Europe Vehicle Leasing Market Research Report: Forecast (2026-2032)

Europe Vehicle Leasing Market - By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs), Hybrid Vehicles), By D ... uration (Short-Term (Less than 12 months), Medium-Term (13–36 months), Long-Term (More than 36 months), By Propulsion Type (Internal Combustion Engine (ICE), Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicles (HEVs), Alternative Fuels (CNG, LNG, Hydrogen, etc.), By Mode of Booking (Online, Offline), By End-User (Corporate Enterprises, Small & Medium Enterprises (SMEs), Individual Consumers, Government & Public Sector, Fleet Management Companies, Logistics & Transportation Companies, Tourism & Hospitality Operators, Delivery & Last-Mile Service Providers, Others), and others Read more

- Automotive

- Jan 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Europe Vehicle Leasing Market

Projected 5.76% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 141.70 Billion

Market Size (2032)

USD 209.71 Billion

Base Year

2025

Projected CAGR

5.76%

Leading Segments

By End-User: Corporate Enterprises

Europe Vehicle Leasing Market Report Key Takeaways:

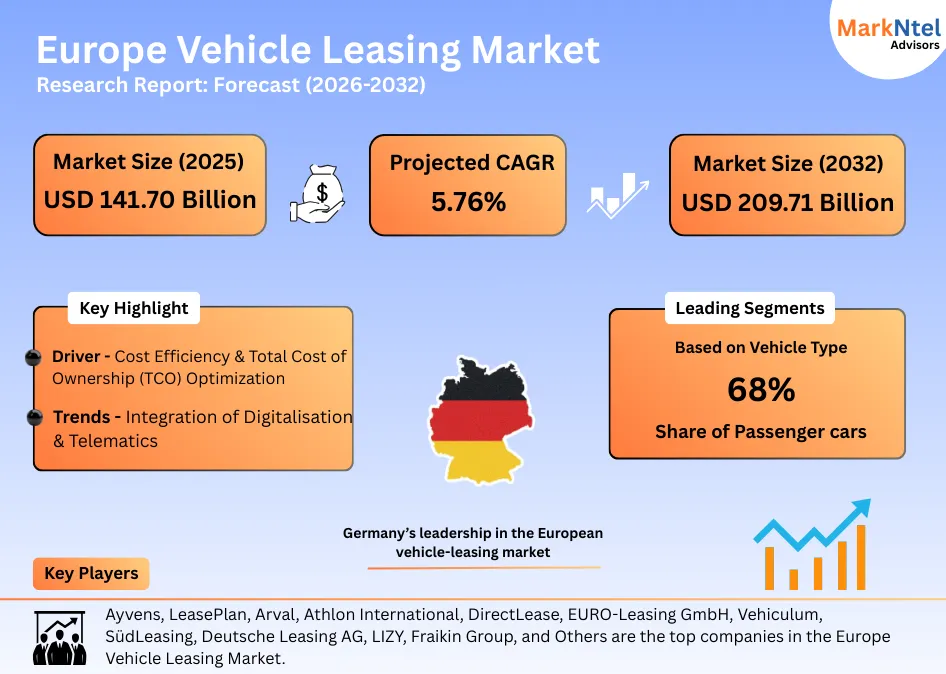

- Market size was valued at around USD141.70 billion in 2025 and is projected to reach USD209.71 billion by 2032. The estimated CAGR from 2026 to 2032 is around 5.76%, indicating strong growth.

- By Country, Germany is dominating this market with around 25% market share in 2025.

- By Vehicle Type, the Passenger Cars represented a significant share of about 68% in the Europe Vehicle Leasing Market in 2025.

- By End-User, the Corporate Enterprises segment represented a major share of nearly 45% of the Europe Vehicle Leasing Market in 2025.

- Leading Vehicle Leasing in Europe are Ayvens, LeasePlan, Arval, Athlon International, DirectLease, EURO-Leasing GmbH, Vehiculum, SüdLeasing, Deutsche Leasing AG, LIZY, Fraikin Group, and Others.

Market Insights & Analysis: Europe Vehicle Leasing Market (2026-32):

The Europe Vehicle Leasing Market size was valued at around USD141.70 billion in 2025 and is projected to reach USD209.71 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.76% during the forecast period, i.e., 2026-32.

The European vehicle leasing market is evolving into a structurally essential mobility model, driven by the combined effects of cost inflation, regulation, electrification, and industry scale-up. As a direct result, capital-intensive vehicle ownership has become less attractive, accelerating the shift toward leasing as a cost-smoothing and risk-management solution.

For instance, EU new passenger-car registrations increased by about 1.4% year-on-year in 2025, showing that mobility demand remains resilient despite elevated prices. Consequently, leasing providers benefit from stable fleet renewal volumes, while customers secure predictable monthly costs and avoid balance-sheet strain. Additionally, Europe’s rapid electrification is reinforcing leasing demand. For reference, battery-electric vehicles represented around 23% of new EU registrations by November 2025, intensifying the need for leasing structures that absorb battery, technology, and resale uncertainty.

Similarly, consolidation is reshaping market dynamics. The creation of Ayvens through the integration of ALD Automotive and LeasePlan has strengthened scale advantages in vehicle procurement, digital fleet platforms, and remarketing efficiency. Likewise, although ECB policy rates stabilized toward the end of 2025, the persistently higher financing-cost environment continues to pressure margins, forcing lessors to optimize asset utilization and pricing discipline.

Taken together, rising vehicle prices, steady demand, accelerating EV penetration, consolidation, and tighter financial conditions point to an outlook where digital capability, telematics integration, and capital efficiency will increasingly determine competitive success in Europe’s vehicle leasing market.

Europe Vehicle Leasing Market Recent Developments:

- 2025: Ayvens was launched as the new brand integrating ALD Automotive and LeasePlan in Germany and Europe in 2025, operating ~3.4 million vehicles and emphasizing sustainability and digitalisation.

- 2025: Arval entered exclusive talks with Mercedes-Benz Group to acquire Athlon, aiming to create an approximately 2.3 million vehicle leasing leader, with completion expected in 2026.

Europe Vehicle Leasing Market Scope:

| Category | Segments |

|---|---|

| By Vehicle Type | Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs), Hybrid Vehicles |

| By Duration | Short-Term (Less than 12 months), Medium-Term (13–36 months), Long-Term (More than 36 months |

| By Propulsion Type | Internal Combustion Engine (ICE), Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicles (HEVs), Alternative Fuels (CNG, LNG, Hydrogen, etc. |

| By Mode of Booking | Online,Offline |

| By End-User | Corporate Enterprises, Small & Medium Enterprises (SMEs), Individual Consumers, Government & Public Sector, Fleet Management Companies, Logistics & Transportation Companies, Tourism & Hospitality Operators, Delivery & Last-Mile Service Providers, Others), and others |

Europe Vehicle Leasing Market Driver:

Cost Efficiency & Total Cost of Ownership (TCO) Optimization

Cost efficiency is a fundamental driver of the European vehicle leasing market because rising vehicle prices, financing costs, and operating expenses have made ownership increasingly capital-intensive. For instance, the EU Harmonized Index of Consumer Prices for new motor cars reached around 128 index points in 2025. As a result, upfront purchase costs have escalated sharply.

For instance, higher interest rates since 2022 have increased the cost of vehicle loans across Europe, raising monthly repayment burdens for owned fleets. Consequently, leasing becomes more attractive as it converts high upfront and financing costs into predictable monthly payments. Additionally, full-service leasing bundles maintenance, servicing, insurance, and roadside assistance, shielding customers from volatile repair and spare-parts costs that have risen materially since 2021.

Similarly, leasing transfers residual-value risk to the lessor at a time when used-vehicle prices, particularly for EVs, remain uncertain. Likewise, as electric vehicles account for nearly one-fifth of new EU registrations by 2025, leasing allows companies to adopt EVs without bearing battery degradation or resale risk.

Europe Vehicle Leasing Market Trend:

Integration of Digitalisation & Telematics

Digitalisation and telematics integration have become a defining trend in the European vehicle leasing market because real-time vehicle data is shifting how lessors manage fleets, control costs, and protect residual values. For instance, large leasing providers such as LeasePlan, Arval, Deutsche Leasing AG, and Athlon International now embed connected-car telematics into contracts to monitor vehicle health, driver behavior, and energy use throughout the lease term. As a result, they can move from reactive to predictive maintenance, reducing unplanned service events and lowering operating costs.

Additionally, telematics-based analytics are linked to demonstrable improvements in fuel efficiency and uptime, which helps lessors such as Ayvens and LIZY reduce the total cost of fleet ownership and improve customer service.

Similarly, as EV adoption rises, providers including Fraikin Group and SüdLeasing use telematics to track battery performance and charging patterns, which is critical for residual value forecasting. Taken together, telematics integration enhances fleet efficiency and risk management but requires significant investment in IT, cybersecurity, and data governance systems, making digitalisation both a competitive advantage and an operational challenge.

Europe Vehicle Leasing Market Challenges:

Regulatory Fragmentation Hindering Market Growth

Regulatory fragmentation is a direct and persistent challenge for vehicle leasing providers in Europe because leasing economics are shaped primarily by national tax, vehicle, and company-car regulations rather than a single harmonized framework. For instance, the European Union allows each Member State to set its own vehicle registration taxes, annual circulation taxes, and benefit-in-kind rules, resulting in sharply different total lease costs for the same vehicle across countries. As a result, Pan-European lessors cannot standardize pricing models or contract structures.

For instance, vehicle-related taxation per car differs widely across Europe, with high-tax markets such as Belgium and Austria collecting more than USD 2,830–3,050 per vehicle annually, while southern markets collect less than USD 1,415, directly affecting monthly lease rates and fleet affordability. Consequently, leasing providers must redesign pricing, accounting, and residual-value assumptions country by country. Additionally, EV incentives and company-car tax benefits vary significantly. For instance, Germany applies a reduced 0.25%–0.5% benefit-in-kind rate for electric company cars, while other countries rely on purchase grants or fuel-tax advantages instead. Similarly, frequent national policy changes force repeated contract repricing and system updates, thus slowing down the adoption.

Europe Vehicle Leasing Market (2026-32) Segmentation Analysis:

The Europe Vehicle Leasing Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Vehicle Type:

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles (EVs)

- Hybrid Vehicles

Passenger cars dominate the European vehicle leasing industry by holding a market share of around 68% because leasing is structurally aligned with corporate mobility, employee benefit schemes, and high-volume remarketing channels, rather than with goods transportation. Consequently, long-term leasing revenues, maintenance services, and remarketing outcomes are heavily anchored to passenger-car fleets.

Additionally, Europe has a very large and liquid passenger-car base, with around 256 million cars on EU roads, which supports efficient end-of-lease resale and lowers residual-value risk compared with narrower commercial-vehicle segments. Similarly, leasing demand is reinforced by company-car usage, as corporate and rental fleets account for a significant share of vehicles in circulation, many of which are leased passenger cars used for business mobility rather than ownership. Taken together, high corporate usage, strong resale liquidity, portfolio concentration, and scalable fleet management make passenger cars the dominant and most economically attractive segment within Europe’s vehicle leasing market.

Based on End-User:

- Corporate Enterprises

- Small & Medium Enterprises (SMEs)

- Individual Consumers

- Government & Public Sector

- Fleet Management Companies

- Logistics & Transportation Companies

- Tourism & Hospitality Operators

- Delivery & Last-Mile Service Providers

- Others

Corporate Enterprises hold the largest market share of about 45% in the European Vehicle Leasing Market because leasing is structurally aligned with business mobility, cost control, and regulatory compliance, rather than private ownership. For instance, data from the European Automobile Manufacturers’ Association (ACEA) consistently show that company fleets represent the largest single registration channel in the EU, accounting for roughly one-third of new passenger-car registrations in recent years, far exceeding private leasing volumes. As a result, leasing providers design most products, pricing, and service bundles around corporate requirements.

Consequently, long-term operating leases, full-service contracts, and fleet-management solutions are primarily tailored for enterprises rather than individuals. Additionally, corporate leasing enables companies to keep vehicles off balance sheets, stabilize cash flows, and bundle maintenance, insurance, and compliance into predictable monthly costs. Similarly, EU-level emissions regulations and national company-car tax frameworks incentivize frequent fleet renewal, which leasing supports more efficiently than ownership.

Europe Vehicle Leasing Market (2026-32): Regional Projection

Germany’s leadership in the European vehicle-leasing market, with a market share of about 25%, is grounded in exceptional leasing penetration, high investment volumes, and strong fleet demand. For instance, about 26.1% of all equipment investment in Germany is financed through leasing, ranking it alongside the UK as the highest in Europe and signaling deep market integration. Similarly, the German leasing sector recorded approximately USD90 billion in new leasing investments in 2023, reflecting robust growth and capital deployment across automotive and other asset classes.

Similarly, Germany’s corporate-led transition toward electric vehicles strengthens leasing dominance, since most EV registrations occur through company fleets rather than private ownership.

Likewise, advanced fleet-management services, deep bank-lessor integration, and regulatory stability reduce operational risk and improve capital efficiency. Taken together, these interlinked drivers consistently position Germany as the structural anchor of Europe’s vehicle-leasing ecosystem.

Gain a Competitive Edge with Our Europe Vehicle Leasing Market Report:

- Europe Vehicle Leasing Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Vehicle Leasing Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Vehicle Leasing Market Regulations, Policies & Standards

- Europe Vehicle Leasing Market Trends & Developments

- Europe Vehicle Leasing Market Dynamics

- Growth Drivers

- Challenges

- Europe Vehicle Leasing Market Hotspots & Opportunities

- Europe Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles (EVs)

- Hybrid Vehicles

- By Duration- (USD Million)

- Short-Term (Less than 12 months)

- Medium-Term (13–36 months)

- Long-Term (More than 36 months)

- By Propulsion Type- (USD Million)

- Internal Combustion Engine (ICE)

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Hybrid Electric Vehicles (HEVs)

- Alternative Fuels (CNG, LNG, Hydrogen, etc.)

- By Mode of Booking- (USD Million)

- Online

- Offline

- By End-User- (USD Million)

- Corporate Enterprises

- Small & Medium Enterprises (SMEs)

- Individual Consumers

- Government & Public Sector

- Fleet Management Companies

- Logistics & Transportation Companies

- Tourism & Hospitality Operators

- Delivery & Last-Mile Service Providers

- Others

- By Country

- UK

- Germany

- France

- Italy

- Spain

- Netherlands

- Poland

- Rest of Europe

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- Market Size & Analysis

- UK Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- Germany Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- France Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- Italy Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- Spain Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- Netherlands Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- Poland Vehicle Leasing Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Vehicle Type- (USD Million)

- By Duration- (USD Million)

- By Propulsion Type- (USD Million)

- By Mode of Booking- (USD Million)

- By End-User- (USD Million)

- Market Size & Analysis

- Europe Vehicle Leasing Market Key Strategic Imperatives for Growth & Success

- Competitive Outlook

- Company Profiles

- Ayvens

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- LeasePlan

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Arval

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Athlon International

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- DirectLease

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- EURO-Leasing GmbH

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Vehiculum

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- SüdLeasing

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Deutsche Leasing AG

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- LIZY

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Fraikin Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Ayvens

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now