China Warehouse Automation Market Research Report: Trends & Forecast (2026-2032)

By Component (Hardware, Robots (AMRs, AGVs, SCARA/Delta Arms), Conveyors & Sorters, AS/RS Cranes & Shuttles, Sensors & Scanners, PLC / Controls), Software (WMS / Warehouse Executio ... n Software, Warehouse Control Systems, Fleet / Robot Orchestration, Analytics & Optimization), Services (Installation & Integration, Maintenance & Support, Training & Consulting, Custom Engineering), By Automation Type (Automated Storage and Retrieval Systems (AS/RS), Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Conveyor & Sortation Systems, Robotic Picking & Palletizing, Automated Packing & Labeling, Warehouse Management Systems (WMS / WES / WCS), Automated Identification Systems (RFID / Barcode / Vision), Automated Packaging Systems, Drones & Vision Inspection Automation), By Warehouse Scale (Small Warehouses (Below 10,000 sq. meters), Medium Warehouses (10,000–50,000 sq. meters), Large Warehouses (Above 50,000 sq. meters)), By End-Use Industry (Retail & E-commerce, Logistics Service Providers (3PL / 4PL), Manufacturing, Food & Beverage, Healthcare & Pharmaceuticals, Automotive & Industrial, Electronics & High-Tech, Cold Chain Specialists, Government / Defense Logistics, Warehouse Property Developers), and others Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 140

- Report Format: PDF, Excel, PPT

China Warehouse Automation Market

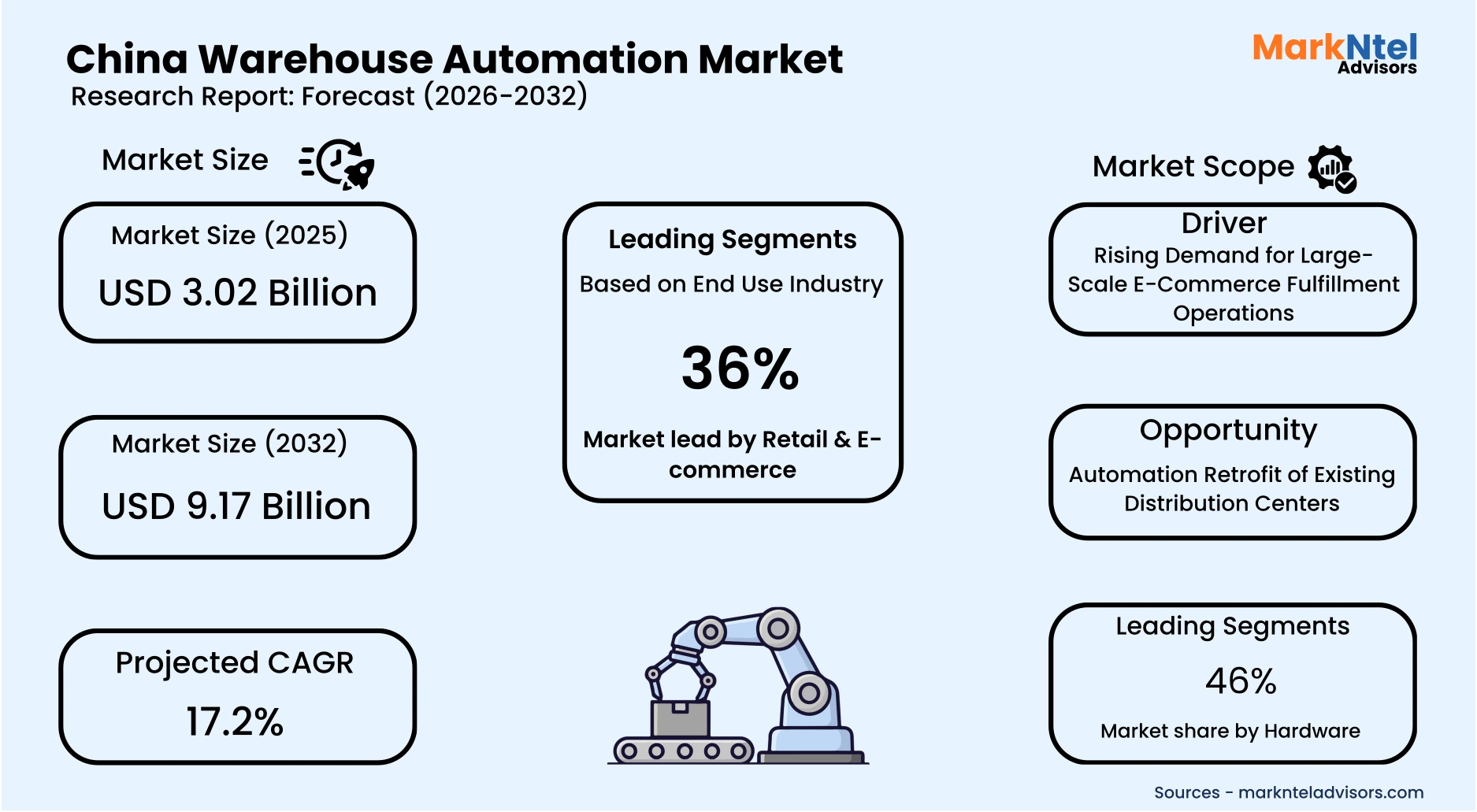

Projected 17.2% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 3.02 Billion

Market Size (2032)

USD 9.17 Billion

Base Year

2025

Projected CAGR

17.2%

Leading Segments

By End Use Industry: Retail and E‑Commerce

China Warehouse Automation Market Report Key Takeaways:

- Market size was valued at around USD3.02 Billion in 2025 and is projected to reach USD9.17 Billion by 2032. The estimated CAGR from 2026 to 2032 is around 17.2%, indicating strong growth.

- By Component, hardware represented a significant share of about 46% in the China Warehouse Automation Market during 2026-32.

- By End Use Industry, the Retail & E-commerce industry seized a major share of around 36% in the China Warehouse Automation Market during the forecast period.

- East China leads the market in 2025 with an estimated market share of around 33%.

- Leading warehouse automation companies in China are Hikrobot, Geekplus Technology Co., Ltd., Quicktron Intelligent Technology, Hai Robotics, Intralox (Shanghai) Automation Equipment Co., Ltd., Dematic (KION Group), Honeywell Intelligrated, Swisslog (Waldner Group), SIASUN Robot & Automation Co., Ltd., BPS Global Group, Shanghai Jingxing Storage Equipment Engineering Co., Ltd., Vanderlande Industries, SSI Schaefer, Knapp AG, Murata Machinery, and others.

Market Insights & Analysis: China Warehouse Automation Market (2026-32):

The China Warehouse Automation Market size was valued at around USD3.02 billion in 2025 and is projected to reach USD9.17 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 17.2% during the forecast period, i.e., 2026-32.

China’s warehouse automation market has expanded steadily over the past decade, underpinned by the country’s scale in manufacturing, retail logistics, and digital commerce. Official data from China’s Ministry of Commerce shows that national e-commerce transaction value exceeded USD3.3 trillion in 2025, sustaining high parcel volumes that accelerated automated storage, sorting, and retrieval adoption across logistics hubs . During the 14th Five-Year Plan period, the National Development and Reform Commission identified “smart logistics” as a core productivity lever, aligning automation investments with industrial upgrading objectives. This policy continuity has translated into sustained capital expenditure by logistics operators and manufacturers seeking throughput efficiency and labor cost stabilization .

Current market conditions reflect a structurally supportive macro environment, characterized by urban consumption growth, aging labor demographics, and rising compliance requirements for workplace safety and energy efficiency. According to the National Bureau of Statistics, China’s working-age population aged 16–59 accounted for 60.6% of the total population in 2025, down from 60.9% in 2024, reinforcing automation demand in labor-intensive warehouse operations . Infrastructure programs under the “new-type infrastructure” framework have expanded 5G, industrial internet, and data center coverage, enabling real-time warehouse execution systems and autonomous mobile robots at scale. Concurrently, regulatory emphasis on carbon intensity reduction has encouraged the adoption of energy-efficient conveyors, regenerative drives, and optimized inventory layouts.

End-user demand is primarily driven by industrial and commercial segments, with third-party logistics providers, e-commerce fulfillment centers, and manufacturing distribution hubs accounting for the majority of installations. The Ministry of Transport reported in 2025 that national logistics costs as a share of GDP continued to trend downward, reflecting efficiency gains from automation in large distribution facilities. Institutional users, including state-owned postal and cold-chain operators, have expanded automated sorting and temperature-controlled storage to meet food safety and pharmaceutical traceability standards. Residential demand is indirect, materializing through higher service expectations that compel commercial operators to invest in faster, more accurate fulfillment systems .

Looking ahead, market prospects remain favorable as policy, technology, and industry strategies converge. The State Council’s 2025 guidance on modern logistics explicitly encourages intelligent warehousing, robotics, and localized equipment manufacturing to strengthen supply chain resilience. Leading domestic players such as Hikrobot , SSI Schaefer China , and China Post Technology have announced new robot platforms, localized production lines, and AI-driven control software aligned with these priorities . Supported by continued public investment, enterprise digitization, and sustainability mandates, China’s warehouse automation market is positioned for resilient growth through the late 2020s.

China Warehouse Automation Market Recent Developments:

- 2025 : KNAPP and SICK have expanded their technology partnership by deploying an automated production logistics solution at SICK’s Kunsziget, Hungary, plant. The project combines Open Shuttle autonomous mobile robots, an automated small parts warehouse, and SAP EWM on S/4HANA to enable just-in-time material supply, seamless goods flow, and improved inventory visibility, while supporting future production growth.

- 2025: Quicktron Robotics, a China-based maker of autonomous forklifts and warehouse robots, has confidentially filed for a Hong Kong IPO that could raise at least USD 100 million as early as next year, according to people familiar with the matter. The timing and size of the offering remain subject to change.

China Warehouse Automation Market Scope:

| Category | Segments |

|---|---|

| By Component | (Hardware, Robots (AMRs, AGVs, SCARA/Delta Arms), Conveyors & Sorters, AS/RS Cranes & Shuttles, Sensors & Scanners, PLC / Controls), Software (WMS / Warehouse Execution Software, Warehouse Control Systems, Fleet / Robot Orchestration, Analytics & Optimization), Services (Installation & Integration, Maintenance & Support, Training & Consulting, Custom Engineering), |

| By Automation Type | (Automated Storage and Retrieval Systems (AS/RS), Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Conveyor & Sortation Systems, Robotic Picking & Palletizing, Automated Packing & Labeling, Warehouse Management Systems (WMS / WES / WCS), Automated Identification Systems (RFID / Barcode / Vision), Automated Packaging Systems, Drones & Vision Inspection Automation), |

| By Warehouse Scale | (Small Warehouses (Below 10,000 sq. meters), Medium Warehouses (10,000–50,000 sq. meters), Large Warehouses (Above 50,000 sq. meters)), |

| By End-Use Industry | (Retail & E-commerce, Logistics Service Providers (3PL / 4PL), Manufacturing, Food & Beverage, Healthcare & Pharmaceuticals, Automotive & Industrial, Electronics & High-Tech, Cold Chain Specialists, Government / Defense Logistics, Warehouse Property Developers), |

China Warehouse Automation Market Driver:

Rising Demand for Large-Scale E-Commerce Fulfillment Operations

The rapid expansion of large-scale e-commerce fulfillment operations has emerged as a decisive structural driver for China’s warehouse automation market, as delivery speed and order accuracy become competitive imperatives. According to the State Post Bureau, China’s parcel delivery sector handled over 140 billion shipments in 2025, averaging more than 530 million parcels per day, with single-day peaks surpassing 600 million . This sustained, ultra-high parcel intensity has placed fulfillment centers under constant throughput pressure, directly accelerating investments in automated sorting systems, high-speed conveyors, and robotic picking technologies.

This demand is increasingly amplified by the globalization of Chinese e-commerce platforms as domestic growth matures. In October 2025, Singles Day promotions expanded simultaneously into 20 international markets, reflecting the growing reliance on cross-border order volumes to sustain growth . Supporting both domestic and overseas demand from centralized fulfillment hubs has increased operational complexity, pushing operators in East and South China to scale warehouse automation to handle higher order diversity, export readiness, and tighter dispatch timelines.

Crucially, this driver expands overall market volume rather than merely accelerating technology substitution, as rising parcel density and geographic reach require additional automated capacity. Manual sorting and labor-intensive workflows are reaching physical and economic limits under sustained peak loads, making automation a prerequisite for incremental volume handling. As a result, each increase in fulfillment scale necessitates new automated warehouses, system expansions, and equipment deployments, anchoring long-term growth in China’s warehouse automation market.

China Warehouse Automation Market Trend:

Increasing Deployment of Autonomous Mobile Robots in Warehouses

The China warehouse automation market is increasingly shifting toward the deployment of autonomous mobile robots (AMRs), driven by the need for flexible intralogistics, rapid scalability, and AI-enabled operational intelligence. In 2025, warehouse operators continued to favor mobile robotics over fixed automation as order variability, SKU complexity, and space constraints intensified across e-commerce and manufacturing facilities. This shift reflects a measurable preference for systems that can be reconfigured quickly without structural redesign while maintaining high throughput and accuracy.

Technology standardization and software-led orchestration frameworks are playing a central role in accelerating this trend. At LogiMAT 2026, SSI Schaefer emphasized mobile robotics and AI as foundational to next-generation intralogistics, presenting FastBots solutions, four-way shuttle systems, and RackBot System ELEVATE, all coordinated through its WAMAS software platform . These solutions demonstrate how AMRs are being integrated into hybrid warehouse environments, allowing operators to incrementally automate workflows, maintain system resilience during peak demand, and optimize space utilization without compromising operational continuity.

Similarly, in 2025, Hikrobot showcased its integrated “eyes-feet-hands” logistics architecture at the China (Guangzhou) International Logistics Equipment and Technology Exhibition, combining machine vision, autonomous mobile robots, and robotic arms into unified warehouse solutions. The company reported deploying over 100,000 mobile robots by 2024 and generating approximately USD 0.83 billion in revenue , highlighting the commercial scale and maturity of AMR adoption in China. These developments illustrate how vendor innovation, AI integration, and modular deployment models are transforming AMRs from supplementary tools into core infrastructure within China’s warehouse automation landscape.

China Warehouse Automation Market Opportunity:

Automation Retrofit of Existing Distribution Centers

China’s warehouse automation market is increasingly supported by the modernization of existing distribution centers that were originally built for labor-intensive operations. A significant share of China’s logistics infrastructure was commissioned before advanced robotics and AI-enabled warehouse software became commercially viable, resulting in low space utilization and constrained throughput. In 2025, industry highlights that logistics operators are increasingly prioritizing on-site capacity expansion, upgrading existing warehouses instead of pursuing new construction to accommodate rising order volumes . This shift reflects both cost pressures and regulatory hurdles associated with greenfield development.

Automation retrofit projects typically focus on modular and scalable technologies, including autonomous mobile robots, automated sortation systems, goods-to-person picking solutions, and software-based warehouse execution platforms. Industry disclosures indicate that retrofitting with modern handling and robotic technologies can lift storage capacity and operational efficiency by up to roughly one-third within unchanged building footprints, making retrofits particularly attractive in land-constrained urban and peri-urban logistics zones . Incremental deployment allows warehouses to remain operational while progressively improving accuracy, speed, and labor stability.

This opportunity materially expands market volume by transforming existing warehouse space into recurring demand for automation hardware, control software, and system integration services. Each retrofit phase often triggers follow-on upgrades as throughput increases or product mixes evolve, creating sustained investment cycles rather than one-time efficiency gains. Consequently, automation retrofitting represents a durable growth pathway that broadens warehouse automation adoption across small, mid-sized, and large distribution centers throughout China.

China Warehouse Automation Market Challenge:

Limited Skilled Workforce for Advanced Warehouse Automation

China’s warehouse automation market faces a structural challenge due to a significant shortage of skilled logistics and technical personnel required to operate, maintain, and optimize advanced automation systems. With widespread adoption of autonomous mobile robots, AI-driven warehouse execution systems, and high-speed sortation equipment, the sector requires professionals capable of handling design, development, commissioning, and operational maintenance. According to the China Federation of Logistics and Purchasing (CFLP), by 2025, emerging positions such as intelligent scheduling algorithm engineers will face a shortage of approximately 437,000 personnel, while drone pilots will be under-supplied by 453,000, underscoring the scale of the skills gap .

The shortage is particularly acute for high-tech and AI-integrated logistics operations, where technical understanding must be paired with operational management capabilities. Even as automation projects expand across China, the lack of adequately trained engineers, robotics technicians, and system operators creates a bottleneck that slows deployment, increases operational risk, and limits throughput efficiency. The skills gap affects both metropolitan and regional logistics hubs, constraining companies from fully leveraging automation technologies despite available capital and infrastructure.

This structural challenge is expected to persist into the medium term, as traditional workforce training programs are insufficient to meet the rapidly growing demand for advanced logistics and automation expertise. The CFLP highlights that current talent cultivation and supply models are unable to satisfy the industry’s technical personnel needs, creating a tangible barrier to scaling warehouse automation nationwide. Consequently, workforce limitations remain a key inhibitor to accelerated adoption and operational optimization in China’s warehouse automation market.

China Warehouse Automation Market (2026-32) Segmentation Analysis:

The China Warehouse Automation Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Component:

- Hardware

- Software

- Services

The hardware segment dominates the China warehouse automation market, accounting for around 46% of the market size, because it constitutes the essential physical infrastructure required for automated logistics operations across diverse warehouse environments. Physical components such as autonomous mobile robots (AMRs), automated storage and retrieval systems (AS/RS), sortation lines, conveyors, and robotic picking units are foundational to end‑to‑end automation, enabling material movement, storage, and handling at scale that software and services alone cannot deliver. This essential role gives hardware a structural advantage over software and services segments, as physical equipment installations directly translate to deployment volume and revenue.

This trend is exemplified by the increasing deployment of AMRs and robotic systems in China’s logistics landscape. Quicktron Robotics, for instance, deployed its QuickBin robotic picking solution at Tianjin SLC’s medical device warehouse, automating inbound, outbound, inventory, and sorting operations, demonstrating tangible productivity gains . Additionally, in 2025, the company showcased its QuickMix integrated goods-handling suite, combining tote‑to‑person, shelf‑to‑person, and pallet‑to‑person systems, reflecting the ongoing innovation and adoption of robotics hardware in large-scale warehouses across China .

These deployments illustrate how hardware drives operational performance and market expansion simultaneously. By enabling high-density storage, faster picking cycles, and scalable throughput, AMRs, AS/RS systems, and related equipment create measurable efficiency improvements that are unattainable with software-only solutions. The combination of critical physical infrastructure, continuous hardware innovation, and large-scale deployment positions the hardware segment as the dominant revenue contributor in China’s warehouse automation market.

Based on End Use Industry:

- Retail & E-commerce

- Logistics Service Providers (3PL / 4PL)

- Manufacturing

- Food & Beverage

- Healthcare & Pharmaceuticals

- Automotive & Industrial

- Electronics & High-Tech

- Cold Chain Specialists

- Government / Defense Logistics

- Warehouse Property Developers

The retail and e‑commerce sector dominates the China warehouse automation industry, holding around 36% market share, because it represents the largest and most dynamic source of sustained warehouse throughput demand across the logistics ecosystem. Retail and e‑commerce fulfillment requires handling extremely high SKU counts, rapid order cycles, and frequent peak periods driven by consumer purchasing behavior, creating a persistent need for automated storage, picking, sorting, and dispatch solutions that can operate reliably at scale. This volume‑driven demand structurally favors the retail and e‑commerce segment over industrial, commercial, or institutional users, whose fulfillment patterns are typically less frequent and more predictable.

In China, the expansion of online retail has continued to outpace traditional consumption channels, with digital commerce deeply integrated into everyday purchasing through platforms such as Taobao, JD.com, and Pinduoduo. This e‑commerce prevalence leads to massive fulfillment volumes year‑round, punctuated by major promotional events that drive order spikes, necessitating scalable, high‑capacity warehouse automation systems to maintain service levels and delivery speed. The persistent requirement to reduce lead times and improve order accuracy reinforces automation investments within this segment, contributing to its dominant market share.

Additionally, the economies of scale within retail and e‑commerce fulfillment further entrench its leadership in the warehouse automation market. High-order densities and frequent throughput cycles improve the utilization rates of automated hardware and software systems, spreading fixed costs over larger volumes and shortening payback periods on automation investments. Combined with continuous inventory turnover and rapid SKU flow, these characteristics make the retail and e‑commerce segment a consistent driver of demand for advanced warehouse automation technologies, solidifying its position as the largest end‑use industry contributor to market growth.

Gain a Competitive Edge with Our China Warehouse Automation Market Report:

- China Warehouse Automation Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- China Warehouse Automation Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- China Warehouse Automation Market Policies, Regulations, and Product Standards

- China Warehouse Automation Market Trends & Developments

- China Warehouse Automation Market Dynamics

- Growth Factors

- Challenges

- China Warehouse Automation Market Hotspot & Opportunities

- China Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Component- Market Size & Forecast 2022-2032, USD Million

- Hardware

- Robots (AMRs, AGVs, SCARA/Delta Arms)

- Conveyors & Sorters

- AS/RS Cranes & Shuttles

- Sensors & Scanners

- PLC / Controls

- Software

- WMS / Warehouse Execution Software

- Warehouse Control Systems

- Fleet / Robot Orchestration

- Analytics & Optimization

- Services

- Installation & Integration

- Maintenance & Support

- Training & Consulting

- Custom Engineering

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- Automated Storage and Retrieval Systems (AS/RS)

- Autonomous Mobile Robots (AMRs)

- Automated Guided Vehicles (AGVs)

- Conveyor & Sortation Systems

- Robotic Picking & Palletizing

- Automated Packing & Labeling

- Warehouse Management Systems (WMS / WES / WCS)

- Automated Identification Systems (RFID / Barcode / Vision)

- Automated Packaging Systems

- Drones & Vision Inspection Automation

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- Small Warehouses (Below 10,000 sq. meters)

- Medium Warehouses (10,000–50,000 sq. meters)

- Large Warehouses (Above 50,000 sq. meters)

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Retail & E-commerce

- Logistics Service Providers (3PL / 4PL)

- Manufacturing

- Food & Beverage

- Healthcare & Pharmaceuticals

- Automotive & Industrial

- Electronics & High-Tech

- Cold Chain Specialists

- Government / Defense Logistics

- Warehouse Property Developers

- By Region - Market Size & Forecast 2022-2032, USD Million

- East China

- South China

- North China

- Central China

- North-East China

- South-West China

- By Company

- Competition Characteristics

- Market Share & Analysis

- Market Size & Outlook

- China Hardware Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Software Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Services Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Warehouse Automation Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Hikrobot

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Geekplus Technology Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quicktron Intelligent Technology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hai Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Intralox (Shanghai) Automation Equipment Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dematic (KION Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell Intelligrated

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Swisslog (Waldner Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SIASUN Robot & Automation Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BPS Global Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shanghai Jingxing Storage Equipment Engineering Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vanderlande Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SSI Schaefer

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Knapp AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Murata Machinery

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hikrobot

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now