Dubai Facility Management Market Research Report: Growth Drivers & Forecast (2026-2032)

By Operating Model (In-house, Outsourced), By End User (Commercial, Residential, Government, Retail, Education, Healthcare, Hospitality, Others) ... Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Dubai Facility Management Market

Projected 9.5% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 6.2 Billion

Market Size (2032)

USD 10.69 Billion

Base Year

2025

Projected CAGR

9.5%

Leading Segments

By Operating Model: In-house

Dubai Facility Management Market Report Key Takeaways:

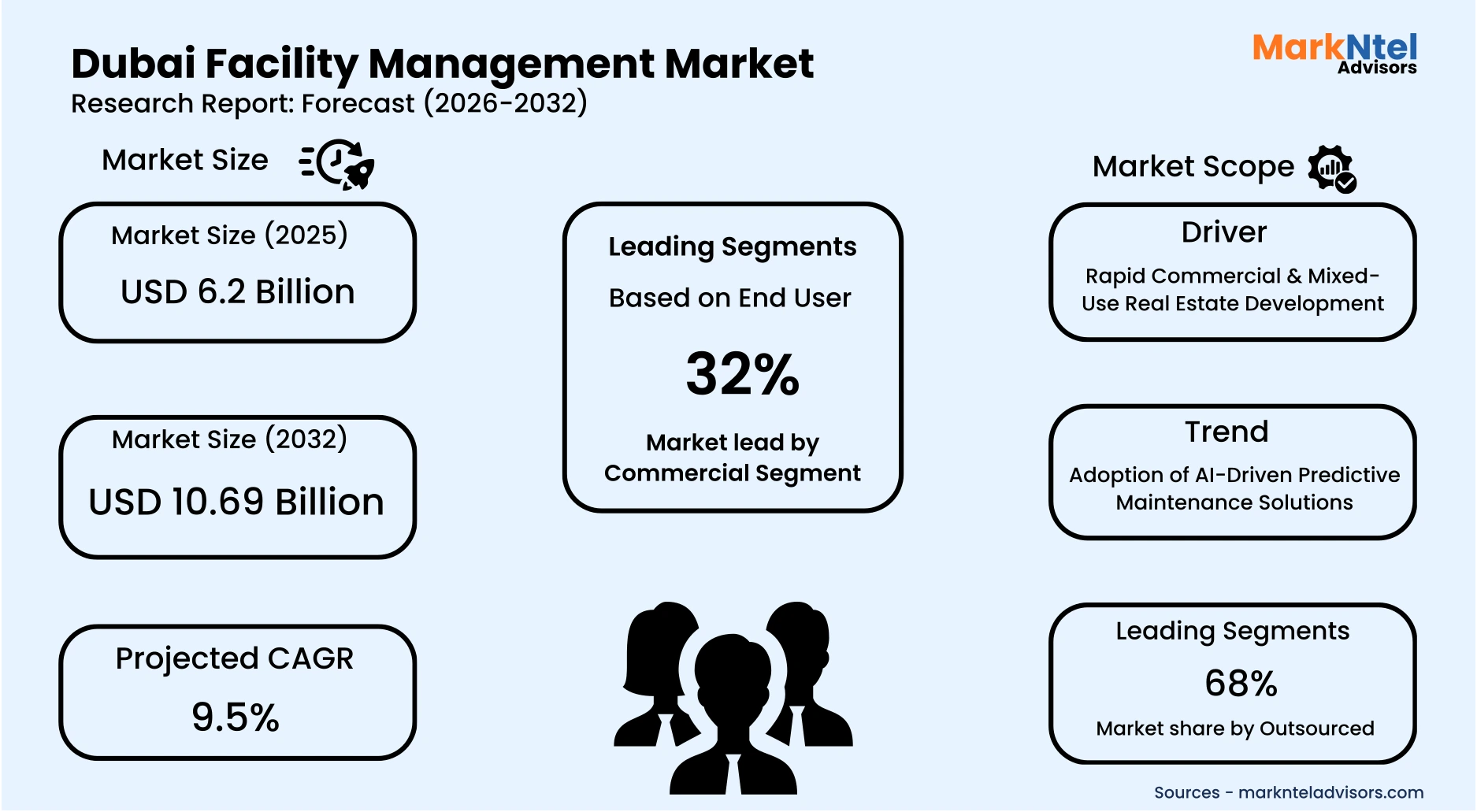

- Market size was valued at around USD 6.2 billion in 2025 and is projected to reach USD 10.69 billion by 2032. The estimated CAGR from 2026 to 2032 is around 9.5%, indicating strong growth.

- By Operating Model, the Outsourced segment represented a significant share of about 68% in the Dubai Facility Management Market in 2025.

- By End User, the Commercial segment represented a significant share of about 32% in the Dubai Facility Management Market in 2025.

- Leading Facility Management Companies in Dubai are Emrill Services LLC, Farnek Services LLC, Imdaad LLC, Transguard Group, EFS Facilities Services Group, Enova Facilities Management Services, ServeU Facilities Management, Khansaheb Facilities Management, and Others.

Market Insights & Analysis: Dubai Facility Management Market (2026-32):

The Dubai Facility Management Market size was valued at around USD 6.2 billion in 2025 and is projected to reach USD 10.69 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 9.5% during the forecast period, i.e., 2026-32.

The Dubai Facility Management (FM) market has expanded in tandem with sustained real estate and infrastructure growth, underpinned by the Dubai 2040 Urban Master Plan, which aims to increase urban capacity and expand public facilities. According to the Dubai Statistics Center (2025) and the Dubai Land Department, the emirate recorded continued growth in real estate transactions, driving consistent demand for maintenance and integrated Facility Management (FM) services. This structural expansion has strengthened outsourced FM adoption across commercial, hospitality, and residential assets.

Current market conditions are supported by dense asset clusters in business districts such as Downtown Dubai and Dubai International Financial Centre, where Grade A office development drives maintenance and compliance needs. The hospitality sector further reinforces FM demand as Dubai tourism reached 19.59 million visitors in 2025, up 5% year-on-year, creating recurring needs for soft services and preventive maintenance across hotels and resorts. Residential high-rise communities managed by developers such as Emaar Properties and Nakheel require integrated technical and community management contracts, expanding outsourced FM penetration across end-users.

Additionally, the regulatory and sustainability frameworks are influencing FM service sophistication and technology adoption. For instance, the UAE Net Zero by 2050 Strategy and Dubai Demand Side Management Strategy 2050 continue to drive energy-efficiency retrofits, building performance monitoring, and carbon reduction measures in 2025 and 2026 , which are significantly increasing the market growth.

Moreover, Dubai Municipality’s Green Building System (Al Sa’fat) increases demand for advanced HVAC optimization, building automation systems, and lifecycle asset audits. Leading FM providers such as Farnek Services LLC and Emrill Services LLC have expanded digital facility platforms and energy management services aligned with these policy objectives, accelerating technology uptake in the sector.

Looking ahead, continued infrastructure investments linked to aviation expansion, metro extensions, and mixed-use developments are expected to sustain multi-year FM contract pipelines. Furthermore, in this market, the commercial segment is projected to remain the largest contributor, while outsourced operating models continue to dominate due to efficiency and regulatory compliance requirements. With ongoing policy-driven sustainability mandates and asset modernization, Dubai’s Facility Management Market outlook remains structurally positive and supported by verifiable economic and regulatory foundations.

Dubai Facility Management Market Recent Developments:

- 2024 : Farnek secured contracts worth over USD 188 million across the UAE, including major projects in Dubai and Saudi Arabia, strengthening its integrated facilities management portfolio and reflecting sustained demand across commercial, hospitality, and residential infrastructure segments in the emirate.

Dubai Facility Management Market Scope:

| Category | Segments |

|---|---|

| By Operating Model | (In-house, Outsourced), |

| By End User | (Commercial, Residential, Government, Retail, Education, Healthcare, Hospitality, Others) |

Dubai Facility Management Market Driver:

Rapid Commercial & Mixed-Use Real Estate Development

Dubai’s sustained commercial and mixed-use real estate expansion remains the most influential structural driver of facility management demand. In 2025, the Dubai Land Department reported real estate transactions exceeding USD 249 billion, reflecting continued project launches, asset transfers, and new property completions . Under the Dubai 2040 Urban Master Plan, the emirate is expanding business districts, urban centers, and mixed-use corridors to accommodate population and economic growth. This expansion directly enlarges the stock of buildings requiring long-term mechanical, electrical, cleaning, and integrated facility services.

The intensification of development is reinforced by rising asset utilization across hospitality and commercial segments. According to the Dubai Department of Economy and Tourism, the emirate welcomed 9.88 million overnight visitors in the first half of 2025, a 6% increase compared with the same period in 2025 . Higher occupancy across hotels and serviced apartments increases operational strain on infrastructure, driving recurring demand for housekeeping, HVAC maintenance, and compliance-driven inspections. Simultaneously, continued office supply growth in financial and business districts strengthens hard and soft FM service requirements.

This driver materially expands market volume because each newly delivered tower, retail complex, or residential community generates multi-year outsourced service contracts. Regulatory frameworks such as Dubai Municipality’s Al Sa’fat Green Building System and the UAE Net Zero by 2050 initiative further increase technical service scope through mandated energy monitoring and performance standards. These policies elevate the complexity and duration of FM engagements rather than merely influencing short-term pricing. Consequently, real estate expansion structurally increases the serviceable facility base, ensuring sustained and scalable demand growth across Dubai.

Dubai Facility Management Market Trend:

Adoption of AI-Driven Predictive Maintenance Solutions

The adoption of AI-driven predictive maintenance has accelerated in Dubai due to national digital transformation policies and smart infrastructure investments. The UAE Artificial Intelligence Strategy 2031 and Dubai Digital Strategy aim to embed AI across government and enterprise operations, strengthening data-driven asset management practices. In 2025, Dubai Electricity and Water Authority (DEWA) expanded its use of AI and digital twin technologies to enhance grid reliability and infrastructure monitoring. These public-sector deployments have encouraged commercial property owners to implement sensor-based and analytics-enabled building management systems.

This shift is structurally transforming facility management operations from reactive maintenance toward predictive, condition-based service models. IoT-enabled HVAC, elevator, and MEP systems now generate continuous performance data, enabling early fault detection and reduced downtime. Dubai’s aviation and transport infrastructure, including airport and metro modernization programs reported in 2025, increasingly relies on intelligent asset monitoring platforms.

For instance, in 2025, Dubai Municipality signed a strategic Memorandum of Understanding (MoU) with Siemens to enhance the integration of artificial intelligence (AI) and advanced digital technologies across the emirate’s public facilities, focusing on predictive maintenance, smart infrastructure, energy optimisation, and digital asset management solutions. Technology integration also enhances transparency and reporting, strengthening long-term client relationships and contract stability. Consequently, AI-driven predictive maintenance represents a sustained structural transformation reshaping service delivery, workforce skills, and competitive positioning across Dubai’s FM market.

Dubai Facility Management Market Opportunity:

Growth in Healthcare & Educational Infrastructure Assets

The expansion of healthcare and education infrastructure in Dubai presents a compelling structural opportunity for new facility management entrants. In 2025, Dubai Healthcare City Authority announced a USD 354 million infrastructure expansion to develop advanced medical and commercial facilities, reinforcing the emirate’s healthcare capacity . Under the Dubai Social Agenda 33, the government also plans to open three new hospitals and 33 primary healthcare centers by 2033 . These initiatives reflect a long-term institutional asset expansion strategy rather than short-term project cycles.

This expansion directly generates demand for specialized facility services, including biomedical equipment maintenance, infection control systems, HVAC filtration management, and regulatory compliance monitoring. Healthcare facilities operate under stringent operational and hygiene standards, requiring continuous environmental performance oversight and technical servicing. Similarly, expanding private school infrastructure under Dubai’s education growth framework increases demand for integrated campus maintenance, laboratory safety management, and energy monitoring systems. The institutional nature of these assets ensures recurring and technically complex FM service requirements.

The opportunity is particularly favourable for emerging players because institutional clients prioritize technical specialization and compliance capability over scale alone. Smaller firms can differentiate through niche expertise in medical facility standards, cleanroom environments, or digital monitoring solutions. Long-term public and private investment commitments reduce demand volatility and enable contract stability. Consequently, healthcare and educational infrastructure expansion creates scalable and defensible entry pathways for specialized FM providers in Dubai.

Dubai Facility Management Market Challenge:

Rising Compliance Costs for Sustainability Standards

Rising compliance costs associated with sustainability mandates represent a structural constraint for facility management providers in Dubai. The UAE’s Net Zero by 2050 strategic initiative and Dubai’s Demand Side Management Strategy require continuous energy monitoring, retrofitting of existing assets, and improved building performance standards . Dubai Municipality’s Al Sa’fat Green Building System imposes design, material, and operational efficiency requirements on new developments and major refurbishments. These evolving regulations increase capital expenditure obligations for energy audits, smart metering systems, and high-efficiency HVAC upgrades .

The financial burden is measurable across the region, where energy retrofits and performance optimization projects require substantial upfront investment before cost savings materialize. According to official UAE energy strategy disclosures, billions of dollars are earmarked for clean energy and efficiency initiatives , with implementation responsibilities often transferred to building operators and service providers. Compliance also necessitates workforce training, digital monitoring infrastructure, and certification processes. Smaller FM firms may face higher relative costs due to limited economies of scale and restricted access to financing.

This challenge materially restricts market expansion by raising entry barriers and compressing operating margins. High compliance expenditures can delay contract awards, particularly in price-sensitive segments such as residential and retail. The need for certified sustainability expertise further narrows the pool of eligible providers. Consequently, rising regulatory obligations increase operational complexity and investment risk, constraining scalability for emerging and mid-sized market participants.

Dubai Facility Management Market (2026-32) Segmentation Analysis:

The Dubai Facility Management Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the Dubai level. Based on the analysis, the market has been further classified as;

Based on the Operating Model

- In-house

- Outsourced

The outsourced segment dominates the Dubai Facility Management Market with approximately 68% market share because large-scale asset owners increasingly rely on specialized third-party operators to manage complex, high-value infrastructure. Dubai’s commercial and aviation assets require continuous technical oversight, compliance monitoring, and operational scalability that outsourced providers are structurally positioned to deliver. For example, in 2025, Serco secured a contract extension with Dubai Airports valued at approximately USD 135 million, reinforcing long-term reliance on third-party FM expertise . Similarly, Farnek was awarded a five-year facilities management contract by Dubai Airports to deliver services across DXB and DWC, further evidencing the institutional preference for outsourced operating models .

This reliance is not limited to aviation infrastructure but extends across large mixed-use and commercial developments, where asset uptime, safety compliance, and performance monitoring are critical. Outsourced providers centralize workforce management, digital systems, and regulatory compliance processes, reducing administrative burden for asset owners. High-traffic environments such as airports and major commercial hubs require scalable manpower and advanced monitoring platforms, which are more efficiently delivered under integrated FM contract s.

Additionally, outsourced models offer cost predictability and risk transfer advantages compared to in-house operations. By leveraging economies of scale across multiple contracts, service providers can invest in technology, training, and compliance systems without duplicating costs at each site. As asset complexity and regulatory standards continue to rise, outsourcing remains structurally favoured, reinforcing its dominant position in Dubai’s facility management ecosystem.

Based on End User

- Commercial

- Residential

- Government

- Retail

- Education

- Healthcare

- Hospitality

- Others

The commercial segment dominates the Dubai Facility Management Market, accounting for approximately 32% market share, because it represents the emirate’s most asset-intensive and operationally complex built environment. Dubai’s economy is heavily service-oriented, with finance, trade, aviation, and professional services concentrated in high-rise office districts. In 2025, Dubai International Airport handled close to 100 million passengers, reinforcing the scale of commercial and business-linked infrastructure requiring continuous facility services. This high-density commercial ecosystem structurally expands demand for technical maintenance, cleaning, security, and energy managemen t.

For instance, major office districts such as Dubai International Financial Centre and Business Bay operate under strict uptime and compliance requirements, where uninterrupted HVAC, electrical systems, and safety infrastructure are critical. Corporate tenants demand performance-based service level agreements, increasing reliance on integrated facility management contracts. In addition, large retail malls and business parks require centralized building management systems and 24/7 operational oversight. These requirements create larger and more complex FM contracts compared to residential or educational facilities.

Moreover, commercial buildings typically operate extended hours with high occupancy turnover, leading to accelerated equipment wear and higher maintenance frequency. Lease structures often include compliance and sustainability obligations that require professional FM oversight. Compared to institutional or residential segments, commercial properties generate higher per-asset service intensity and contract value. As a result, the commercial segment maintains dominance through scale, operational complexity, and recurring long-term service commitments across Dubai’s business infrastructure.

Gain a Competitive Edge with Our Dubai Facility Management Market Report

- Dubai Facility Management Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Dubai Facility Management Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Dubai Facility Management Market Policies, Regulations, and Product Standards

- Dubai Facility Management Market Supply Chain Analysis

- Dubai Facility Management Market Trends & Developments

- Dubai Facility Management Market Dynamics

- Growth Drivers

- Challenges

- Dubai Facility Management Market Hotspot & Opportunities

- Dubai Facility Management Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Operating Model– Market Size & Forecast 2022–2032, USD Million

- In-house

- Outsourced

- By End User– Market Size & Forecast 2022–2032, USD Million

- Commercial

- Residential

- Government

- Retail

- Education

- Healthcare

- Hospitality

- Others

- By Operating Model– Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Dubai In-house Facility Management Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End User-Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Dubai Outsourced Facility Management Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End User-Market Size & Forecast 2022–2032, USD Million

- Market Size & Outlook

- Dubai Facility Management Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Emrill Services LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Farnek Services LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Imdaad LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Transguard Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- EFS Facilities Services Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Enova Facilities Management Services

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- ServeU Facilities Management

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Khansaheb Facilities Management

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Emrill Services LLC

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now