics zone, with capacity projected to reach 3.8 million TEUs by 2026, strengthening demand for logistics-linked industrial structures. Industrial projects typically operate on accelerated timelines and require modular, scalable, and durable structural systems capable of accommodating heavy equipment and high load capacities. Prefabricated and pre-engineered buildings provide cost efficiency, structural flexibility, and faster erection compared to conventional construction methods.

GCC Prefabricated Buildings Market (2026-32): Regional Projection

Saudi Arabia dominates the GCC Prefabricated Buildings Market, accounting for approximately 38% of total regional demand, because it hosts the largest construction and infrastructure ecosystem in the Gulf. The Kingdom’s construction industry has remained robust through 2025, with official projections showing steady public investment into urban, industrial, and mega-scale developments. For example, the Saudi Ministry of Finance’s 2025 budget documents highlight sustained capital expenditure on infrastructure and housing programs, which underpin large-scale building activity. These extensive programs generate high volumes of demand for prefabricated and pre-engineered structures that can be delivered more rapidly than traditional builds.

This dominance is reinforced by Saudi Arabia’s extensive logistics and mixed-use master plans, which consistently favor modular and PEB systems. In 2025, Saudi transport and logistics upgrades, including port expansions and corridor networks, were prioritized as part of national infrastructure plans, driving the construction of supporting facilities such as warehouses, maintenance hubs, and utility buildings . This infrastructure spending outpaces that of smaller GCC markets with narrower construction pipelines. The size and distribution of Saudi projects also necessitate repeatable, scalable building systems across large geographic areas.

Saudi Arabia’s leadership is further strengthened by its expanding domestic industrial base and in-country value programs, which encourage local manufacturing of structural components and prefabricated units. This integration decreases dependency on imports and aligns construction supply chains with national economic diversification goals. Consequently, consistent government-backed development and comprehensive industrialization efforts position Saudi Arabia ahead of other GCC countries in prefabricated buildings demand.

Gain a Competitive Edge with Our GCC Prefabricated Buildings Market Report

- GCC Prefabricated Buildings Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Prefabricated Buildings Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Prefabricated Buildings Market Policies, Regulations, and Product Standards

- GCC Prefabricated Buildings Market Trends & Developments

- GCC Prefabricated Buildings Market Dynamics

- Growth Drivers

- Challenges

- GCC Prefabricated Buildings Market Hotspot & Opportunities

- GCC Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type

- Modular Buildings

- Panelized Buildings

- Pre-Engineered Buildings

- Container Buildings

- By Application

- Residential

- Commercial

- Industrial

- Healthcare

- Education

- Hospitality

- By Country

- Saudi Arabia

- UAE

- Qatar

- Kuwait

- Oman

- Bahrain

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Outlook

- Saudi Arabia Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type -Market Size & Forecast 2022–2032, USD Million

- By Application -Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- UAE Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type -Market Size & Forecast 2022–2032, USD Million

- By Application -Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Qatar Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type -Market Size & Forecast 2022–2032, USD Million

- By Application -Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Kuwait Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type -Market Size & Forecast 2022–2032, USD Million

- By Application -Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Oman Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type -Market Size & Forecast 2022–2032, USD Million

- By Application -Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Bahrain Prefabricated Buildings Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type -Market Size & Forecast 2022–2032, USD Million

- By Application -Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- GCC Prefabricated Buildings Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Cemex

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Extra Co Group of Companies

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Hunter Middle East

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Speed House Group of Companies

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Exeed Precast

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Memaar Building Systems (MBS)

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Dubox

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Strabag Dubai LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Red Sea International

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Cemex

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now