UAE Architectural Coatings Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Resin Type (Acrylic, Alkyd, Polyurethane, Epoxy), By Technology (Water-borne Coatings, Solvent-borne Coatings), By End User (Residential, Commercial), and others ... Read more

- Chemicals

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

UAE Architectural Coatings Market

Projected 4.5% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 512.05 Million

Market Size (2032)

USD 666.82 Million

Base Year

2025

Projected CAGR

4.5%

Leading Segments

By End User: Residential

UAE Architectural Coatings Market Report Key Takeaways:

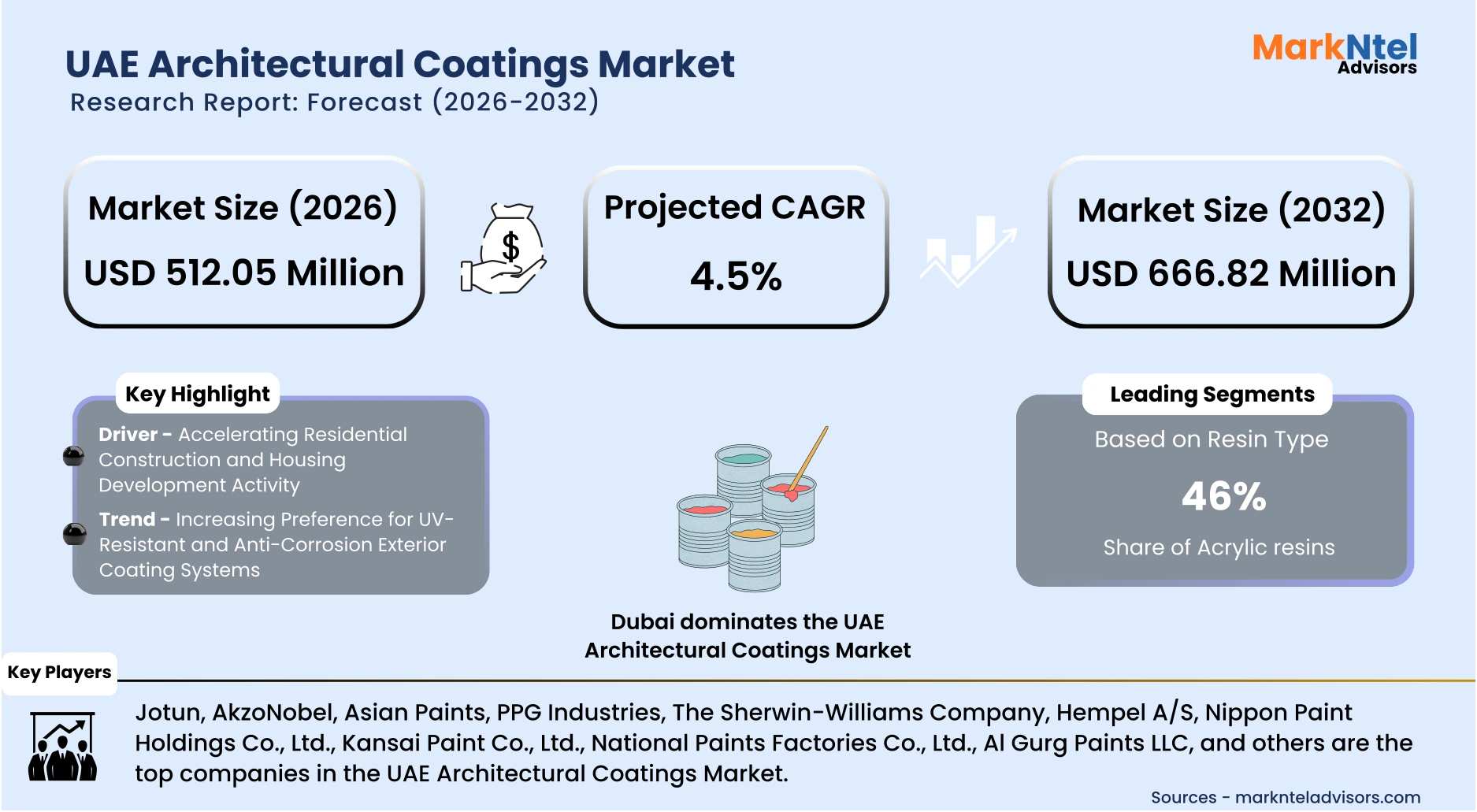

- The UAE Architectural Coatings Market size was valued at around USD 490 million in 2025 and is projected grow from USD 512.05 million in 2026 to USD 666.82 million by 2032, exhibiting a CAGR of 4.5% during the forecast period.

- Dubai holds the largest market share of about 36% in the UAE Architectural Coatings Market in 2026.

- By Resin Type, the Acrylic segment represented a significant share of about 46% in the UAE Architectural Coatings Market in 2026.

- By End User, the Residential segment presented a significant share of about 57% in the UAE Architectural Coatings Market in 2026.

- Leading Architectural Coatings companies in the UAE Market are Jotun, AkzoNobel, Asian Paints, PPG Industries, The Sherwin-Williams Company, Hempel A/S, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., National Paints Factories Co., Ltd., Al Gurg Paints LLC, and Others.

Market Insights & Analysis: UAE Architectural Coatings Market (2026-32):

The UAE Architectural Coatings Market size was valued at around USD 490 million in 2025 and is projected grow from USD 512.05 million in 2026 to USD 666.82 million by 2032, exhibiting a CAGR of 4.5% during the forecast period, i.e., 2026-32.

The UAE Architectural Coatings Market has demonstrated sustained expansion alongside record real estate and construction activity. According to the Dubai Land Department, Dubai’s real estate transactions reached approximately USD 207 billion in 2024 , reflecting historic project launches and handovers. This scale of development directly increases coating consumption, as each newly delivered residential or commercial unit requires interior and exterior paint application. The World Bank also reported non-oil economic growth above 4% in 2024, reinforcing construction financing and infrastructure momentum.

Residential demand remains the primary volume contributor, supported by demographic expansion and structured housing programs. As per the Dubai Statistics Center confirms continued population growth and rising building permits, signaling sustained housing supply. In 2025, the Ministry of Energy and Infrastructure introduced a housing support funding program with insurance coverage extending to age 95, strengthening beneficiary security. Additionally, Abu Dhabi signed agreements worth approximately USD 28.9 billion to develop 13 residential communities delivering over 40,000 homes and plots by 2029.

To enhance affordability, Abu Dhabi introduced a community support subsidy of approximately USD 68,000 deducted from housing loans of up to approximately USD 476,000, alongside extended repayment terms of 30 years. Total housing benefits issued reached approximately USD 4.19 billion, benefiting more than 10,700 citizens . Each completed housing unit generates first-cycle coatings demand across multiple layers, materially expanding volume consumption. Commercial demand remains supported by tourism, with Dubai recording over 17 million international visitors in 2024.

Sustainability regulations further influence product adoption, as the UAE Net Zero 2050 Strategy promotes low-emission construction materials and environmentally compliant coatings. The Central Bank of the UAE reported continued growth in mortgage lending in 2025, supporting property purchases and project continuity. Large master-planned communities and infrastructure upgrades across major emirates are expected to sustain application volumes. Together, economic resilience, housing investments, regulatory alignment, and financing support position the market for steady medium-term expansion driven by structural demand growth.

UAE Architectural Coatings Market Recent Developments:

- 2026 : Caparol announced enhancements to its climate-adapted façade and decorative paint lines tailored to UAE conditions, including expanded sustainable and weather-resistant products. These innovations aim to strengthen performance in the region’s harsh climate and improve indoor air quality for residential and mixed-use developments.

- 2025 : Asian Paints announced the development of its second UAE manufacturing facility through Berger Paints Emirates Ltd Co (LLC) at Khalifa Economic Zones Abu Dhabi (KEZAD). The project involves an investment of approximately USD 38 million and will have an initial production capacity of 55,800 kiloliters per year, strengthening regional supply and supporting Middle East market expansion.

UAE Architectural Coatings Market Scope:

| Category | Segments |

|---|---|

| By Resin Type | (Acrylic, Alkyd, Polyurethane, Epoxy), |

| By Technology | (Water-borne Coatings, Solvent-borne Coatings), |

| By End User | (Residential, Commercial), |

UAE Architectural Coatings Market Driver:

Accelerating Residential Construction and Housing Development Activity

Residential project execution across the UAE has intensified beyond transaction value growth, reflecting tangible increases in unit completions and project pipelines. According to official releases from the Abu Dhabi Media Office in 2025, new community developments are being advanced under structured urban expansion plans to support long-term population capacity. The UAE’s National Housing Strategy framework continues to prioritize citizen housing allocation and infrastructure readiness, reinforcing sustained construction output. This systemic expansion translates into measurable increases in built-up residential floor space across emirates.

The strengthening of off-plan sales absorption rates and developer backlog execution has further amplified construction intensity. Public announcements in 2025 confirmed accelerated project handovers within integrated communities, reflecting improved contractor mobilization and supply chain stability. Unlike speculative land transactions, these developments represent physical housing delivery milestones, which directly translate into coatings application requirements. Additionally, luxury-branded residential developments such as the 43-storey Bugatti Residences in Dubai, with apartments starting at approximately USD 5.2 million and penthouses reportedly sold for up to USD 54 million, further illustrate premium segment expansion within the housing pipeline .

Moreover, Dubai’s property sector entered 2026 with dual momentum, as government data showed record 2025 transactions exceeding approximately USD 142 billion across more than 170,000 deals, rising buyer and seller search activity, and population surpassing 3.8 million, indicating sustained absorption of new housing supply . This driver materially expands market volume because architectural coatings consumption scales proportionally with square meter additions to housing stock. Each villa, townhouse, or apartment requires primer, base coat, and finishing layers before occupancy, generating compulsory material demand. Therefore, accelerated residential delivery functions as a structural demand catalyst, enlarging coatings consumption across the UAE rather than merely influencing pricing or short-term procurement cycles.

UAE Architectural Coatings Market Trend:

Increasing Preference for UV-Resistant and Anti-Corrosion Exterior Coating Systems

The UAE’s extreme climatic conditions have accelerated demand for high-performance exterior coating systems. According to the UAE National Center of Meteorology, summer temperatures frequently exceed 45°C, while coastal humidity and saline exposure intensify material degradation. Prolonged ultraviolet radiation contributes to surface chalking, fading, and cracking in conventional exterior paints. These environmental pressures have structurally shifted specification practices toward UV-resistant acrylics and anti-corrosion systems designed for extended durability.

Rapid urban expansion in coastal cities such as Dubai and Abu Dhabi has further amplified this transition. High-rise residential towers, waterfront developments, and infrastructure assets are increasingly exposed to marine conditions that accelerate reinforcement corrosion and façade deterioration. Municipal maintenance authorities have emphasized lifecycle cost efficiency, encouraging developers to select longer-lasting protective systems. Additionally, in 2025, Adelaide-based Acryloc signed a Dubai distribution agreement to introduce heat-reflective coatings capable of reflecting up to 87% of solar heat, underscoring growing regional demand for advanced exterior performance solutions.

This trend is expected to persist because climatic exposure remains constant and urban density continues to rise. Government-backed infrastructure expansion and coastal master-planned communities will sustain demand for advanced exterior protection technologies. Manufacturers are responding by strengthening portfolios focused on heat-reflective and corrosion-resistant formulations. As lifecycle durability becomes a central procurement criterion, performance-driven exterior coatings are increasingly redefining product standards across the UAE architectural coatings market.

UAE Architectural Coatings Market Opportunity:

Growth in Hospitality and Tourism Infrastructure Projects

The UAE’s hospitality sector expansion presents a compelling opportunity for architectural coatings suppliers. According to the UAE Government’s Tourism Strategy 2031, the country aims to attract 40 million hotel guests annually and increase tourism’s GDP contribution to USD 122 billion by 2031 . In 2025–2026, Dubai and Abu Dhabi continued expanding hotel capacity and leisure districts to support international exhibitions, sporting events, and business tourism. These policy-backed objectives create sustained construction and refurbishment activity across hospitality assets.

This opportunity translates directly into coatings demand through new hotel developments, resort-style communities, and adaptive reuse of commercial spaces. Hospitality projects require premium exterior façade systems, decorative interior finishes, waterproofing layers, and corrosion-resistant applications in coastal zones. Additionally, Dubai announced the USD 1.08 billion Al Layan Oasis eco-tourism development in Al Marmoom, covering one million square meters with integrated leisure, camping, and recreational infrastructure, further expanding tourism-linked construction activity. Moreover, in 2025, Dubai approved a new architectural identity framework dividing the emirate into six zones and launching a multi-phase tunnel beautification program incorporating durable, heat- and humidity-resistant materials, reinforcing demand for high-performance exterior coatings .

The segment is particularly advantageous for new and emerging players because hospitality developers often engage project-based suppliers offering customized finishes and climate-adapted systems. Boutique hotels, mid-scale resorts, and branded leisure projects allow smaller manufacturers to compete on performance and responsiveness rather than distribution scale. This reduces entry barriers compared to mass retail segments. Consequently, tourism-linked infrastructure growth provides a scalable and differentiation-driven entry pathway within the UAE architectural coatings market.

UAE Architectural Coatings Market Challenge:

Volatility in Prices of Raw Material and Resin

Volatility in petrochemical feedstock prices remains the most critical structural challenge for architectural coatings manufacturers. According to the World Bank Commodity Markets Outlook (2025), crude oil prices experienced renewed fluctuations amid geopolitical tensions and supply adjustments, directly influencing downstream petrochemical derivatives. Resins such as acrylics, epoxies, and polyurethanes are derived from oil-based inputs, making coatings producers highly exposed to feedstock instability. This structural dependency links global energy price movements to local manufacturing cost structures.

The International Energy Agency reported continued uncertainty in global oil supply balances through 2025, driven by production cuts and regional conflicts affecting trade flows. In 2026, Brent crude prices fluctuated around USD 70 per barrel amid geopolitical tensions and supply concerns, reinforcing ongoing instability in global energy markets . Such volatility translates into unpredictable resin procurement costs for manufacturers operating in import-dependent markets like the UAE. Established producers often mitigate this risk through long-term supply contracts, whereas smaller firms face spot-market exposure and compressed margins.

The challenge materially restricts market expansion because cost instability complicates pricing strategies and project bidding. Construction contracts in the UAE are typically fixed-price, limiting manufacturers’ ability to pass through sudden input increases. Elevated working capital requirements and inventory risk further constrain scalability for new entrants. Consequently, persistent raw material price volatility acts as a systemic barrier, affecting profitability, investment planning, and long-term capacity expansion within the architectural coatings market.

UAE Architectural Coatings Market (2026-32) Segmentation Analysis:

The UAE Architectural Coatings market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Resin Type:

- Acrylic

- Alkyd

- Polyurethane

- Epoxy

- Other Resins

Acrylic resins dominate the UAE Architectural Coatings Market, accounting for approximately 46% of total demand, primarily because they offer superior resistance to intense ultraviolet exposure and high ambient temperatures. According to the UAE National Center of Meteorology, summer temperatures frequently exceed 45°C, creating harsh exterior conditions that accelerate coating degradation. Acrylic formulations demonstrate strong color retention, flexibility, and resistance to chalking under prolonged solar radiation. This performance profile makes them particularly suitable for façades, villas, and high-rise residential towers exposed to desert climates.

Large-scale residential and mixed-use developments further reinforce acrylic’s dominance due to their compatibility with water-borne systems and ease of application. Dubai Municipality’s Green Building Regulations emphasize environmental performance and indoor air quality standards, encouraging the use of low-VOC, water-based coatings, a segment where acrylic emulsions are widely utilized. Their fast-drying properties and adhesion to concrete substrates align well with the UAE’s high-volume construction cycles. Contractors favor acrylic systems for their balance between durability, cost-efficiency, and regulatory compliance.

Industrial supply capacity also supports acrylic’s leading share. The UAE hosts major petrochemical producers such as Abu Dhabi National Oil Company (ADNOC), which strengthens the regional availability of petrochemical feedstocks used in acrylic production . Compared to epoxy and polyurethane systems, acrylic coatings require lower application complexity and are more adaptable to residential repaint cycles. The combination of climatic suitability, regulatory alignment, and scalable supply infrastructure positions acrylic as the dominant resin category in the UAE architectural coatings market.

Based on End User:

- Residential

- Commercial

The residential segment dominates the UAE Architectural Coatings Market, accounting for approximately 57% of total demand, primarily because sustained population growth and structured housing expansion continue to drive large-scale unit delivery across major emirates. According to official population data released by the Government of Dubai, the emirate’s population surpassed 3.8 million in 2025, increasing long-term housing requirements. Each newly completed villa, townhouse, or apartment requires multiple layers of primer and finish coatings for interiors and exteriors. This recurring first-cycle application volume structurally positions residential construction as the largest coatings-consuming end-use category.

Government-backed housing initiatives further reinforce this dominance. In 2025, Abu Dhabi approved residential development agreements worth approximately USD 28.9 billion to deliver more than 40,000 homes and land plots by 2029. Federal housing support programs overseen by the Ministry of Energy and Infrastructure continue to accelerate approvals for citizen housing projects. These structured public investments translate directly into measurable coating demand, as each housing unit generates mandatory surface protection and decorative finishing requirements.

Additionally, residential repainting cycles contribute significantly to volume consumption. Unlike commercial projects with longer refurbishment intervals, residential properties undergo more frequent maintenance due to climate exposure and aesthetic upgrades. Dubai Municipality’s building regulations emphasize durability and environmental performance in residential construction, increasing specification standards for interior and exterior paints. The combination of demographic expansion, government-led housing supply, and recurring repaint demand structurally positions residential applications as the dominant end-user segment in the UAE architectural coatings market.

UAE Architectural Coatings Market (2026-32): Regional Projection

Dubai dominates the UAE Architectural Coatings Market, accounting for approximately 36% of total demand, primarily because it concentrates the country’s highest level of construction permits, infrastructure upgrades, and urban redevelopment activity. As per Dubai Municipality, the emirate consistently records the largest share of building permits issued nationally, reflecting sustained project initiation across residential, commercial, and mixed-use categories. High-density vertical construction, including super-tall residential towers and mixed-use districts, generates significantly greater façade surface area per project compared to lower-rise developments in other emirates. This structural concentration of buildable floor space directly increases coatings consumption volume.

Dubai’s infrastructure modernization initiatives further reinforce regional dominance. The Roads and Transport Authority announced a multi-phase tunnel beautification program covering 18 major tunnels, incorporating humidity- and heat-resistant wall systems. In addition, the recently approved architectural identity framework divides the city into six distinct urban zones, requiring coordinated façade aesthetics and durable exterior finishes. Moreover, in 2026, Emirates Airlines announced a multi-billion-dirham Cabin Crew Village project at Dubai Investments Park comprising 20 residential towers to accommodate up to 12,000 staff, further expanding large-scale vertical housing construction in the emirate . Additionally, in 2025, premium community redevelopment activity intensified, with renovation investments across areas such as Palm Jumeirah and Emirates Hills reflecting a broader shift toward high-value residential upgrades that further increase repainting and surface refurbishment demand .

The emirate’s role as a regional investment gateway also sustains higher project turnover. Dubai continues to attract foreign direct investment into real estate and urban infrastructure, according to official government investment updates, reinforcing construction continuity. Compared to smaller emirates with more localized project pipelines, Dubai’s diversified development base, spanning luxury residential, retail districts, and transport corridors, creates continuous application cycles. Consequently, its scale of permitted construction, infrastructure beautification programs, institutional housing expansion, premium redevelopment activity, and investment inflows structurally position Dubai as the leading regional contributor to architectural coatings demand in the UAE.

Gain a Competitive Edge with Our UAE Architectural Coatings Market Report:

- UAE Architectural Coatings Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- UAE Architectural Coatings Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- UAE Architectural Coatings Market Policies, Regulations, and Product Standards

- UAE Architectural Coatings Market Trends & Developments

- UAE Architectural Coatings Market Dynamics

- Growth Factors

- Challenges

- UAE Architectural Coatings Market Hotspot & Opportunities

- UAE Architectural Coatings Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity in Tons

- Market Share & Outlook

- By Resin Type- Market Size & Forecast 2022-2032, USD Million & Tons

- Acrylic

- Alkyd

- Polyurethane

- Epoxy

- By Technology- Market Size & Forecast 2022-2032, USD Million & Tons

- Water-borne Coatings

- Solvent-borne Coatings

- By End User- Market Size & Forecast 2022-2032, USD Million & Tons

- Residential

- Commercial

- By Region- Market Size & Forecast 2022-2032, USD Million & Tons

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Resin Type- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- UAE Acrylic Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity in Tons

- Market Share & Outlook

- By Technology- Market Size & Forecast 2022-2032, USD Million & Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- UAE Alkyd Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity in Tons

- Market Share & Outlook

- By Technology- Market Size & Forecast 2022-2032, USD Million & Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- UAE Polyurethane Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity in Tons

- Market Share & Outlook

- By Technology- Market Size & Forecast 2022-2032, USD Million & Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- UAE Epoxy Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity in Tons

- Market Share & Outlook

- By Technology- Market Size & Forecast 2022-2032, USD Million & Tons

- By End User- Market Size & Forecast 2022-2032, USD Million & Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- UAE Architectural Coatings Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Jotun

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AkzoNobel

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asian Paints

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PPG Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Sherwin-Williams Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hempel A/S

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nippon Paint Holdings Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kansai Paint Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Paints Factories Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Gurg Paints LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jotun

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now