Global Thermoplastic Elastomers Market Research Report: Trends & Forecast (2026,2032)

By Type (SBC (Styrenic Block Copolymers), TPU (Thermoplastic Polyurethanes), TPO (Thermoplastic Polyolefins), TPV (Thermoplastic Vulcanizates), COPE (Copolymers/Copolyesters), PEBA ... (Polyether Block Amide)), By End-Use Industry (Automotive, Building & Construction, Footwear, Wire & Cable, Medical, Engineering, Others), and others Read more

- Chemicals

- Feb 2026

- Pages 215

- Report Format: PDF, Excel, PPT

Global Thermoplastic Elastomers Market

Projected 4.6% CAGR from 2026,2032 to

Study Period

2026,2032

Market Size (2026)

USD 30.12 Billion

Market Size (2032)

USD 39.45 Billion

Largest Region

Asia-Pacific

Projected CAGR

4.6%

Leading Segments

By Type: Styrenic Block Copolymers (SBC)

Global Thermoplastic Elastomers Market Report Key Takeaways:

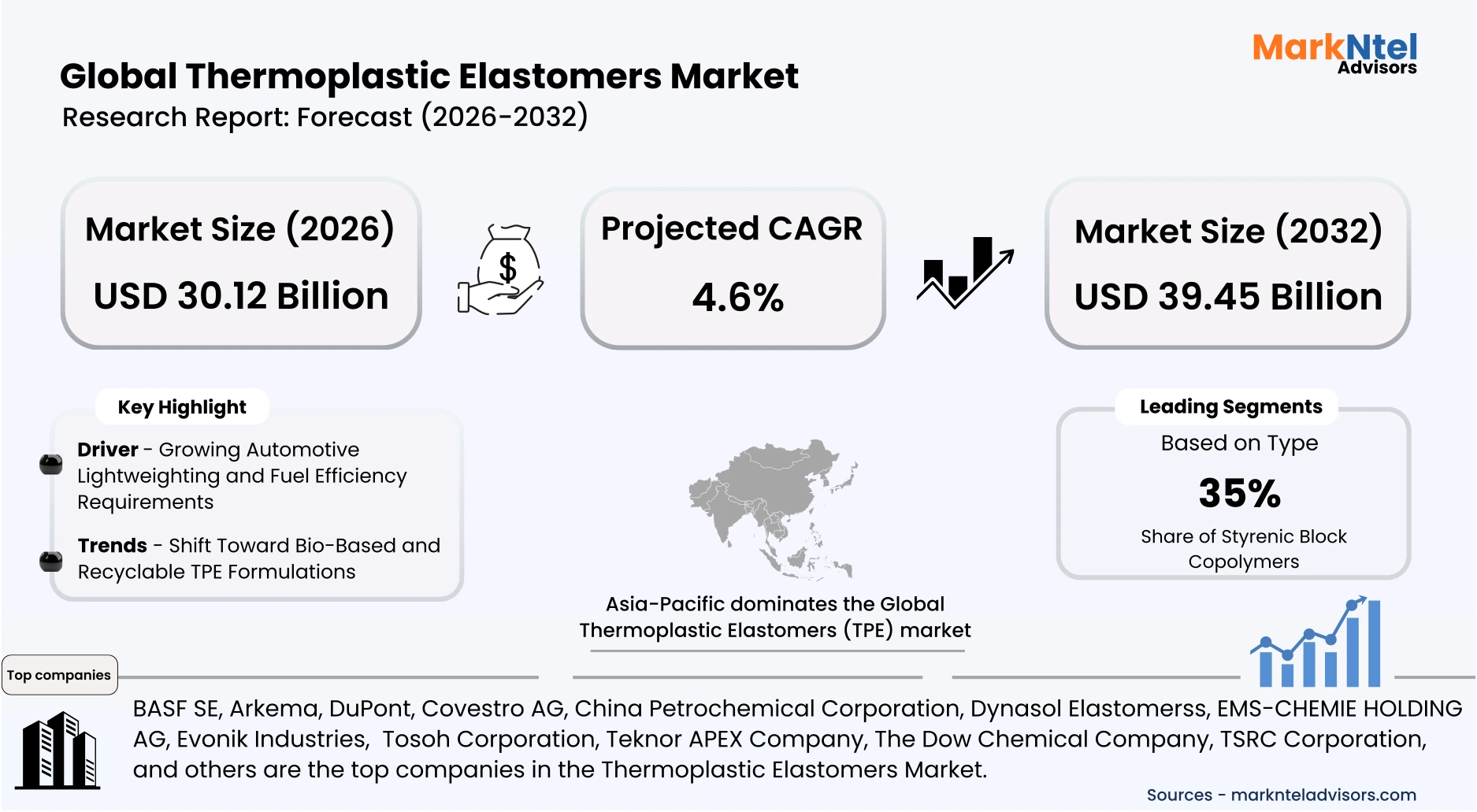

- The Global Thermoplastic Elastomers Market size was valued at around USD 28.80 billion in 2025 and is projected grow from USD 30.12 billion in 2026 to USD 39.45 billion by 2032, exhibiting a CAGR of 4.6% during the forecast period.

- Asia-Pacific, holds the largest market share of about 45.32% in the Global Thermoplastic Elastomers Market in 2026.

- By Type, the Styrenic Block Copolymers (SBC) segment represented a significant share of about 35% in the Global Thermoplastic Elastomers Market in 2026.

- By End User, the Automotive segment presented a significant share of about 31% in the Global Thermoplastic Elastomers Market in 2026.

- Leading Thermoplastic Elastomers Companies in the Global Market are BASF SE, Arkema, DuPont, Covestro AG, China Petrochemical Corporation, Dynasol Elastomerss, EMS-CHEMIE HOLDING AG, Evonik Industries, Kraton Polymers LLC, LG Chem, LCY Chemical Corporation, Lubrizol Corporation, LyondellBasell Industries, Tosoh Corporation, Avient Corporation, Teknor APEX Company, The Dow Chemical Company, TSRC Corporation, and Others.

Market Insights & Analysis: Global Thermoplastic Elastomers Market (2026-32):

The Global Thermoplastic Elastomers Market size was valued at around USD 28.80 billion in 2025 and is projected grow from USD 30.12 billion in 2026 to USD 39.45 billion by 2032, exhibiting a CAGR of 4.6% during the forecast period, i.e., 2026-32.

The global thermoplastic elastomers (TPE) market is structurally supported by sustained automotive production and vehicle lightweighting trends. According to the International Organization of Motor Vehicle Manufacturers (OICA), global motor vehicle production reached approximately 92.5 million units in 2024, reflecting stabilization near pre-pandemic levels . Automotive manufacturers increasingly substitute conventional rubber and PVC with TPE in sealing systems, airbag covers, interior trims, and under-the-hood components due to weight reduction and recyclability advantages. For instance, Toyoda Gosei announced that its curtain airbags are being fitted in the new Honda Prelude sports coupe, highlighting OEM-level integration of advanced elastomeric materials in safety systems. The continued expansion of electric vehicle production further strengthens demand for advanced elastomeric materials used in cable insulation, battery sealing, and vibration damping systems.

Construction and infrastructure development remain critical demand anchors. The United States Infrastructure Investment and Jobs Act allocates approximately USD 1.2 trillion toward long-term transport, energy, and water infrastructure modernization, directly stimulating polymer consumption in piping, roofing membranes, insulation, and expansion joints. Similarly, India’s Pradhan Mantri Awas Yojana housing program continues to support large-scale residential construction, with millions of homes sanctioned under official government reporting . These initiatives sustain steady demand from residential and commercial end-users, where flexible, weather-resistant, and durable materials such as TPE are increasingly adopted.

Healthcare and consumer goods sectors further reinforce volume growth. Expanding public healthcare spending reported by the World Health Organization in 2025 supports rising production of medical tubing, syringe components, and device housings that rely on sterilizable thermoplastic elastomers. In parallel, growing demand for soft-touch consumer products, wearable devices, and electrical components increases TPE penetration due to design flexibility and ease of processing. Regulatory focus on recyclable and low-VOC materials in the European Union and United States is accelerating substitution toward thermoplastic systems over thermoset alternatives.

Looking ahead, urbanization and electrification trends provide durable growth foundations. The United Nations projects that nearly 68% of the global population will live in urban areas by 2050 , reinforcing infrastructure, transportation, and consumer product demand. As governments prioritize energy efficiency, sustainable construction, and vehicle electrification, material innovation will remain central to industrial competitiveness. Supported by automotive production stability, infrastructure spending, and regulatory-driven material substitution, the global TPE market is positioned for steady and structurally grounded expansion in the coming years.

Global Thermoplastic Elastomers Market Recent Developments:

- 2025 : KRAIBURG TPE Americas participated in PLASTIMAGEN® MÉXICO 2025 in Mexico City, showcasing its latest thermoplastic elastomer solutions for medical and consumer applications. The company introduced its THERMOLAST® M Supersoft compounds, designed to deliver enhanced softness, flexibility, and performance for next-generation TPE applications.

- 2025 : Mitsui Chemicals announced that Kumho Mitsui Chemicals will increase MDI production capacity at its Yeosu, South Korea plant by 100,000 tons per year, raising total capacity to 710,000 tons annually. The expansion, beginning in February 2026, is intended to meet growing demand for polyurethane materials used in automotive components and insulation applications, while enhancing energy efficiency and reducing greenhouse gas emissions.

Global Thermoplastic Elastomers Market Scope:

| Category | Segments |

|---|---|

| By Type | (SBC (Styrenic Block Copolymers), TPU (Thermoplastic Polyurethanes), TPO (Thermoplastic Polyolefins), TPV (Thermoplastic Vulcanizates), COPE (Copolymers/Copolyesters), PEBA (Polyether Block Amide)), |

| By End-Use Industry | (Automotive, Building & Construction, Footwear, Wire & Cable, Medical, Engineering, Others), |

Global Thermoplastic Elastomers Market Driver:

Growing Automotive Lightweighting and Fuel Efficiency Requirements

Automotive lightweighting has become a structurally embedded driver of thermoplastic elastomer (TPE) demand as governments intensify fuel efficiency and emissions regulations. In 2025, the United States Environmental Protection Agency confirmed strengthened greenhouse gas standards for light- and medium-duty vehicles through 2032 , while the European Union continues enforcing binding CO₂ reduction targets requiring significant emission cuts by 2030. These regulatory mandates compel automakers to reduce vehicle mass and improve energy efficiency, accelerating substitution of heavier rubber and metal components with advanced polymer systems. For instance, Freudenberg Sealing Technologies introduced Quantix ULTRA, a high-temperature-resistant thermoplastic material designed for EV battery flame protection systems that withstands extreme heat while enabling lightweight metal substitution in series production vehicles .

This shift is materially expanding elastomer consumption across both conventional and electric vehicle platforms. Lightweight materials are increasingly integrated into sealing systems, airbag modules, cable insulation, vibration-damping components, and interior assemblies to offset structural weight and enhance energy performance. Electric vehicles further intensify this requirement, as battery systems increase vehicle mass and necessitate compensatory reductions in other component categories. As a result, TPE usage is becoming embedded at the design stage of new vehicle architectures rather than added incrementally.

Importantly, this driver expands market volume rather than influencing pricing dynamics alone. Regulatory compliance is mandatory and applies across entire production portfolios, ensuring widespread adoption across original equipment manufacturers. Each vehicle platform redesign incorporates greater polymer integration to meet fuel economy and range targets, structurally increasing material demand per unit produced. With emissions standards tightening through 2026 and beyond, automotive lightweighting remains a systemic and long-term catalyst for sustained TPE market growth.

Global Thermoplastic Elastomers Market Trend:

Shift Toward Bio-Based and Recyclable TPE Formulations

The shift toward bio-based and recyclable thermoplastic elastomer (TPE) formulations has accelerated due to binding circular economy regulations across major markets. In 2025, the European Union’s Packaging and Packaging Waste Regulation (PPWR) entered into force, introducing mandatory design-for-recycling requirements and recycled content targets for plastic packaging placed on the EU market . The regulation aims to ensure that all packaging is recyclable by 2030, compelling polymer manufacturers to prioritize recyclability and secondary material integration. These legally enforceable measures have transformed sustainability from a voluntary initiative into a compliance-driven product development imperative.

This regulatory shift is restructuring value chains by increasing demand for mechanically recyclable elastomers and bio-based feedstocks compatible with circular systems. Downstream manufacturers in automotive, consumer goods, and electronics are tightening procurement standards to align with sustainability disclosures and carbon reporting frameworks. In parallel, producers are expanding mass-balance certified materials and recycled-content compounds to meet customer and regulatory requirements. For instance, in 2025, Lignin Industries introduced Renol® TPV, a bio-based thermoplastic elastomer containing 70% renewable lignin feedstock. The material reportedly delivers up to a 50% reduction in CO₂ emissions while remaining compatible with existing manufacturing systems . Similarly, HEXPOL TPE expanded its Mediprene portfolio with ISCC PLUS-certified mass-balance medical TPEs, enabling fossil feedstock replacement while maintaining identical regulatory and technical performance. As a result, formulation strategies are increasingly centered on material recovery compatibility, lifecycle emissions reduction, and regulatory traceability.

The persistence of this trend is reinforced by codified EU targets extending through 2030 and similar circular economy frameworks emerging in North America and Asia. Regulatory timelines provide long-term investment certainty, encouraging capital allocation toward recyclable thermoplastic systems. End-user industries are embedding recyclability metrics into supplier qualification processes, structurally influencing material selection decisions. Consequently, bio-based and recyclable TPE development is expected to remain a defining force shaping long-term market evolution.

Global Thermoplastic Elastomers Market Opportunity:

Growth in Smart Materials and Flexible Electronics Applications

The expansion of smart materials and flexible electronics represents a structural opportunity for thermoplastic elastomers (TPE), supported by accelerating global digital adoption. According to the International Telecommunication Union’s Facts and Figures 2025, the number of Internet users reached approximately 6 billion in 2025, reflecting sustained growth in connected populations . Governments across major economies are simultaneously advancing semiconductor and digital infrastructure programs to strengthen domestic electronics manufacturing. This convergence of connectivity expansion and production capacity growth is increasing demand for flexible, durable polymer components in smart devices.

This opportunity translates into tangible material demand because flexible electronics rely on elastomeric materials for insulation, sealing, overmolding, and impact resistance. Wearable health monitors, smart home systems, and connected sensors require lightweight and bendable polymers compatible with compact, high-performance designs. As digital inclusion policies continue to expand access and device penetration, production volumes of connected hardware rise correspondingly. For example, at K 2025, Celanese introduced Santoprene® halogen-free flame-retardant TPV grades designed for dynamic cable and connectivity applications, underscoring growing material innovation for next-generation electronic systems . Consequently, advanced TPE grades become enabling materials embedded within next-generation electronic architectures.

The segment is particularly favorable for emerging players because electronics ecosystems prioritize rapid innovation and customization. Shorter product development cycles allow smaller material suppliers to collaborate directly with device manufacturers. Unlike highly consolidated automotive supply chains, electronics production supports diversified sourcing strategies. These structural conditions create scalable entry pathways for new TPE manufacturers aligned with global digital expansion.

Global Thermoplastic Elastomers Market Challenge:

Regulatory Complexity and Escalating Chemical Compliance Costs

Regulatory complexity has emerged as a critical structural barrier for thermoplastic elastomer (TPE) manufacturers, driven by tightening chemical safety and environmental standards. In 2025, the European Chemicals Agency continued expanding substance evaluations under REACH, while the European Union advanced restrictions on intentionally added microplastics and certain PFAS compounds. These measures require detailed substance registration, exposure assessments, and reformulation where restricted additives are identified. Compliance obligations are increasingly cross-border, as exporters to the EU must also meet these standards regardless of production location.

This evolving regulatory environment imposes measurable operational burdens on manufacturers. REACH registration requires extensive toxicological data submission and ongoing dossier updates, increasing testing and documentation costs for chemical producers. In the United States, the Environmental Protection Agency continues implementing amendments under the Toxic Substances Control Act, including risk evaluations and reporting requirements that demand additional data generation and supply chain traceability . Smaller compounders face disproportionate pressure due to limited in-house regulatory expertise and financial resources.

These compliance demands materially restrict market expansion by raising entry barriers and lengthening product development timelines. Reformulation to replace restricted additives can require new testing, certification, and customer requalification, delaying commercialization. Investment decisions are increasingly influenced by regulatory uncertainty, particularly regarding PFAS and microplastic classifications. As regulatory scrutiny intensifies through 2026 and beyond, chemical compliance complexity remains a systemic constraint on scalable growth within the TPE market.

Global Thermoplastic Elastomers Market (2026-32) Segmentation Analysis:

The Global Thermoplastic Elastomers Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the global level. Based on the analysis, the market has been further classified as;

Based on Type:

- SBC (Styrenic Block Copolymers)

- TPU (Thermoplastic Polyurethanes)

- TPO (Thermoplastic Polyolefins)

- TPV (Thermoplastic Vulcanizates)

- COPE (Copolymers/Copolyesters)

- PEBA (Polyether Block Amide)

Styrenic Block Copolymers (SBC) have emerged as the dominant product type in the Global Thermoplastic Elastomers (TPE) market, accounting for approximately 35% of total market share, primarily due to their balanced performance, cost efficiency, and broad application versatility. Compared with specialty TPE types such as TPV, TPU, or COPE, SBC offers excellent elasticity, clarity, softness, and ease of processing at a comparatively lower material cost. This favorable performance-to-price ratio makes SBC particularly attractive for high-volume consumer and industrial applications where flexibility and economic feasibility are equally critical. Its ability to be processed using standard thermoplastic equipment further enhances its commercial scalability.

The dominance of SBC is reinforced by its widespread adoption across packaging, consumer goods, medical devices, and footwear sectors. In food and beverage packaging, SBC-based compounds are extensively used in seals, closures, and flexible films due to their softness, transparency, and compliance with food-contact regulations. In healthcare applications, SBC materials are increasingly preferred for tubing, syringe components, and overmolded grips as latex-free alternatives. Additionally, the footwear industry continues to utilize SBC for lightweight soles and cushioning components, benefiting from its resilience and cost-effectiveness in mass production environments.

SBC also benefits from mature global manufacturing infrastructure and formulation flexibility. Producers can easily modify hardness, tackiness, and clarity through blending and compounding without requiring complex crosslinking processes. Unlike thermoset elastomers, SBC can be reprocessed and recycled within production cycles, supporting circular economy objectives. For example, Kraton’s CirKular+™ platform, marking five years of development, enhances recycled-content integration and renewable feedstock adoption in styrenic block copolymers, reinforcing SBC’s alignment with circular economy and decarbonization goals. Its compatibility with injection molding, extrusion, and blow molding technologies enables rapid production cycles and broad supplier participation . Collectively, strong demand across high-volume industries, favorable economics, and scalable processing have enabled SBC to maintain its leading position within the global TPE market.

Based on End User Industry:

- Automotive

- Building & Construction

- Footwear

- Wire & Cable

- Medical

- Engineering

The automotive sector has emerged as the dominant end-user industry in the Global Thermoplastic Elastomers (TPE) market, accounting for approximately 31% of total market size, primarily due to sustained vehicle production volumes and increasing material substitution trends. TPE materials offer a balanced combination of flexibility, lightweight properties, chemical resistance, and cost efficiency compared with conventional rubber and certain engineering plastics. This performance-to-cost advantage positions TPE as a preferred material for high-volume automotive components where durability, weight reduction, and processing efficiency are critical. As automakers intensify lightweighting strategies to meet fuel efficiency and emission targets, demand for versatile elastomeric materials continues to expand structurally.

The dominance of the automotive segment is reinforced by the broad integration of TPE across both conventional and electric vehicle platforms. TPE is extensively used in weather seals, window gaskets, airbag covers, cable insulation, interior soft-touch components, and vibration-damping systems. The rapid growth of electric vehicles further amplifies this demand, as battery systems require advanced sealing, thermal management, and high-voltage cable protection solutions. In 2025, material suppliers continued introducing flame-retardant and high-heat-resistant TPE grades tailored for EV connectivity and battery safety applications, reflecting OEM focus on performance and regulatory compliance.

Additionally, automotive manufacturing benefits from mature global supply chains and standardized processing technologies such as injection molding and extrusion, enabling efficient scalability. TPE’s compatibility with automated high-volume production lines supports consistent quality and shorter cycle times. Its recyclability and formulation flexibility also align with increasing sustainability targets within automotive procurement policies. Together, high production volumes, diversified component applications, and scalable processing infrastructure have enabled the automotive sector to maintain its leading position within the global TPE market.

Global Thermoplastic Elastomers Market (2026-32): Regional Projection

Asia-Pacific dominates the Global Thermoplastic Elastomers (TPE) market, holding around 31% market share, primarily due to its extensive manufacturing base and diversified end-use industries. According to UNIDO’s 2025 industrial statistics, Asia contributes more than half of global manufacturing value added, led by China, Japan, South Korea, and India. This concentration of automotive, electronics, consumer goods, and industrial production creates a structurally high baseline demand for elastomeric materials used in seals, gaskets, soft-touch components, and cable insulation . The region’s large-scale, export-oriented production ecosystems consistently require cost-efficient and processable polymer solutions such as TPE.

The region’s dominance is further reinforced by its leadership in automotive manufacturing. Data from the International Organization of Motor Vehicle Manufacturers (OICA) indicates that Asia Pacific accounts for the largest share of global vehicle production, driven by China, Japan, India, and South Korea. As automotive OEMs expand electric vehicle output and integrate lightweight materials, demand for TPE in battery sealing systems, weatherstrips, interior trims, and vibration-damping components continues to increase . Parallel expansion in electronics manufacturing across East Asia also supports TPE consumption in cable insulation, connectors, and wearable device components.

In addition, supportive industrial policies and infrastructure investment programs across major Asian economies strengthen regional competitiveness. Government-led manufacturing incentives, semiconductor expansion initiatives, and supply chain localization strategies enhance material procurement and processing capabilities. The presence of integrated petrochemical complexes and mature compounding infrastructure reduces production costs and improves scalability. Together, high-volume manufacturing output, diversified end-user demand, and cost-competitive supply chains position Asia Pacific as the dominant regional market within the global TPE industry.

Gain a Competitive Edge with Our Global Thermoplastic Elastomers Market Report:

- Global Thermoplastic Elastomers Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Global Thermoplastic Elastomers Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Global Thermoplastic Elastomers Market Policies, Regulations, and Product Standards

- Global Thermoplastic Elastomers Market Trends & Developments

- Global Thermoplastic Elastomers Market Dynamics

- Growth Factors

- Challenges

- Global Thermoplastic Elastomers Market Hotspot & Opportunities

- Global Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- SBC (Styrenic Block Copolymers)

- TPU (Thermoplastic Polyurethanes)

- TPO (Thermoplastic Polyolefins)

- TPV (Thermoplastic Vulcanizates)

- COPE (Copolymers/Copolyesters)

- PEBA (Polyether Block Amide)

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Automotive

- Building & Construction

- Footwear

- Wire & Cable

- Medical

- Engineering

- Others

- By Region

- North America

- South America

- Europe

- The Middle East & Africa

- Asia Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- North America Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Canada Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Mexico Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Market Size & Outlook

- South America Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Argentina Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Market Size & Outlook

- Europe Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Country

- The UK

- Germany

- France

- Italy

- Switzerland

- BENELUX

- Rest of Europe

- The UK Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Germany Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- France Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Italy Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Switzerland Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- BENELUX Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Market Size & Outlook

- The Middle East & Africa Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Country

- Saudi Arabia

- UAE

- Qatar

- Turkey

- Israel

- South Africa

- Egypt

- Rest of the Middle East & Africa

- Saudi Arabia Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- UAE Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Qatar Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Turkey Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Israel Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- South Africa Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Egypt Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Market Size & Outlook

- Asia Pacific () Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By Country

- China

- Japan

- India

- South Korea

- Indonesia

- Australia

- Singapore

- Vietnam

- Rest of Asia-Pacific

- China Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Japan Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- India Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- South Korea Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Indonesia Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Australia Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Singapore Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Vietnam Thermoplastic Elastomers Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Number of Units Sold in Tons

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Million Tons

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million & Million Tons

- Market Size & Outlook

- Market Size & Outlook

- Global Thermoplastic Elastomers Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arkema

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DuPont

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Covestro AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China Petrochemical Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dynasol Elastomerss

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EMS-CHEMIE HOLDING AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Evonik Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kraton Polymers LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Chem

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LCY Chemical Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lubrizol Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LyondellBasell Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tosoh Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Avient Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Teknor APEX Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Dow Chemical Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TSRC Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now