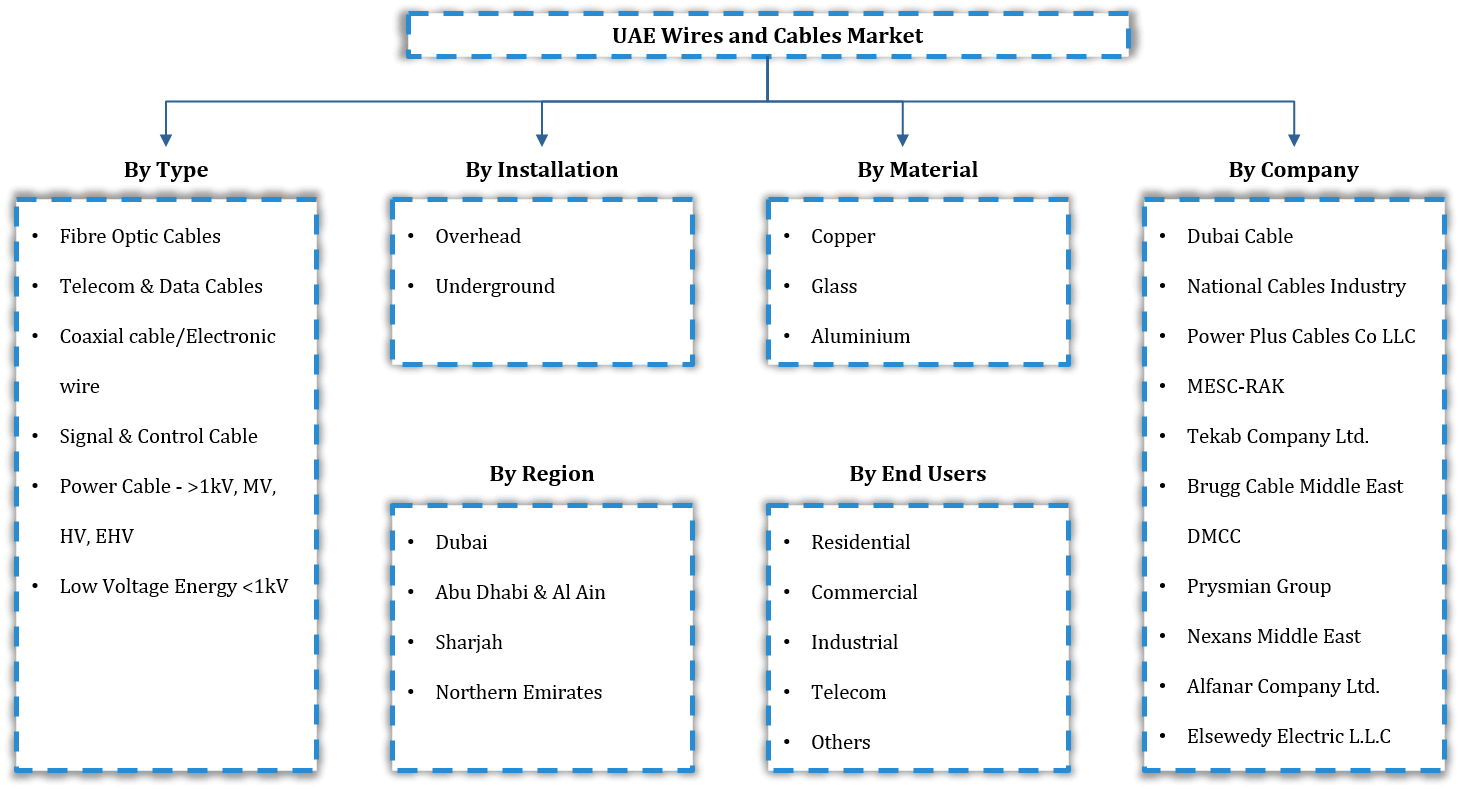

By Product Type (Electronic Wires, Power Cables, Control & Instrumentation Cables, Communication Cables, Flexible & Specialty Cables), By Voltage (Low Voltage, Medium Voltage, High...... Voltage, Extra High Voltage), By Installation (Overhead, Underground), By Material (Copper, Glass, Aluminium), By End User (Energy & power utilities, Building & construction, IT & telecommunications, Automotive & transportation, Oil & gas, Industrial manufacturing, Aerospace & defense), and others Read more

- Energy

- May 2026

- 140

- PDF, Excel, PPT

UAE Wires and Cables Market Key Takeaways

- The United Arab Emirates wires and cables market was valued at USD 1.15 billion in 2025 and is projected to grow from USD 1.22 billion in 2026 to USD 1.70 billion by 2032, registering a CAGR of 5.69% during 2026–2032.

- By installation type, the overhead segment holds a significant market share of approximately 58%, supported by its widespread deployment across power transmission and distribution infrastructure projects.

- By end user, the building & construction segment accounted for a notable share of nearly 33% in 2026, driven by ongoing urban development, commercial expansion, and large-scale infrastructure investments across the UAE.

- The industry remains moderately fragmented; however, the top five players collectively account for an estimated 45% market share, reflecting the presence of both regional and international manufacturers operating within the market.

UAE Wires and Cables Market Size and Outlook

The United Arab Emirates wires and cables market is expected to grow at a CAGR of around 5.69% during 2026–2032, driven by rapid infrastructure development, expanding smart grid initiatives, increasing investments in power transmission and distribution networks, and ongoing projects supporting the country’s energy transition and urban development strategies.

Continuous urban growth across Dubai, Abu Dhabi, and Sharjah, along with rising electricity demand from construction, utilities, and industrial sectors, is strengthening the requirement for advanced power transmission cables and modern electrical distribution systems.

A key structural driver shaping long-term market growth is the UAE Energy Strategy 2050, which focuses on diversifying the energy mix and accelerating the transition toward clean and sustainable power generation. The strategy emphasizes major investments in grid modernization, renewable integration, and energy efficiency improvements. This shift is directly increasing demand for high-performance cabling solutions, including smart grid cables, high-voltage transmission systems, and energy-efficient wiring networks that support reliable and sustainable infrastructure development.

Further reinforcing this growth landscape, Dubai Electricity and Water Authority (DEWA) has increased the capacity target of the Mohammed bin Rashid Al Maktoum Solar Park by 60%, raising it from 5,000 MW to over 8,000 MW by 2030. This expansion reflects the UAE strong push toward clean energy leadership and large-scale renewable integration. It is significantly boosting demand for high-voltage cables UAE, transmission infrastructure, and intelligent grid connectivity systems required to support solar energy evacuation and AI-enabled operational efficiency.

From a structural perspective, the market is segmented by installation and end-use applications. Overhead systems dominate with nearly 58% share due to cost efficiency, faster deployment, and suitability for long-distance transmission networks. These systems play a critical role in utility-scale power distribution and intercity connectivity, particularly in regions where underground cabling is less feasible or economically viable.

While based on end use, the building and construction segment leads with approximately 33% share, driven by rapid urbanization, smart city development, and continuous expansion of residential and commercial infrastructure. Growing adoption of smart building wiring UAE, energy-efficient systems, and advanced fire-safe cabling solutions is further strengthening demand across modern construction projects.

Overall, the United Arab Emirates wires and cables industry is positioned for sustained growth, with the market projected to expand from USD 1.22 billion in 2026 to USD 1.70 billion by 2032, driven by infrastructure modernization, renewable energy expansion, and increasing deployment of smart technologies. The combined impact of energy transition policies and urban development is reinforcing the role of advanced cabling systems as a foundational component of the UAE’s evolving electrical infrastructure.

UAE Wires and Cables Market Key Indicators

- According to the International Energy Agency, electricity consumption in the UAE increased by 2.8% in 2024 and is projected to expand at nearly 3% annually through 2027. This sustained upward trajectory is directly driving continuous investments in low-voltage distribution cable networks across residential, commercial, and industrial sectors, ensuring reliable power connectivity for new developments and rising load requirements.

- The Barakah Nuclear Energy Plant has achieved full commercial operation with a total capacity of 5.6 GW, supplying nearly 25% of the UAE electricity needs. This baseload generation from Abu Dhabi’s Al Dhafra region requires extensive high-voltage underground and overhead cable infrastructure to transmit stable power to urban load centers, reinforcing long-distance transmission reliability across the national grid.

- ADNOC’s USD 150 billion investment plan is targeting increased oil production capacity of 5 million barrels per day by 2027. This large-scale upstream and downstream expansion is generating strong demand for specialized electrical cables, including medium-voltage power systems, fire-rated instrumentation cables, and submersible pump wiring, all designed to meet stringent AGES technical standards across complex energy operations.

UAE Wires and Cables Market Scope

| Category | Segments |

|---|---|

| By Product Type | Electronic Wires, Power Cables, Control & Instrumentation Cables, Communication Cables, Flexible & Specialty Cables |

| By Voltage | Low Voltage, Medium Voltage, High Voltage, Extra High Voltage |

| By Installation | Overhead, Underground |

| By Material | Copper, Glass, Aluminium |

| By End User | Energy & power utilities, Building & construction, IT & telecommunications, Automotive & transportation, Oil & gas, Industrial manufacturing, Aerospace & defense |

UAE Wires and Cables Market Growth Drivers

Large-Scale Infrastructure Development and Smart City Initiatives

The wires and cables industry in the UAE is witnessing strong momentum driven by large-scale infrastructure development and the accelerated rollout of smart city initiatives across the country. Continuous government investment in urban transformation projects across Dubai, Abu Dhabi, and Sharjah is reshaping residential, commercial, and industrial infrastructure. These developments are increasingly integrating digital systems, energy-efficient designs, and automated building technologies, which require advanced and reliable electrical cabling solutions.

Rising construction of smart residential communities, metro expansions, commercial towers, and utility modernization projects is significantly increasing demand for low-voltage distribution cables, fire-resistant wiring systems, and intelligent building management infrastructure. The focus on safety standards, energy efficiency, and long-term operational reliability is further strengthening the adoption of high-performance cable systems across end-use sectors.

For example, the collaboration between Ducab Group and the Mohammed Bin Rashid Housing Establishment, where advanced cable solutions were supplied for residential developments in Dubai. The project included low-voltage power cables, flexible cables, and fire-resistant wiring systems designed to meet stringent safety and performance requirements in modern housing infrastructure. This reflects the increasing reliance on local manufacturers to support national housing and urban development objectives.

Overall, the UAE sustained infrastructure expansion and smart city transformation strategy are reinforcing demand for technologically advanced cabling systems. This is positioning electrical cables as a critical backbone of urban connectivity, driving long-term growth and innovation in the UAE wires and cables market.

Recent Trends

Integration of Smart and Intelligent Packaging

The UAE wires and cables market is witnessing a strong upward trend driven by the rapid expansion of AI-enabled data centers and next-generation digital infrastructure. Increasing adoption of artificial intelligence, cloud computing, and large-scale digital transformation across government and enterprise sectors is accelerating investments in high-capacity computing facilities. These infrastructure assets require extensive deployment of fiber optic cables and low-voltage power distribution systems to ensure uninterrupted connectivity, high-speed data transfer, and energy-efficient operations.

A major development highlighting this trend is the “Stargate UAE” AI data center project in Abu Dhabi, announced through a global technology alliance led by G42 in partnership with OpenAI, Oracle, NVIDIA, Cisco, and SoftBank. The facility is designed as a 1-gigawatt AI infrastructure cluster forming part of a larger UAE–U.S. AI Campus. The project aims to support hyperscale AI workloads and advanced cloud computing applications, reinforcing the UAE’s position as a global digital hub.

Such large-scale data center ecosystems significantly increase demand for precision-engineered cabling systems capable of handling high-density power loads, ultra-low latency communication, and continuous operational performance. The integration of cybersecurity frameworks, automation systems, and AI-driven analytics further amplifies the need for reliable and high-performance wiring infrastructure.

Furthermore, the expansion of AI data centers is reshaping the cabling landscape, shifting demand toward advanced fiber-based connectivity and high-efficiency electrical systems. This trend is expected to remain a long-term growth driver for the UAE wires and cables market, strengthening its role in global digital infrastructure development.

UAE Wires and Cables Industry Opportunities and Challenges

Volatile Raw Material Prices and Supply Chain Pressures Driving Localization and Value Addition

The UAE wires and cables market faces a significant challenge due to volatility in raw material prices, particularly copper, aluminum, and petrochemical-based insulation materials such as PVC and XLPE. Since these materials account for a major share of total production cost, price fluctuations directly impact profit margins and project costing for manufacturers and contractors. In addition, global supply chain disruptions, shipping delays, and dependency on imported semi-finished components create further pressure on timely project execution, especially in large-scale infrastructure and utility developments.

However, this challenge is simultaneously creating strong opportunities for local manufacturing expansion and supply chain localization within the UAE. Companies are increasingly investing in backward integration, recycling of copper and aluminum, and regional production hubs to reduce import dependency and stabilize input costs. For instance, major manufacturers like Ducab have expanded in-country production capabilities to ensure faster delivery and better cost control for high-voltage and industrial cable projects. Similarly, demand for recycled conductor materials is rising as sustainability and cost efficiency become key procurement priorities in government-led infrastructure projects.

This shift is also encouraging strategic partnerships between global cable producers and regional suppliers, leading to more resilient supply networks and improved pricing stability. As a result, the market is moving toward a more self-reliant and efficiency-driven ecosystem, where localization and material optimization become core competitive advantages.

Segmentation Insights

Overhead Installations Account for the Largest Market Share

The overhead installation contributes approximately 58% share of the overall volume in the UAE Wires and Cables Market, due to its cost efficiency, faster deployment, and suitability for large-scale transmission networks. Overhead cable systems are widely preferred in utility-scale power distribution, especially for connecting substations across long distances where underground installation becomes economically unviable. In the UAE, the continuous expansion of electricity demand from industrial zones, residential developments, and mega infrastructure projects has strengthened reliance on overhead transmission infrastructure. Utilities such as high-capacity grids and desert-region transmission corridors also favor overhead systems due to easier maintenance access and lower fault restoration time.

Additionally, ongoing investments in grid modernization and renewable energy integration, particularly solar power evacuation networks, further support the adoption of overhead lines. Despite urbanization trends, overhead systems remain strategically important in less densely populated and intercity transmission networks, ensuring stable and scalable energy delivery across the emirates. This combination of cost advantage, operational flexibility, and infrastructure expansion continues to reinforce the dominance of the overhead segment in the market landscape. Based on installation, the scope has been segmented into

- Overhead

- Underground

Building & Construction Emerges as the Largest End-Use Segment

The building and construction segment holds approximately 33% share in the UAE wires and cables market, driven by rapid urbanization, large-scale infrastructure projects, and continuous real estate development across residential, commercial, and mixed-use sectors. The UAE construction ecosystem is highly active, supported by government-led initiatives such as smart cities, tourism infrastructure, and mega developments in Dubai and Abu Dhabi. Electrical wiring demand in this segment is primarily driven by internal building electrification, lighting systems, HVAC integration, safety systems, and smart building automation solutions. The increasing adoption of energy-efficient infrastructure and green building standards has further accelerated demand for advanced cable solutions, including fire-resistant and low-smoke wiring systems. High-rise residential towers, commercial complexes, hospitality projects, and public infrastructure developments collectively contribute to sustained cable consumption.

Additionally, rising focus on intelligent building management systems and IoT-enabled infrastructure has increased dependency on structured cabling networks. As construction activity continues to expand across urban and industrial zones, this segment remains a key consumption driver for electrical cables, ensuring steady long-term demand growth. The key end users mapped in the study involve:

- Energy & power utilities

- Building & construction

- IT & telecommunications

- Automotive & transportation

- Oil & gas

- Industrial manufacturing

- Aerospace & defense

UAE Wires and Cables Industry Competitive Analysis

The UAE Wires and Cables Market remains moderately consolidated, with a mix of global and regional manufacturers operating across power, construction, and industrial cable segments. The top five companies, including Prysmian Group, Nexans Middle East, Elsewedy Electric, Alfanar Company, and Dubai Cable Company, collectively account for approximately 45% of the total market share, reflecting a competitive structure driven by project-based demand and strong infrastructure development activity.

Major Companies in the Wires and Cables Industry

- Dubai Cable

- National Cables Industry

- Power Plus Cables Co LLC

- Middle East Specialized Cables (MESC-RAK)

- Tekab Company Ltd.

- Prysmian Group

- Nexans Middle East

- Elsewedy Electric

- Alfanar Company

- Brugg Cable Middle East DMCC

- Others

UAE Wires and Cables Industry News and Recent Developments

September 2025: Ducab Group Expands Regional Footprint with Acquisition of Oman’s National Cable Factory

Ducab Group has acquired Oman’s National Cable Factory (NCF) in Salalah to strengthen its regional manufacturing base and expand its presence in the GCC cable industry. The move enhances production capacity for low, medium, and high-voltage cables while supporting infrastructure and energy projects across Oman and the wider Gulf region. The factory also serves key utility and industrial sectors.

Impact Analysis: The acquisition significantly strengthens Ducab’s regional supply chain integration and improves its ability to meet rising demand from infrastructure, oil & gas, and utility projects. By leveraging Oman’s strategic location and existing manufacturing capabilities, Ducab can reduce lead times, improve export efficiency, and enhance cost competitiveness. It also supports Oman’s industrial diversification goals while reinforcing UAE-Oman trade collaboration, positioning Ducab as a stronger regional leader in the wires and cables market.

November 2025: DU Launches UAE–Kenya Segment of PEACE Cable System to Strengthen Global Connectivity

du, in partnership with PEACE Cable International Network, has launched a new UAE–Kenya segment under the PEACE Cable System. The development enhances direct digital connectivity between the Middle East and Africa, improving data transmission speed, latency, and network resilience. The project strengthens the UAE’s position as a global connectivity hub supporting cloud services, AI infrastructure, and digital communication networks

Impact Analysis: The UAE–Kenya subsea cable segment significantly strengthens international bandwidth capacity and supports rising demand from data centers, cloud computing, and AI-driven applications. It improves route diversity and reduces dependency on existing traffic corridors, enhancing overall network reliability. For the UAE cables market, this increases demand for high-performance fiber optic and submarine cable systems, while also reinforcing the country’s role as a strategic digital gateway connecting Asia, Africa, and Europe.

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- UAE Wires and Cables Market Policies, Regulations, and Product Standards

- UAE Wires and Cables Market Trends & Developments

- UAE Wires and Cables Market Dynamics

- Growth Factors

- Challenges

- UAE Wires and Cables Market Hotspot & Opportunities

- UAE Wires and Cables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Thousand Tons)

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Electronic Wires

- Power Cables

- Control & Instrumentation Cables

- Communication Cables

- Flexible & Specialty Cables

- By Voltage- Market Size & Forecast 2022-2032, USD Million

- Low Voltage

- Medium Voltage

- High Voltage

- Extra High Voltage

- By Installation- Market Size & Forecast 2022-2032, USD Million

- Overhead

- Underground

- By Material- Market Size & Forecast 2022-2032, USD Million

- Copper

- Glass

- Aluminium

- By End User- Market Size & Forecast 2022-2032, USD Million

- Energy & power utilities

- Building & construction

- IT & telecommunications

- Automotive & transportation

- Oil & gas

- Industrial manufacturing

- Aerospace & defense

- By Region- Market Size & Forecast 2022-2032, USD Million

- Dubai

- Abu Dhabi & Al Ain

- Sharjah & Northern Emirates

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Overhead Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Thousand Tons)

- Market Share & Outlook

- By Voltage- Market Size & Forecast 2022-2032, USD Million

- By Installation- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Underground Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold (Thousand Tons)

- Market Share & Outlook

- By Voltage- Market Size & Forecast 2022-2032, USD Million

- By Installation- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Wires and Cables Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Dubai Cable

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Cables Industry

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Power Plus Cables Co LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Middle East Specialized Cables (MESC-RAK)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tekab Company Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prysmian Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nexans Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Elsewedy Electric

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfanar Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Brugg Cable Middle East DMCC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Dubai Cable

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

FILL THE FORM TO GET THE FREE SAMPLE PAGES

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now