US Weapon Telemetry & Usage Analytics Market Research Report: Growth Drivers & Forecast (2026-2032)

By Component (Hardware (Transmitters and Sensors, Antennas and Modulators), Software (Data analytics platforms, AI/ML predictive analytics software, Visualization & dashboards, Dig ... ital twin & simulation software, Cybersecurity & data protection software)), By Deployment Model (On-Premise, Cloud-Based, Hybrid), By Weapon Platform (Small Arms & Light Weapons, Heavy Weapons & Ground Systems, Missile & Precision-Guided Munitions, Airborne Weapons, Naval Weapon Systems), By Connectivity Technology (Radio Frequency (RF) Telemetry (Dominant), Satellite Communication (SATCOM), Secure IP / Tactical Network Telemetry), By Application (Training & Simulation Analytics, Operational Weapon Monitoring, Predictive Maintenance & Lifecycle Management, Incident Reconstruction & Forensics, Safety, Compliance & Armory Management), By End User (Military & Defense, Federal Law Enforcement & Homeland Security, State & Local Law Enforcement, Defense Contractors & Test Ranges, Commercial Security & Civilian Training) Read more

- Aerospace & Defense

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

US Weapon Telemetry & Usage Analytics Market

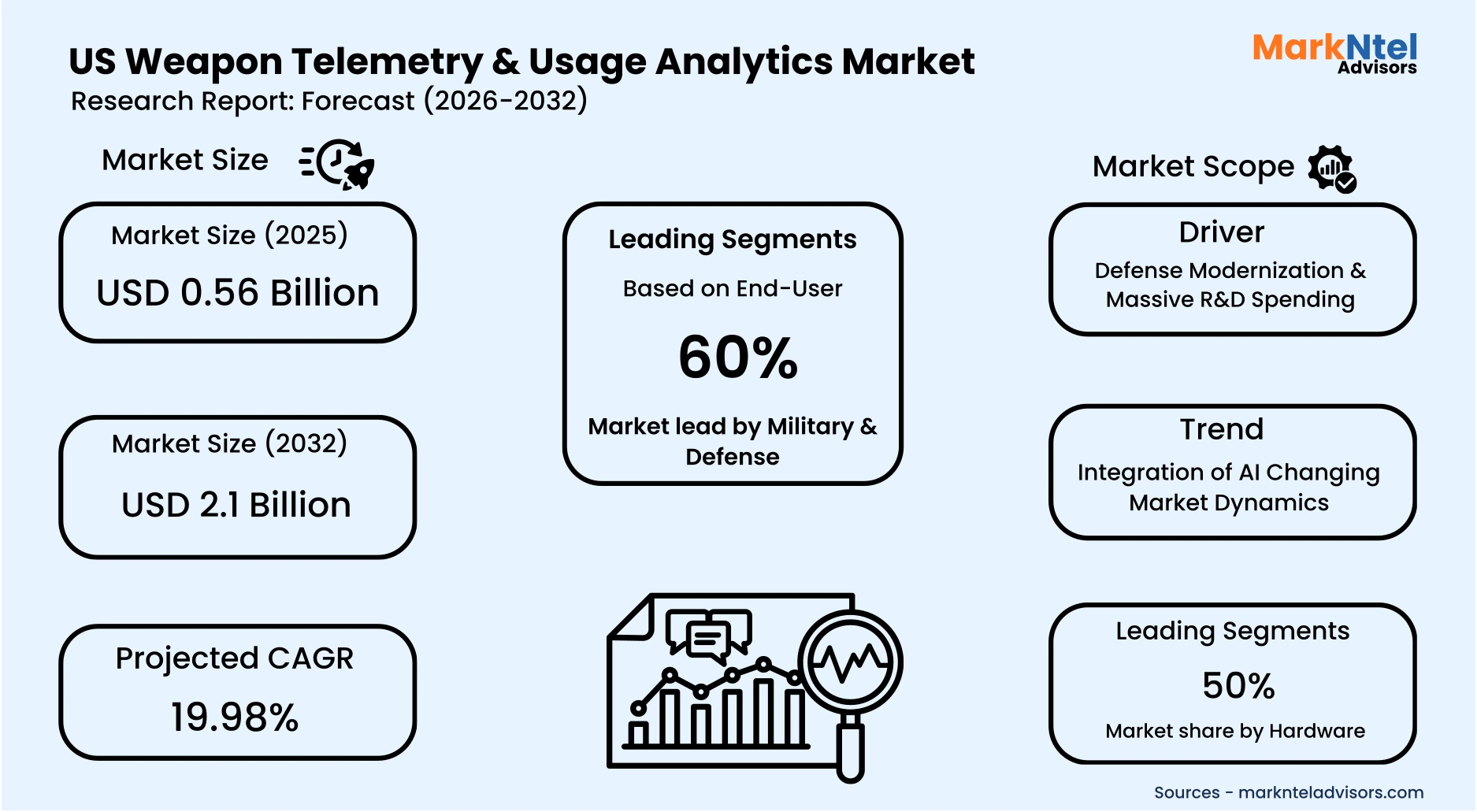

Projected 19.98% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 0.56 Billion

Market Size (2032)

USD 2.1 Billion

Base Year

2025

Projected CAGR

19.98%

Leading Segments

By End User: Military & Defense

US Weapon Telemetry & Usage Analytics Market Report Key Takeaways:

- Market size was valued at around USD 0.56 billion in 2025 and is projected to reach USD 2.1 billion by 2032. The estimated CAGR from 2026 to 2032 is around 19.98%, indicating strong growth.

- By component, the hardware segment represented a significant share of about 50% in the US Weapon Telemetry & Usage Analytics Market in 2025.

- By end user, the military & defense segment presented a significant share of about 60% in the US Weapon Telemetry & Usage Analytics Market in 2025.

- Leading weapon telemetry & usage analytics companies in the US Market are L3Harris Technologies, Inc., Lockheed Martin Corporation, BAE Systems plc, RTX Corporation, General Dynamics Corporation, Northrop Grumman Corporation, Honeywell International Inc., Curtiss-Wright Corporation, Kratos Defense & Security Solutions, Inc., Teledyne Technologies Incorporated, Viasat, Inc., Safran S.A., The Boeing Company, AeroVironment, Inc., Palantir Technologies Inc., and Others.

Market Insights & Analysis: US Weapon Telemetry & Usage Analytics Market (2026-32):

The US Weapon Telemetry & Usage Analytics Market size was valued at around USD 0.56 billion in 2025 and is projected to reach USD 2.1 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 19.98% during the forecast period, i.e., 2026-32.

The US Weapon Telemetry & Usage Analytics Market is projected to expand steadily, driven by rising defense modernization investments and the increasing adoption of AI-powered telemetry and advanced usage analytics across military systems.

The growing complexity of next-generation weapons, combined with the need for real-time performance monitoring and mission analytics, is making telemetry infrastructure an essential component of U.S. defense capability development.

A major growth driver is the scale of defense spending directed toward research, procurement, and strategic deterrence. The FY2025 U.S. defense budget request totals USD 849.8 billion, underscoring the nation’s commitment to maintaining a technologically superior and combat-ready force.

Within this budget, USD 143.2 billion is allocated to Research, Development, Test & Evaluation (RDT&E) and USD 167.5 billion to procurement, demonstrating strong support for the development and deployment of advanced weapons and testing ecosystems.

Meanwhile, modernization funding spans multiple domains, including USD 61.2 billion for airpower, USD 48.1 billion for seapower, and USD 13 billion for land forces, all of which depend heavily on telemetry data for system validation, reliability assessment, and mission readiness.

Strategic deterrence initiatives further reinforce the need for sophisticated telemetry solutions. The budget allocates USD 49.2 billion to nuclear triad modernization, including funding for the Columbia-class ballistic missile submarine (USD 9.9 billion), the B-21 Raider bomber (USD 5.3 billion), and the Sentinel intercontinental ballistic missile program (USD 3.7 billion).

In addition, USD 33.7 billion is dedicated to space capabilities and USD 28.4 billion to missile defense programs, reflecting the expanding importance of space-based tracking, real-time performance evaluation, and data-driven command systems. These initiatives significantly increase the volume of telemetry generated across testing, training, and operational missions.

Artificial intelligence is emerging as a transformative force in defense analytics. AI-driven telemetry enables automated data fusion, predictive insights, and faster operational decision-making. For example, Anduril’s Lattice platform integrates sensor, autonomous system, and surveillance data into a unified command-and-control environment, using AI to deliver real-time situational awareness for military and homeland security operations. This shift toward AI-enabled data fusion is accelerating demand for scalable telemetry pipelines and advanced analytics platforms.

Looking beyond 2025, congressional projections indicate continued expansion in defense innovation funding, with proposals targeting approximately USD 149.7 billion in DoD RDT&E funding for 2026. Th is long-term commitment to experimentation, digital engineering, and advanced weapons development will further increase reliance on telemetry and analytics infrastructure.

Sustained defense modernization, nuclear and space investments, and rapid AI adoption are establishing a data-centric military environment. These structural shifts will drive long-term demand for telemetry and usage analytics, positioning the market for continued growth in the coming decade.

US Weapon Telemetry & Usage Analytics Market Recent Developments:

- 2025: Lockheed Martin partnered with Q-CTRL to develop next-generation quantum sensors for navigation under DARPA’s Robust Quantum Sensors program. The initiative includes contracts valued at about USD 24.4 million, supporting quantum-enabled navigation resilient to GPS jamming and spoofing for advanced defense platforms.

- 2025: L3Harris Technologies secured a U.S. government contract to develop a next-generation security processor designed to protect global communication devices and strengthen secure, resilient communications infrastructure for defense systems against evolving cyber threats.

US Weapon Telemetry & Usage Analytics Market Scope:

| Category | Segments |

|---|---|

| By Component | (Hardware (Transmitters and Sensors, Antennas and Modulators), Software (Data analytics platforms, AI/ML predictive analytics software, Visualization & dashboards, Digital twin & simulation software, Cybersecurity & data protection software)), |

| By Deployment Model | (On-Premise, Cloud-Based, Hybrid), |

| By Weapon Platform | (Small Arms & Light Weapons, Heavy Weapons & Ground Systems, Missile & Precision-Guided Munitions, Airborne Weapons, Naval Weapon Systems), |

| By Connectivity Technology | (Radio Frequency (RF) Telemetry (Dominant), Satellite Communication (SATCOM), Secure IP / Tactical Network Telemetry), |

| By Application | (Training & Simulation Analytics, Operational Weapon Monitoring, Predictive Maintenance & Lifecycle Management, Incident Reconstruction & Forensics, Safety, Compliance & Armory Management), |

| By End User | (Military & Defense, Federal Law Enforcement & Homeland Security, State & Local Law Enforcement, Defense Contractors & Test Ranges, Commercial Security & Civilian Training) |

US Weapon Telemetry & Usage Analytics Market Driver:

Defense Modernization & Massive R&D Spending

The United States’2024 defense budget demonstrates a historic expansion in modernization and research spending, creating strong demand for advanced weapon telemetry and usage analytics across testing, deployment, and lifecycle management.

The U.S. Department of Defense requested USD 842 billion, an increase of USD 26 billion over 2023, to support the National Defense Strategy and strengthen technological superiority against peer adversaries .

A central component of the request includes USD 145 billion for Research, Development, Test and Evaluation (RDT&E) and USD 170 billion for procurement, the largest allocations ever recorded. These investments accelerate development cycles and expand the need for high-precision telemetry, real-time performance monitoring, and data-driven validation across next-generation weapon systems.

Missile and precision-strike modernization represent a key growth catalyst. The budget allocates USD 29.8 billion for missile defense and defense-supporting programs such as the Next Generation Interceptor, hypersonic weapon development, and new low-Earth-orbit missile-warning architectures. Such programs depend on high-fidelity telemetry and analytics to evaluate flight performance, reliability, and mission readiness.

Additionally, USD 11 billion is dedicated to highly lethal precision weapons, including the procurement of 24 hypersonic missiles and long-range strike capabilities, further increasing demand for advanced testing and operational data capture .

Sustained record-level defense investment is significantly increasing the volume, complexity, and strategic importance of weapons testing and performance data, positioning telemetry and usage analytics as a critical enabling technology for future U.S. military capability.

US Weapon Telemetry & Usage Analytics Market Trend:

Integration of AI Changing Market Dynamics

Artificial intelligence is becoming a core enabler of next-generation telemetry and usage analytics across U.S. defense programs, fundamentally changing how performance data is collected, processed, and operationalized.

The Department of Defense allocated USD 1.8 billion for AI in the 2024 defense budget, underscoring the Pentagon’s commitment to expanding AI-driven data analysis, autonomy, and decision-support capabilities across mission systems . This investment reflects the growing need to manage the vast telemetry streams generated by advanced weapons, sensors, and multi-domain platforms.

AI is also central to the Joint All-Domain Command and Control (JADC2) initiative, funded at USD 1.4 billion, which aims to deliver real-time information advantage by connecting data across air, land, sea, space, and cyber domains . AI-enabled analytics can fuse telemetry data from missiles, aircraft, satellites, and ground systems into actionable intelligence, enabling commanders and engineers to make faster, more informed decisions. As modern warfare becomes increasingly data-centric, the ability to transform raw telemetry into real-time operational insight is becoming mission-critical.

Federal technology priorities further emphasize trusted AI and autonomy alongside hypersonics and biotechnology, signaling sustained long-term investment in intelligent defense systems.

The rapid integration of AI into defense data ecosystems is accelerating the evolution of intelligent telemetry platforms, strengthening real-time decision-making and positioning AI-driven analytics as a key growth driver for the U.S. weapon telemetry and usage analytics market.

US Weapon Telemetry & Usage Analytics Market Opportunity:

Digital Twin & Simulation Ecosystems

Digital twin technology and advanced modeling environments are creating a significant growth opportunity for the U.S. Weapon Telemetry & Usage Analytics Market as the Department of Defense accelerates the adoption of digital engineering across weapon development programs. By integrating real-world telemetry into high-fidelity virtual environments, defense organizations can continuously evaluate system performance, reliability, and mission readiness without relying exclusively on expensive live testing.

The Pentagon’s technology investment priorities further reinforce this opportunity through substantial funding for foundational capabilities that rely on simulation ecosystems. Key allocations include USD 1.7 billion for microelectronics, USD 1.2 billion for integrated sensing and cyber, and USD 763 million for networked systems-of-systems. These investments enable advanced modeling frameworks that support large-scale performance validation, mission rehearsal, and failure-scenario testing before physical deployment. Telemetry-fed digital twins allow engineers to analyze system behavior under diverse operational conditions, improving predictive maintenance and enhancing overall system resilience.

Initiatives such as the Rapid Defense Experimentation Reserve (RDER) and the Replicator Initiative are further accelerating the transition toward simulation-driven acquisition. By emphasizing rapid prototyping and faster fielding of emerging technologies, these programs increase reliance on telemetry-supported modeling and virtual testing environments.

As the DoD expands digital engineering and simulation-first acquisition strategies, demand for advanced telemetry and usage analytics will intensify, positioning digital twin ecosystems as a key long-term growth opportunity for the U.S. market.

US Weapon Telemetry & Usage Analytics Market Challenge:

Cybersecurity and Data Interception Risks

Cybersecurity threats targeting U.S. defense networks and the Defense Industrial Base (DIB) present a significant barrier to the adoption and scaling of weapon telemetry and usage analytics. These systems depend on the secure transmission of sensitive real-time data from weapons, test ranges, satellites, and connected sensors, making them highly attractive targets for espionage and disruption.

The U.S. Department of Defense has indicated that its networks encounter millions of cyber events each day, highlighting the persistent and large-scale nature of adversary cyber activity directed at military infrastructure.

In response to escalating threats, the DoD is implementing the Cybersecurity Maturity Model Certification (CMMC) program to strengthen cybersecurity requirements across thousands of contractors that handle controlled defense information.

The Department of Homeland Security has similarly identified aerospace and defense platforms as high-value cyber targets due to their reliance on satellite communications, wireless telemetry links, and networked sensing architectures. Between November 2024 and August 2025, 41 U.S. agencies collaborated on joint cybersecurity advisories led by CISA, the FBI, and the NSA, underscoring the growing urgency of the threat landscape .

Rising cyber risks increase compliance costs, slow data integration, and complicate the secure deployment of telemetry systems. These factors may delay program timelines and restrain broader market expansion.

US Weapon Telemetry & Usage Analytics Market (2026-32) Segmentation Analysis:

The US Weapon Telemetry & Usage Analytics Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Component:

- Hardware

- Transmitters and Sensors

- Antennas and Modulators

- Software

- Data analytics platforms

- AI/ML predictive analytics software

- Visualization & dashboards

- Digital twin & simulation software

- Cybersecurity & data protection software

The hardware segment dominates the US Weapon Telemetry & Usage Analytics market, accounting for around 50% market share, because telemetry capabilities are fundamentally built on specialized physical infrastructure embedded across weapons, platforms, and test environments.

Advanced transmitters, antennas, sensors, and modulators are essential for capturing high-fidelity performance data and transmitting it securely during development, testing, and operational deployment. As a result, software and analytics solutions remain dependent on the availability and continuous modernization of telemetry hardware, positioning this segment as the market’s operational backbone.

Demand for advanced telemetry hardware is further reinforced by the harsh and complex conditions in which modern defense systems operate. Telemetry equipment must function reliably under extreme temperature, pressure, vibration, and electromagnetic interference, requiring highly engineered and costly components that undergo continuous upgrades.

Additionally, the expansion of multi-domain operations across air, land, sea, space, and cyber environments is increasing the need for distributed ground stations, tracking antennas, and secure communication modules across testing ranges and operational theaters.

The rapid advancement of hypersonic weapons, missile defense systems, and space-based platforms is also accelerating the need for high-bandwidth, long-range telemetry solutions capable of real-time monitoring.

As the U.S. military prioritizes mission assurance and real-time performance visibility, sustained investment in telemetry hardware continues to secure the segment’s dominant market position.

Based on End User:

- Military & Defense

- Federal Law Enforcement & Homeland Security

- State & Local Law Enforcement

- Defense Contractors & Test Ranges

- Commercial Security & Civilian Training

The military & defense segment dominates the US Weapon Telemetry & Usage Analytics Market, with a market share of around 60%, due to its critical reliance on continuous testing, validation, and operational performance monitoring of advanced weapon systems.

Modern defense strategy prioritizes data-centric warfare, where real-time telemetry supports mission readiness, reliability assessment, and lifecycle optimization across air, land, maritime, space, and cyber domains. Every stage of the defense acquisition cycle, from research and development to live testing and deployment, requires high-fidelity telemetry to evaluate weapon behavior, safety, and effectiveness in complex operational environments.

The growing adoption of multi-domain operations and integrated command-and-control frameworks further strengthens this segment’s dominance. Programs designed to connect sensors, platforms, and warfighters depend heavily on telemetry streams to deliver real-time situational awareness and enable faster decision-making.

In addition, modernization initiatives involving hypersonic systems, missile defense, autonomous platforms, and next-generation aircraft demand advanced analytics to monitor performance and predict maintenance needs throughout the lifecycle of increasingly software-defined systems.

Large-scale training exercises, simulation-driven mission rehearsal, and continuous readiness assessments generate vast volumes of operational data, increasing reliance on advanced analytics platforms.

As defense systems become more interconnected and technologically complex, the Military & Defense sector will continue to account for the majority of telemetry and usage analytics demand, sustaining its leadership within the U.S. market.

Gain a Competitive Edge with Our US Weapon Telemetry & Usage Analytics Market Report:

- The US Weapon Telemetry & Usage Analytics Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The US Weapon Telemetry & Usage Analytics Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- US Weapon Telemetry & Usage Analytics Market Policies, Regulations, and Product Standards

- US Weapon Telemetry & Usage Analytics Market Trends & Developments

- US Weapon Telemetry & Usage Analytics Market Dynamics

- Growth Factors

- Challenges

- US Weapon Telemetry & Usage Analytics Market Hotspot & Opportunities

- US Weapon Telemetry & Usage Analytics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Component- Market Size & Forecast 2022-2032, USD Million

- Hardware

- Transmitters and Sensors

- Antennas and Modulators

- Software

- Data analytics platforms

- AI/ML predictive analytics software

- Visualization & dashboards

- Digital twin & simulation software

- Cybersecurity & data protection software

- Hardware

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- On-Premise

- Cloud-Based

- Hybrid

- By Weapon Platform- Market Size & Forecast 2022-2032, USD Million

- Small Arms & Light Weapons

- Heavy Weapons & Ground Systems

- Missile & Precision-Guided Munitions

- Airborne Weapons

- Naval Weapon Systems

- By Connectivity Technology- Market Size & Forecast 2022-2032, USD Million

- Radio Frequency (RF) Telemetry (Dominant)

- Satellite Communication (SATCOM)

- Secure IP / Tactical Network Telemetry

- By Application- Market Size & Forecast 2022-2032, USD Million

- Training & Simulation Analytics

- Operational Weapon Monitoring

- Predictive Maintenance & Lifecycle Management

- Incident Reconstruction & Forensics

- Safety, Compliance & Armory Management

- By End User- Market Size & Forecast 2022-2032, USD Million

- Military & Defense

- Federal Law Enforcement & Homeland Security

- State & Local Law Enforcement

- Defense Contractors & Test Ranges

- Commercial Security & Civilian Training

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Small Arms & Light Weapons Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Connectivity Technology- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Heavy Weapons & Ground Systems Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Connectivity Technology- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Missile & Precision-Guided Munitions Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Connectivity Technology- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Airborne Weapons Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Connectivity Technology- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Naval Weapon Systems Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment Model- Market Size & Forecast 2022-2032, USD Million

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Connectivity Technology- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Weapon Telemetry & Usage Analytics Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- L3Harris Technologies, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lockheed Martin Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- RTX Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Dynamics Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Northrop Grumman Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell International Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Curtiss-Wright Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kratos Defense & Security Solutions, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Teledyne Technologies Incorporated

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Viasat, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Safran S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Boeing Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AeroVironment, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Palantir Technologies Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- L3Harris Technologies, Inc.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now