Latin America Warehouse Automation Market Research Report: Forecast (2026-2032)

Latin America Warehouse Automation Market - By Component (Hardware (Automated Storage & Retrieval Systems (Unit-load, Mini-load, Shuttle-based), Mobile Robots (AGVs, AMRs), Industr ... ial Robots, Conveyor & Sortation Systems, Picking, Palletizing & Depalletizing Robots, Goods-to-Person (GTP) Systems, Automatic Identification & Data Capture (AIDC)), Software (Warehouse Management Systems (WMS), Warehouse Control Systems (WCS), Warehouse Execution Systems (WES), Inventory & Order Management Software, Fleet & Robot Management Platforms, AI / ML-based Analytics & Predictive Modules, Cloud-based vs On-Premise Software), Services (Consulting & Advisory, System Design & Integration, Installation & Commissioning, Maintenance & Support, Training & Change Management, System Upgrades & Optimization)), By Automation Level (Manual / Basic Automation, Semi-Automated Warehouses, Highly Automated Warehouses, Fully Autonomous Warehouses (AI-driven, robotics-led)), By Warehouse Size (Small (Below 50,000 sq. ft., Medium (50,000–200,000 sq. ft.), Large (200,000–500,000 sq. ft.), Mega Warehouses (Above 500,000 sq. ft.)), By Deployment Model (Cloud-based, On-Premise, Hybrid), By Ownership Model (Company-Owned Warehouses, Third-Party Logistics (3PL) / Contract Warehouses, E-commerce Pure-Play Fulfillment Centers, Government & Defense Warehouses), By Enterprise Size (Small & Medium Enterprise (SMEs), Large Enterprise), By Application (Order Fulfillment Automation, Inventory Tracking & Management, Goods-to-Person (GTP) Picking, Palletizing & Depalletizing, Automated Packaging, Labeling & Sorting, Reverse Logistics & Returns Handling), By End User (Retail & E-commerce, Manufacturing, Automotive, Industrial Goods, Healthcare & Pharmaceuticals, Food & Beverage, Consumer Products, Electronics & High-Tech, Cold Chain & Perishables, Others), and others Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Latin America Warehouse Automation Market

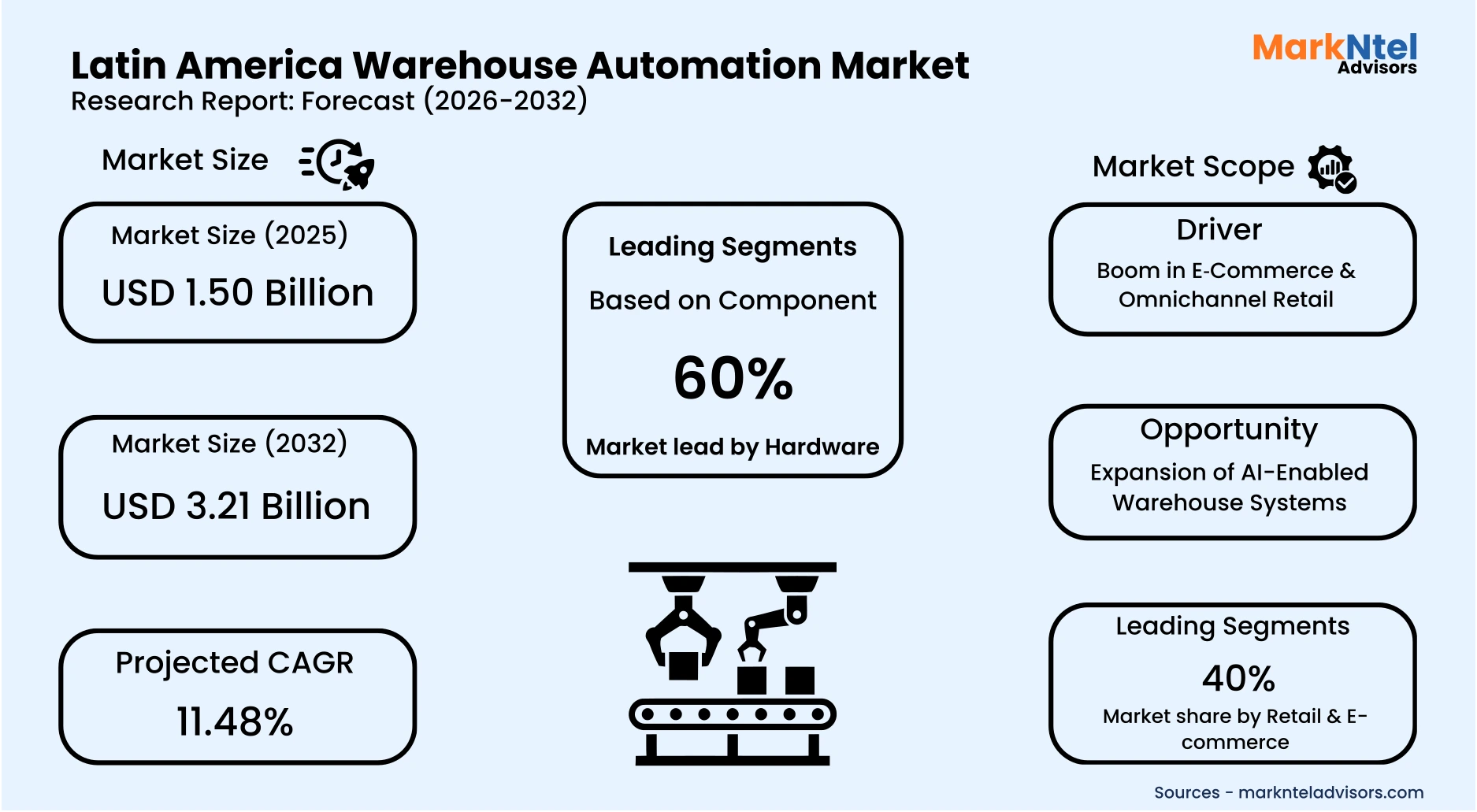

Projected 11.48% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 1.50 Billion

Market Size (2032)

USD 3.21 Billion

Base Year

2025

Projected CAGR

11.48%

Leading Segments

By End User: Retail & E-Commerce

Latin America Warehouse Automation Market Report Key Takeaways:

- Market size was valued at around USD 1.50 billion in 2025 and is projected to reach USD 3.21 billion by 2032. The estimated CAGR from 2026 to 2032 is around 11.48%, indicating strong growth.

- Brazil holds the largest market share of about 45% in the Latin America Warehouse Automation Market in 2025.

- By component, the hardware segment represented a significant share of about 60% in the Latin America Warehouse Automation Market in 2025.

- By end user, the retail & e-commerce segment presented a significant share of about 40% in the Latin America Warehouse Automation Market in 2025.

- Leading warehouse automation companies in the Latin America Market are Dematic Ltda., Daifuku Co., Ltd, Honeywell Intelligrated, SSI Schäfer Group, Knapp AG, Vanderlande Industries, Swisslog Holding AG, Murata Machinery, Ltd, TGW Logistics Group, Mecalux, S.A., Bastian Solutions, LLC, Eurotecsa, S.A. de C.V, and Others.

Market Insights & Analysis: Latin America Warehouse Automation Market (2026-32):

The Latin America Warehouse Automation Market size was valued at approximately USD 1.50 billion in 2025 and is projected to reach USD 3.21 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 11.48% during the forecast period, i.e., 2026-32.

The Latin America Warehouse Automation Market is projected to expand steadily, driven by rapid e‑commerce and omnichannel retail expansion, alongside increasing adoption of Autonomous Mobile Robots (AMRs) and collaborative robots (cobots).

Latin America’s warehouse automation market growth is closely tied to structural advances in digital transformation and e-commerce expansion. Government digital strategies such as Brazil’s Brazilian Digital Transformation Strategy (E-Digital 2022–2026) aim to broaden digital infrastructure and encourage technology adoption across industries, including logistics and automation technologies that underpin warehouse modernization.

Meanwhile, Mexico’s National Digital Strategy (Estrategia Digital Nacional) focuses on expanding internet access and digital services, facilitating a platform for e-commerce and logistics evolution.

E-commerce continues to reshape demand for automated warehouses by increasing parcel volumes and delivery expectations. For instance, Latin American online retail sales are on track to reach USD 215.31 billion in 2026, with 84 % of transactions mobile-first and concentrated in Argentina, Brazil, and Mexico. This accelerated online shopping growth drives logistics networks to adopt systems such as automated sortation, robotics, and real-time tracking to meet requirements for next-day and same-day delivery, increasing throughput and reducing error rates.

Logistics automation adoption is also influenced by operational and digital infrastructure improvements. In Mexico, digital commerce contributed an estimated 6.4 % of national GDP in 2023, with online sales growing over 20 % in 2024, underscoring logistics and automation’s role in economic output . Providers are increasingly orienting to intelligent supply chain models that integrate data, automation, and real-time decision support to optimize fulfillment and agility in high-growth segments such as omnichannel retail.

Looking ahead, government digital transformation and industrial modernization plans are set to reinforce automation demand. For example, Brazil’s broader investment of USD 37 billion into digital transformation, including industrial robotics, AI, and IoT initiatives, targets a digital modernized industrial base by 2033, increasing automation readiness.

In Mexico, infrastructure such as the launch of Alibaba Cloud’s Mexico region in 2025 is expanding digital capacity, which supports logistics analytics and advanced automation capabilities.

Overall, Latin America’s warehouse automation growth is anchored in e‑commerce expansion, government-led digital transformation, and advanced robotics adoption, with Brazil and Mexico poised to drive continued modernization, efficiency, and scalability in regional logistics and fulfillment operations.

Latin America Warehouse Automation Market Recent Developments:

- 2025: Mercado Libre and Agility Robotics have signed a commercial agreement to deploy Agility’s humanoid robot Digit in Mercado Libre’s San Antonio, Texas, fulfillment center, with plans to expand usage across Latin American warehouses. Digit will initially support repetitive logistics tasks to enhance safety, reduce labor gaps, and increase productivity, enabling teams to focus on higher‑value work .

- 2025: DHL Group signed a strategic Memorandum of Understanding (MOU) with Boston Dynamics to deploy over 1,000 additional advanced robotics units globally and accelerate its cross‑business automation strategy. Building on the success of Boston Dynamics’ Stretch robot for container unloading, DHL plans to expand applications, including case picking, to boost productivity and logistics efficiency.

Latin America Warehouse Automation Market Scope:

| Category | Segments |

|---|---|

| By Component | Hardware (Automated Storage & Retrieval Systems (Unit-load, Mini-load, Shuttle-based), Mobile Robots (AGVs, AMRs), Industrial Robots, Conveyor & Sortation Systems, Picking, Palletizing & Depalletizing Robots, Goods-to-Person (GTP) Systems, Automatic Identification & Data Capture (AIDC)), Software (Warehouse Management Systems (WMS), Warehouse Control Systems (WCS), Warehouse Execution Systems (WES), Inventory & Order Management Software, Fleet & Robot Management Platforms, AI / ML-based Analytics & Predictive Modules, Cloud-based vs On-Premise Software), Services (Consulting & Advisory, System Design & Integration, Installation & Commissioning, Maintenance & Support, Training & Change Management, System Upgrades & Optimization) |

| By Automation Level | Manual / Basic Automation, Semi-Automated Warehouses, Highly Automated Warehouses, Fully Autonomous Warehouses (AI-driven, robotics-led) |

| By Warehouse Size | Small (Below 50,000 sq. ft., Medium (50,000–200,000 sq. ft.), Large (200,000–500,000 sq. ft.), Mega Warehouses (Above 500,000 sq. ft.) |

| By Deployment Model | Cloud-based, On-Premise, Hybrid), |

| By Ownership Model | Company-Owned Warehouses, Third-Party Logistics (3PL) / Contract Warehouses, E-commerce Pure-Play Fulfillment Centers, Government & Defense Warehouses |

| By Enterprise Size | Small & Medium Enterprise (SMEs), Large Enterprise), |

| By Application | Order Fulfillment Automation, Inventory Tracking & Management, Goods-to-Person (GTP) Picking, Palletizing & Depalletizing, Automated Packaging, Labeling & Sorting, Reverse Logistics & Returns Handling |

| By End User | Retail & E-commerce, Manufacturing, Automotive, Industrial Goods, Healthcare & Pharmaceuticals, Food & Beverage, Consumer Products, Electronics & High-Tech, Cold Chain & Perishables, Others |

Latin America Warehouse Automation Market Driver:

Boom in E‑Commerce & Omnichannel Retail

Latin America’s warehouse automation market is being materially driven by the rapid expansion of e‑commerce and the rise of omnichannel retail, which are creating structural demand for logistics modernization.

Official data show Brazil’s e‑commerce sector is expected to generate approximately USD 36.3 billion in revenue in 2025, with around 94 million Brazilians making online purchases, up by 3 million from the previous year, reflecting deepening consumer digital adoption and intensifying pressure on fulfillment systems .

Retailers and platforms are responding with investments that directly influence logistics and warehouse automation needs. Latin America’s leading e‑commerce firm announced a USD 3.4 billion investment in Mexico for 2025, with expanded logistics, technology, and workforce deployments, underscoring how e‑commerce expansion fuels infrastructure and automation demand.

E‑commerce growth is being reinforced by broader digital transformation trends, including Brazil’s Pix instant payment system, which by 2025 had accumulated over 175 million users and accounted for a large share of digital transactions; this payment ubiquity lowers frictions for online purchases and further accelerates order volumes that logistics networks must serve .

Collectively, these structural shifts, significant revenue expansion in online retail, strategic investments targeting logistics capabilities, widespread digital payments, and integrated omnichannel strategies, are creating a measurable increase in demand for warehouse automation.

Unlike seasonal or speculative trends, this driver reflects enduring transformations in consumer behavior and enterprise systems, directly increasing the volume and complexity of goods flows that automation technologies must handle across Latin American supply chains.

Latin America Warehouse Automation Market Trend:

Inclination Towards Autonomous Mobile Robots (AMRs) & Collaborative Robots (Cobots)

A key trend reshaping warehouse automation in Latin America is the deployment of Autonomous Mobile Robots (AMRs) and collaborative robots (cobots) to improve efficiency and human–robot collaboration.

In Mexico, GEODIS implemented next‑generation AMRs from Locus Robotics at a fulfillment center in Cuautitlan Izcalli, using Origin bots controlled by a warehouse execution platform to enhance order‑picking productivity and real-time operational visibility. This deployment highlights the growing adoption of intelligent robotics in high‑throughput e‑commerce operations.

Collaborative robotics is also gaining traction. In late 2025, DHL Supply Chain partnered with Robust. AI to deploy Carter cobots in its retail logistics operations in Mexico, marking the company’s first use of collaborative robots in Latin America . These cobots work alongside human operators to boost productivity and operational accuracy, signaling a shift toward human-centric automation.

This trend reflects broader structural adjustments in logistics, where operators seek to reduce reliance on manual labor while improving safety. AMRs enable flexible navigation and automated transport, while cobots support close human interaction tasks such as assisted picking and sortation. Adoption is further accelerated by rising labor costs and skill shortages, making robotics a scalable and efficient alternative.

Looking forward, AMRs and cobots are expected to remain central to warehouse automation in Latin America, enabling operators to meet growing e-commerce demand, optimize throughput, and enhance operational agility across multi-channel supply chains.

Latin America Warehouse Automation Market Opportunity

Expansion of AI-Enabled Warehouse Systems

The Latin America warehouse automation market presents a compelling opportunity for new entrants through the adoption of AI-driven warehouse management systems (WMS) and robotics orchestration platforms.

Brazil’s Artificial Intelligence Plan (PBIA 2024–2028) earmarks approximately USD 4 billion for AI infrastructure, research, and industrial applications, fostering an environment conducive to intelligent logistics solutions that improve inventory optimization, predictive analytics, and autonomous workflow coordination .

Mexico’s digital infrastructure growth, highlighted by the launch of Alibaba Cloud’s Mexico region in 2025, enables scalable deployment of AI-powered WMS and robot orchestration systems. This reduces the capital burden for emerging technology providers, allowing them to implement cloud-ready, modular automation solutions that efficiently manage complex fulfillment operations for e-commerce and omnichannel retail .

Looking ahead, government initiatives promoting digital supply chain modernization, including Brazil’s Pix instant payment adoption and Mexico’s Nearshoring Decree, are driving higher e-commerce volumes and cross-border logistics activity. These structural changes create measurable demand for advanced warehouse automation.

Overall, new and smaller players can leverage this opportunity by offering AI-enabled, flexible systems that enhance operational efficiency, support omnichannel fulfillment, and provide competitive differentiation against traditional logistics providers.

Latin America Warehouse Automation Market Challenge:

Infrastructure and Regulatory Barriers

The Latin America warehouse automation market is constrained by persistent infrastructure deficiencies and fragmented regulatory frameworks, which materially limit the adoption of advanced logistics technologies.

Transport networks, including roads, railways, and ports, remain unevenly developed, raising freight costs and causing delays that reduce the operational efficiency needed to justify investments in automation. The OECD Latin American Economic Outlook 2025 estimates that closing regional infrastructure gaps requires approximately USD 2.2 trillion, with an annual shortfall of USD 99 billion, highlighting the scale of investment needed for efficient, automated supply chains.

Policy uncertainties exacerbate these challenges. For instance, Argentina’s 2025 restructuring of its National Roads Authority transferred maintenance responsibilities and generated concerns over road quality, directly affecting warehouse-to-port connectivity and logistics reliability. Such infrastructure and regulatory limitations restrict automation scalability, increase investment risks, and hinder the efficiency and integration necessary for modern, AI-driven, and robotic-enabled warehouse systems.

Addressing infrastructure gaps and harmonizing regulatory frameworks is critical for Latin America to fully realize warehouse automation potential, enabling scalable, efficient, and AI-driven logistics systems while reducing operational risks and investment barriers.

Latin America Warehouse Automation Market (2026-32) Segmentation Analysis:

The Latin America Warehouse Automation Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Component:

- Hardware

- Robots (AMRs, AGVs, SCARA/Delta Arms)

- Conveyors & Sorters

- AS/RS Cranes & Shuttles

- Sensors & Scanners

- PLC / Controls

- Software

- WMS / Warehouse Execution Software

- Warehouse Control Systems

- Fleet / Robot Orchestration

- Analytics & Optimization

- Services

- Installation & Integration

- Maintenance & Support

- Training & Consulting

- Custom Engineering

The hardware segment dominates the Latin America Warehouse Automation market, holding around 60% market share, driven by rising e-commerce volumes and labor shortages across the region.

Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), and SCARA/Delta robotic arms are increasingly deployed in Brazil, Mexico, and Chile to handle high-throughput picking, sorting, and material movement tasks, reducing reliance on manual labor.

Other hardware segments, including conveyors, sorters, AS/RS cranes, and sensor systems, support seamless integration of robotic fleets. Brazilian logistics hubs are increasingly installing automated conveyors and shuttles to connect high-density storage with order-picking zones, demonstrating a structural commitment to hardware-based automation.

While software and services are essential for orchestration and analytics, hardware investment represents the largest capital allocation, driven by measurable gains in speed, accuracy, and labor efficiency.

Continued growth in AMR and AGV deployment is expected as governments and private operators prioritize modernized logistics infrastructure, ensuring hardware remains the backbone of warehouse automation in Latin America.

Based on End User:

- Retail & E-commerce

- Manufacturing

- Automotive

- Industrial Goods

- Healthcare & Pharmaceuticals

- Food & Beverage

- Consumer Products

- Electronics & High-Tech

- Cold Chain & Perishables

- Others

The retail & e-commerce segment dominates the Latin America Warehouse Automation Market, holding around 40% market share, due to its high order frequency, fluctuating volumes, and stringent delivery timelines, which necessitate automated solutions such as Autonomous Mobile Robots (AMRs), robotic sortation systems, and automated storage/retrieval systems (AS/RS) to maintain speed, accuracy, and reliability in fulfillment operations. Omnichannel retail further amplifies these demands, requiring seamless coordination between online and physical store inventories.

Manufacturing and industrial end-users primarily adopt automation to enhance material handling efficiency, reduce manual labor in repetitive processes, and support just-in-time production models. Robotics, conveyors, and sensor-enabled storage systems mitigate operational bottlenecks, optimize inventory flow, and ensure consistency in high-volume production environments.

Specialized sectors like Food & Beverage, Healthcare, and Pharmaceuticals require temperature-controlled handling, precise inventory management, and compliance with regulatory standards, influencing tailored automation investments in robotics, sensors, and warehouse management software.

The intersection of operational complexity, labor intensity, regulatory compliance, and scalability requirements. These structural factors explain why Retail & E-Commerce commands the largest share of warehouse automation adoption, while other sectors adopt complementary technologies based on industry-specific needs, ensuring targeted, efficiency-driven automation investments.

Latin America Warehouse Automation Market (2026-32): Regional Projection

Brazil dominates the Latin America Warehouse Automation market with an estimated 45% share, driven by robust logistics infrastructure, concentrated industrial and retail activity, and strong digital transformation policies.

The country’s logistics sector is projected to grow substantially, with overall logistics activity expected to expand by 23% through 2029, fueled by e‑commerce growth, omnichannel retail expansion, and increased investment in automation and digital supply chain solutions . This structural growth positions Brazil as a key hub for advanced warehouse technologies.

A critical factor underpinning Brazil’s dominance is the scale of logistics spending and technology adoption. In 2024, annual logistics and transport expenditures surpassed USD 188 billion, reflecting the economic weight of freight movement and the significant capacity for technology-driven operational improvements .

High-volume logistics corridors, particularly in urban centers such as São Paulo and Rio de Janeiro, generate concentrated demand for automated warehouse hardware, including AMRs, AGVs, AS/RS cranes, and robotic sortation systems.

This combination of economic scale, technological readiness, and concentrated end-user demand ensures that Brazil maintains a clear leadership position in the Latin America warehouse automation market.

Sustained investments in digital transformation and logistics modernization are expected to reinforce this dominance, supporting long-term growth in hardware, software, and robotics adoption across industrial, retail, and e‑commerce sectors.

Gain a Competitive Edge with Our Latin America Warehouse Automation Market Report:

- Latin America Warehouse Automation Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Latin America Warehouse Automation Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Latin America Warehouse Automation Market Policies, Regulations, and Product Standards

- Latin America Warehouse Automation Market Trends & Developments

- Latin America Warehouse Automation Market Dynamics

- Growth Factors

- Challenges

- Latin America Warehouse Automation Market Hotspot & Opportunities

- Latin America Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component - Market Size & Forecast 2022-2032, USD Million

- Hardware

- Automated Storage & Retrieval Systems (Unit-load, Mini-load, Shuttle-based)

- Mobile Robots (AGVs, AMRs)

- Industrial Robots

- Conveyor & Sortation Systems

- Picking, Palletizing & Depalletizing Robots

- Goods-to-Person (GTP) Systems

- Automatic Identification & Data Capture (AIDC)

- Software

- Warehouse Management Systems (WMS)

- Warehouse Control Systems (WCS)

- Warehouse Execution Systems (WES)

- Inventory & Order Management Software

- Fleet & Robot Management Platforms

- AI / ML-based Analytics & Predictive Modules

- Cloud-based vs On-Premise Software

- Services

- Consulting & Advisory

- System Design & Integration

- Installation & Commissioning

- Maintenance & Support

- Training & Change Management

- System Upgrades & Optimization

- Hardware

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- Manual / Basic Automation

- Semi-Automated Warehouses

- Highly Automated Warehouses

- Fully Autonomous Warehouses (AI-driven, robotics-led)

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- Small (Below 50,000 sq. ft.

- Medium (50,000–200,000 sq. ft.)

- Large (200,000–500,000 sq. ft.)

- Mega Warehouses (Above 500,000 sq. ft.)

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- Cloud-based

- On-Premise

- Hybrid

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- Company-Owned Warehouses

- Third-Party Logistics (3PL) / Contract Warehouses

- E-commerce Pure-Play Fulfillment Centers

- Government & Defense Warehouses

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- Small & Medium Enterprise (SMEs)

- Large Enterprise

- By Application- Market Size & Forecast 2022-2032, USD Million

- Order Fulfillment Automation

- Inventory Tracking & Management

- Goods-to-Person (GTP) Picking

- Palletizing & Depalletizing

- Automated Packaging, Labeling & Sorting

- Reverse Logistics & Returns Handling

- By End User - Market Size & Forecast 2022-2032, USD Million

- Retail & E-commerce

- Manufacturing

- Automotive

- Industrial Goods

- Healthcare & Pharmaceuticals

- Food & Beverage

- Consumer Products

- Electronics & High-Tech

- Cold Chain & Perishables

- Others

- By Country

- Brazil

- Mexico

- Argentina

- Chile

- Colombia

- Peru

- Rest of Latin America

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Component - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Automation Technology - Market Size & Forecast 2022-2032, USD Million

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Automation Technology - Market Size & Forecast 2022-2032, USD Million

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Argentina Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Automation Technology - Market Size & Forecast 2022-2032, USD Million

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Chile Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Automation Technology - Market Size & Forecast 2022-2032, USD Million

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Colombia Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Automation Technology - Market Size & Forecast 2022-2032, USD Million

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Peru Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Automation Technology - Market Size & Forecast 2022-2032, USD Million

- By Automation Level- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Size- Market Size & Forecast 2022-2032, USD Million

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Ownership Model- Market Size & Forecast 2022-2032, USD Million

- By Enterprise Size - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Latin America Warehouse Automation Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Dematic Ltda.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daifuku Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell Intelligrated

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SSI Schäfer Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Knapp AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vanderlande Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Swisslog Holding AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Murata Machinery, Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TGW Logistics Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mecalux, S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bastian Solutions, LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eurotecsa, S.A. de C.V

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dematic Ltda.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now