Spain Agribusiness Market Research Report: Trends & Forecast (2026-2032)

By Product (Grains and cereals, Dairy, Oilseeds, Livestock, Others), By Application (Crop Production, Livestock Production, Aquaculture, Agroforestry), By Farming Type (Conventiona ... l Farming, Organic Farming, Precision Farming, Contract Farming, Vertical & Controlled Environment Farming), By Farm Size (Small-Scale Farms, Medium-Scale Farms, Large-Scale Farms), By End-Use Industry (Food & Beverage Industry, Textile Industry (Cotton, Jute), Biofuel Industry, Pharmaceutical Industry, Animal Husbandry & Dairy Industry), and others Read more

- Environment

- Mar 2026

- Pages 150

- Report Format: PDF, Excel, PPT

Spain Agribusiness Market

Projected 2.55% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 57.6 Billion

Market Size (2032)

USD 67.0 Billion

Base Year

2025

Projected CAGR

2.55%

Leading Segments

By End-Use Industry: Food & Beverage Industry

Spain Agribusiness Market Report Key Takeaways:

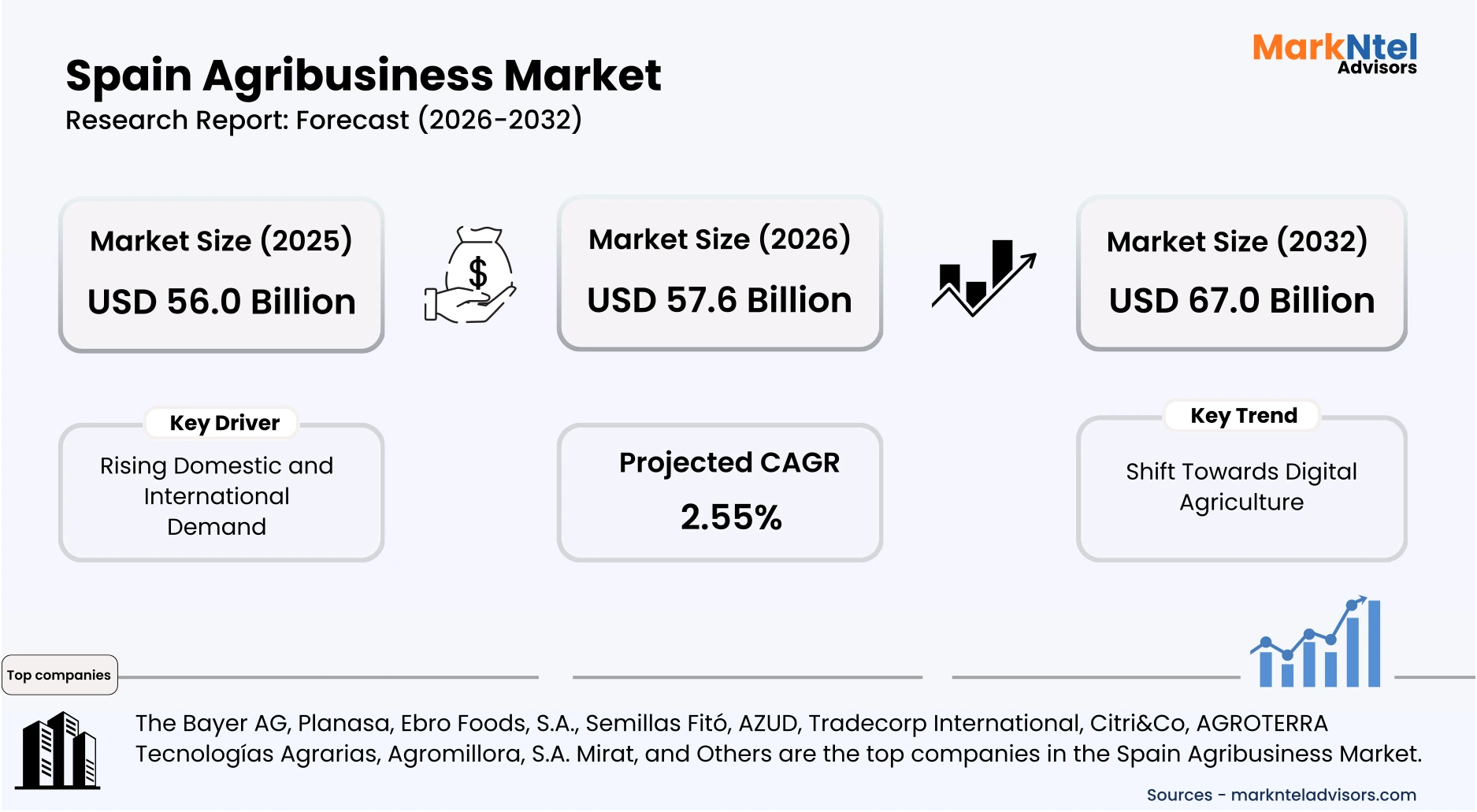

- The Spain Agribusiness Market size was valued at USD 56.0 billion in 2025 and is projected to grow from USD 57.6 billion in 2026 to USD 67.0 billion by 2032, exhibiting a CAGR of 2.55% during the forecast period.

- By product, the Grains and cereals segment represented a significant share of about 25% in the Spain Agribusiness Market in 2026.

- By end-use industry, the Food & beverage industry segment presented a significant share of about 58% in the Spain Agribusiness Market in 2026.

- Leading agribusiness companies in the Global Market are Bayer AG, Planasa, Ebro Foods, S.A., Semillas Fitó, AZUD, Tradecorp International, Citri&Co, AGROTERRA Tecnologías Agrarias, Agromillora, S.A. Mirat, and Others.

Market Insights & Analysis: Spain Agribusiness Market (2026-32):

The Spain Agribusiness Market size was valued at USD 56.0 billion in 2025 and is projected to grow from USD 57.6 billion in 2026 to USD 67.0 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 2.55% during the forecast period, i.e., 2026-32.

Spain’s agribusiness market is poised for sustained expansion, supported by rising domestic consumption and resilient export demand for high-value crops, fruits, vegetables, olive oil, and processed food products. Strong international appetite continues to reinforce production, trade flows, and capital investment across the value chain. In 2024, Catalonia alone generated approximately USD 17.4 billion in agricultural and food exports, marking a 2.6% annual increase and accounting for 21% of Spain’s total agri-food exports. Premium wines, processed foods, and artisanal products led growth, while expanding SME participation and trade diversification strategies are expected to further strengthen export performance through 2025–2026 .

Alongside demand expansion, rapid digital transformation is reshaping the competitive landscape. Precision agriculture, IoT-based monitoring systems, advanced data analytics, and institutionalized digital farm record tools are improving operational efficiency, traceability, and sustainability. The Government of Spain, in partnership with Navarra and La Rioja, launched Europe’s first “Sandbox AgriFoodtech” initiative to test agri-food innovations under real farming conditions, accelerating the deployment of automation and data-driven technologies. Government representatives have emphasized that digital agriculture is now integrated into daily farming activities, with strong public support directed toward cooperatives, farms, and SMEs nationwide.

Future-focused investment further reinforces positive market prospects. In September 2025, the government allocated approximately USD 250 million under the Plan de Recuperación, Transformación y Resiliencia to finance more than 6,700 precision agriculture projects. These initiatives aim to modernize farms with smart sensors, robotics, and integrated data systems, strengthening productivity, sustainability, and global competitiveness.

Overall, strengthening export performance, regional diversification, accelerated digital adoption, and targeted public investment collectively position Spain’s agribusiness market for stable medium-term growth. As technology integration deepens and global demand remains firm, the sector is expected to enhance value creation, resilience, and international market share.

Spain Agribusiness Market Recent Developments:

- 2025: Spain’s pistachio production surged 73.6% in the 2025 season, expanding from 8,200 t in 2018 to 42,400 t. This rapid output growth is creating new opportunities for processing, value‑added products, and export markets .

- 2025: MHP completed its purchase of a 92% stake in Grupo UVESA, a major vertically integrated poultry and pork producer in Spain. This consolidation strengthens production scale and distribution capacity across domestic and export channels .

Spain Agribusiness Market Scope:

| Category | Segments |

|---|---|

| By Product | (Grains and cereals, Dairy, Oilseeds, Livestock, Others), |

| By Application | (Crop Production, Livestock Production, Aquaculture, Agroforestry), |

| By Farming Type | (Conventional Farming, Organic Farming, Precision Farming, Contract Farming, Vertical & Controlled Environment Farming), |

| By Farm Size | (Small-Scale Farms, Medium-Scale Farms, Large-Scale Farms), |

| By End-Use Industry | (Food & Beverage Industry, Textile Industry (Cotton, Jute), Biofuel Industry, Pharmaceutical Industry, Animal Husbandry & Dairy Industry), |

Spain Agribusiness Market Driver:

Rising Domestic and International Demand

Rising domestic and international demand remains a fundamental growth driver for Spain’s agribusiness market. Official government data show that agri-food and fisheries exports reached USD 77.9 billion in 2023, marking a 3% year-on-year increase and accounting for 18.4% of Spain’s total foreign trade. Key export categories included meat, fruits, and vegetables, with meat exports alone valued at USD 11.4 billion, underscoring the sector’s strong global positioning .

Export momentum strengthened further in 2024, when Spain recorded a new high of USD 78 billion. In agri-food exports, reflecting 6.1% annual growth. Fruits, vegetables, meat, and olive oil remained leading contributors, highlighting consistent global demand for Spanish agricultural products .

Spain also maintains global leadership in olive oil exports. During the 2024/25 season, olive oil shipments surpassed 1 million tons, representing a 35% increase in volume compared with the previous year. Notably, export volumes frequently exceed domestic consumption, illustrating the international market’s reliance on Spanish produce .

Overall, sustained domestic consumption combined with expanding export volumes reinforces production growth, investment in value-added processing, and regional expansion, positioning demand as a primary engine of Spain’s agribusiness market development.

Spain Agribusiness Market Trend:

Shift Towards Digital Agriculture

The shift towards digital agriculture is significantly transforming Spain’s agribusiness sector by enhancing operational efficiency, traceability, and data-driven decision-making. Spain has emerged as a European leader in agricultural technology adoption. According to the Informe de Adopción Tecnológica en el Sector Agroalimentario 2025, more than 90% of Spanish farms use digital tools, surpassing the EU average of 78%, reflecting widespread deployment of precision farming systems, sensors, and data management platforms .

The Ministry of Agriculture, Fisheries, and Food has reinforced this transition by supporting over 200 digital innovation initiatives, backed by public investment exceeding USD 54 million. These initiatives promote robotics, artificial intelligence, and advanced monitoring systems aimed at improving farm profitability and environmental sustainability .

Institutional measures such as the implementation of the Cuaderno Digital de Explotación are formalizing digital record-keeping, strengthening compliance, transparency, and farm management efficiency. Precision technologies, including IoT-based soil and water sensors and big data analytics, are enabling producers to optimize input use and increase yields .

A practical example is a 525-hectare farm in Pedraza de Campos, which adopted an Agriculture 4.0 model in 2026 under the Ministry’s Programa CULTIVA, integrating digital harvesters, portable soil laboratories, and variable-rate machinery .

Overall, Spain’s strong policy backing and high adoption rates indicate that digital agriculture will continue driving productivity gains and long-term competitiveness in the agribusiness market.

Spain Agribusiness Market Opportunity:

Development of Agro-Processing and Bioproducts

A major growth opportunity in Spain’s agribusiness market lies in the expansion of agro-processing and bio-based product development, enabling the sector to capture higher value from agricultural output. Official data indicate that Spain’s agri-food sector generated USD 136 billion in added value in 2024, with food processing and marketing activities contributing significantly to national GDP and employment. The food and beverage industry alone comprises nearly 30,000 companies, highlighting the scale of downstream processing capacity within the country .

Building on this foundation, the Spanish Government has continued to strengthen the Agro-Food PERTE (Strategic Project for Economic Recovery and Transformation) in 2025, supporting modernization of processing facilities, energy-efficient production systems, traceability technologies, and circular economy solutions. Public funding under this framework is channeled toward upgrading industrial plants and promoting innovation in packaged foods, functional ingredients, and sustainable biomaterials.

At the same time, bioeconomy initiatives are encouraging the conversion of agricultural and livestock waste into biogas, biofertilizers, and other renewable bio-products, creating additional income streams for rural producers. As processing depth increases, Spain can transition from primarily exporting raw produce to exporting high-margin, value-added agri-food and bio-industrial products, strengthening long-term market expansion and competitiveness.

Spain Agribusiness Market Challenge:

Climate Change & Water Scarcity Hindering Market Growth

Climate change–driven water scarcity remains a structural constraint on Spain’s agribusiness market. Spain experienced prolonged drought conditions that significantly curtailed agricultural production. According to the Banco de España (Economic Bulletin, 2025), water shortages reduced yields of rain-fed cereals such as wheat and barley by 20–30%, while olive production declined by at least 10%, demonstrating the direct sensitivity of core crops to rainfall deficits .

Although rainfall partially recovered in 2024, the after-effects of extended dry spells continued to pressure irrigation systems and farm operations. Producers in southern and eastern regions, including Andalusia and Catalonia, faced constrained reservoir levels, reductions in irrigated hectares, and higher operating costs linked to water management and input adjustments . These structural pressures persisted into 2024–2025, compelling farmers to modify cropping patterns and reassess production strategies under uncertain water availability.

Looking ahead to 2025 and beyond, climate assessments indicate a rising likelihood of more frequent and severe drought episodes, increasing long-term risks for olive oil, cereal, and wine production.

Overall, recurring drought and water stress threaten yield stability, raise production costs, and weaken output reliability, making climate resilience and efficient water management critical for sustaining Spain’s agribusiness growth.

Spain Agribusiness Market (2026-32) Segmentation Analysis:

The Spain Agribusiness Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product:

-

- Grains and cereals

- Dairy

- Oilseeds

- Livestock

- Others

Grains and cereals are the leading product segment in Spain’s agribusiness, accounting for approximately 25% of the market size. The dominance of this segment is largely due to its role as a staple food, both for domestic consumption and export. Spain’s diverse climate supports the cultivation of wheat, barley, maize, and rice, enabling high yields and stable production. Grains serve as the foundation for several value-added products such as flour, bakery items, breakfast cereals, and processed foods.

Moreover, grains are also critical for livestock feed, linking this segment to the broader agro-industrial supply chain. Government support, technological adoption in cultivation, and the growing demand for processed grain-based products in Europe and international markets further reinforce the leadership of this segment. The consistent consumption patterns and adaptability of grains to mechanized farming ensure their continued prominence in Spain’s agricultural portfolio.

Based on End-Use Industry:

- Food & Beverage Industry

- Textile Industry (Cotton, Jute)

- Biofuel Industry

- Pharmaceutical Industry

- Animal Husbandry & Dairy Industry

The Food & Beverage Industry leads the end-use segment, capturing around 58% of Spain’s agribusiness market size. This is primarily because it serves as the primary destination for most agricultural outputs, including grains, fruits, vegetables, dairy, and livestock products. Spain has a strong tradition of food processing, including olive oil, wine, dairy products, and ready-to-eat foods, which fuels demand for raw agricultural inputs. The industry benefits from domestic consumption, growing tourism, and export opportunities across Europe and beyond. The rise of value-added products, processed foods, and ready-to-cook offerings has further expanded market demand.

Additionally, the adoption of modern processing technologies, strict quality standards, and a focus on healthy and organic food products strengthen the position of the Food & Beverage Industry as the dominant end-use sector, making it central to Spain’s agribusiness growth.

Spain Agribusiness Market (2026-32): Regional Projection

The Spain agribusiness market is dominated by Andalusia, the country’s primary agricultural hub. In 2024, Andalusia contributed over 30% of Spain’s total agrarian output, maintaining leadership in olive oil, fruits, vegetables, and industrial crops. The region plays a central role in supporting Spain’s USD 79.4 billion agro-food export value, driven by strong international demand for Mediterranean products. Provinces such as Jaén and Almería are globally recognized for large-scale olive cultivation and advanced greenhouse horticulture, respectively, enhancing both productivity and export competitiveness.

Andalusia benefits from extensive irrigated farmland, established agro-processing industries, and strong cooperative networks that integrate production with packaging and global distribution. Continued investments in modern irrigation systems, cold-chain logistics, and export facilitation programs are expected to further strengthen the region’s production efficiency and international market access. The concentration of high-output farming, processing infrastructure, and export-oriented enterprises firmly positions Andalusia as the leading contributor to Spain’s agribusiness market growth.

Gain a Competitive Edge with Our Spain Agribusiness Market Report:

- Spain Agribusiness Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Spain Agribusiness Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Spain Agribusiness Market Policies, Regulations, and Product Standards

- Spain Agribusiness Market Trends & Developments

- Spain Agribusiness Market Dynamics

- Growth Factors

- Challenges

- Spain Agribusiness Market Hotspot & Opportunities

- Spain Agribusiness Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Product - Market Size & Forecast 2022-2032, USD Million

- Grains and cereals

- Dairy

- Oilseeds

- Livestock

- Others

- By Application- Market Size & Forecast 2022-2032, USD Million

- Crop Production

- Livestock Production

- Aquaculture

- Agroforestry

- By Farming Type- Market Size & Forecast 2022-2032, USD Million

- Conventional Farming

- Organic Farming

- Precision Farming

- Contract Farming

- Vertical & Controlled Environment Farming

- By Farm Size- Market Size & Forecast 2022-2032, USD Million

- Small-Scale Farms

- Medium-Scale Farms

- Large-Scale Farms

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Food & Beverage Industry

- Textile Industry (Cotton, Jute)

- Biofuel Industry

- Pharmaceutical Industry

- Animal Husbandry & Dairy Industry

- By Region- Market Size & Forecast 2022-2032, USD Million

- Andalusia

- Catalonia

- Madrid

- Valencia

- Galicia

- Castile and León

- Basque Country

- Canary Islands

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Grains and Cereals Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Farming Type- Market Size & Forecast 2022-2032, USD Million

- By Farm Size- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Dairy Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Farming Type- Market Size & Forecast 2022-2032, USD Million

- By Farm Size- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Oilseeds Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Farming Type- Market Size & Forecast 2022-2032, USD Million

- By Farm Size- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Livestock Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Application- Market Size & Forecast 2022-2032, USD Million

- By Farming Type- Market Size & Forecast 2022-2032, USD Million

- By Farm Size- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Agribusiness Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Bayer AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Planasa

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ebro Foods, S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Semillas Fitó

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AZUD

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tradecorp International

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Citri&Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AGROTERRA Tecnologías Agrarias

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agromillora

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- S.A. Mirat

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bayer AG

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now