Europe Ready Meals Market Research Report: Growth Drivers & Forecast (2026-2032)

By Product Type (Dried Ready Meals, Shelf-Stable Ready Meals, Chilled Ready Meals, Frozen Ready Meals), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Onli ... ne Retail, Specialty Stores, Foodservice/HoReCa, Others), By End-User (Household, Commercial), and others Read more

- Food & Beverages

- Feb 2026

- Pages 290

- Report Format: PDF, Excel, PPT

Europe Ready Meals Market

Projected 5.25% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 30.10 Billion

Market Size (2032)

USD 40.92 Billion

Base Year

2025

Projected CAGR

5.25%

Leading Segments

By Product Type: Frozen Ready Meals

Europe Ready Meals Market Report Key Takeaways:

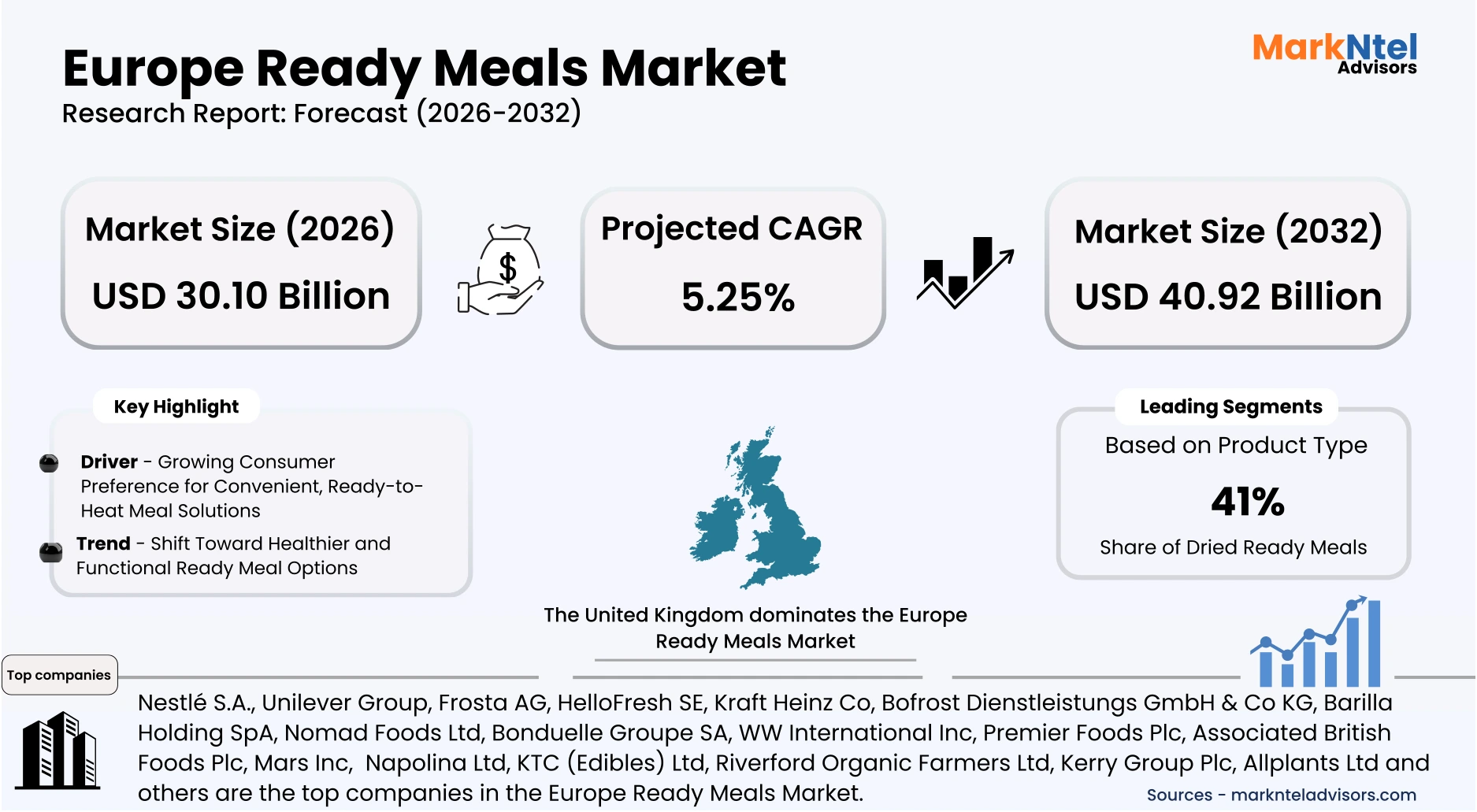

- The Europe Ready Meals Market size was valued at around USD 28.60 billion in 2025 and is projected grow from USD 30.10 billion in 2026 to USD 40.92 billion by 2032, exhibiting a CAGR of 5.25% during the forecast period.

- The U.K. holds the largest market share of about 16% in the Europe Ready Meals Market in 2026.

- By Product Type, the Frozen Ready Meals segment represented a significant share of about 41% in the Europe Ready Meals Market in 2026.

- By Distribution Channel, the Supermarkets/Hypermarkets segment presented a significant share of about 46% in the Europe Ready Meals Market in 2026.

- Leading Ready Meals companies in the Europe market are Nestlé S.A., Unilever Group, Frosta AG, HelloFresh SE, Kraft Heinz Co, Bofrost Dienstleistungs GmbH & Co KG, Barilla Holding SpA, Nomad Foods Ltd, Bonduelle Groupe SA, WW International Inc, Premier Foods Plc, Associated British Foods Plc, Mars Inc, PizzaExpress Plc, Kepak Group, Samworth Bros Ltd, Hain Celestial Group Inc, Valeo Foods Ltd, Loxton Frozen Foods Ltd, Symington's Ltd, Nando's Group Holdings Ltd, Pukka Pies Ltd, Napolina Ltd, KTC (Edibles) Ltd, Riverford Organic Farmers Ltd, Kerry Group Plc, Allplants Ltd, and Others.

Market Insights & Analysis: Europe Ready Meals Market (2026-32):

The Europe Ready Meals Market size was valued at around USD 28.60 billion in 2025 and is projected grow from USD 30.10 billion in 2026 to USD 40.92 billion by 2032, exhibiting a CAGR of 5.25% during the forecast period, i.e., 2026-32.

The Europe ready meals market has demonstrated consistent structural expansion, supported by long-term urbanization and evolving household consumption patterns. With approximately 75% of the EU population residing in urban areas, demand for time-efficient and easily accessible meal solutions has strengthened across metropolitan regions . Rising workforce participation and changing lifestyle dynamics have reduced time allocated to home cooking, structurally reinforcing ready-to-eat meal adoption. These demographic shifts have embedded convenience foods into routine consumption rather than discretionary purchasing behavior.

Current market conditions remain underpinned by strong industrial capacity and organized retail infrastructure. The European Commission identifies food and beverage manufacturing as the largest manufacturing sector in the EU by turnover, supporting stable processed food output across member states. Residential households remain the dominant end-user segment, while commercial and institutional buyers increasingly integrate ready meals to enhance operational efficiency and reduce preparation complexity. In 2024, German food-tech company Freda secured seven-figure funding to expand its premium frozen ready meals portfolio, reflecting strong investor confidence and double-digit monthly growth in the convenience meal segment .

Regulatory and sustainability frameworks further reinforce market expansion by driving packaging and production innovation. The EU Packaging and Packaging Waste Regulation, adopted in 2025, mandates higher recyclability standards, accelerating industry transition toward eco-friendly formats. In response, Sabert rolled out its PulpUltra PFAS-free fiber packaging across Europe in 2025, providing recyclable and industrially compostable solutions tailored for ready-to-eat meals. Such industry-led adaptations align environmental compliance with product innovation, supporting long-term market credibility and consumer trust.

Looking ahead, demographic aging and digital grocery penetration are expected to sustain demand momentum. Eurostat population projections indicate a growing proportion of elderly residents, a cohort favoring convenient, portion-controlled meals. Expansion of online grocery and click-and-collect platforms further broadens ready meal accessibility across urban and semi-urban regions. Supported by demographic fundamentals, regulatory modernization, and continued corporate investment, the Europe ready meals market is positioned for stable medium-term growth anchored in structural demand drivers.

Europe Ready Meals Market Recent Developments:

- 2025 : UK retail giant Tesco introduced a Finest Chef’s Collection of restaurant-quality ready meals across ~160 stores in 2025, featuring 12 chef-created dishes (e.g., lamb, Indian-inspired meals) priced ~USD 22–USD 25 per main. The range aims to elevate retail convenience meals with high-end ingredients and plated-style presentation.

- 2025 : Irish convenience foods producer Greencore Group plc finalized its acquisition of Bakkavör in 2025 for ~USD 1.5 billion, creating a leading UK-based prepared meals entity. The deal expands Greencore’s product capabilities across salads, sandwiches, and ready meals, enhancing scale and retail reach.

Europe Ready Meals Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Dried Ready Meals, Shelf-Stable Ready Meals, Chilled Ready Meals, Frozen Ready Meals), |

| By Distribution Channel | (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Foodservice/HoReCa, Others), |

| By End-User | (Household, Commercial), |

Europe Ready Meals Market Driver:

Growing Consumer Preference for Convenient, Ready-to-Heat Meal Solutions

Rising labor force participation and sustained urbanization across Europe have structurally intensified demand for convenience-oriented food products. According to Eurostat, the EU employment rate reached 75.3% in 2024, with continued workforce expansion observed into 2025, particularly among women. OECD time-use data indicate a steady decline in average daily time allocated to meal preparation across dual-income households. This structural shift in time allocation directly increases reliance on ready-to-heat and pre-prepared meal solutions.

The demand impact is measurable across major European economies through official consumption and retail indicators. The UK Office for National Statistics reported higher overall household expenditure levels in 2024–2025, signaling sustained consumer purchasing capacity. Germany’s Federal Statistical Office reported that ready meal production increased by 25.6% in 2024 compared to 2019, reaching 1.7 million tonnes valued at approximately USD 6.4 billion, indicating strong volume expansion in convenience food consumption. These indicators confirm expanding unit volumes rather than purely inflation-driven value increases .

This driver materially expands market size and volume by altering structural consumption patterns rather than creating temporary demand spikes. Eurostat reports that single-person households in the EU increased by 16.9% between 2015 and 2024, reinforcing structural demand for portion-controlled ready meals . Additionally, 2025 EU food waste reduction initiatives encourage portion efficiency and optimized packaged meal formats. The convergence of demographic restructuring and labor participation growth establishes a sustained and systemic expansion pathway for the Europe ready meals market.

Europe Ready Meals Market Trend:

Shift Toward Healthier and Functional Ready Meal Options

Rising public health concerns and regulatory scrutiny across Europe have accelerated demand for healthier ready meal formulations. According to the World Health Organization, obesity rates in the European Region remain among the highest globally, affecting nearly 60% of adults . In response, governments have intensified nutrition-focused policies, including front-of-pack labeling systems and reformulation targets. These developments have pushed manufacturers to reduce salt, sugar, and saturated fat in ready meals.

The European Commission’s Farm to Fork Strategy continues to promote healthier and more sustainable food systems, encouraging nutrient transparency and reformulation commitments . Several EU member states strengthened mandatory front-of-pack labeling frameworks through 2025, increasing consumer visibility into nutritional profiles. This regulatory environment has structurally altered product development cycles, procurement standards, and labeling compliance requirements. As a result, manufacturers are investing in high-protein, plant-based, and functional ready meal variants to meet evolving standards.

The persistence of this trend is reinforced by long-term demographic and policy drivers rather than temporary consumer preferences. Eurostat data show sustained growth in health-conscious consumer segments and aging populations prioritizing nutritional quality. Public health expenditure pressures further incentivize governments to maintain preventive nutrition strategies. For example, in 2025, UK-based Grubby reintroduced Allplants’ frozen ready meal range featuring high-protein, high-fibre, and plant-diverse formulations, reflecting growing consumer demand for functional plant-based ready meals . Consequently, healthier and functional ready meals are reshaping competitive positioning and innovation pathways across the European market.

Europe Ready Meals Market Opportunity:

Untapped Growth Potential in Multicultural and International Ready Meal Categories

Rising migration and demographic diversification across Europe have structurally expanded demand for multicultural food offerings. According to Eurostat, more than 27 million non-EU citizens resided in the EU in 2024, reshaping consumption patterns across major urban markets. International tourism flows also rebounded strongly in 2024–2025, reinforcing cross-cultural culinary exposure. These structural shifts have normalized global flavors in mainstream retail environments, creating scalable demand for ethnic ready meal formats.

This opportunity translates into tangible market demand through measurable retail and foodservice expansion of international cuisine categories. The UK Office for National Statistics reports sustained growth in household expenditure on restaurants and takeaways serving global cuisines, reflecting broad consumer acceptance. As consumers seek affordable at-home alternatives to dining out, ready meal producers can replicate popular international dishes at lower price points. This creates a direct substitution effect that supports volume expansion in ethnic ready meal SKUs.

This environment is particularly advantageous for new and emerging players due to lower brand legacy constraints and greater formulation flexibility. Smaller manufacturers can introduce niche regional recipes without disrupting established product portfolios dominated by traditional European dishes. Additionally, modern contract manufacturing and private-label partnerships reduce capital barriers to entry. For instance, in 2024, UK-based SHICKEN launched plant-based Indian frozen ready meals at the Netherlands’ largest retailer, Albert Heijn, demonstrating scalable retail demand for international ready meal formats . Similarly, Symington’s introduced a new range of MANOMASA® Mexican-inspired meal kits in an exclusive partnership with Waitrose, further evidencing growing retail investment in international convenience meal formats across the UK . Consequently, multicultural ready meal categories offer scalable entry pathways for differentiated brands seeking rapid market penetration across Europe.

Europe Ready Meals Market Challenge:

Strict EU Regulatory and Food Safety Compliance Requirements

The European ready meals market operates within a highly stringent regulatory framework governing food safety, labeling, and traceability. Regulation (EC) No 178/2002 establishes mandatory traceability across the food chain, while Regulation (EU) No 1169/2011 enforces detailed allergen and nutritional disclosure requirements . In addition, the European Commission adopted Regulation (EU) 2024/2895, effective July 2026, strengthening microbiological criteria for Listeria monocytogenes in ready-to-eat foods . These layered rules significantly increase technical compliance obligations for manufacturers operating across multiple member states.

The regulatory tightening is supported by measurable public health concerns. The European Food Safety Authority’s 2023 Zoonoses Report recorded 2,952 confirmed listeriosis cases, the highest level since 2007, prompting stricter oversight of ready-to-eat products. Compliance now requires enhanced microbiological testing, documented shelf-life validation, and extended responsibility across distributors and retailers. Such requirements raise operational costs and heighten exposure to recalls, product withdrawals, and reputational risk .

This environment materially restricts scalability and market entry, particularly for small and mid-sized producers. Firms must invest in laboratory infrastructure, digital traceability systems, and multilingual packaging adaptations to meet EU-wide standards. Compliance timelines can delay cross-border expansion and new product launches. Consequently, strict EU regulatory and food safety requirements function as a structural barrier limiting growth and operational flexibility in the ready meals market.

Europe Ready Meals Market (2026-32) Segmentation Analysis:

The Europe Ready Meals market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Dried Ready Meals

- Shelf-Stable Ready Meals

- Chilled Ready Meals

- Frozen Ready Meals

Frozen Ready Meals dominate the Europe Ready Meals Market, accounting for approximately 41% of total product-type revenue, primarily due to their extended shelf life, supply chain efficiency, and strong household penetration. Unlike chilled variants, frozen meals offer longer storage stability without compromising food safety, making them suitable for bulk purchasing and weekly shopping patterns common across European households. The widespread availability of home freezers and high freezer penetration rates across Western Europe further support consistent demand. This storage advantage reduces food waste risk and enhances purchase frequency, strengthening volume contribution.

Retail and distribution dynamics further reinforce this segment’s leadership position. Frozen ready meals benefit from established cold-chain infrastructure and dedicated freezer aisle space in major supermarket chains, ensuring visibility and scale. Manufacturers continue to introduce premium frozen SKUs, including chef-inspired dishes, plant-based options, and portion-controlled formats, expanding consumer appeal. For example, Associated British Foods increased its stake in UK-based premium frozen ready meal producer Cook Trading in 2024, reflecting growing corporate investment confidence in the frozen convenience segment . Technological advancements in flash-freezing and packaging innovation have improved texture retention and product quality, narrowing the perception gap between chilled and frozen formats.

Additionally, frozen ready meals provide cost efficiency for both retailers and consumers. Bulk production, longer inventory cycles, and reduced spoilage losses improve margin stability compared to chilled products. The segment also supports private-label expansion, enabling competitive pricing strategies without sacrificing profitability. These structural advantages collectively position frozen ready meals as the dominant product category in the European ready meals market.

Based on Distribution Channel:

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Foodservice/HoReCa

- Others

Supermarkets and hypermarkets dominate the Europe Ready Meals Market, accounting for approximately 46% of total distribution channel revenue, primarily due to their structural control over organized grocery retail and high private-label penetration. In Europe, the majority of packaged food purchases occur through large-format grocery chains, positioning ready meals as a core category within mainstream retail rather than niche outlets. Supermarkets leverage centralized procurement systems and long-term supplier agreements to secure volume-based pricing advantages, enabling competitive positioning across economy, mid-tier, and premium ready meal segments.

Category management capabilities further reinforce this dominance. Large retailers allocate dedicated shelf space to frozen and chilled ready meals, optimize assortment based on regional demand analytics, and frequently deploy multi-buy promotions and bundled meal deals to stimulate higher basket value. Private-label ready meals, which are primarily supermarket-controlled, enhance margin stability while strengthening consumer loyalty. This dual-brand strategy, which expands price accessibility and broadens demographic reach.

Additionally, supermarkets integrate ready meals into omnichannel retail ecosystems, including online grocery platforms and click-and-collect services, extending their distribution footprint beyond physical stores. Their scale enables efficient inventory turnover, centralized logistics coordination, and reduced per-unit handling costs compared to smaller channels. These structural advantages in retail concentration, pricing leverage, assortment control, and supply chain integration collectively position supermarkets and hypermarkets as the dominant distribution channel in the European ready meals market.

Europe Ready Meals Market (2026-32): Regional Projection

The United Kingdom dominates the Europe Ready Meals Market, accounting for approximately 16% of total regional revenue, primarily due to its deeply embedded ready meal consumption culture and high household penetration rates. The UK has one of the most mature convenience food markets in Europe, with ready meals forming a routine component of weekly grocery baskets. According to the UK government statistics, household expenditure on prepared and convenience foods has shown sustained resilience, reflecting structural reliance on ready-to-eat meal formats rather than occasional purchase behavior . This entrenched consumption pattern provides a stable demand base unmatched by most continental markets.

The dominance is further reinforced by the UK’s highly developed chilled ready meal segment, which is more advanced than in many other European countries. Major UK retailers allocate significant shelf space to private-label ready meals spanning economy to premium tiers, driving both accessibility and innovation. The country’s strong private-label ecosystem enables rapid product development cycles, seasonal launches, and category experimentation. This retail-driven innovation intensity accelerates volume turnover and strengthens repeat purchasing behavior.

Additionally, the UK benefits from concentrated modern retail infrastructure and strong online grocery penetration, facilitating seamless distribution of frozen and chilled ready meals nationwide. High urban density and dual-income household prevalence further support convenience-oriented consumption. The combination of cultural acceptance, retail innovation leadership, and structured distribution networks collectively positions the United Kingdom ahead of other European countries in the ready meals market share.

Gain a Competitive Edge with Our Europe Ready Meals Market Report:

- Europe Ready Meals Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Ready Meals Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Ready Meals Market Policies, Regulations, and Product Standards

- Europe Ready Meals Market Trends & Developments

- Europe Ready Meals Market Dynamics

- Growth Factors

- Challenges

- Europe Ready Meals Market Hotspot & Opportunities

- Europe Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Dried Ready Meals

- Shelf-Stable Ready Meals

- Chilled Ready Meals

- Frozen Ready Meals

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

- Foodservice/HoReCa

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Household

- Commercial

- By Country

- Germany

- The UK

- Italy

- France

- Spain

- The Netherlands

- Poland

- Belgium

- Sweden

- Finland

- Norway

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The UK Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The Netherlands Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Poland Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Belgium Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Sweden Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Finland Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Norway Ready Meals Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Europe Ready Meals Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Nestlé S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unilever Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Frosta AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HelloFresh SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kraft Heinz Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bofrost Dienstleistungs GmbH & Co KG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Barilla Holding SpA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nomad Foods Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bonduelle Groupe SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- WW International Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Premier Foods Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Associated British Foods Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mars Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PizzaExpress Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kepak Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samworth Bros Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hain Celestial Group Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Valeo Foods Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Loxton Frozen Foods Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Symington's Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nando's Group Holdings Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Pukka Pies Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Napolina Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KTC (Edibles) Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Riverford Organic Farmers Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kerry Group Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Allplants Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nestlé S.A.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now