UAE Energy Drinks Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Hypertonic Drinks, Isotonic Drinks, Hypotonic Drinks), By Flavored (Flavored, Unflavored), By Sugar Content (Sugar-Free, Non Sugar-Free), By Target Consumer (Teena ... gers, Adults, Geriatric Population), By Packaging Type (Metal Cans, Bottles (PET Bottles), Bottles (Glass Bottles), Others), By Distribution Channel (Offline Channel, Online Channel), and others Read more

- Food & Beverages

- Feb 2026

- Pages 145

- Report Format: PDF, Excel, PPT

UAE Energy Drinks Market

Projected 4.66% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 1.05 Billion

Market Size (2032)

USD 1.38 Billion

Base Year

2025

Projected CAGR

4.66%

Leading Segments

By Product Type: Isotonic Drinks

UAE Energy Drinks Market Report Key Takeaways:

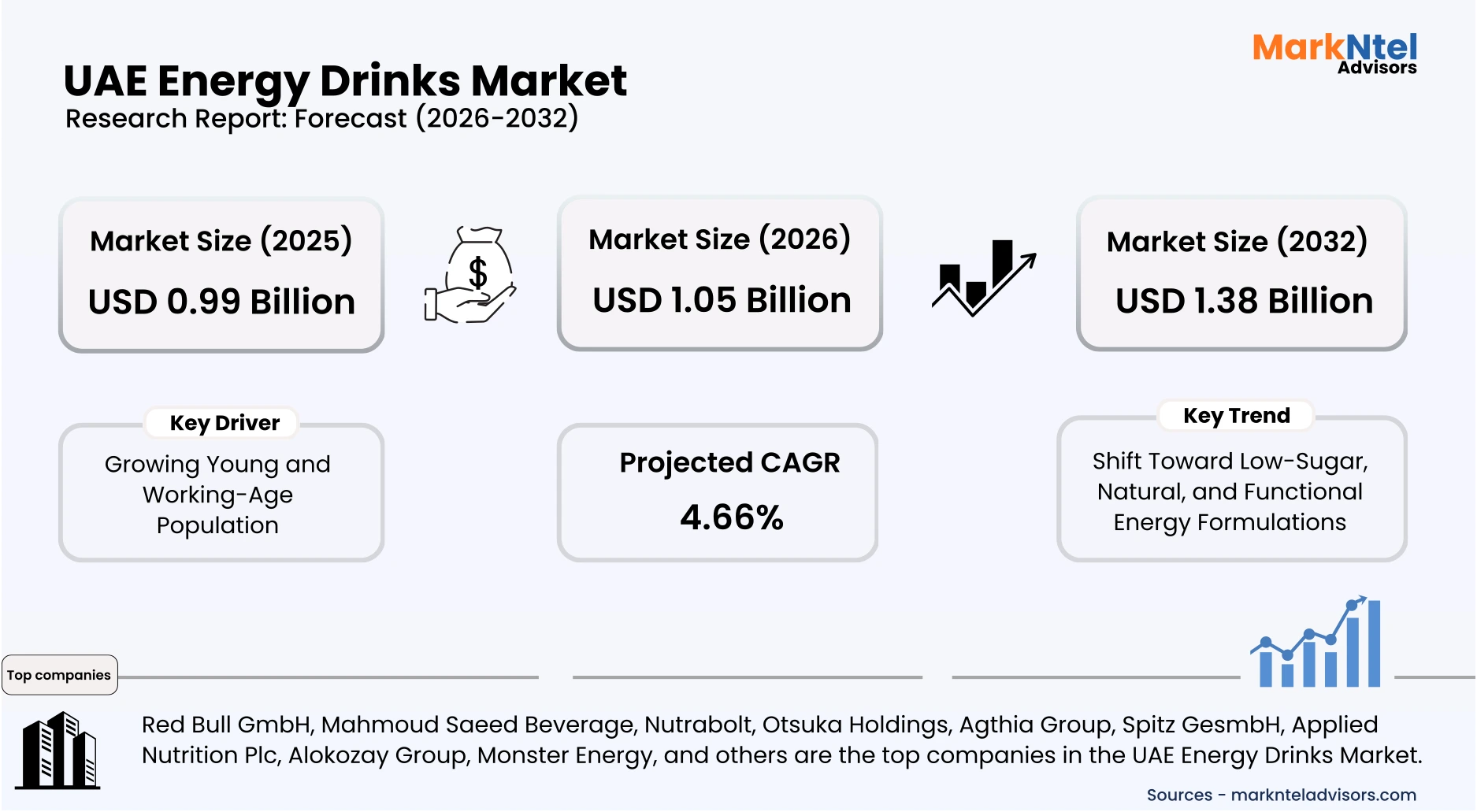

- The UAE Energy Drinks Market size was valued at around USD 0.99 billion in 2025 and is projected grow from USD 1.05 billion in 2026 to USD 1.38 billion by 2032, exhibiting a CAGR of 4.66% during the forecast period.

- Dubai holds the largest market share of about 45% in the UAE Energy Drinks Market in 2026.

- By Product Type, the Isotonic Drinks segment represented a significant share of about 52% in the UAE Energy Drinks Market in 2026.

- By Distribution Channel, the Offline Channel segment presented a significant share of about 74% in the UAE Energy Drinks Market in 2026.

- Leading Energy Drinks companies in the UAE Market are Red Bull GmbH, Mahmoud Saeed Beverage, Nutrabolt, Otsuka Holdings, Agthia Group, Spitz GesmbH, Applied Nutrition Plc, Alokozay Group, Monster Energy, and Others.

Market Insights & Analysis: UAE Energy Drinks Market (2026-32):

The UAE Energy Drinks Market size was valued at around USD 0.99 billion in 2025 and is projected grow from USD 1.05 billion in 2026 to USD 1.38 billion by 2032, exhibiting a CAGR of 4.66% during the forecast period, i.e., 2026-32.

The United Arab Emirates market for energy drinks benefits from a young, working-age population and continued population growth, providing a large base of active consumers attracted to functional and convenience beverages; official population data show roughly 10.99 million residents in 2024, with continued growth into 2025, and employment ratios remain high, supporting retail demand. These demographic fundamentals underpin everyday and leisure consumption across urban centers and tourist hubs, sustaining baseline volume for energy and performance beverages.

Recent fiscal and regulatory actions have materially reshaped industry economics and product strategy, led by the Ministry of Finance amendments that introduced a tiered, sugar-based volumetric excise model for sweetened beverages effective in 2026 while the Federal Tax Authority has confirmed that energy drinks remain subject to a specific 100% excise treatment; together these measures incentivize reformulation, influence shelf pricing, and guide portfolio shifts toward lower-sugar and clearer-label products .

Economic diversification and retail modernization amplify distribution and institutional demand official multilateral forecasts and UAE national accounts point to positive GDP growth in 2025–2026, supporting consumer spending and retail expansion, while public health initiatives from the Ministry of Health & Prevention encourage reduced sugar intake and awareness programmes that reshape consumer preferences; gyms, hospitality outlets and convenience retail therefore act as steady commercial channels complementing household purchases .

Industry responses and forward prospects are focused on reformulation, supply resilience, and sustainability to capture evolving demand. Official guidance and tax implementation materials set compliance and pricing norms that suppliers are adapting to through product reformulation, local import-processing strategies, and packaging commitments, while government tax and trade notices provide transitional rules for excise accounting and taxable-person obligations . These aligned policy, demographic, and retail dynamics support a positive outlook for diversified energy drink portfolios through 2026 and beyond.

UAE Energy Drinks Market Recent Developments:

- 2025: Gorilla Energy rolled out its product portfolio across the UAE with three signature flavors: Ultimate Energy, Mango Coconut, and Watermelon available via Noon and other outlets, marking a significant national retail launch.

- 2025: Cloud 9, an India-based energy drink brand, expanded into the UAE market through a strategic partnership with local distributor MKS and exporter UNBX, marking its entry into the Middle East. The company introduced multiple variants, including Classic, Berry, and Apple flavors, with distribution planned across retail outlets, cafés, and hospitality channels in the UAE. This expansion reflects the growing demand for energy and functional beverages in the region and highlights increasing participation from emerging brands seeking to capitalize on the UAE’s dynamic and high-consumption beverage market.

UAE Energy Drinks Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Hypertonic Drinks, Isotonic Drinks, Hypotonic Drinks), |

| By Flavored | (Flavored, Unflavored), |

| By Sugar Content | (Sugar-Free, Non Sugar-Free), |

| By Target Consumer | (Teenagers, Adults, Geriatric Population), |

| By Packaging Type | (Metal Cans, Bottles (PET Bottles), Bottles (Glass Bottles), Others), |

| By Distribution Channel | (Offline Channel, Online Channel), |

UAE Energy Drinks Market Driver:

Growing Young and Working-Age Population

The expansion of the UAE’s young and working-age population represents the most structurally significant driver of energy drink demand. According to the United Nations World Population Prospects 2024, approximately 84% of the UAE’s population falls within the 15–64 age bracket, reflecting one of the highest working-age ratios globally . The World Bank estimates the total population exceeded 10.1 million in 2024 and continued rising into 2025, supported by sustained expatriate workforce inflows. This demographic composition creates a structurally large consumer base with a higher propensity for convenience and functional beverages .

The intensification of this driver is linked to continued labor market expansion in services, logistics, construction, aviation, and hospitality sectors officially prioritized under the UAE’s national development strategies. Government labor statistics show high labor force participation rates among residents aged 20–49, the primary consuming cohort for stimulant and performance beverages. A 2024 peer-reviewed study published in the Journal of Nutrition and Metabolism examining UAE university populations confirmed widespread energy drink consumption among young adults, reinforcing behavioral evidence of demand concentration. These consumption patterns are structurally embedded rather than temporary .

This demographic scale translates directly into higher market volume rather than merely influencing pricing. A large, economically active population generates recurring daily consumption occasions through work schedules, fitness participation, and shift-based employment. Unlike cyclical drivers, population expansion increases the absolute number of consumers year over year, sustaining baseline demand across residential, commercial, and institutional channels. As expatriate inflows continue and workforce participation remains elevated, the UAE Energy Drinks Market benefits from durable volume growth anchored in demographic fundamentals.

UAE Energy Drinks Market Trend:

Shift Toward Low-Sugar, Natural, and Functional Energy Formulations

The most significant structural trend in the UAE energy drinks market is the shift toward low-sugar, natural, and functionally enhanced formulations. This transition has accelerated as UAE health authorities intensified public nutrition campaigns under the National Strategy for Wellbeing 2031 and the 2025 National Policy for Promoting Healthy Lifestyles. The Ministry of Health and Prevention has expanded front-of-pack labeling guidance and public awareness initiatives highlighting excessive sugar intake risks. Concurrently, peer-reviewed regional studies published in 2024–2025 report rising consumer preference for reduced-sugar beverages among young adults.

This health-driven shift is restructuring the value chain, compelling manufacturers to reformulate products with natural caffeine sources, B-vitamins, electrolytes, and botanical extracts. Global brands such as Red Bull and Monster Beverage Corporation have expanded zero-sugar and functional lines across Gulf retail channels, and in December 2025, Monster announced the early 2026 launch of FLRT, a zero-sugar, female-focused energy drink containing 200 mg of caffeine per 12-ounce can, reinforcing targeted sugar-free innovation. Retailers are reallocating shelf space toward sugar-free variants, while gyms and wellness platforms increasingly stock functional energy beverages. Ingredient sourcing is also evolving toward plant-based stimulants and clean-label additives to align with transparency expectations.

Notably, in 2025, an UAE entrepreneur is developing energy drinks derived entirely from date pits, underscoring localized innovation in natural and sustainable formulations . The persistence of this trend is reinforced by sustained government health initiatives and measurable shifts in consumer purchasing behavior toward lower-calorie beverages. UAE federal nutrition awareness campaigns continue through 2026, embedding healthier consumption norms across youth and working populations. Functional positioning now differentiates brands in a saturated marketplace, influencing long-term innovation pipelines and marketing strategies. As wellness integration deepens across.

UAE Energy Drinks Market Opportunity:

Expansion into Functional & Healthy Variants

A compelling structural opportunity in the UAE energy drinks market lies in partnerships with fitness, sports, and lifestyle ecosystems to create experiential marketing platforms. This opportunity exists due to the UAE government’s sustained investment in physical activity initiatives under the National Sports Strategy 2031 and Dubai Fitness Challenge 2025, which recorded millions of participants across community events. The Ministry of Community Development and Dubai Sports Council continue to promote mass participation sports programs, increasing organized fitness engagement. These initiatives structurally expand access points where performance beverages align naturally with consumer intent and usage occasions.

This ecosystem expansion translates directly into demand as higher participation in gyms, endurance events, and wellness programs increases functional beverage consumption linked to performance and recovery. Official Dubai Fitness Challenge reporting confirms sustained year-on-year growth in registered participants through 2025 , reinforcing an expanding active consumer base. Increased visibility of wellness events creates high-conversion sampling environments where consumers trial new products in performance-driven settings. As a result, experiential partnerships convert health engagement into repeat beverage purchases.

The opportunity particularly favors new entrants because fitness ecosystems value differentiated, purpose-driven brands over mass-market incumbents. Smaller players can co-create limited-edition products, sponsor niche sporting events, and integrate directly with gym communities at lower activation costs. Established multinationals often rely on large-scale advertising models, whereas emerging brands can embed themselves within localized wellness networks. This proximity-driven strategy enables scalable growth through community loyalty rather than national media expenditure.

UAE Energy Drinks Market Challenge:

High Excise Tax Burden on Energy Drinks

The UAE energy drinks market operates within a stringent excise framework that imposes a 100% tax under Federal Decree-Law No. 7 of 2017, as administered by the Federal Tax Authority and reaffirmed in updated 2025 compliance guidance. Energy drinks are classified as excise goods due to caffeine and stimulant content, irrespective of sugar levels. Market participants must register with the authority, submit periodic returns, implement digital tax stamps, and comply with warehousing and tracking requirements. These obligations increase administrative burden and significantly elevate upfront working capital requirements for importers and distributors.

The financial implications are substantial, as the 100% excise tax effectively doubles the pre-tax base price before VAT is applied, materially raising shelf prices across retail channels. Federal Tax Authority enforcement provisions include strict penalties for non-compliance and mandatory reporting systems. Furthermore, the Ministry of Finance confirmed that from early 2026, the flat 50% excise tax on sweetened beverages will transition to a graded volumetric model, whereby beverages with higher sugar per 100 ml will be taxed more and lower-sugar drinks will be taxed less, reshaping pricing and reformulation strategies. Smaller distributors face heightened inventory financing pressures due to excise prepayments.

Such a fiscal structure constrains market expansion by compressing operating margins and discouraging entry by capital-limited firms. Excise liabilities must be financed before product sale, increasing liquidity risk and limiting portfolio experimentation. Compliance complexity also reduces cross-border flexibility within the GCC and deters smaller importers from scaling operations. As a result, the excise regime functions as a systemic barrier to innovation, investment appetite, and competitive diversification in the UAE energy drinks sector.

UAE Energy Drinks Market (2026-32) Segmentation Analysis:

The UAE Energy Drinks market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Hypertonic Drinks

- Isotonic Drinks

- Hypotonic Drinks

Isotonic drinks dominate the UAE Energy Drinks Market, accounting for approximately 52% of total product-type demand, primarily because they align closely with the country’s expanding fitness and outdoor activity culture. The UAE government’s National Sports Strategy 2031 and initiatives such as the Dubai Fitness Challenge 2025 have significantly increased participation in endurance sports, gym memberships, and community fitness events. Isotonic formulations are specifically designed to replenish fluids and electrolytes lost through perspiration, making them functionally relevant in the UAE’s high-temperature climate. This physiological suitability directly supports stronger repeat consumption compared to stimulant-heavy alternatives.

Climatic conditions further reinforce category dominance. According to the UAE National Center of Meteorology, summer temperatures frequently exceed 40°C, elevating dehydration risks during outdoor activities. In such an environment, beverages positioned around hydration and electrolyte balance resonate more strongly than high-caffeine energy products. Retail placement strategies in supermarkets and convenience stores increasingly position isotonic drinks within sports and hydration aisles rather than traditional carbonated beverage shelves, reinforcing their functional identity. This cross-positioning broadens their appeal beyond core energy drink consumers to include recreational athletes and wellness-focused residents.

Industrial supply dynamics also contribute to this leadership. Major multinational beverage producers operating in the GCC maintain regional bottling facilities capable of high-volume isotonic production, ensuring distribution depth and competitive pricing. The established sports beverage manufacturing ecosystem allows consistent product availability across hypermarkets, gyms, and sporting venues. While hypertonic and stimulant-based drinks serve niche segments, isotonic products benefit from climate relevance, institutional sports promotion, and scalable production infrastructure, sustaining their 52% market leadership position in the UAE.

Based on Distribution Channel:

- Offline Channel

- Offline Channel

The offline channel dominates the UAE Energy Drinks Market, accounting for approximately 74% of total distribution, primarily because beverage consumption in the country remains highly impulse-driven and convenience-oriented. The UAE Federal Competitiveness and Statistics Centre reports continued growth in retail trade activity through 2024–2025, supported by the expansion of hypermarkets, supermarkets, and neighborhood convenience stores. Energy drinks are commonly purchased in petrol stations, malls, and small grocery outlets where immediate consumption occasions drive transaction volume. This dense physical retail presence sustains higher in-store conversion rates compared to planned online purchases.

Retail infrastructure strength further reinforces this position. Large chains such as Carrefour, Lulu Hypermarket, and Union Coop operate extensive store networks across the emirates, supported by integrated logistics and centralized warehousing. Dubai Economy and Tourism retail updates highlight consistent mall footfall and in-person consumer spending as key contributors to overall FMCG sales. Energy drinks benefit from refrigerated display units, checkout counter placement, and in-store promotional activations, all of which stimulate impulse buying behavior. These merchandising advantages remain structurally stronger in brick-and-mortar environments.

Operational realities also favor offline distribution. Energy drinks require chilled availability and immediate accessibility, particularly given the UAE’s high ambient temperatures. Physical retail ensures cold-chain integrity and rapid stock rotation, preserving product quality and consumer trust. Although e-commerce grocery adoption is rising, online beverage purchases are typically bulk and planned rather than spontaneous. Consequently, the combination of retail density, experiential visibility, and consumption immediacy sustains offline channels as the leading distribution pathway in the UAE.

UAE Energy Drinks Market (2026-32): Regional Projection

Dubai dominates the UAE Energy Drinks Market, accounting for approximately 45% of total national demand, primarily because it represents the country’s largest population and commercial hub. According to the Dubai Statistics Center, Dubai’s population surpassed 3.7 million in 2024, supported by continued expatriate inflows and workforce expansion. This high concentration of working professionals, tourists, and young adults creates sustained demand for convenience beverages, particularly energy drinks associated with fast-paced urban lifestyles. The emirate’s dense retail footprint further amplifies point-of-sale accessibility across malls, petrol stations, and neighborhood outlets.

Tourism and hospitality activities significantly reinforce Dubai’s consumption advantage. Dubai’s Department of Economy and Tourism reported record international visitor arrivals in 2024–2025, strengthening demand across hotels, nightlife venues, and entertainment districts. Energy drinks benefit from late-night consumption patterns and event-driven sales in high-traffic zones such as Downtown Dubai and Dubai Marina. Large-scale sporting events, fitness festivals, and exhibitions hosted at venues like the Dubai World Trade Centre also expand institutional and impulse-based beverage purchases. This event-driven ecosystem structurally elevates beverage turnover relative to other emirates.

Dubai’s logistics and distribution infrastructure further consolidates its leadership position. The emirate serves as the UAE’s primary import and re-export gateway through Jebel Ali Port and major distribution hubs. Beverage manufacturers and distributors often centralize warehousing operations in Dubai to service nationwide retail networks efficiently. This concentration of commercial activity, population density, tourism flows, and supply-chain infrastructure collectively positions Dubai ahead of other regions in overall energy drink consumption and market share.

Gain a Competitive Edge with Our UAE Energy Drinks Market Report:

- UAE Energy Drinks Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- UAE Energy Drinks Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- UAE Energy Drinks Market Policies, Regulations, and Product Standards

- UAE Energy Drinks Market Trends & Developments

- UAE Energy Drinks Market Dynamics

- Growth Factors

- Challenges

- UAE Energy Drinks Market Hotspot & Opportunities

- UAE Energy Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Hypertonic Drinks

- Isotonic Drinks

- Hypotonic Drinks

- By Flavored- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Flavored

- Unflavored

- By Sugar Content- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Sugar-Free

- Non Sugar-Free

- By Target Consumer- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Teenagers

- Adults

- Geriatric Population

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Metal Cans

- Bottles (PET Bottles)

- Bottles (Glass Bottles)

- Others

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Offline Channel

- Hypermarkets / Supermarkets

- Convenience Stores

- Online Channel

- Offline Channel

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- UAE Hypertonic Drinks Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Outlook

- By Flavored- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Sugar Content- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Target Consumer- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- UAE Isotonic Drinks Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Outlook

- By Flavored- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Sugar Content- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Target Consumer- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- UAE Hypotonic Drinks Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Outlook

- By Flavored- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Sugar Content- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Target Consumer- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Region- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- UAE Energy Drinks Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Red Bull GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mahmoud Saeed Beverage

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nutrabolt

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Otsuka Holdings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agthia Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Spitz GesmbH, S

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Applied Nutrition Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alokozay Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Monster Energy

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Red Bull GmbH

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now