China Food Waste Management Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Waste Type (Fruits & Vegetables, Dairy & Dairy Products, Cereals & Grains, Meat & Poultry, Fish & Seafood, Processed Foods, Others), By Management Process (Aerobic Digestion, An ... aerobic Digestion, Combustion/Incineration, Others), By Service Type (Collection, Transportation, Disposal/Recycling), By Source (Primary Food Producers, Food Manufacturers, Food Distributors and Suppliers, Food Service Providers, Municipalities and Households), By Application (Animal Feed, Fertilizers, Biofuel & Biogas, Power Generation, Others), By End User (Municipal Authorities / Governments, Private Waste Management Firms, Food Manufacturers & Processors, Retailers & Food Service Chains, Household Consumers), and others Read more

- Food & Beverages

- Feb 2026

- Pages 120

- Report Format: PDF, Excel, PPT

China Food Waste Management Market

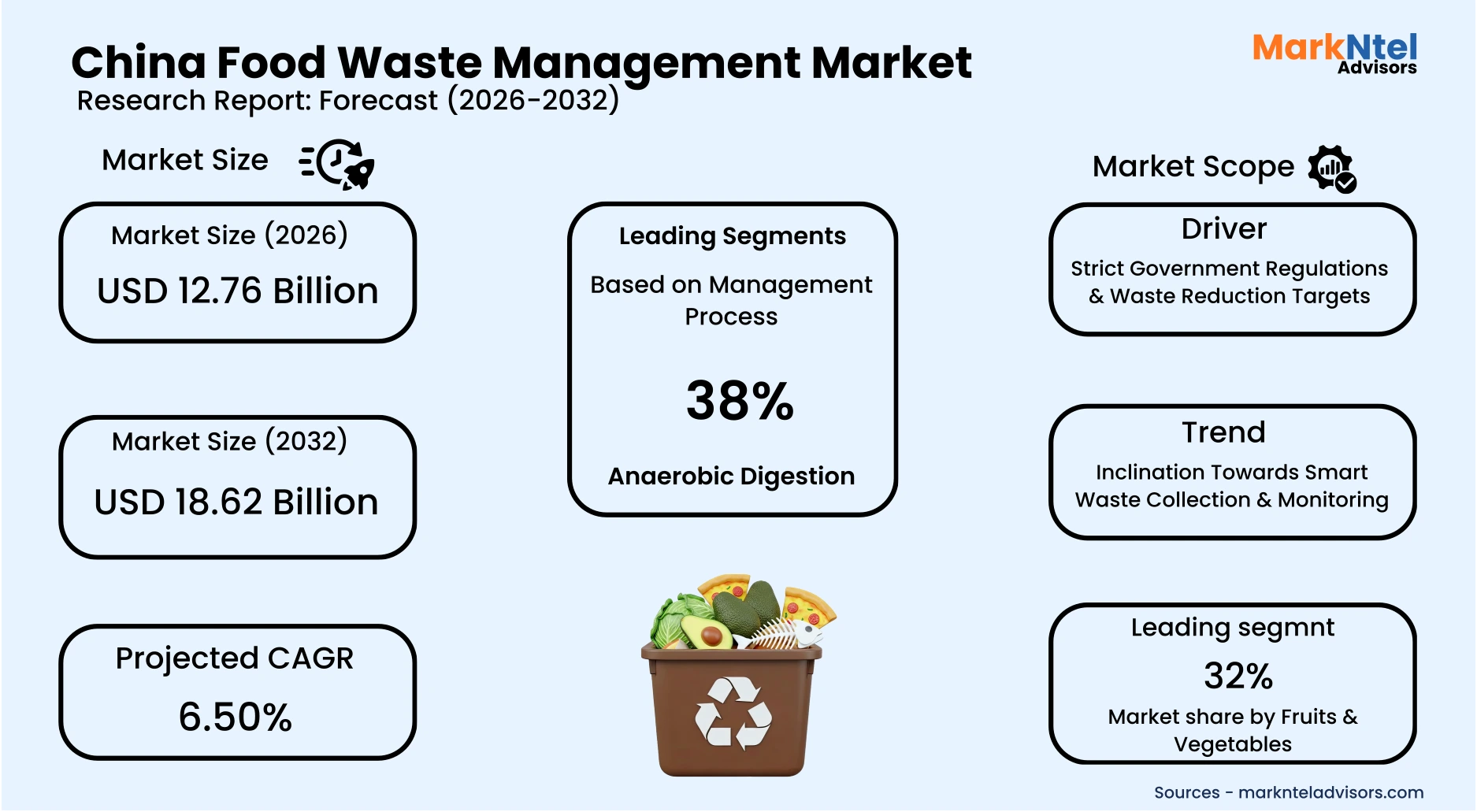

Projected 6.50% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 12.76 Billion

Market Size (2032)

USD 18.62 Billion

Base Year

2025

Projected CAGR

6.50%

Leading Segments

By Waste Type: Fruits & Vegetables

China Food Waste Management Market Report Key Takeaways:

- The China Food Waste Management market size was valued at USD 11.92 billion in 2025 and is projected to grow from USD 12.76 billion in 2026 to USD 18.62 billion by 2032, exhibiting a CAGR of 6.50% during the forecast period.

- East China holds the largest market share of about 42% in the China Food Waste Management Market in 2026.

- By waste type, the fruits & vegetables segment represented a significant share of about 32% in the China Food Waste Management Market in 2026.

- By management process, the anaerobic digestion segment presented a significant share of about 38% in the China Food Waste Management Market in 2026.

- Leading food waste management companies in the China Market are Veolia Environnement S.A., SUEZ Group, China Everbright Environment Group, Capital Environment Holdings, Dynagreen Environmental Protection Group, Beijing Enterprises Environment Group, Shanghai Environment Group, Veolia China, SUEZ China, Waste Management, Inc., Republic Services, Inc., Reworld Holding Corporation, Bioforce USA, Inc., Rubicon Global, and Others.

Market Insights & Analysis: China Food Waste Management Market (2026-32):

The China Food Waste Management Market size was valued at around USD 11.92 billion in 2025 and is projected to grow from USD 12.76 billion in 2026 to USD 18.62 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 6.50% during the forecast period, i.e., 2026-32.

The China Food Waste Management Market is projected to expand steadily, driven by increasingly stringent government regulations and waste reduction mandates, alongside rising adoption of smart waste collection, digital monitoring systems, and data-driven management technologies nationwide.

At the national level, in November 2024, the Central Committee of the Communist Party of China and the State Council jointly issued the Food Conservation and Anti-Food Waste Action Plan. The policy establishes a clear roadmap to build a long-term governance mechanism by 2027 , targeting food loss rates across production, storage, transportation, and processing stages below international averages, while significantly reducing per-meal waste in public institutions and commercial catering. The plan institutionalizes food conservation within administrative performance systems, signaling heightened compliance requirements nationwide.

Complementing national directives, Shanghai’s municipal government intensified enforcement in 2024 through a comprehensive local regulatory framework aligned with the Anti-Food Waste Law. Authorities defined 28 priority annual tasks, embedded food conservation metrics into district-level accountability evaluations, and expanded technical standards across agriculture, catering, retail, and storage sectors. Regulatory inspections covered approximately 112,000 catering establishments, resulting in 341 enforcement cases demonstrating active supervisory oversight and measurable compliance enforcement .

Provincial-level innovation further strengthens implementation depth. For instance, in August 2024, central authorities highlighted diversified regional practices supporting the Anti-Food Waste Law. Guangdong introduced a citizen-based “Snap & Report” digital application to monitor waste violations, while Guangxi embedded food conservation messaging into public cultural events. Several provinces also operationalized “civilized dining red-black list” systems to enhance transparency and public accountability . These localized mechanisms collectively broaden enforcement reach beyond traditional regulatory inspections.

In January 2025, the Grain Conservation and Food Waste Reduction Action Plan reinforced quantitative national targets. The initiative aims to reduce per-capita food waste and bring China’s overall grain loss rate below the global average of approximately 14% by 2027 .

Official data indicate China’s current average grain loss is about 7%, with authorities estimating potential savings of up to 20 million tons through improved scientific storage systems, smart logistics upgrades, high-standard granary construction, and establishment of a nationwide statistical monitoring framework.

Digital transformation is emerging as a parallel growth catalyst. Hangzhou’s planned 2026 rollout of “digital passports” for waste streams will enable real-time tracking from collection to processing via intelligent management platforms, enhancing traceability, sorting accuracy, and resource recovery efficiency.

The convergence of stringent regulatory enforcement, quantified reduction targets, and smart monitoring infrastructure is reshaping China’s food waste management landscape. Sustained policy pressure and technology integration will continue to formalize operations, expand infrastructure investment, and drive long-term market expansion.

China Food Waste Management Market Recent Developments:

- 2025: Shenzhen’s 24-hour smart food bank initiative gained prominence as a community-oriented solution linking waste reduction with social support. Operated via refrigerated smart cabinets, the program stores surplus or near-expiry food donated by local businesses and makes it available through the “iShenzhen” app. Since its launch, the initiative has distributed around 500,000 portions, preventing an estimated 195 tons of food from going to waste and cutting approximately 390 tons of carbon emissions.

- 2025: Yantian District in Shenzhen expanded its food waste management capabilities by launching an intelligent “5G + robotics” black soldier fly breeding project at its environmental park. The system processes about 15 tons of solid food waste per day, transforming it into valuable outputs such as insect protein, biogas, biodiesel, and organic fertilizer. The project processed over 55,000 tons of food waste and reduced CO₂ emissions by 326 tons, showcasing technological innovation in sustainable organic waste utilization.

China Food Waste Management Market Scope:

| Category | Segments |

|---|---|

| By Waste Type | (Fruits & Vegetables, Dairy & Dairy Products, Cereals & Grains, Meat & Poultry, Fish & Seafood, Processed Foods, Others), |

| By Management Process | (Aerobic Digestion, Anaerobic Digestion, Combustion/Incineration, Others), |

| By Service Type | (Collection, Transportation, Disposal/Recycling), |

| By Source | (Primary Food Producers, Food Manufacturers, Food Distributors and Suppliers, Food Service Providers, Municipalities and Households), |

| By Application | (Animal Feed, Fertilizers, Biofuel & Biogas, Power Generation, Others), |

| By End User | (Municipal Authorities / Governments, Private Waste Management Firms, Food Manufacturers & Processors, Retailers & Food Service Chains, Household Consumers), |

China Food Waste Management Market Driver:

Strict Government Regulations & Waste Reduction Targets

China’s food waste management market is being significantly driven by the institutionalization of nationwide monitoring and enforcement systems. In 2023, the National Development and Reform Commission (NDRC) and the Ministry of Commerce launched the country’s first national sample survey on food waste, initially covering approximately 30 prefecture-level cities.

Further, the initiative aims to systematically assess food waste patterns across catering and related sectors to enhance regulatory supervision and data-driven policy formulation. By 2025, authorities plan to expand the survey coverage to around 100 cities and, where feasible, extend it to county-level regions. This scale-up strengthens benchmarking capabilities, improves traceability of waste generation, and supports targeted administrative interventions.

Parallel enforcement efforts at the municipal level further reinforce regulatory momentum. For example, in 2025, Tianjin intensified implementation of the nationwide “Clear Your Plate” campaign under the Anti-Food Waste Law, encouraging restaurants to adopt portion-size guidelines and provide food-saving reminders to consumers .

Meanwhile, Beijing piloted structured “food bank” redistribution programs to channel surplus edible food toward social welfare groups, aligning operational practice with national conservation regulations . Collectively, expanded statistical monitoring, stricter compliance campaigns, and redistribution frameworks are formalizing waste reduction mechanisms across urban centers.

The integration of nationwide data collection with localized enforcement initiatives is strengthening transparency, accountability, and operational discipline. These measures directly stimulate demand for advanced waste tracking, redistribution logistics, and compliance-driven waste management infrastructure, accelerating market expansion.

China Food Waste Management Market Trend:

Inclination Towards Smart Waste Collection & Monitoring

China’s transition toward digitized urban management is accelerating the deployment of intelligent food waste collection and monitoring infrastructure. Between 2024 and 2025, Shanghai advanced smart waste management pilots across districts including Jing’an, Putuo, and Huangpu. These initiatives integrate AI-powered cameras, purity recognition technologies, intelligent weighing devices, and real-time data transmission systems into daily collection operations.

The smart platforms enable automated identification of improper segregation, instant anomaly alerts, and dynamic route optimization for sanitation teams. By linking collection vehicles with centralized management dashboards, authorities can monitor waste levels in real time and adjust dispatch schedules accordingly. This reduces unnecessary collection trips, minimizes on-street waste exposure time, and enhances operational efficiency. Intelligent weighing systems further support data-backed performance tracking, strengthening compliance with waste-sorting regulations and sustainability targets.

Shanghai’s model reflects a broader urban governance shift toward digital supervision and precision resource management. The integration of AI recognition systems and smart alert mechanisms enhances transparency across the waste lifecycle, from source separation to transportation and processing.

The rapid integration of AI-enabled monitoring, data analytics, and automated response systems is transforming food waste management from labor-intensive operations to technology-driven infrastructure. Continued smart city investments will accelerate adoption of intelligent collection systems, driving sustained growth in China’s food waste management market.

China Food Waste Management Market Opportunity:

Public–Private Partnerships to Offer Lucrative Growth Opportunities

China’s expanding Zero-Waste City initiative, led by the Ministry of Ecology and Environment, represents a significant opportunity for the food waste management market by accelerating public–private collaboration.

As of 2025, more than 3,700 zero-waste projects are being implemented nationwide with cumulative investment exceeding approximately USD 140 billion. These projects focus on reducing solid waste generation at source, strengthening recycling systems, and promoting resource utilization across urban and rural areas.

A substantial portion of these initiatives integrates private operators into municipal waste collection, treatment, and resource recovery networks. This has encouraged the construction of waste-to-energy plants, organic and kitchen waste treatment facilities, and advanced recycling infrastructure, expanding commercial participation in waste management value chains.

At the city level, governments such as those in Hangzhou and Suzhou are partnering with technology firms and environmental service providers to develop smart waste management platforms. These systems enhance real-time monitoring, sorting efficiency, and circular reuse of food waste, creating scalable business opportunities for private technology and infrastructure providers.

Large-scale capital deployment and structured PPP frameworks significantly reduce entry barriers for private players. Continued expansion of zero-waste city programs will stimulate long-term demand for advanced food waste treatment, smart monitoring systems, and integrated recycling infrastructure thereby accelerating growth in China’s food waste management market.

China Food Waste Management Market Challenge:

High Capital and Operational Costs

High capital intensity significantly constrains the expansion of China’s food waste treatment infrastructure, as substantial upfront investment requirements limit project feasibility, slow facility deployment, and deter private sector participation in large-scale operations.

According to a 2025 peer-reviewed technical analysis published in an industry journal affiliated with China’s environmental engineering sector, operational data from 530 centralized and 3,971 decentralized food waste treatment facilities (total designed capacity: 141,100 tons per day) show that capital investment costs range from approximately USD 41,000–USD 109,000 per ton of treatment capacity.

The study further indicates that many facilities operate at below 70% utilization rates, significantly weakening economies of scale and increasing per-ton processing costs. In addition, average government subsidies were reported at USD 32 insufficient to fully offset construction, energy consumption, odor control, and maintenance expenses. Decentralized plants, while improving collection coverage, face higher per-unit operational costs and technical inefficiencies, placing additional fiscal pressure on municipal authorities.

Substantial upfront capital requirements, suboptimal plant utilization, and limited subsidy support constrain financial viability. These cost pressures discourage private investment and delay infrastructure expansion, ultimately slowing the overall growth trajectory of China’s food waste management market.

China Food Waste Management Market (2026-32) Segmentation Analysis:

The China Food Waste Management Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Waste Type:

- Fruits & Vegetables

- Dairy & Dairy Products

- Cereals & Grains

- Meat & Poultry

- Fish & Seafood

- Processed Foods

- Others

The fruits & vegetables segment dominates the China Food Waste Management market, accounting for approximately 32% of the market size, primarily due to the country’s substantial agricultural output and the highly perishable nature of fresh produce.

As the world’s leading producer of fruits and vegetables, China generates significant volumes throughout cultivation, wholesale distribution, retail, and food service channels. This scale inherently results in comparatively higher waste volumes versus processed or shelf-stable food categories.

Fresh produce is particularly vulnerable to post-harvest losses arising from handling damage, inadequate temperature control, storage limitations, and logistical inefficiencies. Despite ongoing improvements in cold-chain infrastructure, variability in preservation capacity especially across lower-tier cities and rural supply chains continues to contribute to measurable spoilage rates. In addition, stringent visual and quality standards in urban retail markets lead to the rejection of cosmetically imperfect but edible products, further expanding discard volumes.

Food service establishments, wet markets, supermarkets, and wholesale markets collectively generate substantial daily quantities of fruit and vegetable residues, forming a stable and concentrated organic waste stream.

Given the structural scale of production, rapid urban consumption patterns, and regulatory emphasis on source separation of organic waste, fruits and vegetables are expected to maintain their leading contribution within China’s food waste management ecosystem.

Based on Management Process:

- Aerobic Digestion

- Anaerobic Digestion

- Combustion/Incineration

- Others

The anaerobic digestion segment dominates the China Food Waste Management Market, accounting for about 38% of total market size, reflecting the country’s strategic emphasis on resource efficiency, renewable energy generation, and carbon mitigation.

The technology enables the controlled biological decomposition of organic waste in oxygen-free environments, producing biogas and nutrient-rich digestate. This dual-output model supports both waste reduction and energy recovery objectives, aligning closely with national circular economy and decarbonization frameworks.

China’s substantial and steadily segregated kitchen waste volumes provide a reliable feedstock base for large-scale AD facilities, particularly in densely populated urban regions. Compared with aerobic composting, anaerobic digestion offers superior energy recovery potential and greater greenhouse gas mitigation benefits when supported by proper methane capture systems. The scalability of centralized AD plants makes them well-suited for integration into municipal solid waste treatment infrastructure.

Furthermore, local governments increasingly favor anaerobic digestion within public-private infrastructure investments, as it reduces landfill dependency, minimizes secondary pollution risks, and contributes to renewable power generation targets. The ability to monetize biogas output enhances financial viability relative to conventional treatment methods.

Given China’s regulatory push for organic waste diversion, renewable energy substitution, and emissions control, anaerobic digestion remains the most strategically aligned and economically sustainable solution within the national food waste treatment framework.

China Food Waste Management Market (2026-32): Regional Projection

East China dominates the China Food Waste Management Market with an estimated 42% share, driven by its advanced economic structure, dense urban population, and mature municipal waste infrastructure.

Provinces and municipalities such as Shanghai, Jiangsu, and Zhejiang host large hospitality sectors, extensive food processing industries, and high per-capita consumption levels, resulting in substantial and consistent organic waste generation. This scale supports centralized treatment facilities and accelerates the adoption of technology-enabled waste segregation and processing systems.

In 2025, the strengthened national regulatory framework further reinforced the region’s leadership position. Under the Anti-Food Waste Law, catering establishments are required to actively discourage excessive ordering and are authorized to impose disposal charges on significant leftovers. Updated national standards now integrate food waste reduction metrics into credit rating assessments and operational guidelines for catering services .

Demonstrating measurable compliance outcomes, Shanghai certified approximately 2,950 “green restaurants” focused on waste minimization practices. Moreover, participation in the “Clear Your Plate” campaign contributed to an estimated reduction of nearly 50% in kitchen waste among involved restaurants.

These enforceable regulatory mechanisms, combined with systematic supervision and accountability structures, have institutionalized waste reduction practices across commercial and institutional sectors.

With strong policy enforcement, technological integration, and large-scale waste volumes, East China maintains a structurally advantageous position, sustaining robust demand for organized food waste collection, monitoring, and treatment infrastructure.

Gain a Competitive Edge with Our China Food Waste Management Market Report:

- China Food Waste Management Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- China Food Waste Management Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- China Food Waste Management Market Policies, Regulations, and Product Standards

- China Food Waste Management Market Trends & Developments

- China Food Waste Management Market Dynamics

- Growth Factors

- Challenges

- China Food Waste Management Market Hotspot & Opportunities

- China Food Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- Fruits & Vegetables

- Dairy & Dairy Products

- Cereals & Grains

- Meat & Poultry

- Fish & Seafood

- Processed Foods

- Others

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- Aerobic Digestion

- Anaerobic Digestion

- Combustion/Incineration

- Others

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- Collection

- Transportation

- Disposal/Recycling

- Landfill

- Incineration

- Composting

- Others

- By Source - Market Size & Forecast 2022-2032, USD Million

- Primary Food Producers

- Food Manufacturers

- Food Distributors and Suppliers

- Food Service Providers

- Municipalities and Households

- By Application - Market Size & Forecast 2022-2032, USD Million

- Animal Feed

- Fertilizers

- Biofuel & Biogas

- Power Generation

- Others

- By End User- Market Size & Forecast 2022-2032, USD Million

- Municipal Authorities / Governments

- Private Waste Management Firms

- Food Manufacturers & Processors

- Retailers & Food Service Chains

- Household Consumers

- By Region- Market Size & Forecast 2022-2032, USD Million

- East China

- North China

- South China

- Central China

- Southwest China

- Northwest China

- Northeast China

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Waste Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Fruits & Vegetables Waste Management Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Dairy & Dairy Products Waste Management Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Cereals & Grains Waste Management Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Meat & Poultry Waste Management Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Fish & Seafood Waste Management Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Processed Foods Waste Management Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Management Process - Market Size & Forecast 2022-2032, USD Million

- By Service Type - Market Size & Forecast 2022-2032, USD Million

- By Source - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Food Waste Management Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Veolia Environnement S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SUEZ Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China Everbright Environment Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Capital Environment Holdings

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dynagreen Environmental Protection Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beijing Enterprises Environment Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shanghai Environment Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SUEZ China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Waste Management, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Republic Services, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Reworld Holding Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bioforce USA, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rubicon Global

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Veolia Environnement S.A.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now