GCC Medical Consumables Market Research Report: Trends & Forecast (2026-2032)

By Healthcare Settings Hospitals, (General Hospitals, Specialty Hospitals, Multispecialty Hospitals), Specialty Clinics, Others), By Usage (Surgical, Non-Surgical), By Division (Ex ... am Gloves, Surgeons’ Gloves, Diagnostics Consumables, O.R. Consumables (non-glove), Anaesthesia Consumables, Advanced Wound Care, Vascular Access, Laboratory Consumables, Respiratory Consumables, EVS / Infection Control, Personal Protection (non-glove PPE), Urology, Personal Care, Primary + Preventive Care, SPT, Ready Care, Rehab & Fall Prevention, Medline Textiles, Others / Misc)., By Clinical Specialties (Cardiology, Gynecology, Urology, Orthopedics and Trauma, General Surgery and Laparoscopic Surgery, Nephrology and Dialysis, Oncology Medical and Surgical, Respiratory and Pulmonology, Gastroenterology, Vascular Surgery and Endovascular Procedures, Anesthesiology and Perioperative Care, Others), By Material (Disposable, Non-Disposable), and others Read more

- Healthcare

- Feb 2026

- Pages 225

- Report Format: PDF, Excel, PPT

GCC Medical Consumables Market

Projected 4.73% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 495.22 Million

Market Size (2032)

USD 635.29 Million

Base Year

2025

Projected CAGR

4.73%

Leading Segments

By Materials: Disposable

GCC Medical Consumables Market Report Key Takeaways:

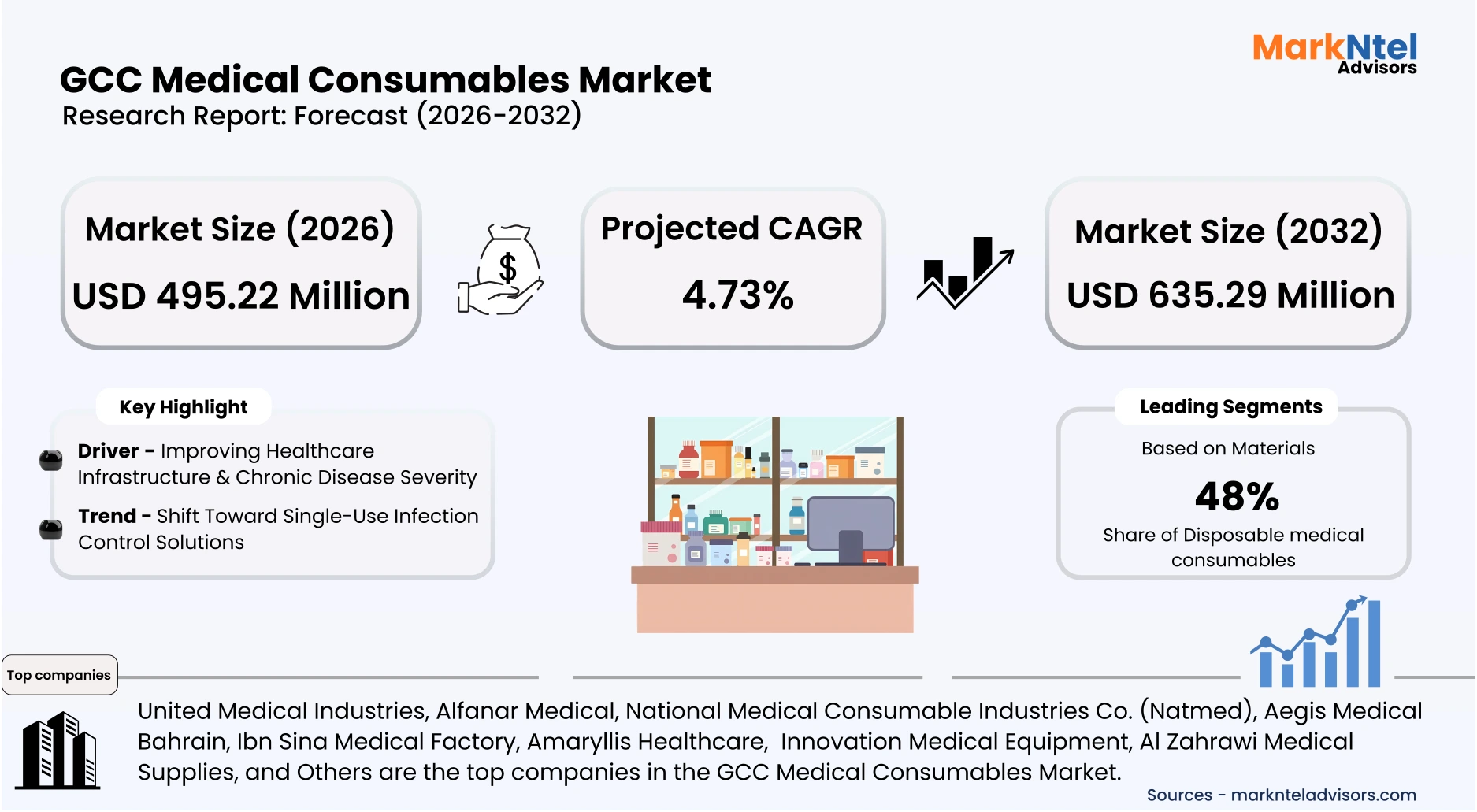

- The GCC Medical Consumables Market size was valued at USD 459.75 million in 2025 and is projected to grow from USD 495.22 million in 2026 to USD 635.29 million by 2032, exhibiting a CAGR of 4.73% during the forecast period.

- By Clinical Specialties, the General Surgery and Laparoscopic Surgery segment represented a significant share of about 39% in the GCC Medical Consumables Market in 2026.

- By Material, the disposable segment presented a significant share of about 48% in the GCC Medical Consumables Market in 2026.

- Leading Medical Consumables Companies in the GCC are United Medical Industries, Alfanar Medical, National Medical Consumable Industries Co. (Natmed), Aegis Medical Bahrain, Ibn Sina Medical Factory, Amaryllis Healthcare, Almaha Medical Supplies Factory, Innovation Medical Equipment, Al Zahrawi Medical Supplies, and Others.

Market Insights & Analysis: GCC Medical Consumables Market (2026-32):

The GCC Medical Consumables market size was valued at USD 459.75 million in 2025 and is projected to grow from USD 495.22 million in 2026 to USD 635.29 million by 2032, exhibiting a CAGR of 4.73% during the forecast period, i.e., 2026-32.

The GCC medical consumables industry has expanded steadily over the past decade, supported by population growth, rising life expectancy, and sustained public healthcare spending. According to the UN Population Division, the GCC population aged above 60 years is projected to cross 5.5 million in 2050, directly increasing demand for surgical procedures and hospital-based care. Institutional end users, particularly public hospitals, account for a substantial share of consumables use due to high patient throughput and standardized procurement frameworks. This concentration of demand has enabled stable baseline consumption volumes across gloves, wound care, and perioperative supplies.

Healthcare infrastructure expansion remains a central contributor to current market conditions. According to Saudi Arabia’s Ministry of Health, new hospitals and specialized medical cities were under development in 2025 as part of the Vision 2030 healthcare transformation programs . These projects emphasize capacity expansion, infection prevention, and surgical readiness, directly supporting recurring procurement of disposable medical consumables. Regulatory harmonization under the Gulf Health Council has further improved cross-border product approvals, reducing entry barriers for compliant manufacturers and accelerating technology adoption.

Industry-led investments have strengthened local supply resilience. In 2025, Qatar’s Ministry of Commerce and Industry launched the Qatar National Manufacturing Strategy 2024–2030 , a comprehensive roadmap designed to enhance local production capabilities and diversify the industrial base, including pharmaceutical and healthcare sectors as priority areas for import substitution and economic growth. Company initiatives focusing on localization, sterilization automation, and quality certification upgrades have enhanced regional production depth. These efforts align with government mandates to improve supply security and reduce exposure to global logistics disruptions experienced in earlier years.

Looking ahead, sustained demand is expected due to continued public-sector dominance in healthcare delivery and rising surgical intervention rates. According to analyses of GCC health data and WHO‑aligned reports, lifestyle‑related risk factors such as physical inactivity, poor diet, and obesity contribute significantly to the burden of non‑communicable diseases, including cardiovascular conditions and diabetes in the region, driving increased clinical demand and complex care management. Which logically contributes to increased surgical and clinical interventions.

GCC Medical Consumables Market Recent Developments:

- 2025: In 2025, Pure Health Holding strengthened its strategic collaboration with Sinopharm Group to enhance the supply and localised distribution of medical consumables, including syringes, diagnostic kits, PPE, and hospital disposables, across the UAE and the wider GCC.

- 2026: Saudi Arabia’s National Unified Procurement Company (NUPCO) signed multiple long-term framework agreements with local and international manufacturers for the supply and localized production of essential medical consumables, including IV sets, syringes, gloves, and wound care products.

GCC Medical Consumables Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Settings | Hospitals, (General Hospitals, Specialty Hospitals, Multispecialty Hospitals), Specialty Clinics, Others), |

| By Usage | Surgical, Non-Surgical |

| By Division | Exam Gloves, Surgeons’ Gloves, Diagnostics Consumables, O.R. Consumables (non-glove), Anaesthesia Consumables, Advanced Wound Care, Vascular Access, Laboratory Consumables, Respiratory Consumables, EVS / Infection Control, Personal Protection (non-glove PPE), Urology, Personal Care, Primary + Preventive Care, SPT, Ready Care, Rehab & Fall Prevention, Medline Textiles, Others / Misc |

| By Clinical Specialties | Cardiology, Gynecology, Urology, Orthopedics and Trauma, General Surgery and Laparoscopic Surgery, Nephrology and Dialysis, Oncology Medical and Surgical, Respiratory and Pulmonology, Gastroenterology, Vascular Surgery and Endovascular Procedures, Anesthesiology and Perioperative Care, Others |

| By Material | Disposable, Non-Disposable), and others |

GCC Medical Consumables Market Driver:

Improving Healthcare Infrastructure & Chronic Disease Severity

Multiple region-specific developments are fueling demand for medical consumables throughout the GCC. The expansion of healthcare infrastructure plays a key role; for example, Saudi Arabia’s ongoing efforts to boost hospital bed capacity under Vision 2030 result in more inpatient admissions and surgical procedures. This growth directly drives higher consumption of gloves, syringes, IV sets, and wound care products.

The GCC also records some of the highest diabetes prevalence rates globally, particularly in Saudi Arabia, Kuwait, and the UAE, resulting in continuous demand for insulin delivery devices, blood glucose test strips, and lancets. In addition, strengthened infection prevention and control regulations across public and private healthcare facilities have accelerated the adoption of single-use consumables, including surgical masks, gowns, and sterilization products.

The growing private healthcare sector and medical tourism market in the UAE have further driven demand for premium-quality disposable medical products to meet international accreditation standards . Moreover, increasing emphasis on preventive healthcare and routine diagnostics has led to higher utilization of diagnostic consumables across primary care centers and laboratories. These developments underpin a resilient, long-term growth trajectory for the GCC medical consumables market.

GCC Medical Consumables Market Opportunity:

Localised Manufacturing for Import Substitution offering Lucrative Opportunities

A compelling opportunity exists for new and emerging players through localised manufacturing aimed at import substitution. Structural changes in GCC industrial policy have created favorable entry conditions for domestic production of medical consumables. In 2026, the UAE’s Ministry of Industry and Advanced Technology expanded incentives under the “Make it in the Emirates” program to include medical disposables, offering land access, financing facilitation, and fast-track regulatory clearances. These measures lower entry barriers for smaller manufacturers .

This opportunity translates into tangible demand through guaranteed institutional offtake. Government procurement frameworks increasingly prioritize locally manufactured products that meet quality standards. According to official UAE federal procurement guidelines issued in 2025, preference scoring mechanisms were introduced for domestically produced healthcare supplies . This policy-driven demand assurance enables new entrants to scale production rapidly without competing solely on price against multinational incumbents.

Localised manufacturing is particularly advantageous for smaller players due to reduced logistics costs and faster response times. Import dependency exposes suppliers to freight volatility and regulatory delays, whereas local facilities align closely with hospital demand cycles. The Oman Vision of 2040 aims to improve local manufacturing capacity for medical products and equipment. Small and medium-sized enterprises have entered the market and are now manufacturing consumables , including masks, gloves, and testing kits, which were previously imported in full quantity.

GCC Medical Consumables Market Challenge:

Regulatory Compliance and Certification Complexities Impeding Market Growth

Regulatory compliance remains the most critical challenge constraining market scalability. Medical consumables are subject to stringent quality, safety, and traceability requirements, which have intensified in recent years. In 2025, Bahrain’s National Health Regulatory Authority revised its medical device conformity assessment rules, introducing expanded documentation, post-market surveillance obligations, and shorter license renewal cycles . These changes increased compliance costs for manufacturers and distributors alike.

The measurable impact on market participants is evident in extended approval timelines and higher operational expenditures. According to enforcement disclosed by government's enforcement, several imported consumable batches faced clearance delays due to incomplete technical files. Such disruptions affect inventory planning, hospital supply continuity, and supplier cash flows, particularly for smaller firms with limited regulatory teams.

This challenge materially restricts market expansion by raising entry and scaling thresholds. High compliance costs discourage new entrants and slow product portfolio expansion. International regulatory benchmarking assessments released in 2025 by multilateral health and standards organizations indicate that fragmented medical device and consumables regulations across GCC member states reduce economies of scale. Until further harmonization of regulatory standards and centralized approval mechanisms is achieved, regulatory complexity is expected to remain a structural constraint on market scalability, investment efficiency, and cross-border trade integration within the GCC medical consumables sector.

GCC Medical Consumables Market Trend:

Shift Toward Single-Use Infection-Control Solutions

A significant trend reshaping the GCC medical consumables market is the accelerated shift toward single-use, infection-control-oriented solutions. This trend has intensified following stricter hospital-acquired infection prevention protocols. In 2026, the Gulf Health Council issued updated regional guidelines emphasizing disposable usage in high-risk clinical environments. These standards have structurally altered procurement preferences across public hospitals.

The trend is driving changes across the value chain. Hospitals are redesigning surgical workflows to minimize sterilization dependency, while suppliers are investing in high-throughput disposable production lines. GCC infection prevention and control adoption assessments published in 2025 by international public health authorities indicate that healthcare facilities implementing single-use clinical protocols have achieved measurable reductions in contamination and cross-infection risks. These documented outcomes have strengthened institutional confidence in disposable-intensive care models, particularly within high-risk clinical environments where infection control performance is closely monitored.

Persistence of this trend is supported by regulatory enforcement and operational efficiency gains. Disposable solutions reduce turnaround times and labor costs associated with reprocessing. Government hospital performance audits published in 2024 by regional supreme audit institutions link disposable adoption with improved operating room utilization rates. These structural benefits ensure long-term influence on procurement strategies and market evolution .

GCC Medical Consumables Market (2026-32) Segmentation Analysis:

The GCC Medical Consumables Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as:

Based on Clinical Specialties:

- Cardiology

- Gynecology

- Urology

- Orthopedics and Trauma

- General Surgery and Laparoscopic Surgery

- Nephrology and Dialysis

- Oncology Medical and Surgical

- Respiratory and Pulmonology

- Gastroenterology

- Vascular Surgery and Endovascular Procedures

- Anesthesiology and Perioperative Care

- Others

General Surgery and Laparoscopic Surgery dominate consumables demand with a market share of 39% due to high procedural volumes and standardized consumable usage per case. International health data from 2025 indicates that minimally invasive procedures are accounting for a larger share of surgical activity globally, with hospitals in the GCC reflecting a similar shift. These procedures require extensive use of sterile drapes, trocar-related accessories, and disposable surgical tools.

Policy further reinforces this dominance. Hospitals and health authorities across the GCC, particularly in the United Arab Emirates, are increasingly adopting advanced minimally invasive and robotic surgical technologies as part of broader healthcare modernization efforts. In 2025, over 145 successful robotic surgeries were performed at Dubai Hospital since the launch of its programme, illustrating expanding utilization of such procedures that rely heavily on disposable consumables like sterile drapes, trocar ports, and single-use instrument kits .

This trend reflects strategic investments in surgical innovation and clinical training that reinforce demand intensity within the general surgery and laparoscopic segment. End-user demand characteristics also favor this segment. General surgery departments operate at high utilization rates and serve diverse patient populations. Regional healthcare performance reports issued in 2025 associate laparoscopic approaches with faster patient recovery and fewer postoperative complications, accelerating procedural uptake. These efficiencies support the continued leadership of the segment.

Based on Materials:

- Disposable

- Non-Disposable

Disposable medical consumables dominate the market with a market share of 48% as infection control remains a core regulatory and operational priority. Updated healthcare safety standards and hospital procurement policies in the UAE increasingly promote the use of single-use supplies over reusable products across surgical and diagnostic applications to minimize the risk of cross-contamination and healthcare-associated infections.

Investment flows further support dominance. According to financial disclosures from regional development banks in 2026, multiple funding programs prioritized automation and capacity expansion for disposable manufacturing lines. These investments enhance economies of scale and reduce unit costs, reinforcing competitive advantages.

End-user demand patterns also sustain leadership. Hospitals prioritize disposables to reduce sterilization overhead and compliance risks. Recent academic assessments using life-cycle costing frameworks highlight that, for many clinical applications, disposable medical products can offer cost efficiencies once sterilization labor, energy consumption, and infection-related risks are factored into total operating costs. These structural advantages ensure the continued dominance of disposable materials .

GCC Medical Consumables Market (2026-32) Regional Analysis:

Saudi Arabia is the most dominant country with 35% share in the GCC medical consumables market due to structural, regulatory, and demand-side advantages. The country benefits from the largest healthcare infrastructure and the highest hospital capacity in the GCC. According to the latest Saudi Healthcare Establishments and Workforce Statistics 2024, the Kingdom operates 516 hospitals with extensive primary care networks and over 23.4 hospital beds per 10,000 population, representing the broadest institutional base for consumables demand across emergency, surgical, diagnostic, and outpatient settings.

Regulatory and procurement advantages further reinforce Saudi Arabia’s regional leadership. The Saudi Food and Drug Authority (SFDA) and centralized procurement processes under the National Unified Procurement Company (NUPCO) create a structured market environment where digitization and streamlined device registration support faster market access for medical consumables. Regional industry insights note that NUPCO’s digital procurement platform actively consolidates high-volume contracts and shortens tender cycles across hundreds of facilities, strengthening supplier responsiveness and aggregate purchasing intensity.

End-user concentration and industry presence also contribute to Saudi Arabia’s dominant position. The Kingdom has a large and growing chronic disease burden, with non-communicable diseases accounting for approximately 70% of all deaths and adult diabetes prevalence near 18%, driving elevated recurring utilization of consumables such as syringes, diagnostic strips, and wound care products. Combined with ongoing investment programs under Saudi Vision 2030, which aims to expand private sector healthcare participation and build integrated health clusters, the high procedural and preventive care volume in Saudi Arabia supports intensive use of medical consumables across the health system.

These interlinked structural expansions, regulatory efficiencies, and concentrated demand patterns position Saudi Arabia as the most influential and dominant GCC market for medical consumables adoption.

Gain a Competitive Edge with Our GCC Medical Consumables Market Report:

- The GCC Medical Consumables Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The GCC Medical Consumables Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Medical Consumables Market Policies, Regulations, and Product Standards

- GCC Medical Consumables Market Trends & Developments

- GCC Medical Consumables Market Dynamics

- Growth Factors

- Challenges

- GCC Medical Consumables Market Hotspot & Opportunities

- GCC Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- General Hospitals

- Specialty Hospitals

- Multispecialty Hospitals

- Specialty Clinics

- Others

- Hospitals

- By Usage- Market Size & Forecast 2022-2032, USD Million

- Surgical

- Non-Surgical

- By Division- Market Size & Forecast 2022-2032, USD Million

- Exam Gloves

- Surgeons’ Gloves

- Diagnostics Consumables

- O.R. Consumables (non-glove)

- Anaesthesia Consumables

- Advanced Wound Care

- Vascular Access

- Laboratory Consumables

- Respiratory Consumables

- EVS / Infection Control

- Personal Protection (non-glove PPE)

- Urology

- Personal Care

- Primary + Preventive Care

- SPT

- Ready Care

- Rehab & Fall Prevention

- Medline Textiles

- Others / Misc.

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- Cardiology

- Gynecology

- Urology

- Orthopedics and Trauma

- General Surgery and Laparoscopic Surgery

- Nephrology and Dialysis

- Oncology Medical and Surgical

- Respiratory and Pulmonology

- Gastroenterology

- Vascular Surgery and Endovascular Procedures

- Anesthesiology and Perioperative Care

- Others

- By Material- Market Size & Forecast 2022-2032, USD Million

- Disposable

- Non-Disposable

- By Country

- Saudi Arabia

- United Arab Emirates (UAE)

- Bahrain

- Kuwait

- Oman

- Qatar

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- United Arab Emirates (UAE) Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- GCC Medical Consumables Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- United Medical Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alfanar Medical

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Medical Consumable Industries Co. (Natmed)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aegis Medical Bahrain

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ibn Sina Medical Factory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amaryllis Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Almaha Medical Supplies Factory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Innovation Medical Equipment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Zahrawi Medical Supplies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- United Medical Industries

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now