Indonesia Diagnostic Labs Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Test Type (Pathology, Radiology & Imaging), By Pathology Test Type (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecula ... r Diagnostics, Genetic Testing), By Radiology Type (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), By Service Delivery Mode (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), By Disease Type (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), By End-User (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), and others Read more

- Healthcare

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Indonesia Diagnostic Labs Market

Projected 7.59% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 3.32 Billion

Market Size (2032)

USD 5.15 Billion

Base Year

2025

Projected CAGR

7.59%

Leading Segments

By End-User Hospitals

Indonesia Diagnostic Labs Market Report Key Takeaways:

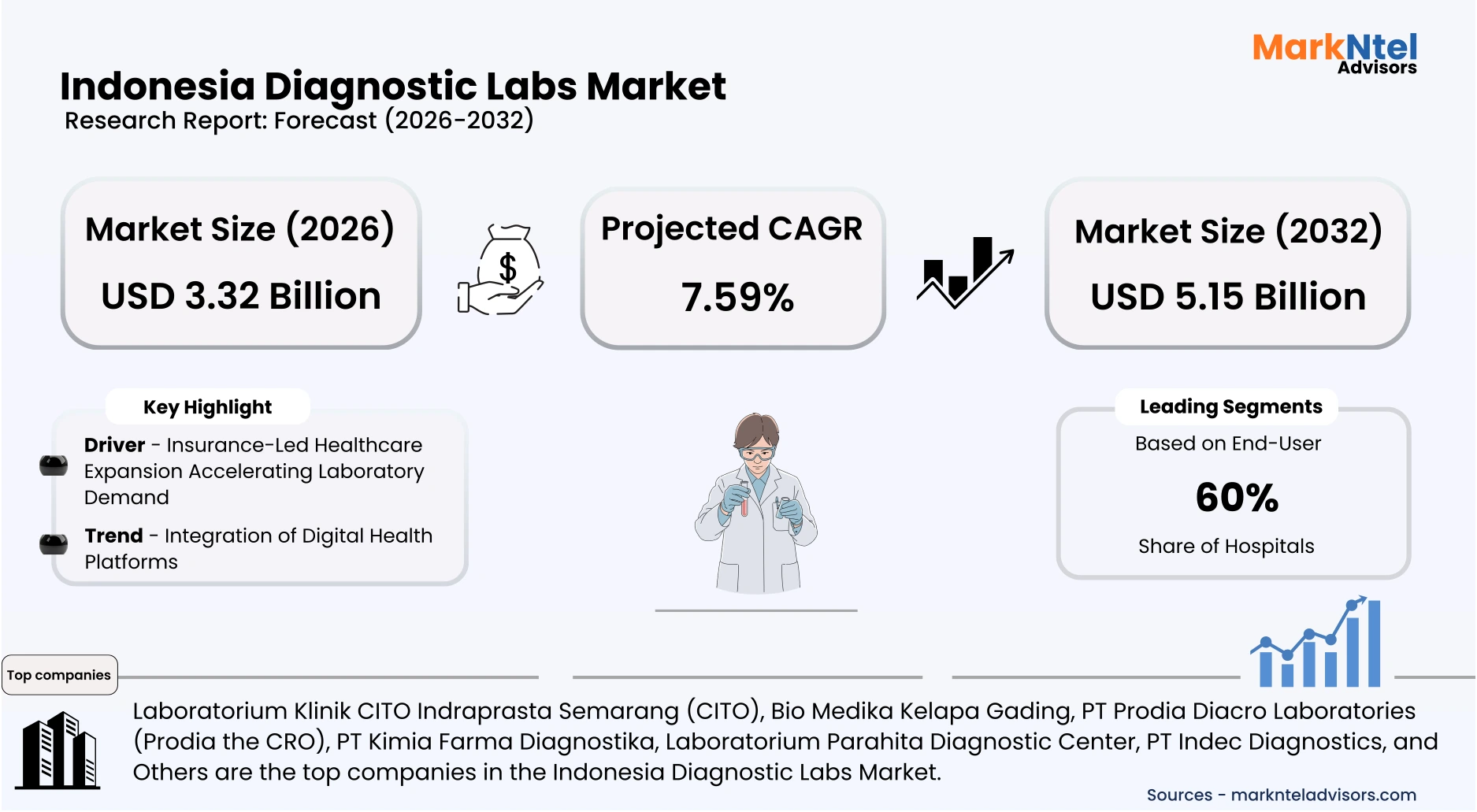

- Indonesia Diagnostic Labs Market size was valued at USD 2.91 billion in 2025 and is projected to grow from USD 3.32 billion in 2026 to USD 5.15 billion by 2032, exhibiting a CAGR of 7.59% during the forecast period.

- Java is the leading region with a significant share of 60% in 2026.

- By Test Type, the Pathology Test segment represented a significant share of about 30% in the Indonesia Diagnostic Labs Market in 2026.

- By End-User, the Hospitals seized a significant share of about 60% in the Indonesia Diagnostic Labs Market in 2026.

- Leading Diagnostic Labs Companies in Indonesia are Laboratorium Klinik CITO Indraprasta Semarang (CITO), Bio Medika Kelapa Gading, PT Prodia Diacro Laboratories (Prodia the CRO), PT Kimia Farma Diagnostika, Laboratorium Parahita Diagnostic Center, PT Indec Diagnostics, Ultra Medica Clinic Surabaya, PT Prima Medika Laboratories, ABC Central Clinical Laboratory, and Others.

Market Insights & Analysis: Indonesia Diagnostic Labs Market (2026-32):

The Indonesia Diagnostic Labs market size was valued at USD 2.91 billion in 2025 and is projected to grow from USD 3.32 billion in 2026 to USD 5.15 billion by 2032, exhibiting a CAGR of 7.59% during the forecast period.

Indonesia’s diagnostic laboratory market demonstrates sustained expansion supported by macroeconomic stability and demographic momentum. According to the World Bank, Indonesia’s GDP growth remained above 5% in 2025, strengthening healthcare financing capacity. The country’s population surpassed 280 million in 2024, as reported by the media, increasing testing volumes across urban and peri-urban centers. Rising life expectancy, reported at 68.3 years in 2024 by the World Health Organization , structurally elevates demand for routine diagnostics and chronic disease monitoring services.

Public financing reforms continue to reinforce institutional demand across hospitals and government health facilities. BPJS(Indonesia’s national health insurance agency)Kesehatan has been actively requiring and promoting health screening tests for participants as part of early detection efforts in 2025, including diabetes , hypertension, cervical cancer, and breast cancer screening available for JKN participants, with plans to expand more screening types. According to government budget sources, Indonesia’s health sector allocation in the 2026 draft State Budget was projected at over USD 13.8 billion, reflecting strong public investment in health services and infrastructure. Portions of this funding, including significant allocations for hospital services, support facility enhancement activities, such as the modernization of diagnostic capabilities in provincial hospitals. Institutional end users remain central to market growth, particularly tertiary hospitals and independent diagnostic networks. Meanwhile, physician clinics increasingly outsource advanced pathology tests to centralized labs, supporting higher specimen throughput and operational specialization across the value chain.

Infrastructure expansion further underpins forward momentum through digital integration and logistics enhancement. The 2026 acceleration of the Satu Sehat digital health platform by the Ministry of Health of Indonesia enables standardized electronic laboratory reporting nationwide. These systemic improvements collectively support scalable operations, technology adoption, and geographically diversified revenue generation across Indonesia’s diagnostic ecosystem.

Indonesia Diagnostic Labs Market Recent Developments:

- 2025: Mandaya Hospital in Indonesia expanded its diagnostic capabilities with technologies such as MRI Ambient X, Digital PET‑CT, and advanced genetic testing, reducing the need for patients to travel abroad for complex diagnostics. Clinical leadership associated with this expansion was recently featured in Fortune Indonesia’s 40 Under 40.

- 2026: Indonesia’s Ministry of Health signed a memorandum with China’s Xuzhou Medical University and the National Standardization Agency to establish a Joint Laboratory for Digital Medicine and Proactive Health, focusing on AI applications, collaborative research, and medical data standardization, strengthening diagnostic innovation and digital health capacity.

Indonesia Diagnostic Labs Market Scope:

| Category | Segments |

|---|---|

| By Test Type | (Pathology, Radiology & Imaging), |

| By Pathology Test Type | (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecular Diagnostics, Genetic Testing), |

| By Radiology Type | (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), |

| By Service Delivery Mode | (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), |

| By Disease Type | (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), |

| By End-User | (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), |

Indonesia Diagnostic Labs Market Driver:

Insurance-Led Healthcare Expansion Accelerating Laboratory Demand

Indonesia’s universal health insurance framework represents the single most influential structural driver of diagnostic demand expansion. In 2025, BPJS Kesehatan reported coverage exceeding 270 million individuals, equivalent to more than 95% of the population. The integration of additional laboratory panels into reimbursable benefit packages has reduced out-of-pocket expenditure barriers. This structural financing mechanism directly increases test volumes rather than merely influencing pricing dynamics.

The driver intensified following the Ministry of Health’s 2025 optimization of JKN capitation and non-capitation financing mechanisms aimed at improving service quality at primary healthcare facilities. According to the Ministry’s Health Policy Agency, Badan Kebijakan Pembangunan Kesehatan, total JKN service utilization reached approximately 673.9 million healthcare service visits annually, reflecting sustained growth in publicly financed healthcare access. As laboratory diagnostics form a core component of clinical evaluation within primary and referral care, rising overall service utilization structurally supports increased diagnostic testing volumes. This systemic linkage between insurance coverage and clinical utilization materially enlarges total market throughput.

The measurable impact extends beyond hospitals into contracted private laboratories participating in the national scheme. Facilities accredited under Health Law compliance standards are eligible for BPJS-linked referrals, increasing specimen flows. Expanded financial protection also encourages preventive screening participation among lower-income populations. Consequently, universal reimbursement reforms operate as a volume-generating engine that sustains structural and geographically distributed demand growth.

Indonesia Diagnostic Labs Market Trend:

Integration of Digital Health Platforms

Indonesia’s diagnostic laboratory sector is undergoing structural transformation through integration with the national digital health infrastructure. In 2025, the Ministry of Health accelerated mandatory connectivity to the Satu Sehat platform, requiring healthcare facilities to standardize electronic medical record exchange. This policy enables laboratories to transmit results electronically to hospitals and primary care centers in real-time. The shift improves traceability, reduces manual reporting errors, and strengthens nationwide data interoperability.

The trend has been reinforced by increasing digital health utilization across both urban and secondary cities. By February 2024, data showed that 8,362 health facilities were connected to Satu Sehat and transmitting EMR data , highlighting the ongoing digitization of medical records across institutional users, including labs. Consequently, laboratories are transitioning from paper-based documentation toward cloud-enabled Laboratory Information Systems aligned with national standards. By late 2025, Indonesia’s Ministry of Health reported that more than 34,000 health facilities, including hospitals, clinics, and laboratories, had successfully connected their electronic medical records with the Satu Sehat national health data platform, marking a significant expansion of digital interoperability across diagnostic services and broader health sectors.

Leading diagnostic networks are investing in interoperable software infrastructure and automated data validation systems to comply with evolving regulatory requirements. Digital dashboards allow clinicians to track patient biomarkers longitudinally, strengthening preventive care programs. Integration with centralized health databases also supports epidemiological surveillance and public health monitoring. As regulatory mandates and provider adoption converge, digital platform integration is becoming a permanent and foundational feature of Indonesia’s diagnostic ecosystem.

Indonesia Diagnostic Labs Market Opportunity:

Development of Domestic In-Vitro Diagnostic (IVD) Manufacturing

A compelling opportunity is emerging in the domestic manufacturing of in-vitro diagnostic reagents and consumables. In 2025, Indonesia’s Ministry of Industry strengthened its import substitution roadmap for medical devices, prioritizing local production under the National Industrial Development Master Plan. The government’s increased use of Domestic Component Level (TKDN) requirements in public procurement encourages hospitals to prioritize locally manufactured diagnostic kits. This regulatory alignment creates structural demand certainty for new IVD producers.

The opportunity translates directly into market demand because public healthcare facilities account for a substantial share of laboratory procurement through centralized purchasing mechanisms. As public hospitals expand diagnostic capacity, preference for TKDN-compliant products provides domestic manufacturers with procurement advantages. Currency volatility and import lead times have further incentivized healthcare providers to seek stable local supply chains. Consequently, locally produced reagents and rapid test kits are gaining stronger institutional traction.

This environment is particularly favorable for new entrants and emerging biotech firms that can establish modular production lines for reagents, molecular test kits, or point-of-care consumables. Entry barriers in reagent production are lower than in establishing nationwide laboratory networks, allowing focused specialization. Government-backed industrial incentives, including tax allowances and manufacturing zone support, further reduce initial capital burdens. Domestic IVD production, therefore, represents a scalable and policy-supported growth avenue within Indonesia’s diagnostic ecosystem.

Indonesia Diagnostic Labs Market Challenge:

Dependence on Imported Reagents and Advanced Diagnostic Equipment

A major structural challenge in Indonesia’s diagnostic laboratory market is the continued dependence on imported reagents, consumables, and high-end diagnostic analyzers. Many molecular testing kits, immunoassay reagents, and automated laboratory platforms are sourced from global manufacturers, exposing laboratories to currency volatility and international supply chain disruptions. Exchange rate fluctuations directly affect procurement costs, particularly for private laboratories operating on fixed reimbursement structures.

This reliance became more visible during recent global logistics disruptions, when shipping delays extended lead times for critical laboratory consumables. Import procedures, customs clearance timelines, and regulatory documentation requirements can further delay the availability of specialized diagnostic kits. Laboratories must therefore maintain higher inventory buffers to avoid service interruptions, increasing working capital requirements. Smaller operators are disproportionately affected due to limited bargaining power with international suppliers.

The structural nature of this challenge constrains pricing flexibility and operational planning. When procurement costs rise, laboratories cannot always immediately adjust service tariffs, particularly for insured patients under fixed reimbursement schemes. Capital-intensive imported analyzers also require foreign technical servicing and maintenance contracts. Consequently, external supply dependence continues to limit cost stability and long-term financial predictability within Indonesia’s diagnostic laboratory ecosystem.

Indonesia Diagnostic Labs Market (2026–2032) Segmentation Analysis:

The Indonesia Diagnostic Labs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Test Type

- Pathology

- Radiology & Imaging

Pathology remains the dominant segment with a market share of 30% due to its central role in routine clinical decision-making across both primary and tertiary care. Unlike imaging, pathology tests are frequently required for chronic disease management and infectious disease surveillance. National public health initiatives, including WHO-supported efforts to strengthen laboratory capacity for diagnosing diseases like diphtheria, reflect systematic investment in microbiology and bacteriology testing, a core part of pathology services.

Policy-backed infectious disease monitoring programs in 2025 further strengthened laboratory-based surveillance networks nationwide. Standardized reporting requirements have increased reliance on certified pathology laboratories. Investment flows prioritize automated analyzers and reagent supply chains over capital-intensive imaging equipment. Alignment between reimbursement frameworks and test frequency consolidates pathology’s volume leadership.

End-user dynamics reinforce this dominance, as physician clinics routinely outsource pathology testing to specialized facilities. Independent laboratories benefit from centralized high-throughput processing models. Hospitals depend on pathology for pre-operative and inpatient diagnostics, creating recurring demand streams. Collectively, these systemic utilization patterns secure pathology’s sustained segmental supremacy.

Based on End-User

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

Hospitals constitute the leading end-user segment with a market share of 60% due to their integrated diagnostic and treatment capabilities. Tertiary facilities manage complex inpatient cases requiring continuous laboratory monitoring. In 2026, the Ministry of Health capital allocations prioritized equipment upgrades for referral hospitals, directly expanding in-house testing volumes.

Public referral hospitals function as regional specimen hubs, aggregating diagnostic demand from surrounding clinics. Accreditation mandates require on-site laboratory compliance for specialized services. Insurance reimbursements are more comprehensive for hospital-based diagnostics, incentivizing capacity expansion. This institutional advantage reinforces volume consolidation within hospital settings.

Additionally, Hospital laboratories in Indonesia perform a wide range of essential tests, including blood analysis, clinical chemistry, microbiology, serology, and pathology, which are critical to patient diagnosis, monitoring, and treatment planning. Their integration into the patient care pathway explains why hospitals generate higher specimen volumes than standalone facilities. Consequently, hospitals maintain structural leadership across Indonesia’s diagnostic end-user landscape.

Indonesia Diagnostic Labs Market (2026-32) Regional Analysis:

Java emerges as the largest and most dominant regional market with a market share of 60% due to its demographic and economic concentration. According to official population distribution data, Java Island was home to approximately 55.93 % of Indonesia’s total population as of the first half of 2024, highlighting its demographic concentration relative to other regions. Urban density supports high patient volumes and efficient laboratory network expansion.

Regulatory and infrastructure advantages further strengthen Java’s leadership. Major tertiary referral hospitals are concentrated in Jakarta and Surabaya, supported by central government funding allocations. Dharmais Cancer Hospital in West Jakarta is a national cancer referral hospital under the Ministry of Health, delivering specialized oncology diagnostics and treatment reflecting the concentration of advanced diagnostic centers in Jakarta. End-user demand patterns reveal a strong corporate and institutional healthcare presence in industrial zones across West Java and Banten.

National Hospital Surabaya introduced an AI-assisted 3T MRI system, representing one of the most advanced imaging modalities in the region and reducing diagnostic turnaround times while enhancing image clarity for critical conditions such as stroke. Large employers integrate occupational health diagnostics into workforce programs. Private laboratory chains typically pilot new technologies within Java before national rollout. These structural, economic, and policy-driven advantages collectively sustain Java’s market dominance.

Gain a Competitive Edge with Our Indonesia Diagnostic Labs Market Report:

- The Indonesia Diagnostic Labs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Indonesia Diagnostic Labs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Indonesia Diagnostic Labs Market Policies, Regulations, and Product Standards

- Indonesia Diagnostic Labs Market Trends & Developments

- Indonesia Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- Indonesia Diagnostic Labs Market Hotspot & Opportunities

- Indonesia Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Pathology

- Radiology & Imaging

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- Walk-in Testing

- Home Sample Collection

- Mobile Diagnostic Units

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- Infectious Diseases

- Oncology

- Diabetes & Endocrinology

- Cardiology

- Neurology

- Nephrology

- Gastroenterology

- Gynecology & Obstetrics

- Respiratory Disorders

- Orthopedics

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

- By Region- Market Size & Forecast 2022-2032, USD Million

- Sumatra

- Java

- Kalimantan

- Sulawesi

- Bali & Nusa Tenggara

- Maluku

- Papua

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Pathology Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Radiology & Imaging Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Diagnostic Labs Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Laboratorium Klinik CITO Indraprasta Semarang (CITO)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bio Medika Kelapa Gading

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Prodia Diacro Laboratories (Prodia the CRO)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Kimia Farma Diagnostika

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorium Parahita Diagnostic Center

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Indec Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ultra Medica Clinic Surabaya

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PT Prima Medika Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ABC Central Clinical Laboratory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Laboratorium Klinik CITO Indraprasta Semarang (CITO)

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now