Europe Sports Drinks Market Research Report: Trends & Forecast (2026-2032)

By Product Type (Isotonic Drinks, Hypotonic Drinks, Hypertonic Drinks, Electrolyte & Recovery Drinks), By Formulation (Regular (Sugar-Based), Low-Sugar, Sugar-Free / Zero-Calorie, ... Natural / Organic Formulations, Fortified), By Packaging Type (PET Bottles, Metal Can, Aseptic packages, Tetra-Pak Pouches), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Specialty Sports & Health Stores, Online Retail), By Trade Type (On Trade, Off Trade, Foodservice / On-Premise (Gyms, Stadiums, Fitness Centers)), and others Read more

- Food & Beverages

- Feb 2026

- Pages 265

- Report Format: PDF, Excel, PPT

Europe Sports Drinks Market

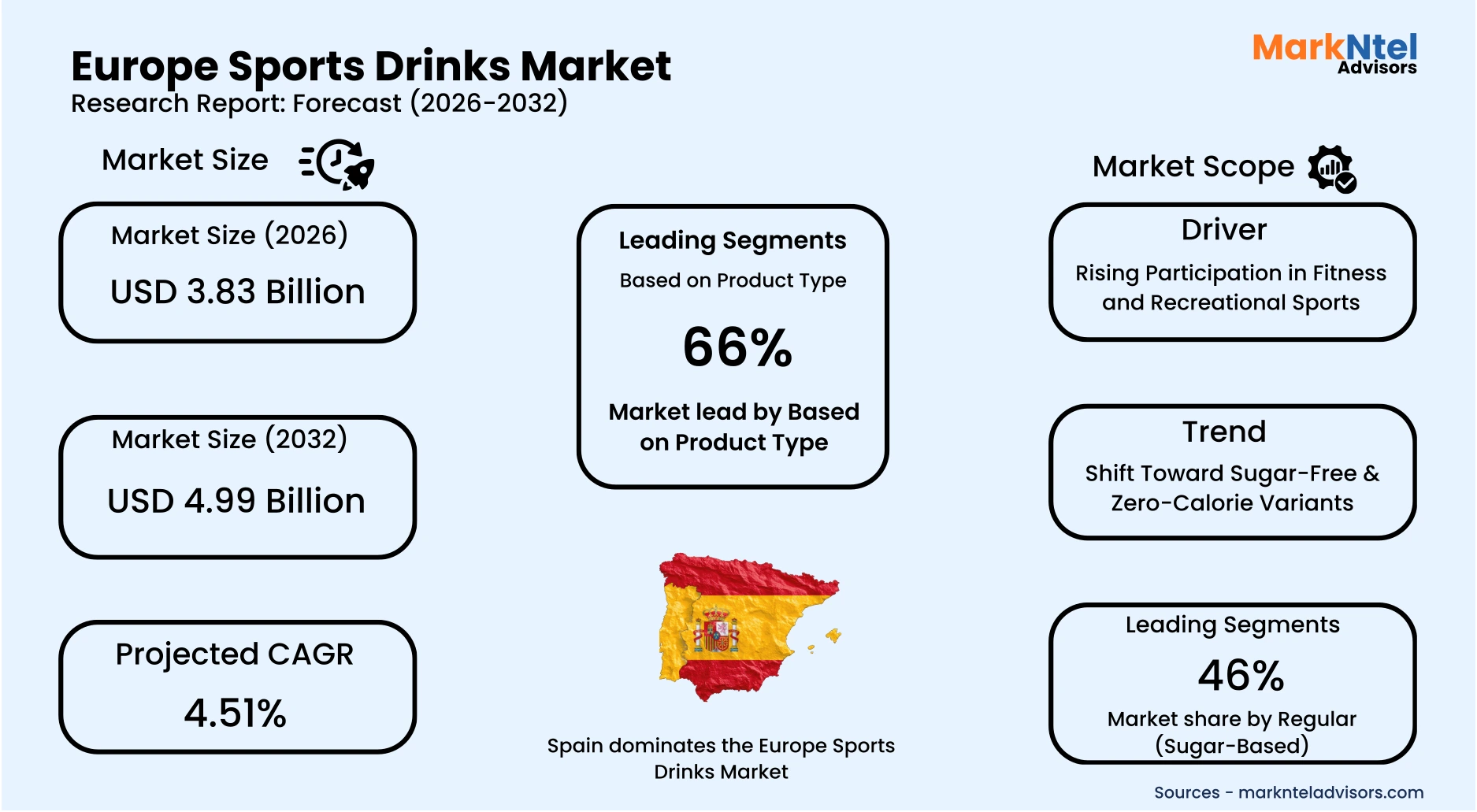

Projected 4.51% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 3.83 Billion

Market Size (2032)

USD 4.99 Billion

Base Year

2025

Projected CAGR

4.51%

Leading Segments

By Formulation: Regular (Sugar-Based)

Europe Sports Drinks Market Report Key Takeaways:

- The Europe Sports Drinks Market size was valued at around USD 3.61 billion in 2025 and is projected grow from USD 3.83 billion in 2026 to USD 4.99 billion by 2032, exhibiting a CAGR of 4.51% during the forecast period.

- Spain holds the largest market share of about 28% in the Europe Sports Drinks Market in 2026, with overall volume anticipated to grow at a CAGR of 5.35%. Germany is the fastest-growing major market in the region, registering a revenue CAGR exceeding 6.5%, and off-trade volume expected to expand at a CAGR of 5.33% during 2026-32.

- By Product Type, the Isotonic Drinks segment represented a significant share of about 66% in the Europe Sports Drinks Market in 2026.

- By Formulation, the Regular (Sugar-Based) segment presented a significant share of about 46% in the Europe Sports Drinks Market in 2026.

- Leading Sports Drinks companies in Europe are Coca-Cola Co., PepsiCo Inc., Otsuka Holdings Co. Ltd., Suntory Holdings Ltd., Congo Brands LLC, Enervit SpA, Oshee Polska Sp zoo, FoodCare Sp zoo, and Others.

Market Insights & Analysis: Europe Sports Drinks Market (2026-32):

The Europe Sports Drinks Market size was valued at around USD 3.61 billion in 2025 and is projected grow from USD 3.83 billion in 2026 to USD 4.99 billion by 2032, exhibiting a CAGR of 4.51% during the forecast period, i.e., 2026-32.

Europe’s sports drinks market continues to expand on the back of sustained participation in structured and recreational physical activity. In 2025, the European Commission reported that the European Week of Sport engaged more than 15 million participants across nearly 40 countries , reflecting broad-based involvement in organized fitness and endurance events. This expanding participation base directly strengthens residential demand for hydration beverages consumed before, during, and after physical activity. Over time, recurring training schedules and competitive sporting calendars have established habitual purchase cycles that support stable volume growth.

Large-scale sporting infrastructure and international event hosting further reinforce market momentum. Spain’s confirmation as host of the 2030 FIFA World Cup final underscores continued investment in stadium development, training facilities, and sports tourism capacity . Such infrastructure expansion increases commercial consumption through stadium concessions, event venues, and organized competitions, while simultaneously stimulating off-trade purchases by spectators and amateur participants. These developments contribute to the heightened visibility and normalization of sports hydration products within mainstream consumer culture.

End-user dynamics remain central to demand sustainability. Residential consumers represent the primary off-trade segment, driven by gym memberships, home fitness routines, and amateur sports leagues. Commercial buyers, including fitness centers, sports academies, and event organizers, generate on-premise sales linked to structured activity schedules; notably, Europe hosts more than 64,000 health and fitness clubs serving approximately 71.6 million members as of 2025, reinforcing organized consumption environments. Institutional initiatives promoting community sports participation indirectly support recurring hydration requirements across schools and local clubs.

Looking ahead, continued expansion of organized sports, endurance events, and recreational fitness participation is expected to sustain market demand. Leading beverage brands are reinforcing category penetration through new electrolyte-enhanced and zero-sugar sports drink launches across European retail networks. As hydration becomes increasingly embedded within active lifestyle routines, repeat consumption patterns are likely to strengthen. Collectively, participation growth, commercial infrastructure expansion, and ongoing product innovation create a resilient foundation for the continued advancement of the Europe sports drinks market.

Europe Sports Drinks Market Recent Developments:

- 2025 : The Coca-Cola Company’s Powerade introduced Powerade Power Water, its first major innovation in five years. The electrolyte-enhanced functional water, formulated with 50% more electrolytes than competitors, will begin regional distribution in late 2025 ahead of a nationwide rollout in 2026. The launch supports Coca-Cola’s broader strategy to expand its presence in the growing functional hydration segment.

- 2024 : Coca-Cola Europacific Partners (CCEP) announced plans to roll out new sports and energy drink innovations across its global markets in 2025, including additions to the Powerade and Monster portfolios. The initiative forms part of the company’s strategy to strengthen its presence in the growing functional beverage segment.

Europe Sports Drinks Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Isotonic Drinks, Hypotonic Drinks, Hypertonic Drinks, Electrolyte & Recovery Drinks), |

| By Formulation | (Regular (Sugar-Based), Low-Sugar, Sugar-Free / Zero-Calorie, Natural / Organic Formulations, Fortified), |

| By Packaging Type | (PET Bottles, Metal Can, Aseptic packages, Tetra-Pak Pouches), |

| By Distribution Channel | (Supermarkets & Hypermarkets, Convenience Stores, Specialty Sports & Health Stores, Online Retail), |

| By Trade Type | (On Trade, Off Trade, Foodservice / On-Premise (Gyms, Stadiums, Fitness Centers)), |

Europe Sports Drinks Market Driver:

Rising Participation in Fitness and Recreational Sports

European institutional policy and public programmes increasingly prioritize physical activity, creating a structural foundation for sustained demand in sports nutrition and hydration products. In 2025, the Erasmus+ Sport programme allocated over USD 87 million to sport projects, funding 350 selected initiatives that promote sport participation, cooperation, and voluntary activities, a 34 % increase in applications from the previous year (2024) . This expansion reflects systematic public investment in sport at the community and membership levels rather than episodic events.

National governments also reinforce this structural shift. For example, Spain published its “National Strategy to Promote Sport against Sedentarism and Physical Inactivity 2025–2030”, with a USD 97 million budget committed to increasing quality sport participation across the population . Such strategies signal long-term public resource commitments to embed sport into everyday life, expanding the base of physically active consumers that drive regular demand for hydration and performance beverages rather than transient episodic purchases.

Complementing funding allocations, EU engagement through flagship initiatives such as the European Week of Sport 2025 engaged over 15 million participants in 80,000+ activities across nearly 40 countries, reinforcing community and lifestyle participation. Official celebration and support of such programmes help sustain multi-year momentum, embedding active behavior into social norms that extend beyond elite sports into widespread recreational and lifestyle segments that regularly consume sports drinks.

This participation rise translates into volume expansion in sports drinks consumption because habitual users require frequent hydration solutions. As public policy deepens active lifestyle participation across age groups and regions, this driver creates a broad structural uplift in the number of potential product purchasers and repeat consumption occasions, a direct cause-and-effect linkage between sustained physical activity engagement and market volume growth, not merely pricing or short-lived trends.

Europe Sports Drinks Market Trend:

Shift Toward Sugar-Free & Zero-Calorie Variants

The transition toward sugar-free and zero-calorie sports drinks has accelerated due to fiscal and public health regulations that directly apply to sugar-sweetened beverages, including isotonic and performance hydration products. In November 2025, the United Kingdom confirmed updates to the Soft Drinks Industry Levy, reinforcing financial disincentives for higher-sugar formulations and sustaining reformulation pressure on sports drink manufacturers. UK government evaluations show that sugar levels in levy-liable beverages have declined by over 40% since implementation, evidencing structural compliance rather than temporary adjustment. Because many sports drinks fall within levy thresholds, producers have increasingly prioritized zero-calorie and reduced-sugar variants.

This regulatory-driven shift is restructuring formulation strategies and portfolio architecture within the sports drinks category. Manufacturers are reformulating electrolyte compositions, adjusting sweetener systems, and redesigning packaging to meet compliance standards while maintaining performance positioning. Retailers across major European markets have expanded shelf allocation for zero-sugar sports drinks, reflecting procurement shifts aligned with public health guidance. For instance, Lucozade Sport expanded its portfolio in 2025 with the launch of Lucozade Sport Zero Sugar in the UK, marking the brand’s strategic entry into the fast-growing low- and no-sugar hydration segment; similarly, new product entries such as KXR Ready-to-Drink and Unwell Hydration in early 2025 demonstrate broader category innovation in reduced-sugar and functional hydration formats. These changes alter production inputs, supply chain requirements, and product mix across both branded and private-label segments.

The persistence of this trend is supported by ongoing European obesity prevention frameworks and national sugar reduction strategies extending through 2030. Because fiscal instruments and labeling regulations remain active policy tools, sports drink producers face continued incentives to maintain compliant formulations. As reformulated variants become embedded in manufacturing systems and retail distribution models, the category’s competitive structure increasingly centers on zero-calorie performance hydration. This represents a durable structural transition shaping long-term market evolution.

Europe Sports Drinks Market Opportunity:

Expansion Potential in Clean-Label and Natural Ingredient Sports Drinks

The opportunity for clean-label sports drinks has strengthened as brands and suppliers actively introduce naturally formulated hydration products across Europe. In 2025, launches such as Unwell Hydration, formulated with real fruit juice and natural flavors without artificial sweeteners, demonstrate the growing commercial viability of clean-label performance beverages . It is also reported that new hydration launches emphasizing natural sweeteners, plant-based ingredients, and additive-free positioning, indicating broader innovation momentum. At the ingredient level, suppliers such as I.T.S. have introduced natural flavor systems tailored for hydration drinks, reinforcing upstream capability to support clean-label reformulation.

This opportunity translates into tangible demand because clean-label positioning aligns with rising consumer preference for ingredient transparency and minimally processed products. Functional beverage analyses consistently highlight that recognizable, real ingredients influence purchase decisions, particularly among health-conscious and digitally engaged consumers. As sports drinks expand beyond elite athletes into lifestyle hydration, natural formulations enhance brand trust and repeat purchase potential. The convergence of consumer preference, supplier readiness, and active product launches creates a commercially scalable growth pocket.

The segment particularly benefits new entrants, as smaller players can design product portfolios around natural inputs without legacy reformulation constraints. Incumbent multinational brands often manage high-volume, cost-optimized formulations centered on artificial sweeteners and synthetic additives. Emerging brands can differentiate through ingredient storytelling, sustainability positioning, and niche distribution strategies. This structural flexibility provides a defensible pathway for market entry and long-term expansion within Europe’s evolving sports drinks landscape.

Europe Sports Drinks Market Challenge:

Stringent EU Regulations on Labeling and Health Claims

The European sports drinks market operates under the EU Nutrition and Health Claims Regulation (EC) No 1924/2006, which strictly governs the use of performance, hydration, and recovery claims on beverage labels. In 2025, the European Commission continued enforcement oversight through coordinated control plans and updated guidance on nutrient profiles and claim substantiation standards. Additionally, the revised EU Directive on Empowering Consumers for the Green Transition, adopted in 2024 and implemented across member states in 2025, tightened rules on environmental and sustainability claims, increasing scrutiny of on-pack marketing language. These regulatory developments reflect a compliance-intensive environment that directly affects sports drink positioning and communication strategies.

The measurable impact of these rules is evident in reformulation, relabeling, and approval procedures that require scientific substantiation before claims such as “improves endurance” or “supports hydration” can be used. Companies must compile clinical evidence and adhere to European Food Safety Authority (EFSA) assessments, extending product development timelines and raising compliance costs. Smaller brands face proportionally higher administrative burdens due to legal advisory, testing, and documentation requirements. Cross-border distribution further compounds complexity, as national authorities conduct independent monitoring and enforcement actions.

This regulatory stringency materially restricts market expansion by limiting marketing flexibility and increasing entry barriers for new participants. Claims-driven differentiation is central to sports drinks, and constrained communication reduces the ability to signal functional benefits to consumers. Extended approval timelines slow innovation cycles and delay commercial launches across EU markets. Consequently, regulatory complexity acts as a structural constraint on scalability, operational efficiency, and competitive entry within the Europe sports drinks sector.

Europe Sports Drinks Market (2026-32) Segmentation Analysis:

The Europe Sports Drinks Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Isotonic Drinks

- Hypotonic Drinks

- Hypertonic Drinks

- Electrolyte & Recovery Drinks

Isotonic drinks dominate the Europe Sports Drinks Market, accounting for approximately 66% of total product type size, primarily because they are specifically formulated to match the body’s natural fluid balance during physical activity. Their balanced combination of carbohydrates and electrolytes enables rapid rehydration and energy replenishment, making them suitable for both endurance athletes and recreational fitness participants. This functional alignment with exercise physiology positions isotonic beverages as the default hydration choice during organized sports, gym workouts, and outdoor activities. The format’s versatility supports consumption before, during, and after exercise, reinforcing repeat purchase behavior across diverse user groups.

Retail availability and brand positioning further strengthen isotonic dominance. Leading European sports drink brands predominantly market isotonic variants, ensuring greater shelf visibility across supermarkets, convenience stores, and stadium outlets. Product innovation cycles also concentrate heavily on isotonic reformulation, including reduced-sugar and zero-calorie extensions, allowing manufacturers to modernize offerings without altering the core hydration proposition. For instance, in March 2025, Electrolit expanded its premium hydration portfolio with new multipack formats across major retail chains, reinforcing isotonic product accessibility and bulk purchase convenience . This adaptability helps preserve volume leadership even amid regulatory pressure on sugar content.

Additionally, isotonic drinks benefit from broader demographic penetration compared to hypotonic or hypertonic alternatives, which are often perceived as niche or recovery-specific products. Their taste profile, moderate sweetness, and ready-to-drink convenience enhance accessibility among casual fitness consumers. Established manufacturing processes and large-scale distribution networks enable efficient production and competitive pricing, reinforcing scalability. Collectively, physiological suitability, retail prioritization, and mass-market appeal sustain isotonic drinks as the leading segment within Europe’s sports drinks market.

Based on Formulation:

- Regular (Sugar-Based)

- Low-Sugar

- Sugar-Free / Zero-Calorie

- Natural / Organic Formulations

- Fortified

Regular (Sugar-Based) formulations lead the Europe Sports Drinks Market with approximately 46% share, largely because carbohydrate content remains central to traditional sports hydration science. During prolonged or high-intensity activity, glucose supports glycogen replenishment and helps sustain performance, making sugar-based isotonic drinks the preferred option for endurance athletes and organized sports participants. Many competitive sporting events and training programs still recommend carbohydrate-electrolyte solutions for optimal performance, reinforcing structural demand for regular formulations rather than purely low-calorie alternatives.

Established brand equity further strengthens this dominance. Several legacy European sports drink brands were originally formulated around carbohydrate-electrolyte blends, and these core SKUs continue to drive high sales volumes across supermarkets, stadium kiosks, and fitness centers. Flavor familiarity and consistent taste profiles enhance consumer loyalty, particularly among repeat purchasers who associate traditional formulations with reliable performance outcomes. Large-scale sponsorships and sports partnerships also predominantly feature standard sugar-based variants, reinforcing their visibility in competitive settings.

Additionally, regular formulations maintain pricing competitiveness due to optimized supply chains and standardized ingredient sourcing. Compared with specialty sweetener-based variants, production processes for sugar-based drinks are well established and cost-efficient at scale. This enables attractive price positioning across mass retail channels, supporting high-volume sales. Combined with functional credibility, brand legacy, and accessible pricing, these factors sustain the leading market share of regular sports drink formulations in Europe.

Europe Sports Drinks Market (2026-32): Regional Projection

Spain dominates the Europe Sports Drinks Market, accounting for approximately 28% of total regional revenue, primarily due to its strong sports culture, favorable climate, and high participation in outdoor and endurance activities. The country hosts numerous football leagues, cycling events, marathons, and fitness festivals throughout the year, sustaining consistent demand for hydration beverages. Spain’s warm weather conditions further elevate per-capita fluid consumption compared to many Northern European countries, structurally supporting higher sports drink volumes. This combination of climatic advantage and active lifestyle participation reinforces Spain’s leadership position within the region.

Retail infrastructure and brand penetration also strengthen Spain’s dominance. Major supermarket chains and convenience networks maintain extensive distribution of leading sports drink brands, ensuring strong shelf visibility and nationwide accessibility. Additionally, Spain benefits from high consumption within off-trade channels, where bulk purchasing and promotional activity stimulate repeat buying. The market’s overall volume is anticipated to grow at a CAGR of 5.35%, reflecting sustained expansion across both recreational and organized sports segments. Moreover, Spain is set to host the final of the 2030 FIFA World Cup, reinforcing long-term sports infrastructure investment and international sporting visibility that further supports hydration demand . Established consumer familiarity with isotonic formulations further supports stable and scalable demand growth.

While Spain leads in overall share, Germany represents the fastest-growing major market, registering a revenue CAGR exceeding 6.5%, with off-trade volume projected to expand at a 5.33% CAGR during the forecast period. Germany’s growth is driven by increasing fitness center memberships, rising health awareness, and broader adoption of performance hydration products. Strong retail modernization and premiumization trends are accelerating category value expansion. Consequently, Spain maintains volume leadership, while Germany emerges as the most dynamic growth engine within Europe’s sports drinks landscape.

Gain a Competitive Edge with Our Europe Sports Drinks Market Report:

- Europe Sports Drinks Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Sports Drinks Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Sports Drinks Market Policies, Regulations, and Product Standards

- Europe Sports Drinks Market Trends & Developments

- Europe Sports Drinks Market Dynamics

- Growth Factors

- Challenges

- Europe Sports Drinks Market Hotspot & Opportunities

- Europe Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Isotonic Drinks

- Hypotonic Drinks

- Hypertonic Drinks

- Electrolyte & Recovery Drinks

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Regular (Sugar-Based)

- Low-Sugar

- Sugar-Free / Zero-Calorie

- Natural / Organic Formulations

- Fortified

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- PET Bottles

- Metal Can

- Aseptic packages

- Tetra-Pak Pouches

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Sports & Health Stores

- Online Retail

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- On Trade

- Off Trade

- Foodservice / On-Premise (Gyms, Stadiums, Fitness Centers)

- By Country

- Spain

- United Kingdom

- France

- Germany

- Russia

- Italy

- Netherlands

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Spain Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- United Kingdom Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- France Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Germany Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Russia Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Italy Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Netherlands Sports Drinks Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Quantity Sold in Million Liters

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Formulation- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Packaging Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Million Liters

- By Trade Type- Market Size & Forecast 2022-2032, USD Million & Million Liters

- Market Size & Outlook

- Europe Sports Drinks Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Coca-Cola Co.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PepsiCo Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Otsuka Holdings Co Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Suntory Holdings Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Congo Brands LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Enervit SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Oshee Polska Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FoodCare Sp zoo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Coca-Cola Co.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now