Latin America Refinery Catalyst Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Product Type (FCC Catalysts, Hydrotreating Catalysts, Hydrocracking Catalysts, Reforming Catalysts, Alkylation Catalysts, Others), By Ingredient (Zeolites, Metals, Chemical Comp ... ounds, Others), and others Read more

- Chemicals

- Feb 2026

- Pages 245

- Report Format: PDF, Excel, PPT

Latin America Refinery Catalyst Market

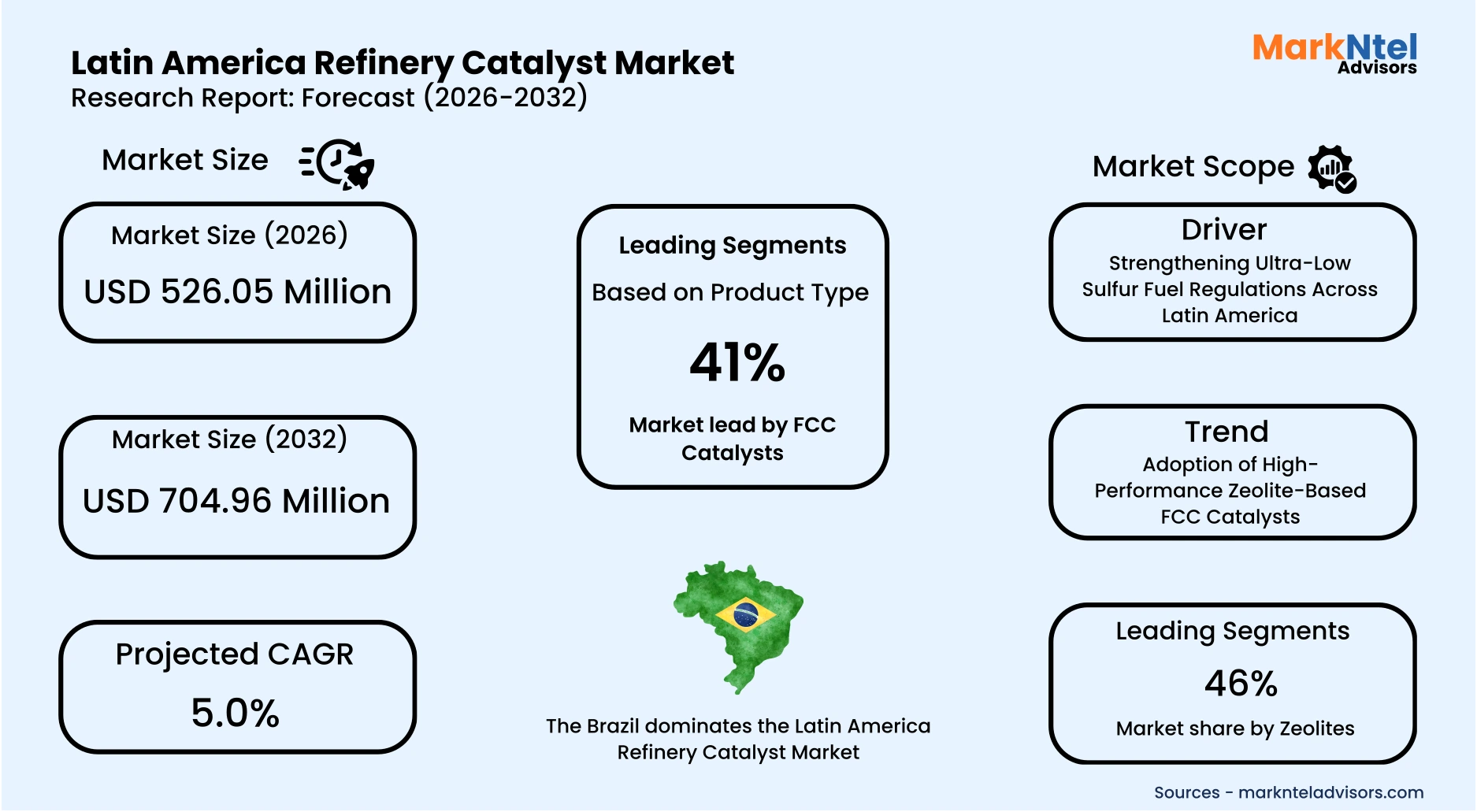

Projected 5.0% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 526.05 Million

Market Size (2032)

USD 704.96 Million

Base Year

2025

Projected CAGR

5.0%

Leading Segments

By Ingredient: Zxeolite

Latin America Refinery Catalyst Market Report Key Takeaways:

- The Latin America Refinery Catalyst Market size was valued at around USD 501 million in 2025 and is projected grow from USD 526.05 million in 2026 to USD 704.96 million by 2032, exhibiting a CAGR of 5.0% during the forecast period.

- Brazil holds the largest market share of about 36% in the Latin America Refinery Catalyst Market in 2026.

- By Product Type, the FCC Catalysts segment represented a significant share of about 41% in the Latin America Refinery Catalyst Market in 2026.

- By Ingredient, the Zeolites segment presented a significant share of about 46% in the Latin America Refinery Catalyst Market in 2026.

- Leading Refinery Catalyst Companies in the Latin America Market are BASF SE, Albemarle Corporation, Haldor Topsoe A/S, W. R. Grace & Co.-Conn., Axens, Honeywell UOP, Shell Catalysts & Technologies, Johnson Matthey, Exxon Mobil Corporation, Clariant AG, and Others.

Market Insights & Analysis: Latin America Refinery Catalyst Market (2026-32):

The Latin America Refinery Catalyst Market size was valued at around USD 501 million in 2025 and is projected grow from USD 526.05 million in 2026 to USD 704.96 million by 2032, exhibiting a CAGR of 5.0% during the forecast period, i.e., 2026-32.

The Latin America refinery catalyst market has expanded in line with regional refining throughput and fuel quality upgrades. According to the International Energy Agency (IEA), Latin America’s oil product demand remained above 6 million barrels per day in 2024, sustaining high utilization of conversion units . Brazil and Mexico together account for the majority of regional refining capacity, supporting continuous catalyst consumption in fluid catalytic cracking (FCC) and hydrotreating units. The structural presence of FCC units, which require ongoing catalyst replenishment, has historically underpinned stable volume growth across the region.

Current market conditions are supported by refinery modernization and capacity additions. In Mexico, Pemex advanced the Dos Bocas refinery project, targeting higher domestic fuel production and reduced import dependency, thereby increasing catalyst demand in hydroprocessing and reforming units. In Brazil, Petrobras has reported investments exceeding USD 10 billion in its 2025–2029 business plan to enhance refining efficiency and low-sulfur fuel output. These initiatives directly stimulate procurement of FCC, hydrotreating, and hydrocracking catalysts to meet cleaner fuel specifications and operational efficiency targets .

End-user demand remains driven by transportation, industrial manufacturing, aviation, and commercial logistics sectors. The World Bank and national energy ministries report continued urbanization and industrial recovery in Brazil, Mexico, and Colombia, sustaining gasoline and diesel consumption. Ultra-low sulfur fuel regulations, aligned with International Maritime Organization sulfur standards and national clean fuel mandates, require refiners to expand hydrotreating capacity . Industrial and commercial users, including freight transport and power generation facilities, indirectly reinforce catalyst demand by maintaining high refinery throughput and desulfurization intensity.

Looking ahead, demand is expected to remain resilient through 2026 as governments prioritize energy security and domestic refining. Brazil’s federal energy planning framework emphasizes downstream optimization and reduced fuel imports, while Mexico continues policy support for refinery self-sufficiency. Technological advancements by global catalyst manufacturers in energy-efficient FCC additives and longer-life hydroprocessing catalysts further enhance refinery economics and sustainability performance. Supported by regulatory tightening, infrastructure upgrades, and stable fuel consumption patterns, the Latin America refinery catalyst market is positioned for steady medium-term expansion.

Latin America Refinery Catalyst Market Recent Developments:

- 2025 : Brazil’s state-run Petrobras signed contracts valued at about USD 892.3 million to complete the RNEST refinery expansion, including a new diesel hydrotreatment unit to enhance processing capability. The expansion is expected to double capacity and boost downstream activities that rely on hydrotreating and catalytic processes.

- 2025 : Petrobras announced USD 4.8 billion in investments to integrate its Reduc refinery with the Boaventura energy complex in Rio de Janeiro, expanding production of low-sulfur diesel and jet fuel. The project includes refinery processing upgrades that will intensify the usage of hydrotreating catalysts in line with cleaner fuel standards.

Latin America Refinery Catalyst Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (FCC Catalysts, Hydrotreating Catalysts, Hydrocracking Catalysts, Reforming Catalysts, Alkylation Catalysts, Others), |

| By Ingredient | (Zeolites, Metals, Chemical Compounds, Others), |

Latin America Refinery Catalyst Market Driver:

Strengthening Ultra-Low Sulfur Fuel Regulations Across Latin America

The tightening of ultra-low sulfur fuel standards remains the most structural driver of refinery catalyst demand across Latin America. In 2025, Brazil’s National Agency of Petroleum (ANP) continued enforcement of S-10 diesel specifications, limiting sulfur content to 10 ppm nationwide, while Mexico’s environmental authorities reaffirmed mandatory ultra-low sulfur diesel distribution in major metropolitan corridors . These regulatory mandates stem from air quality commitments and public health policies, compelling refiners to maintain continuous desulfurization capacity rather than temporary compliance adjustments.

The impact is operational and measurable at the refinery level. In 2025, Mexico exported its first cargo of ultra-low sulfur diesel (ULSD) from the Olmeca refinery, demonstrating active large-scale production of compliant fuels. The milestone indicates sustained hydrotreating operations, directly reinforcing recurring demand for desulfurization catalysts. Hydrotreating units depend on cobalt- and nickel-based catalysts that degrade under higher severity operations, requiring scheduled replacement and thus expanding physical catalyst volumes consumed annually.

This driver enlarges the market size because sulfur compliance raises catalyst intensity per barrel processed. The International Energy Agency reported that Latin America’s refinery throughput recovery continued through 2025, supported by transport and freight demand across Brazil, Mexico, and Colombia. As diesel fuels dominate commercial logistics and heavy transport, refiners must sustain deep desulfurization performance regardless of crude variability. Consequently, sulfur regulation generates structural, recurring catalyst demand linked directly to refinery operations and legally binding fuel specifications rather than discretionary investment cycles.

Latin America Refinery Catalyst Market Trend:

Adoption of High-Performance Zeolite-Based FCC Catalysts

The adoption of high-performance zeolite-based fluid catalytic cracking (FCC) catalysts is emerging as a structural trend driven by changing crude quality and refinery configuration across Latin America. Brazil’s National Agency of Petroleum reported continued growth in pre-salt crude production through 2024–2025, with heavier blends increasingly entering domestic refining systems. Heavier crudes contain higher metals and residue fractions, which intensify thermal and contaminant stress on FCC units. This has accelerated the shift toward ultra-stable Y (USY) and rare-earth-exchanged zeolite catalysts with superior hydrothermal stability and metal tolerance.

This transition is reshaping operational and procurement strategies within refineries. Higher contaminant loads increase catalyst deactivation rates, requiring more resilient formulations capable of sustaining activity under severe cracking conditions. Rather than expanding physical capacity, refiners are upgrading catalyst systems to preserve gasoline yields and maintain conversion efficiency. As a result, catalyst suppliers are moving toward customized, performance-driven zeolite matrices tailored to specific crude slates and residue profiles.

The trend is expected to persist as regional production remains weighted toward heavier offshore and medium-density streams. Structural feedstock complexity, combined with margin pressure in competitive fuel markets, incentivizes refiners to maximize output per barrel without large capital expenditure. Peer-reviewed catalytic research consistently demonstrates that advanced zeolite systems enhance cracking selectivity and thermal resistance under high-severity operations. Consequently, the adoption of high-performance zeolite FCC catalysts represents a durable shift influencing long-term catalyst formulation demand and refinery competitiveness.

Latin America Refinery Catalyst Market Opportunity:

New Refinery Projects and Brownfield Expansion

New refinery projects and brownfield expansions across Latin America present a structurally attractive opportunity for emerging catalyst suppliers. Brazil is progressing with a second refining train at the RNEST refinery, supported by approximately USD 1.2 billion in planned investment, alongside upgrade programs at the Reduc and Repar facilities. These initiatives reflect sustained downstream capital deployment focused on strengthening domestic fuel production capacity. Such expansions structurally increase the installed base of catalyst-intensive conversion and hydroprocessing units.

The opportunity translates directly into measurable catalyst demand because every new refining train or high-conversion unit requires an initial catalyst loading followed by recurring replacement cycles. Modernization programs at Ecuador’s 110,000 barrels-per-day Esmeraldas refinery and Chile’s Aconcagua and Bío Bío facilities further signal continued infrastructure reinforcement. In Guyana, discussions around a proposed 30,000 barrels-per-day refinery at Crab Island highlight incremental downstream diversification. Together, these developments expand the regional footprint of FCC and hydroprocessing capacity.

This environment is particularly advantageous for new and specialized players because expansion-driven procurement enables competitive entry rather than automatic contract renewal. New units typically involve fresh technical evaluations, allowing differentiated formulations to compete on performance metrics. As refinery investments extend into 2026, infrastructure-led growth offers scalable and recurring catalyst demand. Consequently, expansion and modernization projects create a durable structural pathway for market entry and sustained participation.

Latin America Refinery Catalyst Market Challenge:

Crude Oil Price Volatility Impacting Refinery Utilization

Crude oil price volatility represents a structural barrier to stable refinery operations across Latin America. In 2025, as per IEA, Brent crude traded near USD 64 per barrel in September, declining by roughly USD 11 year-to-date amid supply adjustments and demand uncertainty. Such fluctuations compress refining margins when crude input costs shift faster than refined product prices. For refiners in Brazil and Mexico processing heavier domestic crudes, this instability complicates operational forecasting and capital planning.

The impact is directly visible in refinery utilization decisions. When margins narrow, operators reduce throughput or moderate high-severity operations in FCC and hydroprocessing units to preserve cash flow. In 2025, as per IEA assessments of global supply rebalancing, refining margins in emerging markets remained sensitive to feedstock cost movements. Lower operating intensity reduces catalyst circulation volumes and delays scheduled replacement cycles.

This volatility materially restricts scalable market expansion because catalyst demand is directly linked to sustained refinery runs rather than installed nameplate capacity. Price instability discourages discretionary downstream upgrades and limits long-term procurement commitments. Smaller suppliers face heightened uncertainty in contract renewals and volume forecasting. Consequently, persistent crude price fluctuations act as a systemic constraint on sustained catalyst demand growth in Latin America.

Latin America Refinery Catalyst Market (2026-32) Segmentation Analysis:

The Latin America Refinery Catalyst market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- FCC Catalysts

- Hydrotreating Catalysts

- Hydrocracking Catalysts

- Reforming Catalysts

- Alkylation Catalysts

- Others

The FCC catalyst segment dominates the Latin America Refinery Catalyst Market, accounting for approximately 41% of total demand, primarily because gasoline production remains a core output objective for regional refineries. Fluid catalytic cracking units are central to converting heavy gas oils into high-value gasoline and light products, making them indispensable in complex refining configurations. According to Brazil’s National Agency of Petroleum (ANP), gasoline remains one of the most consumed transport fuels domestically, sustaining high FCC utilization rates. Since FCC catalysts circulate continuously within the unit and require regular replenishment, their consumption volume structurally exceeds that of fixed-bed catalyst systems.

Refinery configuration further reinforces this dominance. Major refining systems in Brazil and Mexico are equipped with FCC units as primary conversion assets to process heavier domestic crude streams. Unlike hydrotreating or reforming catalysts, which operate in fixed beds and are replaced in multi-year cycles, FCC catalysts are subject to constant attrition and contamination. This operational characteristic leads to continuous catalyst addition, structurally increasing annual volume demand. As a result, even stable refinery throughput generates recurring FCC catalyst consumption at scale.

Additionally, FCC units play a critical role in maximizing product yield without constructing new large-scale conversion infrastructure. In margin-sensitive markets, refiners prioritize optimizing gasoline output through FCC severity adjustments rather than undertaking capital-intensive hydrocracking expansions. This operational reliance on catalytic cracking strengthens long-term demand for advanced zeolite-based FCC formulations. Consequently, the combination of high gasoline reliance, continuous catalyst replacement, and centrality of FCC units in regional refinery configurations sustains the segment’s 41% market leadership across Latin America.

Based on Ingredient:

- Zeolites

- Metals

- Chemical Compounds

- Others

The zeolite segment dominates the Latin America Refinery Catalyst Market, accounting for approximately 46% of total ingredient demand, primarily because zeolites function as the core crystalline framework in multiple catalytic systems beyond conventional FCC applications. Zeolites provide controlled pore architecture and strong acidity, enabling selective molecular cracking and isomerization reactions essential for gasoline blending and light olefin production. Their unique microporous structure allows refiners to tailor product distribution based on feedstock composition. This functional versatility increases their inclusion across several catalyst formulations rather than limiting them to a single processing unit.

Industrial adaptability further reinforces this dominance. Latin American refineries process a mix of medium and heavy crude streams, which require catalysts capable of maintaining activity under high contaminant exposure. Zeolite frameworks exhibit superior hydrothermal stability and resistance to structural collapse under high-temperature regeneration cycles. Unlike simple metal oxides or amorphous supports, zeolites retain catalytic integrity over prolonged operational periods, reducing performance variability and improving yield predictability.

Additionally, zeolites benefit from decades of structural optimization and scalable synthesis processes. Their standardized crystalline forms allow consistent production quality and integration into advanced catalyst matrices. As refiners seek predictable conversion performance amid fluctuating feedstock quality, zeolite-based systems remain technically indispensable. This combination of structural functionality, operational durability, and formulation flexibility sustains their leading 46% ingredient share across Latin America.

Latin America Refinery Catalyst Market (2026-32): Regional Projection

The Brazil dominates the Latin America Refinery Catalyst Market, accounting for approximately 36% of total regional demand, primarily due to its scale, refinery complexity, and integrated crude supply base. Brazil operates the largest network of refineries in the region, including large conversion-focused complexes such as RNEST and Reduc. These facilities are configured with catalytic cracking, hydrotreating, and reforming units designed to maximize gasoline and diesel yields. The breadth of installed conversion capacity structurally increases catalyst consumption across multiple processing units.

Brazil’s dominance is further supported by its domestic crude production profile, which includes medium and heavier offshore streams from the pre-salt basins. Processing heavier crude requires more intensive catalytic conversion and contaminant management, increasing FCC and hydroprocessing catalyst utilization rates. Unlike smaller regional markets that rely more heavily on fuel imports, Brazil sustains high domestic refining throughput to meet internal fuel demand. Continuous operational severity reinforces recurring catalyst replacement cycles.

Additionally, Petrobras’ refining integration strategy prioritizes yield optimization and reduced import dependency, sustaining downstream activity. The presence of large-scale industrial clusters, established logistics networks, and technical expertise strengthens supply reliability for catalyst procurement. Compared with neighboring markets that operate fewer complex refineries, Brazil’s combination of scale, feedstock characteristics, and operational intensity structurally supports its 36% regional market share.

Gain a Competitive Edge with Our Latin America Refinery Catalyst Market Report:

- Latin America Refinery Catalyst Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Latin America Refinery Catalyst Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Latin America Refinery Catalyst Market Policies, Regulations, and Product Standards

- Latin America Refinery Catalyst Market Trends & Developments

- Latin America Refinery Catalyst Market Dynamics

- Growth Factors

- Challenges

- Latin America Refinery Catalyst Market Hotspot & Opportunities

- Latin America Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- FCC Catalysts

- Hydrotreating Catalysts

- Hydrocracking Catalysts

- Reforming Catalysts

- Alkylation Catalysts

- Others

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Zeolites

- Metals

- Chemical Compounds

- Others

- By Country

- Mexico

- Brazil

- Argentina

- Chile

- Peru

- Columbia

- Rest of Latin America

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Mexico Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Brazil Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Argentina Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Chile Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Peru Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Columbia Refinery Catalyst Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Tons)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Tons

- By Ingredient- Market Size & Forecast 2022-2032, USD Million & Tons

- Market Size & Outlook

- Latin America Refinery Catalyst Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Albemarle Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Haldor Topsoe A/S

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- W. R. Grace & Co.-Conn.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Axens

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell UOP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shell Catalysts & Technologies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson Matthey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Exxon Mobil Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clariant AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now