GCC Wearable Health Devices Market Research Report: Forecast (2026-2032)

GCC Wearable Health Devices Market - By Product Type (Diagnostic & Monitoring Devices, Vital Sign Monitoring Devices, Heart Rate Monitors, Blood Pressure Monitors, Pulse Oximeters, ... Activity Monitors, Spirometers, Multiparameter trackers, Others, Sleep Monitoring Devices, Sleep Trackers, Wrist Actigraphs, Polysomnographs, Others, Electrocardiographs & Fetal/Obstetric Devices, Neuromonitoring Devices, Electroencephalographs, Electromyographs, Others, Continuous Glucose Monitoring (CGM) Devices, Therapeutic Devices, Pain Management Devices, Neurostimulation Devices, Others, Insulin/Glucose Management Devices, Insulin Pumps, Others, Rehabilitation Devices, Accelerometers & Sensors, Ultrasound Platform, Others, Respiratory Therapy Devices, Ventilators, Positive Airway Pressure (PAP) Devices, Portable Oxygen Concentrators, Others), By Device Type (Smartwatches, Trackers, Smart Clothing, Wearable Patches / Skin Sensors, Headband, Handheld, Shoe Sensors, Strap / Clip / Bracelet, Wrist Bands, Others), By Grade (Consumer-Grade Wearable Devices, Clinical-Grade Wearable Devices), By Application (General Health & Fitness, Remote Patient Monitoring (RPM), Home Healthcare / Self-Care, Sports and Fitness), By Distribution Channel (Online Channels, Pharmacies & Retail Pharmacies, Hypermarkets & Specialty Stores), and others Read more

- Healthcare

- Mar 2026

- Pages 168

- Report Format: PDF, Excel, PPT

GCC Wearable Health Devices Market

Projected 14.7% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 1.37 Billion

Market Size (2032)

USD 3.12 Billion

Base Year

2025

Projected CAGR

14.7%

Leading Segments

By Device Type: Smartwatches

GCC Wearable Health Devices Market Report Key Takeaways:

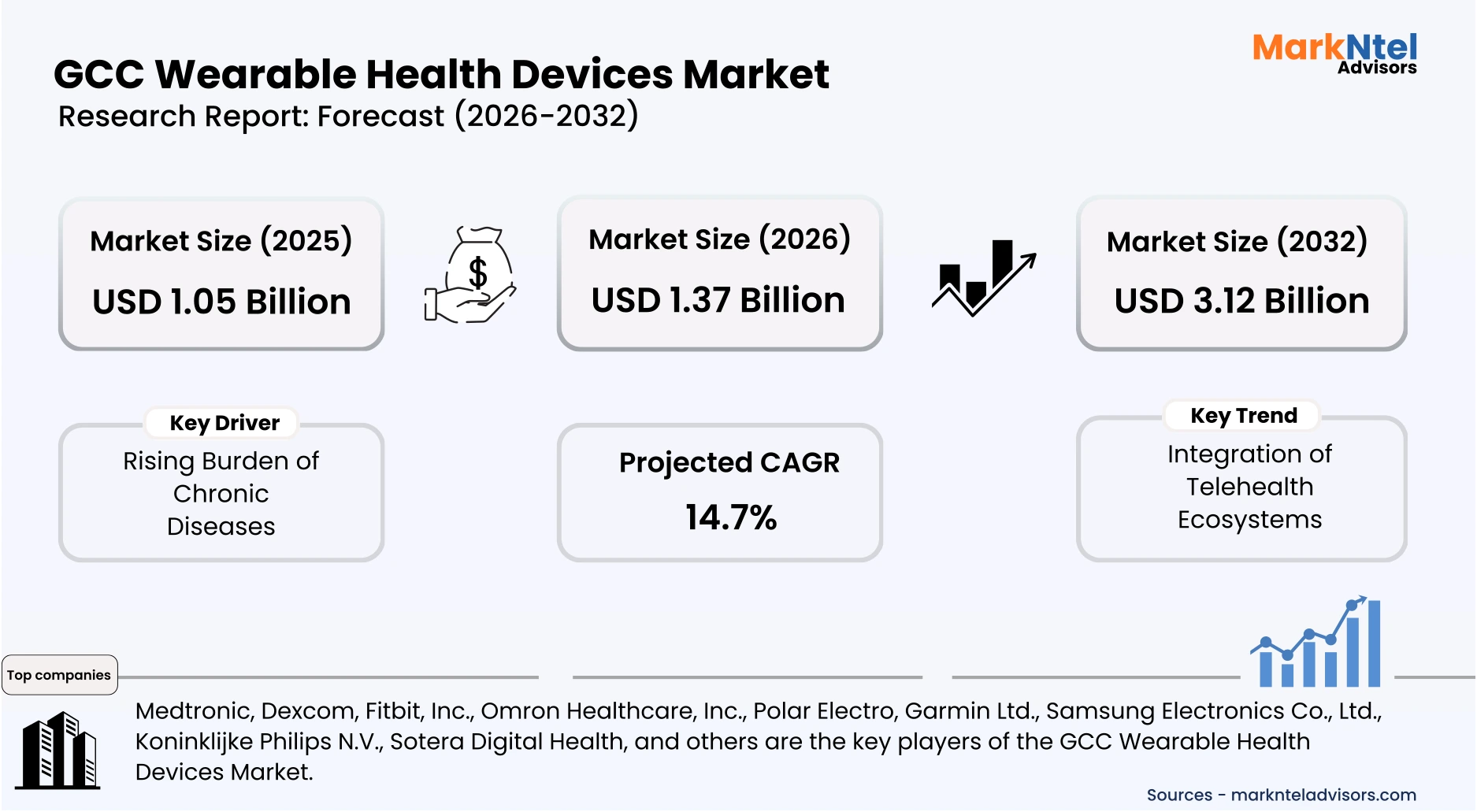

- The GCC Wearable Health Devices Market size is valued at around USD 1.05 billion in 2025 and is projected to grow from USD 1.37 billion to USD 3.12 billion by 2032. The estimated CAGR from 2026 to 2032 is around 14.7%, indicating strong growth.

- By Product Type, the diagnostic & monitoring devices segment represented 44% of the GCC Wearable Health Devices Market size in 2026.

- By Device Type, the smartwatches represented 42% of the GCC Wearable Health Devices Market size in 2026.

- By Country, Saudi Arabia leads the GCC Wearable Health Devices Market with a dominant 37% share in 2026.

- The leading wearable health device companies in the GCC are Medtronic, Dexcom, Fitbit, Inc., Omron Healthcare, Inc., Polar Electro, Garmin Ltd., Samsung Electronics Co., Ltd., Koninklijke Philips N.V., Sotera Digital Health, and others.

Market Insights & Analysis: GCC Wearable Health Devices Market (2026- 2032):

The GCC Wearable Health Devices Market size is valued at around USD 1.05 billion in 2025 and is projected to grow from USD 1.37 billion to USD 3.12 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 14.7% during the forecast period, i.e., 2026-32.

The GCC Wearable Health Devices Market is experiencing rapid growth, primarily driven by the rising prevalence of chronic diseases and the increasing integration of wearable technologies within regulated telehealth and remote patient monitoring ecosystems.

Diabetes prevalence across GCC countries significantly exceeds the global average, reaching 18.3% in Saudi Arabia, 15.4% in the United Arab Emirates, 22% in Kuwait, 15.7% in Oman, and 16.3% in Bahrain.

Obesity prevalence in the region is similarly elevated, averaging 23.7% compared with a global average of 12.91%, intensifying long-term cardiometabolic risks and increasing demand for continuous health monitoring solutions.

Alongside epidemiological pressure, governments are embedding digital health and remote care into national healthcare reforms. For instance, Saudi Arabia’s Health Sector Transformation Program under Vision 2030 prioritizes digital health adoption, outpatient care, and data-driven clinical workflows, expanding telehealth procurement and systematic integration of wearable-generated data into routine care delivery.

Similarly, Bahrain and Oman have issued telemedicine services frameworks and national digital health roadmaps that mandate EHR interoperability and telemedicine availability at the primary-care level, significantly reducing regulatory and technical barriers for wearable data ingestion into clinical systems.

Private-sector innovation is aligning closely with these policy shifts. For example, OMRON Healthcare collaborates with tele-monitoring services to transmit blood pressure and arrhythmia alerts directly into clinician dashboards for remote cardiac care, while specialized RPM platforms integrate wearable metrics into telehealth systems that flag abnormal trends in real time.

Looking ahead, national investment plans will further accelerate adoption. For instance, Qatar’s National Health Strategy 2024–2030 emphasizes population health management, digitalization, and primary-care strengthening, expanding longitudinal wearable monitoring use cases.

In Kuwait, the 2024/25 healthcare budget of USD 10 billion, including USD 56 million allocated to digital transformation, directly supports telehealth platforms and device integration. Meanwhile, Oman’s 2025 National Health Policy similarly prioritizes digital transformation and telehealth expansion to enable interoperable care delivery.

Exceptionally high chronic disease prevalence, combined with government-led telehealth integration and sustained digital health investments, is structurally transforming wearables into essential clinical tools. These dynamics will continue to drive robust growth of the GCC wearable health devices market over the coming decade.

GCC Wearable Health Devices Market Recent Developments:

- December 2025: Apple has rolled out its hypertension notification feature on Apple Watch devices in the United Arab Emirates and Saudi Arabia, enabling users to receive alerts if patterns suggest chronic high blood pressure. The feature runs on compatible models (Series 9 and later; Ultra 2 and later) with watchOS 26 and reflects Apple’s ongoing health services expansion.

- May 2025: WHOOP has introduced its next-generation health wearables, WHOOP 5.0 and WHOOP MG, featuring advanced health monitoring including ECG, blood pressure insights, extended 14+-day battery life, and healthspan metrics. These devices mark a strategic push into medical-grade wearable health tech and are now available in key Gulf markets, including the UAE and Qatar.

GCC Wearable Health Devices Market Scope:

| Category | Segments |

|---|---|

| By Product Type | Diagnostic & Monitoring Devices, Vital Sign Monitoring Devices, Heart Rate Monitors, Blood Pressure Monitors, Pulse Oximeters, Activity Monitors, Spirometers, Multiparameter trackers, Others, Sleep Monitoring Devices, Sleep Trackers, Wrist Actigraphs, Polysomnographs, Others, Electrocardiographs & Fetal/Obstetric Devices, Neuromonitoring Devices, Electroencephalographs, Electromyographs, Others, Continuous Glucose Monitoring (CGM) Devices, Therapeutic Devices, Pain Management Devices, Neurostimulation Devices, Others, Insulin/Glucose Management Devices, Insulin Pumps, Others, Rehabilitation Devices, Accelerometers & Sensors, Ultrasound Platform, Others, Respiratory Therapy Devices, Ventilators, Positive Airway Pressure (PAP) Devices, Portable Oxygen Concentrators, Others), |

| By Device Type | Smartwatches, Trackers, Smart Clothing, Wearable Patches / Skin Sensors, Headband, Handheld, Shoe Sensors, Strap / Clip / Bracelet, Wrist Bands, Others), |

| By Grade | Consumer-Grade Wearable Devices, Clinical-Grade Wearable Devices), |

| By Application | General Health & Fitness, Remote Patient Monitoring (RPM), Home Healthcare / Self-Care, Sports and Fitness), |

| By Distribution Channel | Online Channels, Pharmacies & Retail Pharmacies, Hypermarkets & Specialty Stores), and others |

GCC Wearable Health Devices Market Drivers:

Rising Burden of Chronic Diseases

The Gulf Cooperation Council (GCC) countries are experiencing a persistently high and growing burden of non-communicable diseases, which is emerging as a critical driver for the adoption of wearable health devices.

Official data from Qatar’s STEPwise Survey indicate that 18.1% of the adult population is affected by diabetes, while 33.4% is classified as obese, reflecting widespread cardiometabolic risk and the need for continuous health monitoring beyond episodic clinical visits.

In Kuwait, findings from the Nutrition Surveillance Program reveal that approximately 73.28% of adults are overweight or obese, significantly increasing susceptibility to hypertension, type 2 diabetes, and cardiovascular disease.

Meanwhile, data from Oman’s Ministry of Health further highlight the scale of the challenge, with around 80% of total deaths attributed to NCDs, and cardiovascular diseases accounting for 36% of overall mortality. These figures demonstrate the clinical imperative for early detection and long-term monitoring solutions that can operate outside hospital settings.

Additionally, community-level screening programs in Saudi Arabia reported 32% obesity prevalence, 31% hypertension, and 12–14% diabetes among screened adults, indicating substantial under-diagnosis. Wearable health devices offer scalable, continuous monitoring capabilities that can improve early identification and chronic disease management.

The high prevalence of chronic conditions across GCC countries is driving demand for wearable health devices, as healthcare systems increasingly prioritise early detection and continuous, preventive care models.

GCC Wearable Health Devices Market Trends:

Integration of Telehealth Ecosystems

GCC governments are systematically embedding telehealth and remote patient monitoring (RPM) into national healthcare delivery models, positioning wearable health devices as critical data inputs for clinical decision-making.

In the United Arab Emirates, Abu Dhabi’s Department of Health has issued formal Telehealth Service (Jawda) guidance, effective from Q1-2025, introducing structured telehealth performance indicators and quality benchmarks for remote monitoring. This framework institutionalizes telehealth delivery and creates clear procurement and compliance pathways for device-linked RPM solutions within regulated care settings.

Similarly, Qatar’s Ministry of Public Health approved comprehensive telemedicine regulations under DHP Circular No. DHP/2024/04, which explicitly recognize remote patient monitoring as an authorized telemedicine modality. The regulation mandates governance, data security, and provider accountability at the facility level, enabling wearable-generated health data to be formally used within licensed telehealth services.

Technology companies are actively leveraging these regulatory developments. For instance, WHOOP combines advanced performance and health analytics with remote expert guidance through its app, while digital health providers bundle wearables with clinician or nurse consultations, transforming device data into structured, guided care services.

Formal telehealth regulations across the GCC are integrating wearables into clinical workflows, and as companies align with these frameworks, wearable health device adoption and market growth will accelerate significantly.

GCC Wearable Health Devices Market Challenges:

Regulatory and Clinical Validation Barriers

Regulatory and clinical validation requirements across GCC countries present a significant challenge for the wearable health devices market, particularly for products positioned with medical-grade claims. GCC health authorities enforce country-specific medical device approvals; for example, Saudi Arabia’s SFDA requires formal classification and conformity assessment for medical wearables, often supported by clinical evidence aligned with intended use.

In the UAE, the Ministry of Health and Prevention (MOHAP) mandates medical device registration with local representation, typically requiring around 45 working days for review, while Qatar’s DataFlow primary-source verification, effective October 2023, adds further administrative steps and approval delays.

Moreover, as wearables add AI diagnostics, ECG and arrhythmia detection, regulators now require stronger clinical validation, algorithm transparency and post-market surveillance, increasing compliance costs, extending approval timelines, and often necessitating local clinical studies or partnerships.

Fragmented regulatory frameworks and rising clinical validation standards increase time-to-market and operational costs for wearable manufacturers. Without streamlined approvals, these barriers are likely to slow innovation diffusion and moderate near-term market growth across the GCC.

GCC Wearable Health Devices Market (2026-32) Segmentation Analysis:

The GCC Wearable Health Devices Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Product Type

- Diagnostic & Monitoring Devices

- Vital Sign Monitoring Devices

- Heart Rate Monitors

- Blood Pressure Monitors

- Pulse Oximeters

- Activity Monitors

- Spirometers

- Multiparameter trackers

- Others

- Sleep Monitoring Devices

- Sleep Trackers

- Wrist Actigraphs

- Polysomnographs

- Others

- Electrocardiographs & Fetal/Obstetric Devices

- Neuromonitoring Devices

- Electroencephalographs

- Electromyographs

- Others

- Continuous Glucose Monitoring (CGM) Devices

- Vital Sign Monitoring Devices

- Therapeutic Devices

- Pain Management Devices

- Neurostimulation Devices

- Others

- Insulin/Glucose Management Devices

- Insulin Pumps

- Others

- Rehabilitation Devices

- Accelerometers & Sensors

- Ultrasound Platform

- Others

- Respiratory Therapy Devices

- Ventilators

- Positive Airway Pressure (PAP) Devices

- Portable Oxygen Concentrators

- Others

- Pain Management Devices

The diagnostic & monitoring devices segment holds the top spot in the GCC Wearable Health Devices Market Share, with 44% market share, due to their broad clinical applicability, continuous-use nature, and strong alignment with preventive and remote care models.

This segment benefits from strong adoption of vital sign monitoring devices such as heart rate monitors, blood pressure monitors, pulse oximeters, activity trackers, and multiparameter sensors used for early detection and long-term management of chronic diseases.

During 2024–2025, expanded remote patient monitoring and telehealth programs, particularly in the GCC, have prioritized ECG-enabled wearables, CGM devices, and sleep monitoring solutions to support outpatient, home-based, and post-acute care.

Additionally, diagnostic wearables face relatively lower adoption barriers compared to therapeutic devices, as they are used for monitoring rather than direct intervention, enabling faster integration into clinical workflows and consumer health platforms. Their compatibility with smartphones, electronic health records, and telemedicine systems reinforces repeat usage and large-scale deployment.

Overall, the combination of high disease prevalence, preventive healthcare emphasis, and expanding RPM infrastructure continues to position diagnostic & monitoring devices as the dominant product category within the wearable health devices market.

Based on Device Type

- Smartwatches

- Trackers

- Smart Clothing

- Wearable Patches / Skin Sensors

- Headband

- Handheld

- Shoe Sensors

- Strap / Clip / Bracelet

- Wrist Bands

- Others

The smartwatches category leads the GCC Wearable Health Devices Industry, with 42% market share, due to their multifunctionality, continuous usage, and strong consumer acceptance. These devices integrate multiple health monitoring features such as heart rate tracking, ECG, blood oxygen levels, sleep analysis, activity monitoring, and fall detection within a single, user-friendly platform. Their ability to support both lifestyle and medical-grade applications positions smartwatches as the preferred choice for daily health tracking.

During 2024–2025, increased integration of smartwatches with telehealth platforms and electronic health records has strengthened their role in remote patient monitoring programs, particularly for chronic disease management and preventive care.

Major smartwatch ecosystems enable seamless data sharing with healthcare providers, supporting outpatient monitoring and virtual consultations. Additionally, strong battery performance, regular software upgrades, and compatibility with smartphones have encouraged repeat usage and long-term adoption.

Smartwatches continue to dominate the GCC wearable health devices market by combining advanced health monitoring capabilities with seamless digital health integration. Their expanding role in telehealth and remote patient monitoring will sustain strong adoption and reinforce market leadership in the coming years.

GCC Wearable Health Devices Market (2026-32): Regional Projection

The GCC Wearable Health Devices Market is dominated by Saudi Arabia, which holds a commanding 37% market share, due to the scale of its population, high prevalence of chronic diseases, and strong government-led digital health initiatives. The Kingdom faces elevated rates of diabetes, obesity, and cardiovascular conditions, driving demand for continuous health monitoring and preventive care solutions.

Under Vision 2030, Saudi Arabia’s Health Sector Transformation Program prioritizes digital health adoption, remote patient monitoring, and outpatient care, accelerating the integration of wearable devices into clinical workflows.

Expanding telehealth services, national health platforms, and increased private-sector participation have further strengthened market penetration. Additionally, high smartphone penetration and growing health awareness among consumers support strong adoption of smartwatches and monitoring devices.

The presence of major technology providers, rising investments in digital healthcare infrastructure, and supportive regulatory frameworks continue to position Saudi Arabia as the largest and most mature wearable health devices market within the GCC region.

Gain a Competitive Edge with Our GCC Wearable Health Devices Market Report

- GCC Wearable Health Devices Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Wearable Health Devices Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Market Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Wearable Health Devices Market Trends & Development

- GCC Wearable Health Devices Market Dynamics

- Growth Drivers

- Challenges

- GCC Wearable Health Devices Market Regulations, Policies & Standards

- GCC Wearable Health Devices Market Import & Export Analysis

- GCC Wearable Health Devices Market Supply Chain Analysis

- GCC Wearable Health Devices Market Hotspots & Opportunities

- GCC Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- Diagnostic & Monitoring Devices

- Vital Sign Monitoring Devices

- Heart Rate Monitors

- Blood Pressure Monitors

- Pulse Oximeters

- Activity Monitors

- Spirometers

- Multiparameter trackers

- Others

- Sleep Monitoring Devices

- Sleep Trackers

- Wrist Actigraphs

- Polysomnographs

- Others

- Electrocardiographs & Fetal/Obstetric Devices

- Neuromonitoring Devices

- Electroencephalographs

- Electromyographs

- Others

- Continuous Glucose Monitoring (CGM) Devices

- Vital Sign Monitoring Devices

- Therapeutic Devices

- Pain Management Devices

- Neurostimulation Devices

- Others

- Insulin/Glucose Management Devices

- Insulin Pumps

- Others

- Rehabilitation Devices

- Accelerometers & Sensors

- Ultrasound Platform

- Others

- Respiratory Therapy Devices

- Ventilators

- Positive Airway Pressure (PAP) Devices

- Portable Oxygen Concentrators

- Others

- Pain Management Devices

- Diagnostic & Monitoring Devices

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- Smartwatches

- Trackers

- Smart Clothing

- Wearable Patches / Skin Sensors

- Headband

- Handheld

- Shoe Sensors

- Strap / Clip / Bracelet

- Wrist Bands

- Others

- By Grade - Market Size & Forecast 2022-2032, USD Million

- Consumer-Grade Wearable Devices

- Clinical-Grade Wearable Devices

- By Application - Market Size & Forecast 2022-2032, USD Million

- General Health & Fitness

- Remote Patient Monitoring (RPM)

- Home Healthcare / Self-Care

- Sports and Fitness

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Online Channels

- Pharmacies & Retail Pharmacies

- Hypermarkets & Specialty Stores

- By Country

- The UAE

- Saudi Arabia

- Qatar

- Kuwait

- Oman

- Bahrain

- By Company

- Competition Characteristics

- Market Share of Leading Companies

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- The UAE Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- By Grade - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Saudi Arabia Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- By Grade - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Qatar Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- By Grade - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Kuwait Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- By Grade - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Oman Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- By Grade - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Bahrain Wearable Health Devices Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type - Market Size & Forecast 2022-2032, USD Million

- By Device Type - Market Size & Forecast 2022-2032, USD Million

- By Grade - Market Size & Forecast 2022-2032, USD Million

- By Application - Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel - Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- GCC Wearable Health Devices Market Key Strategic Imperatives for Growth & Success

- Competition Outlook

- Company Profiles

- Medtronic

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Dexcom

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Fitbit, Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Omron Healthcare, Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Polar Electro

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Garmin Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Samsung Electronics Co., Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Koninklijke Philips N.V.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Sotera Digital Health

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Medtronic

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now