Asia Rubber Process Oils Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Product Type (Aromatic, Paraffinic, Naphthenic, Treated Distillate Aromatic Extract (TDAE), Mild Extracted Solvent (MES), Distillate Aromatic Extract (DAE), Residual Aromatic Ex ... tract (RAE), Other specialty types), By Application (Tire Manufacturing, Footwear, Wire & Cable Covering, Flooring Materials, Adhesives & Sealants, Others), By End User Industry (Automotive, Industrial Manufacturing, Construction, Aerospace & Defense, Consumer Products, Energy & Utilities), and others Read more

- Chemicals

- Feb 2026

- Pages 250

- Report Format: PDF, Excel, PPT

Asia Rubber Process Oils Market

Projected 10.21% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 2.31 Billion

Market Size (2032)

USD 4.14 Billion

Base Year

2025

Projected CAGR

10.21%

Leading Segments

By Application: Tire Manufacturing

Asia Rubber Process Oils Market Report Key Takeaways:

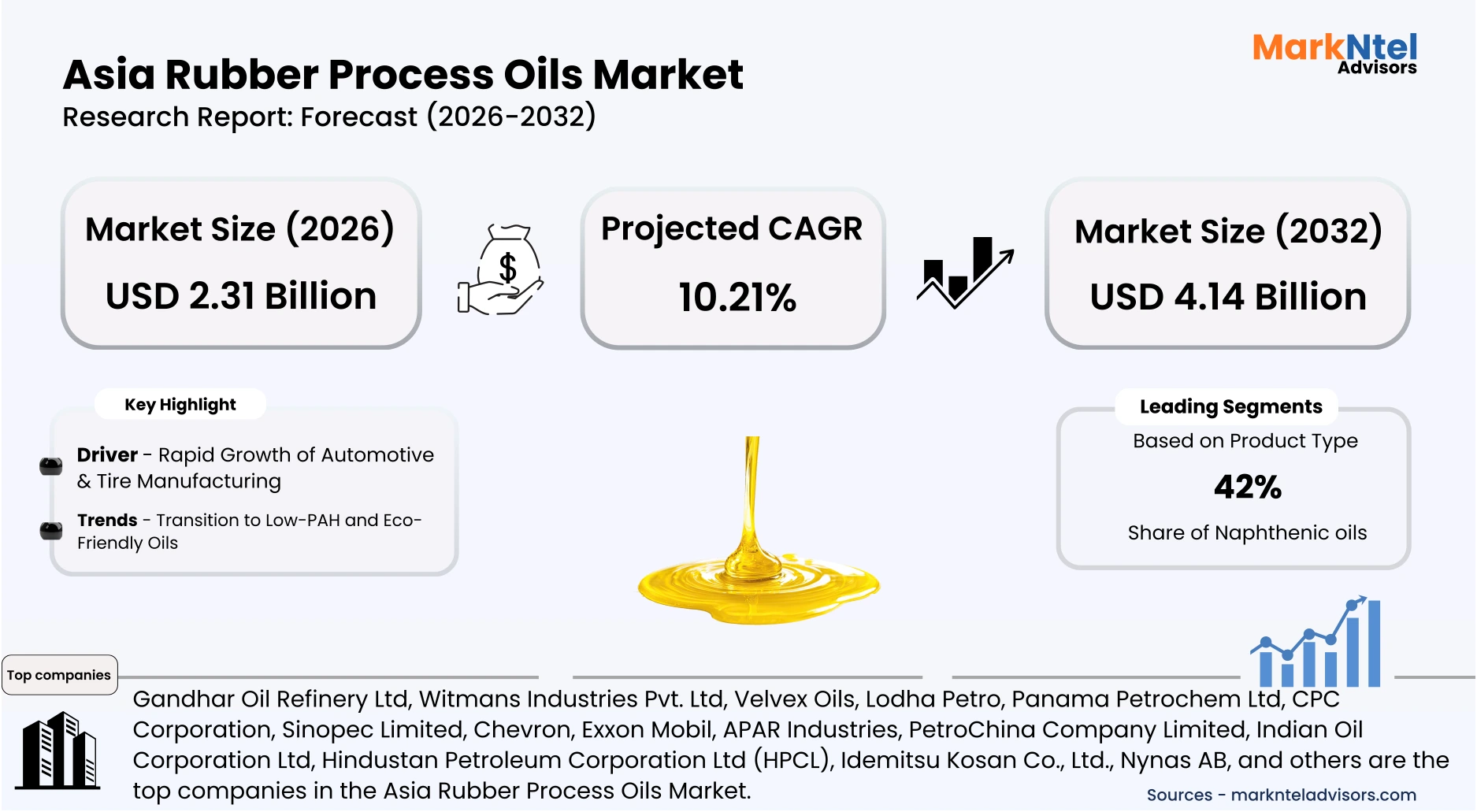

- The Asia Rubber Process Oils Market size was valued at around USD 2.11 billion in 2025 and is projected grow from USD 2.31 billion in 2026 to USD 4.14 billion by 2032, exhibiting a CAGR of 10.21% during the forecast period.

- China holds the largest market share of about 52% in the Asia Rubber Process Oils Market in 2026.

- By Product Type, the Naphthenic segment represented a significant share of about 42% in the Asia Rubber Process Oils Market in 2026.

- By Application, the Tire Manufacturing segment presented a significant share of about 54% in the Asia Rubber Process Oils Market in 2026.

- Leading Rubber Process Oils companies in the Asian Market are Gandhar Oil Refinery Ltd, Witmans Industries Pvt. Ltd, Velvex Oils, Lodha Petro, Panama Petrochem Ltd, CPC Corporation, Sinopec Limited, Chevron, Exxon Mobil, APAR Industries, PetroChina Company Limited, Indian Oil Corporation Ltd, Hindustan Petroleum Corporation Ltd (HPCL), Idemitsu Kosan Co., Ltd., Nynas AB, and Others.

Market Insights & Analysis: Asia Rubber Process Oils Market (2026-32):

The Asia Rubber Process Oils Market size was valued at around USD 2.11 billion in 2025 and is projected grow from USD 2.31 billion in 2026 to USD 4.14 billion by 2032, exhibiting a CAGR of 10.21% during the forecast period, i.e., 2026-32.

Asia’s rubber process oils market has expanded in parallel with the region’s dominance in automotive and tire manufacturing, particularly in China and India. According to the International Organization of Motor Vehicle Manufacturers (OICA), China remained the world’s largest vehicle producer in 2025, while India ranked among the top three globally, reinforcing structural tire demand. The World Bank’s 2025 regional outlook highlighted resilient industrial output growth across emerging East and South Asia, supporting downstream petrochemical consumption. Historically, this combination of large-scale vehicle production, export-oriented rubber goods manufacturing, and integrated refining capacity has created a stable demand base for process oils used in tire compounding and industrial rubber products .

Current market conditions remain supported by infrastructure expansion and rising replacement tire demand across densely populated economies. The Asian Development Bank’s 2025 update confirmed continued public infrastructure spending across Southeast Asia, including highway and urban transit development, which indirectly stimulates commercial vehicle usage and tire wear rates. China’s 2025 industrial policy framework continues to prioritize advanced manufacturing and domestic value addition in petrochemicals and synthetic materials, sustaining feedstock and blending availability. Meanwhile, India’s Production Linked Incentive (PLI) schemes for the automobile and advanced chemistry sectors, extended into 2025, reinforce local manufacturing ecosystems that consume rubber-based components.

Regulatory shifts have also reshaped product preferences, particularly regarding low-polycyclic aromatic hydrocarbon (PAH) content in process oils. Environmental compliance measures aligned with EU REACH standards, increasingly adopted by Asian exporters, have encouraged the transition toward treated distillate aromatic extract (TDAE) and naphthenic grades . National decarbonization commitments announced in 2025 by China and South Korea have accelerated refinery efficiency upgrades and cleaner base oil production. Major refiners such as Sinopec and Indian Oil Corporation have publicly reported investments in cleaner fuels and specialty products, strengthening supply reliability for compliant rubber process oils.

Looking forward, demographic growth, rapid urbanization, and expanding middle-class vehicle ownership across South and Southeast Asia are expected to sustain replacement tire demand. The United Nations’ 2025 population projections show continued urban concentration in Asia, intensifying transport and logistics requirements. Government-led electric mobility initiatives in China and India, updated in 2025 policy statements, are projected to increase demand for specialized tire formulations compatible with electric vehicles. These structural economic, regulatory, and industry-led factors collectively provide a stable and forward-looking foundation for the continued expansion of the Asia rubber process oils market.

Asia Rubber Process Oils Market Recent Developments:

- 2025 : PSP Specialties revealed a bio-based rubber process oil designed to reduce reliance on fossil feedstocks and improve environmental performance. The innovation aims to meet evolving sustainability expectations in rubber compounding while maintaining processing efficacy, with a targeted market launch planned for 2026, reflecting industry shifts toward greener manufacturing.

- 2025 : Nandan Petrochem Ltd. is advancing sustainability through its VELVEX Rubber Process Oils, formulated with low sulphur and reduced metal content to meet global environmental standards. The company also produces high-purity transformers and white oils, emphasizing energy-efficient manufacturing and regulatory compliance across industrial and specialty applications.

Asia Rubber Process Oils Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Aromatic, Paraffinic, Naphthenic, Treated Distillate Aromatic Extract (TDAE), Mild Extracted Solvent (MES), Distillate Aromatic Extract (DAE), Residual Aromatic Extract (RAE), Other specialty types), |

| By Application | (Tire Manufacturing, Footwear, Wire & Cable Covering, Flooring Materials, Adhesives & Sealants, Others), |

| By End User Industry | (Automotive, Industrial Manufacturing, Construction, Aerospace & Defense, Consumer Products, Energy & Utilities), |

Asia Rubber Process Oils Market Driver:

Rapid Growth of Automotive & Tire Manufacturing

The most influential structural driver of Asia’s rubber process oils market is the sustained expansion of vehicle production and fleet size across major economies. According to the China Association of Automobile Manufacturers, China’s total auto output reached 27.69 million units in the first ten months of 2025, while new energy vehicle sales rose 32.7% year on year to 12.94 million units, accounting for 46.7% of total sales. Such large-scale production directly translates into proportional tire manufacturing volumes, as each vehicle requires multiple original equipment tires. Tire compounding structurally incorporates process oils to improve flexibility, dispersion, and thermal resistance, creating a direct cause-and-effect linkage between automotive output and oil consumption.

This driver has intensified due to expanding vehicle fleets and logistics activity across Asia. India’s Ministry of Road Transport and Highways reported that total registered vehicles surpassed 350 million units in 2025, reflecting continuous growth in the active vehicle parc. A larger fleet increases replacement tire cycles, generating recurring and volume-based demand independent of short-term pricing fluctuations. Additionally, Japan’s Ministry of Economy, Trade, and Industry reported stable automotive production recovery in 2025, reinforcing regional supply chain throughput. These developments collectively expand rubber processing activity across passenger, commercial, and industrial vehicle segments.

The driver materially enlarges the market size because tire manufacturing operates on standardized compound formulations with fixed oil loading ratios per ton of rubber. In 2025, the South Korean government also announced plans to increase electric vehicle subsidies by approximately 20% approximately USD 658 million for 2026, reinforcing sustained policy backing for EV manufacturing and associated automotive supply chains . Electric vehicles require specialized tires with enhanced durability and load-bearing capacity, sustaining process oil intensity per unit. Consequently, the structural expansion of automotive and tire manufacturing across Asia is generating measurable increases in rubber compounding volumes rather than merely influencing pricing dynamics.

Asia Rubber Process Oils Market Trend:

Transition to Low-PAH and Eco-Friendly Oils

A sustained structural trend in Asia’s rubber process oils industry is the transition toward low-polycyclic aromatic hydrocarbon (PAH) and environmentally compliant oils. This shift has accelerated due to regulatory enforcement under the European Union’s REACH Regulation, which restricts PAH content in extender oils used in tires and rubber components. As Asian tire manufacturers export significantly to Europe, compliance has become mandatory rather than optional. The European Chemicals Agency continues to enforce Annex XVII restrictions, directly influencing formulation standards across exporting markets.

This regulatory pressure has triggered structural changes across the value chain, particularly in refining and compounding operations. Refiners are upgrading hydro-treatment capacity to produce treated distillate aromatic extract (TDAE) and naphthenic grades with lower harmful aromatic content. Tire manufacturers are reformulating compounds to maintain performance while meeting compliance thresholds, altering procurement strategies and supplier qualification processes. These adjustments are not cosmetic but embedded within long-term manufacturing standards for export-oriented producers.

The trend is expected to persist because sustainability and chemical safety regulations are tightening globally, not reversing. The United Nations Environment Programme’s 2025 chemicals management initiatives emphasize stricter oversight of hazardous substances in industrial applications. Additionally, corporate ESG reporting frameworks increasingly require supply-chain transparency, reinforcing demand for compliant specialty oils. Consequently, the structural migration toward low-PAH and eco-friendly process oils is reshaping product portfolios and long-term investment priorities across Asia.

Asia Rubber Process Oils Market Opportunity:

Expansion Potential Across Emerging Southeast Asian Economies

Fragmented specialty oil supply ecosystems across emerging Southeast Asian economies are creating a strategic entry window for new rubber process oil suppliers. Vietnam earned nearly USD 29 billion from footwear exports in 2025, up 5% year-on-year, according to the Vietnam Leather, Footwear and Handbag Association (Lefaso), reflecting expanding rubber-based sole and component production . Rising footwear and light industrial rubber manufacturing require consistent compounding inputs, including process oils. As production clusters expand, localized sourcing becomes increasingly critical for cost efficiency and supply reliability.

This opportunity exists because ASEAN manufacturing hubs are scaling faster than the development of integrated specialty oil infrastructure. Indonesia’s Ministry of Industry reported continued growth in downstream automotive and component manufacturing under national industrial transformation programs in 2025. Each new tire or rubber goods facility structurally increases oil consumption due to fixed oil loading ratios embedded in compound formulations. However, supply chains in these markets remain less consolidated than in China or Japan, creating competitive whitespace.

For new and emerging players, lower market concentration and evolving distributor networks reduce entry barriers. Governments across Southeast Asia continue to promote export-oriented manufacturing and industrial clustering, supporting scalable production growth. Agile suppliers can establish early partnerships with expanding footwear, automotive, and industrial manufacturers before long-term contracts become entrenched. Consequently, emerging Southeast Asian economies represent a structurally favorable platform for differentiated and scalable rubber process oil market entry.

Asia Rubber Process Oils Market Challenge:

Volatile Crude Oil & Feedstock Prices

Volatility in crude oil and refinery feedstock prices represents a structural constraint for Asia’s rubber process oils market because process oils are derived from petroleum fractions. The International Energy Agency’s 2025 Oil Market Report highlighted continued oil price sensitivity to geopolitical disruptions, OPEC+ production adjustments, and inventory fluctuations. Brent crude prices fluctuated around the USD 75–85 per barrel range during 2025, reflecting ongoing market instability. Such variability directly affects base oil and aromatic extract costs used in rubber compounding.

This price instability measurably impacts producers through margin compression and cost pass-through limitations. Public financial disclosures from major Asian refiners in 2025 showed refining margin variability linked to crude input cost swings and product spread fluctuations. Rubber compounders often operate under fixed or medium-term contracts, limiting their ability to immediately transfer rising feedstock costs to tire and industrial rubber manufacturers. As a result, profitability and working capital requirements are directly affected during periods of elevated crude prices.

The volatility materially restricts market expansion by complicating capital allocation and scaling decisions. Unpredictable feedstock costs increase financial risk for new entrants considering blending facility investments or regional expansion. Downstream manufacturers may delay procurement commitments during periods of price uncertainty, affecting adoption rates and long-term contracts. Consequently, sustained crude oil and base oil price fluctuations function as a systemic barrier to scalable growth and operational stability within the rubber process oils market.

Asia Rubber Process Oils Market (2026-32) Segmentation Analysis:

The Asia Rubber Process Oils market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Aromatic

- Paraffinic

- Naphthenic

- Treated Distillate Aromatic Extract (TDAE)

- Mild Extracted Solvent (MES)

- Distillate Aromatic Extract (DAE)

- Residual Aromatic Extract (RAE)

- Other specialty types

Naphthenic oils dominate the Asia Rubber Process Oils market, accounting for approximately 42% of total product demand, primarily because of their balanced solvency and performance characteristics suited to the region’s large-scale rubber manufacturing base. According to the Japan Automobile Manufacturers Association, Japan’s vehicle production showed continued operational stability in 2025, supporting sustained tire and component output. Large and diversified rubber processing across automotive, industrial goods, and consumer applications requires oils that provide consistent dispersion and flexibility. Naphthenic grades offer strong compatibility with both natural and synthetic rubber systems, reinforcing their structural preference.

The dominance is further supported by Asia’s natural rubber supply base. The International Rubber Study Group reported that Asia continues to account for the majority of global natural rubber production, with Thailand, Indonesia, and Vietnam remaining key contributors. Rubber compounds incorporating high natural rubber content benefit from naphthenic oils’ solvency profile and low-temperature stability. These functional advantages improve processing efficiency in extrusion, molding, and calendaring operations common across regional manufacturing hubs.

Additionally, naphthenic oils offer a favorable balance between performance and regulatory alignment compared to traditional high-aromatic grades. Their lower polycyclic aromatic content supports compliance with export-oriented manufacturing standards while maintaining cost efficiency relative to more heavily treated alternatives. Refinery infrastructure across East and Southeast Asia supports stable naphthenic base oil availability, enhancing supply reliability. The combination of technical suitability, compatibility with regional rubber feedstocks, and consistent production capacity sustains naphthenic oils’ leading 42% market share in Asia.

Based on Application:

- Tire Manufacturing

- Footwear

- Wire & Cable Covering

- Flooring Materials

- Adhesives & Sealants

- Others

Tire manufacturing dominates the Asia Rubber Process Oils market, accounting for approximately 54% of total application demand, primarily because Asia remains the global center of natural rubber production and tire processing capacity. The International Rubber Study Group reports that Thailand, Indonesia, Vietnam, and Malaysia collectively account for the majority of global natural rubber output, supplying raw materials directly into regional tire plants. High-volume tire production requires consistent rubber compounding at an industrial scale, where process oils are structurally incorporated to improve flexibility, dispersion of carbon black, and heat resistance. This material intensity establishes a direct linkage between tire output and process oil consumption.

Infrastructure and transport expansion further reinforce this dominance. The Asian Development Bank’s 2025 regional infrastructure updates highlight sustained investment in highways, logistics corridors, and urban transit systems across Southeast Asia. Increased freight movement and passenger mobility accelerate tire wear rates, expanding replacement demand beyond original equipment manufacturing. Unlike footwear or adhesives applications, tire production operates on standardized compound formulations with defined oil loading ratios, ensuring predictable and substantial oil intake per ton of rubber processed.

Export orientation also strengthens this application’s structural weight. United Nations Comtrade data show that Asian economies remain the leading exporters of rubber tires globally, underscoring sustained manufacturing throughput. Large integrated tire facilities require continuous and high-volume compounding operations, creating stable offtake agreements with process oil suppliers. The combination of raw material availability, infrastructure-driven mobility growth, and export-scale manufacturing, therefore, positions tire production as the dominant application segment within Asia’s rubber process oils market.

Asia Rubber Process Oils Market (2026-32): Regional Projection

China dominates the Asia Rubber Process Oils market, accounting for approximately 52% of regional demand, primarily because it serves as the largest industrial and automotive manufacturing base in the region. According to the National Bureau of Statistics of China, the country maintained robust industrial output growth in 2025, with manufacturing remaining a central contributor to overall economic activity. This industrial scale directly supports high-volume production of rubber goods, particularly tires and automotive components, which structurally incorporate process oils in compounding. As the largest producer of vehicles and industrial rubber products in Asia, China sustains an unmatched baseline demand for petroleum-derived rubber additives.

This dominance is reinforced by China’s integrated petrochemical and refining infrastructure. The International Energy Agency’s 2025 refining outlook highlights China as one of the world’s largest refining capacity holders, enabling domestic production of base oils and aromatic extracts used in rubber processing. Strong vertical integration between refineries, synthetic rubber producers, and tire manufacturers enhances cost efficiency and supply reliability. Such infrastructure depth allows Chinese producers to operate at significant economies of scale compared to other Asian countries that rely more heavily on imports.

Export orientation further strengthens China’s leadership position. United Nations Comtrade data consistently show China as a leading global exporter of rubber tires and industrial rubber products, reflecting sustained compounding throughput. Large manufacturing clusters in provinces such as Shandong and Zhejiang support concentrated tire production with continuous process oil intake. The combination of expansive industrial output, integrated refining capacity, and export-scale rubber manufacturing structurally positions China ahead of other Asian countries, supporting its estimated 52% market share in regional rubber process oil consumption.

Gain a Competitive Edge with Our Asia Rubber Process Oils Market Report:

- Asia Rubber Process Oils Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Asia Rubber Process Oils Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Asia Rubber Process Oils Market Policies, Regulations, and Product Standards

- Asia Rubber Process Oils Market Trends & Developments

- Asia Rubber Process Oils Market Dynamics

- Growth Factors

- Challenges

- Asia Rubber Process Oils Market Hotspot & Opportunities

- Asia Rubber Process Oils Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume in Kiloton

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Aromatic

- Paraffinic

- Naphthenic

- Treated Distillate Aromatic Extract (TDAE)

- Mild Extracted Solvent (MES)

- Distillate Aromatic Extract (DAE)

- Residual Aromatic Extract (RAE)

- Other specialty types

- By Application- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Tire Manufacturing

- Footwear

- Wire & Cable Covering

- Flooring Materials

- Adhesives & Sealants

- Others

- By End User Industry- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Automotive

- Industrial Manufacturing

- Construction

- Aerospace & Defense

- Consumer Products

- Energy & Utilities

- By Country

- China

- India

- Japan

- South Korea

- Southeast Asia

- Rest of Asia

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Market Size & Outlook

- China Rubber Process Oils Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume in Kiloton

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By Application- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By End User Industry- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Market Size & Outlook

- India Rubber Process Oils Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume in Kiloton

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By Application- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By End User Industry- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Market Size & Outlook

- Japan Rubber Process Oils Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume in Kiloton

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By Application- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By End User Industry- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Market Size & Outlook

- South Korea Rubber Process Oils Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume in Kiloton

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By Application- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By End User Industry- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Market Size & Outlook

- Southeast Asia Rubber Process Oils Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume in Kiloton

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By Application- Market Size & Forecast 2022-2032, USD Million & Kiloton

- By End User Industry- Market Size & Forecast 2022-2032, USD Million & Kiloton

- Market Size & Outlook

- Asia Rubber Process Oils Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Gandhar Oil Refinery Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Witmans Industries Pvt. Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Velvex Oils

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lodha Petro

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panama Petrochem Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CPC Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sinopec Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chevron

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Exxon Mobil

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- APAR Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PetroChina Company Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Indian Oil Corporation Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hindustan Petroleum Corporation Ltd (HPCL)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Idemitsu Kosan Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nynas AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gandhar Oil Refinery Ltd

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now