Mexico Diagnostic Labs Market Research Report: Growth Drivers & Forecast (2026-2032)

By Test Type (Pathology, Radiology & Imaging), By Pathology Test Type (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecula ... r Diagnostics, Genetic Testing), By Radiology Type (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), By Service Delivery Mode (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), By Disease Type (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), By End-User (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), and others Read more

- Healthcare

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Mexico Diagnostic Labs Market

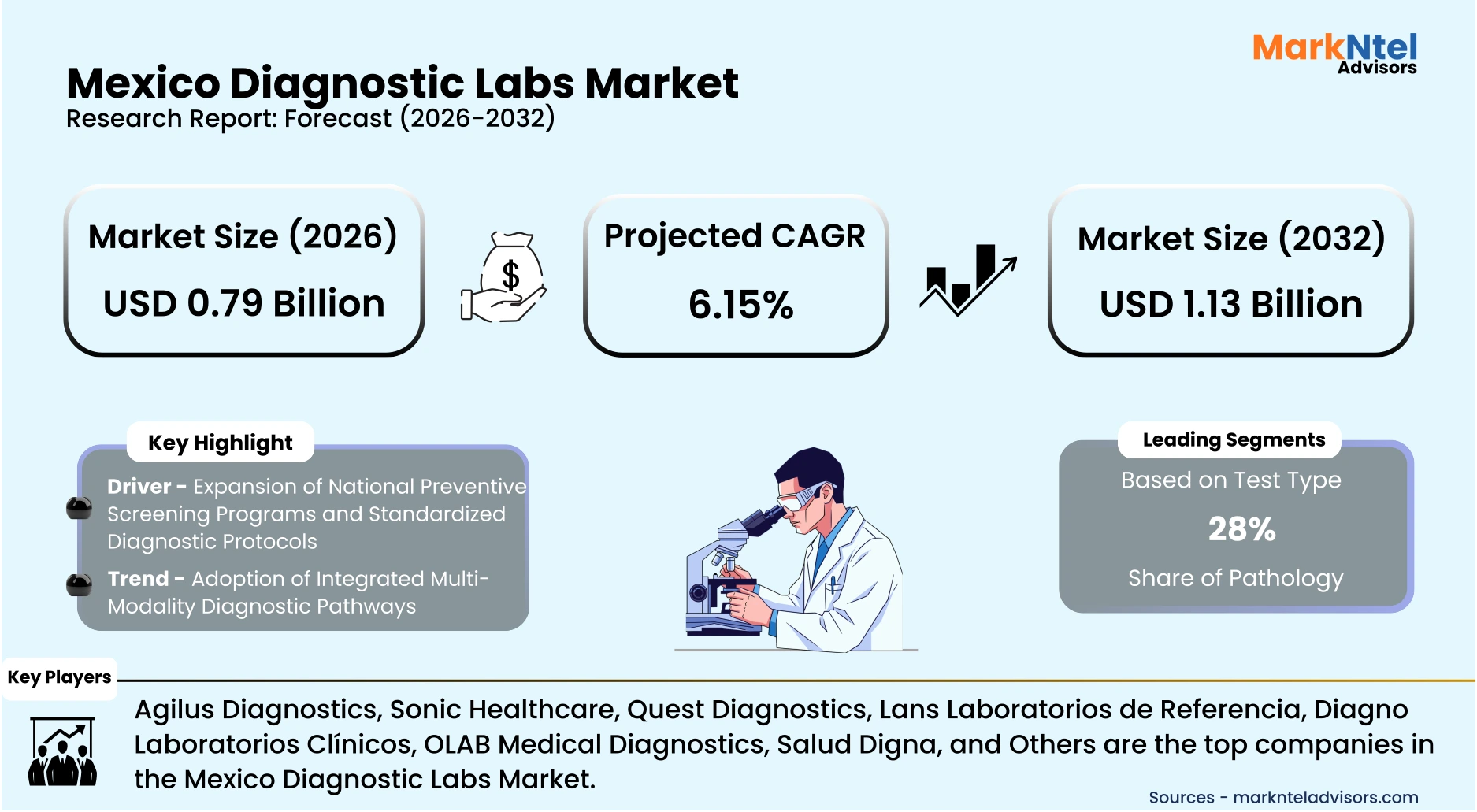

Projected 6.15% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 0.79 Billion

Market Size (2032)

USD 1.13 Billion

Base Year

2025

Projected CAGR

6.15%

Leading Segments

By End-User: Hospitals

Mexico Diagnostic Labs Market Report Key Takeaways:

- The Mexico Diagnostic Labs Market size was valued at USD 0.73 billion in 2025 and is projected to grow from USD 0.79 billion in 2026 to USD 1.13 billion by 2032, exhibiting a CAGR of 6.15% during the forecast period.

- Northern Mexico and Central Mexico are the leading regions with a significant share of 35% and 18%, respectively, in 2026.

- By Test Type, the Pathology Test segment represented a significant share of about 28% in the Mexico Diagnostic Labs Market in 2026.

- By End-User, the Hospitals seized a significant share of about 38% in the Mexico Diagnostic Labs Market in 2026.

- Leading Diagnostic Labs Companies in Mexico are Agilus Diagnostics, Sonic Healthcare, Quest Diagnostics, Lans Laboratorios de Referencia, Diagno Laboratorios Clínicos, OLAB Medical Diagnostics, Salud Digna, and Others.

Market Insights & Analysis: Mexico Diagnostic Labs Market (2026-32):

The Mexico Diagnostic Labs market size was valued at USD 0.73 billion in 2025 and is projected to grow from USD 0.79 billion in 2026 to USD 1.13 billion by 2032, exhibiting a CAGR of 6.15% during the forecast period, i.e., 2026-32.

Mexico’s diagnostic laboratories market has expanded on the back of sustained health system financing and demographic shifts. The 2026 Federal Expenditure Budget approved health allocations exceeding USD 53 billion, reflecting prioritization of medical infrastructure and laboratory capacity expansion by the Ministry of Finance. According to the World Bank’s 2025 demographic update, over 8% of Mexico’s population is aged 65 or above, increasing chronic disease monitoring requirements. This aging cohort directly elevates recurrent testing volumes in both public hospitals and private clinical networks.

Current market conditions reflect institutional modernization and regulatory strengthening. In 2025, Mexico’s health regulator COFEPRIS implemented updated digital submission protocols for in vitro diagnostic device approvals, accelerating equipment certification timelines. A major government initiative is underway to build 31 new hospitals and 12 healthcare centers by late 2025 , aiming to expand service capacity and access in underserved regions. Private hospital operators such as Grupo Ángeles publicly announced laboratory automation upgrades during 2025 to enhance throughput and reduce turnaround time . These initiatives collectively support higher service capacity and improved diagnostic accessibility.

Economic resilience further reinforces market performance. Corporate and preventive health programs expanded as large manufacturing employers in northern industrial corridors strengthened occupational screening requirements in 2026. The National Development Plan 2025–2030 emphasizes universal healthcare access and digital medical records integration, indirectly supporting laboratory information system adoption. These policy-backed structural improvements stimulate both test volumes and technology deployment.

Looking ahead, infrastructure and digitalization strategies are expected to sustain expansion. The Inter-American Development Bank reported ongoing 2026 financing for public hospital modernization projects, including laboratory capacity upgrades. Rising urbanization, with over 81% of the population residing in urban areas as per UN 2025 data, increases proximity to diagnostic facilities and recurring outpatient testing. Institutional procurement reforms promoting transparent public tenders enhance equipment investment confidence. Together, demographic pressure, policy continuity, and technology integration underpin positive long-term market prospects.

Mexico Diagnostic Labs Market Scope:

| Category | Segments |

|---|---|

| By Test Type | (Pathology, Radiology & Imaging), |

| By Pathology Test Type | (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecular Diagnostics, Genetic Testing), |

| By Radiology Type | (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), |

| By Service Delivery Mode | (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), |

| By Disease Type | (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), |

| By End-User | (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), |

Mexico Diagnostic Labs Market Driver:

Expansion of National Preventive Screening Programs and Standardized Diagnostic Protocols

The most influential structural driver accelerating Mexico’s diagnostic labs market is the institutionalization of nationwide preventive screening under federal health strategies. In 2025, Mexico’s Ministry of Health reinforced early detection campaigns for diabetes, cervical cancer, and breast cancer through standardized screening packages delivered across primary care units under IMSS-Bienestar and state health systems. These programs mandate laboratory-based glucose testing, cytology, and biomarker analysis as first-line diagnostic tools. Because screening is protocol-driven and publicly funded, it generates recurring and volume-based pathology demand independent of short-term economic cycles.

The measurable demand impact is reflected in structured testing requirements embedded in clinical guidelines. Official care pathways require routine HbA1c monitoring for diabetes management, lipid profiling for cardiovascular risk stratification, and cytology testing for women within defined age brackets. Public health units must comply with these standardized diagnostic algorithms to qualify for federal transfers and performance reporting. This policy-linked obligation increases aggregate test volumes nationwide, particularly in pathology disciplines such as clinical chemistry, hematology, and immunology.

The driver has intensified as federal authorities prioritize early detection to reduce long-term treatment expenditures. Preventive diagnostics cost substantially less than late-stage hospital interventions, encouraging government financing toward laboratory-centered screening. Institutional healthcare providers, therefore, expand laboratory capacity to meet protocol compliance targets and population coverage metrics. Because screening programs are embedded within universal service entitlements, demand expansion reflects systemic public health policy rather than discretionary testing behavior, materially enlarging market size and operational throughput.

Mexico Diagnostic Labs Market Trend:

Adoption of Integrated Multi-Modality Diagnostic Pathways

Mexico’s diagnostic laboratory sector is increasingly moving toward integrated multi-modality diagnostic pathways, where laboratories coordinate more closely with imaging centers, molecular testing services, and clinical data systems to provide holistic diagnostic outputs. Public and private healthcare institutions are aligning with the Norma Oficial Mexicana standard for electronic health record interoperability, encouraging structured linkage between lab results and diagnostic imaging reports. This trend reflects greater emphasis on comprehensive diagnostic workflows rather than isolated test ordering.

Real-world utilization data underscore this shift, according to Secretaría de Salud service reports. Combined diagnostic clusters, e.g., metabolic panels followed by imaging referrals, have risen in clinical pathways for chronic conditions. Concurrently, professional associations in Mexico have published guidelines advocating integrated reporting for oncology and cardiometabolic patients, requiring pathology, radiology, and molecular results to be synthesized in a single clinical profile.

Another observable trend is the growing uptake of quality accreditation frameworks, such as ISO-15189 alignment, by laboratories seeking formal certification. This trend towards standardized, interoperable diagnostics supports enhanced data consistency and cross-facility comparability . Together, these patterns indicate a sustained movement toward coordinated, multi-modality diagnostics as a defining structural trend in Mexico’s laboratory market.

Mexico Diagnostic Labs Market Opportunity:

Digital Pathology and Tele-Diagnostics Integration

A compelling opportunity lies in digital pathology and tele-diagnostics deployment enabled by Mexico’s national digital health agenda. In 2025, the Ministry of Health advanced electronic medical record interoperability guidelines to standardize clinical data exchange across institutions . This structural shift creates demand for laboratory information systems compatible with remote reporting and image-sharing platforms. Digital integration reduces geographic disparities and supports specialist consultation across underserved regions.

The opportunity translates into tangible demand as public hospitals seek workflow optimization. Academic medical centers are increasingly exploring digital pathology models that connect regional laboratories with tertiary care units for remote slide interpretation, aiming to improve diagnostic turnaround times and subspecialty access in complex cases. This reduces turnaround times and improves diagnostic accuracy in oncology and complex cases. Technology vendors offering scalable, cloud-enabled systems can address integration requirements without heavy on-site infrastructure investments. Such flexibility is particularly advantageous for new entrants targeting mid-tier facilities.

Emerging players benefit from lower entry barriers compared with traditional equipment-intensive models. National digital health coordination initiatives are shaping procurement decisions toward systems capable of secure data sharing and cross-institutional integration, creating structural demand for interoperable laboratory and clinical IT solutions. Smaller technology providers can differentiate through cybersecurity compliance and modular software design aligned with federal standards. As interoperability becomes mandatory across institutional networks, digitally focused entrants gain competitive leverage. This structural digitalization wave, therefore, presents scalable growth potential for agile market participants.

Mexico Diagnostic Labs Market Challenge:

Skilled Workforce Shortages in Specialized Diagnostic Services

Mexico’s diagnostic laboratory sector faces a structural shortage of highly specialized professionals, particularly in molecular pathology, cytogenetics, and laboratory informatics. The Regulatory disclosures indicate that specialist physicians remain concentrated in high-density urban markets, creating regional capacity gaps that constrain service expansion and advanced d iagnostic deployment in underserved state areas. According to the OECD Health at a Glance 2025 report, Mexico had 2.7 practicing doctors per 1,000 population , which is noticeably lower than the OECD average of 3.9 doctors per 1,000 population. This reflects comparatively lower physician density in Mexico relative to other developed economies.

This shortage measurably impacts operational performance, as regional laboratories frequently rely on centralized urban facilities for complex test validation. Rising demand for diagnostic services has intensified workload volumes across laboratory networks, straining processing capacity and reporting efficiency. The shortage of highly specialized pathology expertise further delays the interpretation of molecular oncology markers and high-complexity immunological assays. Smaller private laboratories report difficulty recruiting certified personnel, constraining service diversification into higher-margin molecular testing segments.

The constraint materially restricts market scalability by limiting the adoption of advanced diagnostic platforms that require trained interpretation. Capital investment in automation or molecular analyzers becomes commercially risky without adequate human expertise. Geographic disparities further inhibit equitable service expansion beyond Tier-1 cities. As a result, workforce scarcity functions as a systemic barrier to modernization, integration, and competitive differentiation within Mexico’s diagnostic laboratory market.

Mexico Diagnostic Labs (2026-32) Market Segmentation Analysis:

The Mexico Diagnostic Labs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Test Type:

- Pathology

- Radiology & Imaging

Pathology represents the leading segment within Mexico’s diagnostic labs market with a market share of 28% due to its essential role in chronic disease management. National epidemiological bulletins in 2025 reported a high prevalence of diabetes and cardiovascular conditions, both requiring routine biochemical and hematological testing. Public healthcare institutions mandate periodic laboratory monitoring under standardized treatment protocols. This structural clinical requirement ensures recurring demand independent of discretionary spending patterns.

Pathology testing supports primary care screening initiatives, maternal health assessments, and infectious disease surveillance programs. Cytopathology is widely performed in Mexico, especially Pap smear screening for cervical cancer and histopathology interpretation of biopsies . Molecular diagnostic research on HPV PCR combined with Pap test data reflects active advanced cytopathology diagnostics in practice. Compared with radiology, pathology requires lower per-test capital intensity, enabling broader geographic penetration. This scalability supports higher aggregate test volumes nationwide.

End-user demand characteristics also sustain dominance. Hospitals and physician clinics rely on pathology panels for diagnostic confirmation prior to advanced imaging referral. Corporate health programs implement routine blood screening for workforce wellness compliance. Government facilities prioritize laboratory diagnostics as first-line evaluation tools in community health centers. Consequently, pathology maintains structural volume superiority across institutional and preventive healthcare settings.

Based on End-User:

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

Hospitals constitute the dominant end-user segment with a market share of 38% due to their central role in inpatient and emergency diagnostics. Official federal reporting on health infrastructure indicates that by late 2025, Mexico was implementing plans to open 31 new hospitals and 12 primary care clinics across the country as part of a modernization initiative involving IMSS, ISSSTE, and IMSS Bienestar, reflecting ongoing expansion of hospital capacity. Acute care settings require immediate laboratory and imaging support for surgical, trauma, and intensive care cases. This high-acuity demand ensures consistent utilization rates.

Policy-driven infrastructure investments further consolidate hospital leadership. The federal government’s 2026 hospital modernization agenda includes equipment upgrades for tertiary and specialty centers. Hospitals receive priority budget allocations for diagnostic expansion compared with smaller outpatient clinics. Integration of laboratory services within hospital information systems enhances workflow efficiency and test ordering volumes. These structural advantages elevate hospital-based demand concentration.

End-user intensity also differentiates this segment. Hospitals manage complex cases requiring multidisciplinary diagnostic workflows, increasing per-patient test frequency. Institutional procurement contracts facilitate bulk purchasing of consumables and maintenance services. Private hospital groups similarly invest in on-site laboratory capabilities to maintain service quality standards. Therefore, hospitals sustain market dominance through scale, clinical complexity, and policy-supported investment.

Mexico Diagnostic Labs Market (2026-32) Regional Analysis:

Northern Mexico represents the leading region in Mexico’s diagnostics laboratories market with a market share of 35%, supported by strong economic performance, advanced healthcare infrastructure, and high diagnostic service penetration across both public and private sectors.

The region accounts for the largest share of diagnostic testing volumes in the country, driven by higher healthcare expenditure per capita and greater private sector participation compared to southern regions.

These states demonstrate higher insurance coverage, corporate healthcare programs, and employer-sponsored medical benefits, all of which increase routine and preventive diagnostic testing rates.

Laboratory networks like Salud Digna maintain a strong operational presence in the northern corridor, supporting high patient throughput and expanded service portfolios.

Additionally, higher levels of urbanization and income concentration translate into stronger demand for preventive health check-ups, chronic disease monitoring, and specialty diagnostics, reinforcing the region’s leading market position.Top of Form

Apart from Northern Mexico, Central Mexico is another leading region, with a market share of 18%, particularly in the most popular diagnostic tests, those associated with routine check-ups and the management of chronic conditions. Popular pathology tests like urine analysis, hematology, and 37-element blood chemistry, which are standard for evaluating metabolic health they are mainly leading the market in the form of preventative "Check -Ups".Bottom of Form

Gain a Competitive Edge with Our Mexico Diagnostic Labs Market Report:

- The Mexico Diagnostic Labs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Mexico Diagnostic Labs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Mexico Diagnostic Labs Market Policies, Regulations, and Product Standards

- Mexico Diagnostic Labs Market Trends & Developments

- Mexico Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- Mexico Diagnostic Labs Market Hotspot & Opportunities

- Mexico Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Pathology

- Radiology & Imaging

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- Walk-in Testing

- Home Sample Collection

- Mobile Diagnostic Units

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- Infectious Diseases

- Oncology

- Diabetes & Endocrinology

- Cardiology

- Neurology

- Nephrology

- Gastroenterology

- Gynecology & Obstetrics

- Respiratory Disorders

- Orthopedics

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

- By Region- Market Size & Forecast 2022-2032, USD Million

- Northern

- Central

- Western

- Southern

- Southeastern

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Pathology Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Radiology & Imaging Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Diagnostic Labs Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Agilus Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sonic Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quest Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lans Laboratorios de Referencia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Diagno Laboratories Clinicos

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- OLAB Medical Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Salud Digna

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agilus Diagnostics

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now