GCC Managed & Professional Security Services Market Research Report: Forecast (2026-2032)

GCC Managed & Professional Security Services Market - By Product Type Room Air Conditioners (Window AC, Split AC), VRF Systems, Chillers, Packaged Air Conditioners, Cassette Air Co ... nditioners, Ducted Split Systems, Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.), By Refrigerant Type (R32, R410A, R134a, R1234ze / R1234yf, R744, Others), By Distribution Channel (Direct Sales, Authorized Dealers & Distributors, Multi-Brand Stores, Online), By End-User (Residential, Offices, Retail & Malls, Hotels & Hospitality, Hospitals & Healthcare, Educational Institutions, Manufacturing, Pharmaceuticals, Food & Beverage, Data Centers, Others), and others By Service Type Managed Security Services, (Managed Detection & Response (MDR), Managed SIEM (Security Information & Event Management), Managed UTM (Unified Threat Management), Managed Firewalls, Managed Endpoint Protection, Managed Identity & Access Management (IAM), Managed Risk & Compliance, Managed DDoS Protection, Managed XDR (Extended Detection & Response), Others), Professional Security Services, (Security Consulting, Risk and Vulnerability Assessment, Penetration Testing, Security Strategy & Architecture, Incident Response Consulting, Security Policy & Compliance Services, Forensics & Investigation, Security Training & Awareness), By Deployment (Cloud-based, On-Premises, Hybrid), By Organization Size (Large Enterprises, Small & Medium-Sized Enterprises (SMEs), By End-User (Banking, Financial Services & Insurance (BFSI), Government & Defense, Healthcare, IT & Telecom, Retail, Manufacturing, Energy & Utilities, Others), and others Read more

- ICT & Electronics

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

GCC Managed & Professional Security Services Market

Projected 10.51% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 3.81 Billion

Market Size (2032)

USD 5.19 Billion

Base Year

2025

Projected CAGR

10.51%

Leading Segments

By End User: BFSI

GCC Managed & Professional Security Services Market Report Key Takeaways:

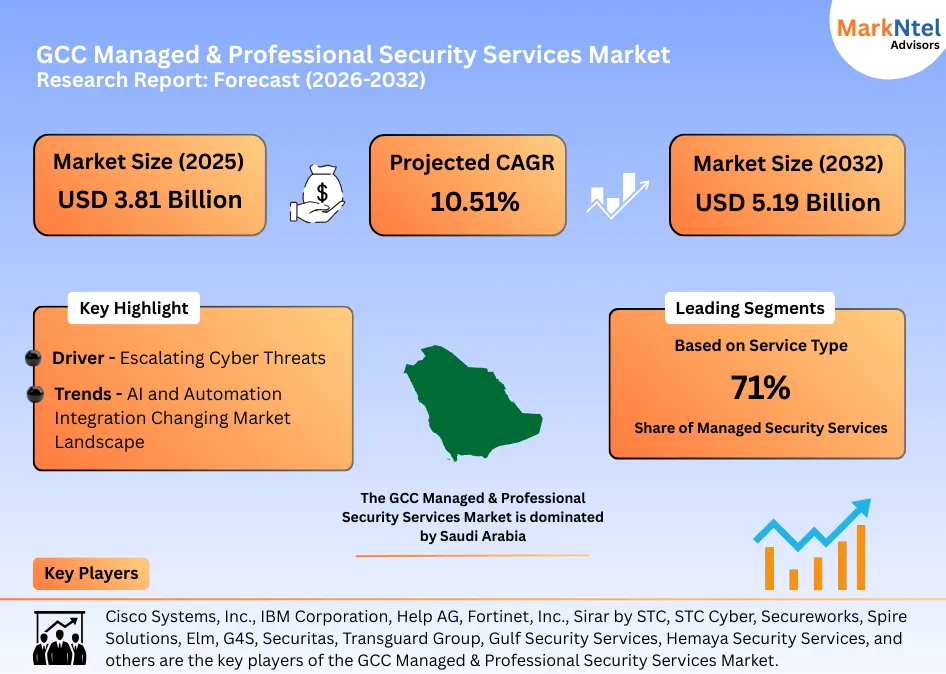

- The GCC Managed & Professional Security Services Market size was valued at around USD 3.81 billion in 2025 and is projected to reach USD 5.19 billion by 2032. The estimated CAGR from 2026 to 2032 is around 10.51%, indicating strong growth.

- By service type, the managed security services segment represented 71% of the GCC Managed & Professional Security Services Market size in 2025.

- By end user, the BFSI represented 32% of the GCC Managed & Professional Security Services Market size in 2025, while healthcare emerged as the fastest-growing segment, expanding at a CAGR of 14.62% during 2026-32.

- By deployment, the cloud-based segment emerged as the fastest-growing segment, expanding at a CAGR of 15.82% during 2026-32.

- Saudi Arabia leads the GCC Managed & Professional Security Services Market with a dominant 36% share. At the same time, the UAE emerges as the fastest-growing major market, projected to expand at a robust 12.98% CAGR.

- The leading managed & professional security services companies in GCC are Cisco Systems, Inc., IBM Corporation, Help AG, Fortinet, Inc., Sirar by STC, STC Cyber, Secureworks, Spire Solutions, Elm, G4S, Securitas, Transguard Group, Gulf Security Services, Hemaya Security Services, and others.

Market Insights & Analysis: GCC Managed & Professional Security Services Market (2026-2032):

The GCC Managed & Professional Security Services Market size was valued at around USD 3.81 billion in 2025 and is projected to reach USD 5.19 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 10.51% during the forecast period, i.e., 2026-32.

The GCC Managed & Professional Security Services Market is experiencing rapid growth, driven by escalating cyber threats across critical sectors and the accelerating integration of AI and automation into national and enterprise security frameworks.

By August 2025, more than 50 million web and local threats were detected across the GCC, with password stealers rising by 21% and spyware by 34%, reflecting the growing sophistication of attack vectors. The geographic distribution of threat activity underscores regional exposure, with 40% of dark-web threat posts targeting the UAE, followed by Saudi Arabia (26%), Kuwait (15%), Qatar (10%), Bahrain (6%), and Oman (3%).

Attack patterns further highlight structural risk. DDoS attacks account for 73.2% of all incidents, rising nearly 70% year-on-year in H1 2024. The region recorded 755 phishing campaigns, a 32% rise in ransomware incidents in the UAE, and 63.5% of data leaks hosted on major breach forums.

Public institutions are increasingly targeted, with 21% of dark-web activity focusing on government entities. In the UAE alone, public sector organizations face approximately 50,000 cyberattacks daily, while Saudi Arabia recorded 88 ransomware incidents in 2024, heavily concentrated in manufacturing and critical infrastructure .

In response, enterprises and governments are accelerating the adoption of AI-driven and cloud-enabled security architectures. By deployment, the cloud-based segment emerged as the fastest-growing segment, expanding at a CAGR of 15.82%, reflecting the need for scalable, continuously updated, and centrally managed security platforms .

This shift is reinforced by AI integration; in Saudi Arabia, over 50% of companies have already embedded AI into cybersecurity operations, with 91% planning to deploy AI agents within a year and 40% anticipating human-AI collaboration within SOC environments.

Similarly, in 2025, Cisco announced AI infrastructure collaborations across Saudi Arabia, the UAE, and Qatar, aimed at building AI-native cybersecurity platforms aligned with national digital transformation agendas.

Looking beyond 2025, government strategies and regional forecasts indicate that the threat landscape will further evolve. For instance, regional security outlooks project that by 2026, over 70% of Middle East organizations will view insider and identity-based threats as their primary risk, driven by hyper-connected cloud ecosystems. This will elevate demand for identity-centric security, behavioral analytics, and continuous monitoring platforms.

Saudi Arabia’s National Cybersecurity Strategy under Vision 2030 anticipates expanded risks to critical infrastructure, energy supply chains, and national networks, committing to enhanced threat intelligence sharing, national response frameworks, and persistent monitoring across sectors.

The convergence of escalating cyber threats, AI-enabled attack methods, and government-led digital transformation is structurally redefining security requirements across the GCC. These forces will continue to propel long-term demand for managed and professional security services, positioning the market for sustained growth through 2026 and beyond.

GCC Managed & Professional Security Services Market Recent Developments:

- May 2025: At GISEC Global 2025 in Dubai, Microsoft highlighted its next-generation Security Copilot Agents, AI-powered autonomous agents designed to augment cybersecurity operations by automating alert triage, surfacing prioritized risk insights, and reducing analyst workload. Partner Help AG demonstrated a Phishing Triage Agent that autonomously handles routine phishing alerts, enabling security teams to focus on complex threats and enhance incident response efficiency.

- May 2025: At GISEC Global 2025 in Dubai, organisers introduced a dedicated Operational Technology (OT) Security track to address surging cyberattacks targeting critical infrastructure such as power, oil & gas, and transport systems. The new segment focused on strategies for securing industrial control systems (ICS/SCADA), AI-driven risks, and Zero Trust adoption, reflecting escalating OT threats and growing regional demand for specialised professional security services.

GCC Managed & Professional Security Services Market Drivers:

Escalating Cyber Threats

The GCC Managed & Professional Security Services Market is being fundamentally shaped by the sharp escalation of cyber threats across both public and private sectors as governments and enterprises confront rising digital risks, regulatory pressure, and the need for continuous, specialized cyber defense.

In the UAE, by 2024, the country became the second most targeted country in MENA, accounting for 12% of regional cyberattacks. Breaches cost organizations an average of USD 2.9 million, with over 12,000 Wi-Fi incidents in early 2025. Authorities now block more than 200,000 attacks daily, highlighting severe pressure on the national digital infrastructure.

Saudi Arabia reflects a similar intensity. In early 2025, the Kingdom represented 63% of all cyber incidents in the Middle East, with phishing attacks increasing by 22.5%. These campaigns are increasingly driven by AI-enabled tools, including deepfakes and automated social engineering, significantly raising the complexity and speed of attacks and reducing the effectiveness of traditional, reactive security models.

Oman is witnessing comparable exposure. During H1 2025, authorities recorded a 50% rise in cybercrime and digital fraud, fueled by the rapid adoption of digital platforms and electronic payments. AI-powered impersonation schemes targeting public and financial institutions have revealed critical systemic vulnerabilities.

The expanding scale, sophistication, and financial impact of cyber threats across the GCC are compelling organizations to transition toward continuous, outsourced security operations. This structural shift will accelerate long-term demand for managed and professional security services across the region.

GCC Managed & Professional Security Services Market Trends:

AI and Automation Integration Changing Market Landscape

AI and automation are rapidly becoming foundational components of cybersecurity strategies across the GCC, driven by governments’ responses to increasingly sophisticated threats and the scale of regional digital transformation programs. Traditional, reactive security models are proving inadequate against AI-enabled phishing, deepfakes, and automated attack campaigns, compelling both public institutions and enterprises to adopt intelligent, always-on defense frameworks.

Saudi Arabia exemplifies this shift. The National Cybersecurity Authority has embedded AI into national defensive architectures to enable real-time threat detection and large-scale data analysis. This transition forms part of the broader cybersecurity expenditure of approximately USD 3.55 billion in 2023, reflecting a strategic move toward predictive and automated cyber defense rather than manual monitoring .

The private sector is reinforcing this direction. At GITEX Global 2025, Sophos showcased AI-powered Managed Detection and Response (MDR) platforms that combine automation with expert oversight to counter advanced threats such as automated phishing and deepfake attacks. These solutions demonstrate how AI is transforming managed security services into proactive, intelligence-led operations.

Further strengthening this trend, CloudSEK partnered with the UAE’s Seed Group in late 2025 to deploy AI-enabled threat intelligence and automated risk management across the UAE and wider GCC. The collaboration highlights cross-border demand for AI-centric security services that can scale with regional digital ecosystems.

As cyber threats become faster and more autonomous, GCC organizations are shifting toward AI-driven security models. This structural transition will significantly accelerate demand for advanced managed and professional security services across the region.

GCC Managed & Professional Security Services Market Challenges:

High Implementation and Service Costs

High implementation and service costs remain a structural barrier in the GCC Managed & Professional Security Services Market, particularly as governments mandate enterprise-grade cybersecurity across increasingly complex digital ecosystems.

Official national strategies acknowledge that building resilient cyber infrastructure requires large-scale, sustained public investment, underscoring the financial intensity of modern security frameworks.

In the UAE, over USD 2 billion in government funding under the National Cybersecurity Strategy underscores the capital intensity of secure digital infrastructure . Likewise, Saudi Arabia’s Vision 2030 ICT expansion positions cybersecurity as a major cost driver, highlighting the inherently high financial burden of advanced security implementation.

While such investments are necessary, they elevate entry barriers for smaller government entities, municipalities, and mid-sized enterprises. Beyond initial deployment, recurring costs for managed services, system integration, compliance audits, and 24/7 monitoring further intensify budgetary pressure. Organizations with constrained fiscal capacity may delay adoption or opt for partial protection, exposing systemic gaps.

Overall, persistently high implementation and service costs can restrict market penetration across smaller institutions and enterprises, slowing sector-wide adoption. Without scalable and cost-efficient delivery models, this challenge will continue to temper the pace of market expansion.

GCC Managed & Professional Security Services Market (2026-32) Segmentation Analysis:

The GCC Managed & Professional Security Services Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Service Type:

- Managed Security Services

- Managed Detection & Response (MDR)

- Managed SIEM (Security Information & Event Management)

- Managed UTM (Unified Threat Management)

- Managed Firewalls

- Managed Endpoint Protection

- Managed Identity & Access Management (IAM)

- Managed Risk & Compliance

- Managed DDoS Protection

- Managed XDR (Extended Detection & Response)

- Others

- Professional Security Services

- Security Consulting

- Risk and Vulnerability Assessment

- Penetration Testing

- Security Strategy & Architecture

- Incident Response Consulting

- Security Policy & Compliance Services

- Forensics & Investigation

- Security Training & Awareness

The managed security services segment holds the top spot in the GCC Managed & Professional Security Services Market, with a market share of around 71%. This segment is maintaining its leadership driven by the region’s increasing need for continuous, enterprise-grade cybersecurity operations.

The expanding threat landscape has made round-the-clock monitoring, rapid threat detection, and coordinated incident response critical, requirements that are more effectively delivered through outsourced managed service models than in-house teams.

Services such as Managed Detection & Response (MDR), Managed SIEM, XDR, managed firewalls, and endpoint protection provide centralized visibility and real-time threat intelligence across complex IT environments. These capabilities are particularly valuable in the GCC, where organizations face a shortage of skilled cybersecurity professionals and rising compliance obligations linked to national cybersecurity frameworks and data protection regulations.

From a financial perspective, MSS enables organizations to avoid high upfront investments in security infrastructure and specialist talent, instead adopting predictable operating expenditure models.

Additionally, managed providers continuously update platforms with AI-driven analytics and automation, ensuring faster adaptation to emerging threats. As governments and enterprises accelerate digital transformation initiatives, Managed Security Services remain the most scalable, resilient, and cost-effective approach to maintaining robust cybersecurity postures across the GCC.

Based on End User:

- Banking, Financial Services & Insurance (BFSI)

- Government & Defense

- Healthcare

- IT & Telecom

- Retail

- Manufacturing

- Energy & Utilities

- Others

The BFSI category leads the GCC Managed & Professional Security Services Industry, accounting for 32% of market share, reflecting its critical dependence on secure digital ecosystems.

Financial institutions handle high-value transactions, confidential customer data, and interconnected payment infrastructures, making them frequent targets for sophisticated cyberattacks such as fraud, ransomware, phishing, and identity compromise.

The rapid expansion of digital banking, mobile payments, cloud-based core systems, and open banking frameworks has significantly increased institutional exposure to cyber risks, reinforcing the need for continuous monitoring and advanced threat management services.

Moreover, stringent regulatory and compliance requirements related to data protection, financial stability, and operational resilience compel BFSI organizations to adopt robust, professionally managed security frameworks.

The financial and reputational consequences of cyber incidents in this sector are substantial, often resulting in direct monetary losses, regulatory penalties, and erosion of customer trust. As a result, BFSI entities prioritize long-term investments in managed detection, incident response, and risk intelligence services.

In comparison, while healthcare emerged as the fastest-growing end-user segment, expanding at a CAGR of 14.62%, its overall contribution remains smaller due to relatively later adoption of complex digital financial systems . However, its accelerating digital transformation is expected to drive stronger security demand over the forecast period.

GCC Managed & Professional Security Services Market (2026-32): Regional Projection:

The GCC Managed & Professional Security Services Market is dominated by Saudi Arabia, which holds a commanding 36% share, supported by the scale and intensity of its nationwide digital transformation agenda.

Vision 2030 has accelerated the deployment of digital government services, cloud platforms, smart infrastructure, and data-driven public services, substantially expanding the cybersecurity requirements of both public and private sectors.

The Kingdom’s large concentration of critical industries, including energy, financial services, manufacturing, and telecommunications, creates sustained demand for advanced managed security operations, threat intelligence, and incident response capabilities.

Centralized cybersecurity governance and stricter compliance mandates have further strengthened reliance on professional security service providers to ensure regulatory alignment, operational resilience, and continuous risk monitoring.

In addition, Saudi Arabia’s growing role as a regional hub for hyperscale data centers and national digital platforms has increased exposure to sophisticated cyber threats, reinforcing long-term security investments.

By comparison, while the UAE emerges as the fastest-growing major market, projected to expand at a robust 12.98% CAGR, it’s leadership reflects its larger digital economy, broader critical infrastructure footprint, and higher absolute security spending.

Saudi Arabia’s market leadership is anchored in scale-driven digitalization, critical infrastructure exposure, and sustained national cybersecurity investments, positioning it as the primary demand center for managed and professional security services in the GCC.

Gain a Competitive Edge with Our GCC Managed & Professional Security Services Market Report:

- GCC Managed & Professional Security Services Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Managed & Professional Security Services Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Market Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Managed & Professional Security Services Market Trends & Development

- GCC Managed & Professional Security Services Market Dynamics

- Growth Drivers

- Challenges

- GCC Managed & Professional Security Services Market Regulations, Policies & Standards

- GCC Managed & Professional Security Services Market Hotspots & Opportunities

- GCC Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- Managed Security Services

- Managed Detection & Response (MDR)

- Managed SIEM (Security Information & Event Management)

- Managed UTM (Unified Threat Management)

- Managed Firewalls

- Managed Endpoint Protection

- Managed Identity & Access Management (IAM)

- Managed Risk & Compliance

- Managed DDoS Protection

- Managed XDR (Extended Detection & Response)

- Others

- Professional Security Services

- Security Consulting

- Risk and Vulnerability Assessment

- Penetration Testing

- Security Strategy & Architecture

- Incident Response Consulting

- Security Policy & Compliance Services

- Forensics & Investigation

- Security Training & Awareness

- Managed Security Services

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- Cloud-based

- On-Premises

- Hybrid

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- Large Enterprises

- Small & Medium-Sized Enterprises (SMEs)

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Banking, Financial Services & Insurance (BFSI)

- Government & Defense

- Healthcare

- IT & Telecom

- Retail

- Manufacturing

- Energy & Utilities

- Others

- By Country

- The UAE

- Saudi Arabia

- Qatar

- Kuwait

- Oman

- Bahrain

- By Company

- Competition Characteristics

- Market Share of Leading Companies

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- The UAE Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Saudi Arabia Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Qatar Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Kuwait Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Oman Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Bahrain Managed & Professional Security Services Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Service Type – Market Size & Forecast 2022-2032, USD Million

- By Deployment – Market Size & Forecast 2022-2032, USD Million

- By Organization Size – Market Size & Forecast 2022-2032, USD Million

- By End-User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- GCC Managed & Professional Security Services Market Key Strategic Imperatives for Growth & Success

- Competition Outlook

- Company Profiles

- Cisco Systems, Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- IBM Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Help AG

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Fortinet, Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Sirar by STC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- STC Cyber

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Secureworks

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Spire Solutions

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Elm

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- G4S

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Securitas

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Transguard Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Gulf Security Services

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Hemaya Security Services

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Cisco Systems, Inc.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now