Saudi Arabia Healthcare Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Healthcare Expenditure Type (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), By Pharmaceutical Segment (Prescription Drugs, Over-the-C ... ounter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), By Therapeutic Area (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), By Medical Device Type (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), By Technology Type (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), By Healthcare Workforce (Physicians, Nurses, Dentists, Allied Health Professionals), By Insurance Type (Public Health Insurance, Private Health Insurance), By Disease Category (Chronic Diseases, Infectious Diseases, Mental Health Disorders), By End User (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) Read more

- Healthcare

- Mar 2026

- Pages 125

- Report Format: PDF, Excel, PPT

Saudi Arabia Healthcare Market

Projected 9.35% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 152 Billion

Market Size (2032)

USD 259 Billion

Base Year

2025

Projected CAGR

9.35%

Leading Segments

By Therapeutic Area: Diabetes

Saudi Arabia Healthcare Market Report Key Takeaways:

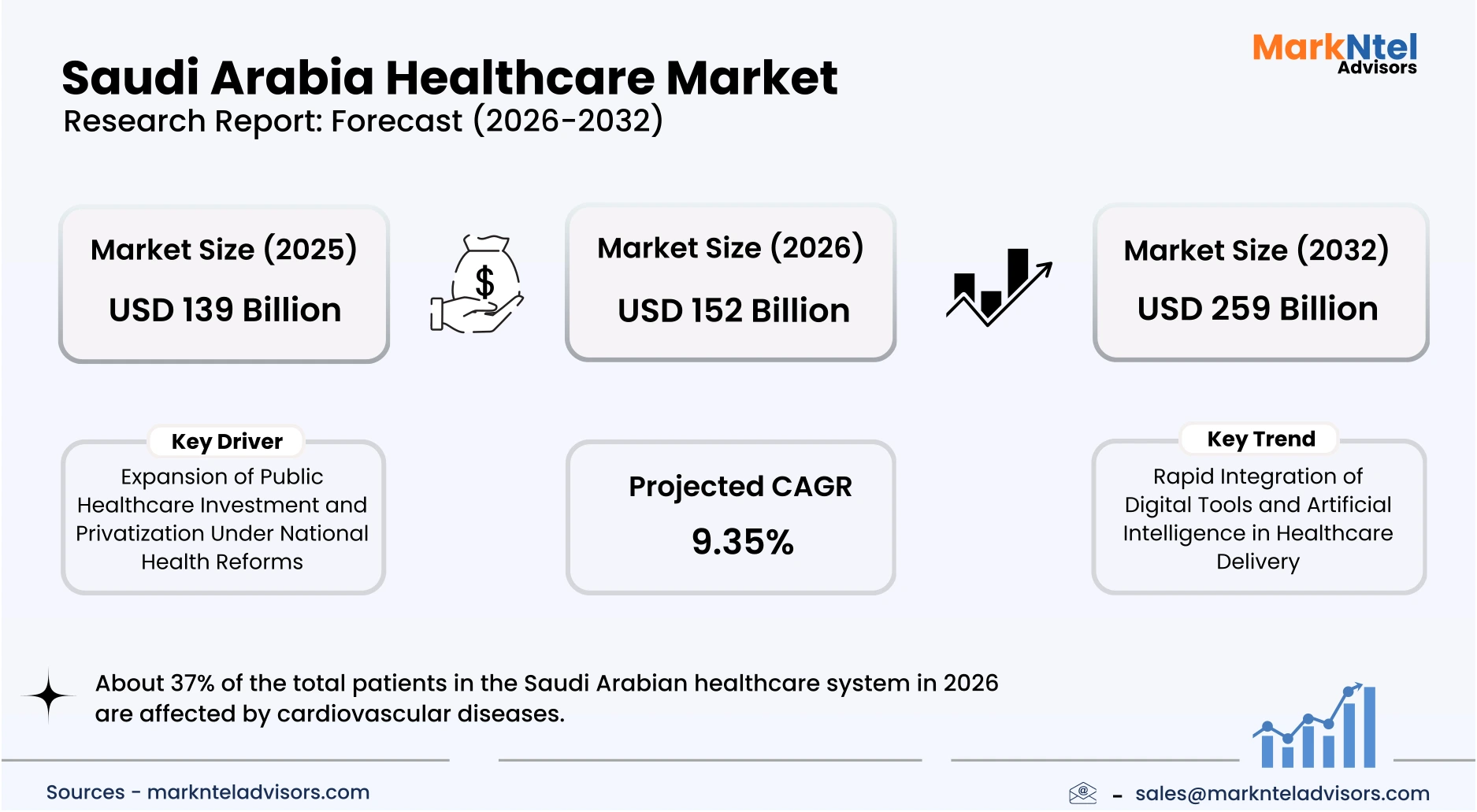

- The Saudi Arabian Healthcare Market size was valued at USD 139 billion in 2025 and is projected to grow from USD 152 billion in 2026 to USD 259 billion by 2032, exhibiting a CAGR of 9.35% during the forecast period.

- About 37% of the total patients in the Saudi Arabian healthcare system in 2026 are affected by cardiovascular diseases,

- Diabetes is another prevalent disease that affects around 23.1% of the population in the Saudi Arabian Healthcare Sector in 2026.

- Saudi Arabia’s healthcare system comprises 516 hospitals, has an average of 23.4 beds per 10,000 people, and is supported by 129,772 physicians and 243,336 nurses nationwide, underscoring the nation’s extensive healthcare infrastructure.

Market Insights & Analysis: Saudi Arabia Healthcare Market (2026-32):

The Saudi Arabia Healthcare Market size was valued at USD 139 billion in 2025 and is projected to grow from USD 152 billion in 2026 to USD 259 billion by 2032, exhibiting a CAGR of 9.35% during the forecast period. i.e., 2026-32.

Saudi Arabia’s healthcare sector has experienced sustained expansion over the past decade, supported by structural reforms, rising population needs, and strong public investment. According to the Saudi General Authority for Statistics, the Kingdom had about 516 hospitals and more than 5,700 primary healthcare centers by 2024, reflecting a steady expansion in healthcare delivery infrastructure. The system also supported approximately 23.4 hospital beds per 10,000 population and over 129,772 physicians, indicating growing clinical capacity across institutional end-users such as hospitals, specialty centers, and government medical complexes. This expansion has strengthened patient access to healthcare services while enabling improved treatment outcomes across urban and regional healthcare networks.

Disease epidemiology is also shaping healthcare demand, with chronic conditions and genetic disorders emerging as key areas of medical focus. Cardiovascular diseases, diabetes, obesity-related complications, and hereditary conditions such as sickle cell disease and thalassemia, which are relatively prevalent due to high rates of consanguineous marriages, continue to drive patient volumes in specialized treatment centers. 331,151 million newborns through early genetic screening programs, improving early diagnosis and long-term treatment planning. These initiatives are expanding demand for advanced diagnostics, genomic medicine, and specialized institutional healthcare services across the country.

Healthcare infrastructure modernization under the Health Sector Transformation Program (HSTP), a central pillar of the national development strategy, has accelerated technology adoption across hospitals and medical institutions. The program promotes integrated care models, digital health systems, and artificial intelligence–enabled diagnostic tools to improve clinical decision-making and patient management. Investments exceeding USD 8.4 billion in new hospital projects and infrastructure developments have been announced through public-private partnerships involving domestic and international hospital operators. Such initiatives encourage capacity expansion, medical technology deployment, and improved service delivery within institutional healthcare facilities.

Looking ahead, Saudi Arabia aims to establish itself as a regional hub for biotechnology, pharmaceutical manufacturing, and advanced medical research. National strategies emphasize building domestic pharmaceutical and biotechnology clusters while strengthening research capabilities in genomics, AI-driven healthcare analytics, and precision medicine. The country is also adapting its healthcare services to demographic shifts, including population growth and gradual ageing, which will increase demand for long-term care and specialized clinical services. Collectively, these policy frameworks, technological investments, and infrastructure expansion plans are expected to sustain strong growth in the Saudi Arabian Healthcare Sector M arket through 2032.

Saudi Arabia Healthcare Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Expenditure Type | (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), |

| By Pharmaceutical Segment | (Prescription Drugs, Over-the-Counter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), |

| By Therapeutic Area | (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), |

| By Medical Device Type | (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), |

| By Technology Type | (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), |

| By Healthcare Workforce | (Physicians, Nurses, Dentists, Allied Health Professionals), |

| By Insurance Type | (Public Health Insurance, Private Health Insurance), |

| By Disease Category | (Chronic Diseases, Infectious Diseases, Mental Health Disorders), |

| By End User | (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) |

Saudi Arabia Healthcare Market Driver:

Expansion of Public Healthcare Investment and Privatization Under National Health Reforms

Saudi Arabia’s healthcare sector is being strongly driven by large-scale public investment and structural reforms aimed at expanding healthcare capacity and improving service accessibility. Under the national Health Sector Transformation Program, healthcare spending has increased substantially to modernize hospitals, develop specialized treatment centers, and expand digital health systems. Saudi Arabia allocated around USD 69 billion to the health and social development sector in the 2025 budget, representing one of the largest public expenditures among government sectors. This sustained fiscal commitment has enabled the expansion of hospitals, procurement of advanced medical equipment, and increased service delivery capacity across institutional healthcare facilities nationwide.

The reform program has also intensified private sector participation through privatization initiatives and public-private partnerships that expand healthcare infrastructure and service provision. According to the Saudi Ministry of Investment, the Kingdom aims to increase private sector participation in healthcare delivery to around 35% of total sector spending by 2030 , encouraging private hospital operators and healthcare service providers to expand operations. This policy has resulted in new hospital developments, diagnostic centers, and specialized clinics being established across major cities and emerging healthcare clusters. As a result, institutional healthcare providers, including hospitals, ambulatory care centers, and specialized medical facilities, are expanding rapidly, generating higher patient treatment volumes and greater demand for healthcare services.

These reforms are materially increasing healthcare utilization by improving geographic accessibility and expanding service capacity. Budget planning documents indicate that the 2026 sector program includes building new hospitals with around 1,100 additional beds to expand healthcare capacity and improve regional coverage. Consequently, the combined effect of sustained government investment and growing private sector participation is directly expanding healthcare service volumes and strengthening long-term demand in the Saudi Arabian Healthcare Sector.

Saudi Arabia Healthcare Market Trend:

Rapid Integration of Digital Tools and Artificial Intelligence in Healthcare Delivery

Saudi Arabia’s healthcare sector is witnessing a structural shift toward digital health and artificial intelligence–enabled medical services, driven by national digital transformation policies and rising healthcare demand. The government has accelerated adoption through national digital health platforms and regulatory frameworks supporting telemedicine, e-prescriptions, and electronic health records. The Reports also confirm that the national Seha Virtual Hospital platform recorded more than 16 million consultations during 2025, highlighting the growing role of telemedicine across Saudi Arabia, enabling remote consultations and specialist support for complex cases. This nationwide digital infrastructure has significantly expanded access to specialized care, particularly for patients located outside major metropolitan healthcare centers.

The rapid expansion of digital healthcare services has begun reshaping operational models across hospitals, clinics, and diagnostic providers. Telemedicine adoption increased significantly following regulatory approval from the Saudi Health Council, which introduced national telehealth standards and licensing frameworks to ensure safe digital medical practices. In addition, hospitals are increasingly deploying artificial intelligence tools for medical imaging analysis, early disease detection, and predictive clinical decision support. The initiative has expanded to connect more than 200 hospitals across Saudi Arabia, enabli ng remote specialist consultations and advanced telemedicine services. These technologies enable healthcare institutions to manage growing patient volumes more efficiently while improving diagnostic accuracy and reducing treatment delays across healthcare facilities.

This digital transformation trend is expected to remain a long-term structural component of Saudi Arabia’s healthcare system due to continued policy support and infrastructure investment. National strategies emphasize expanding digital health capabilities, including unified patient data platforms, AI-driven medical research, and remote healthcare delivery systems. Saudi Arabia has become one of the leading adopters of digital health technologies in the Middle East through coordinated national initiatives. As digital infrastructure continues to scale across healthcare institutions, technology-driven service delivery models are likely to shape the sector’s long-term operational landscape.

Saudi Arabia Healthcare Market Opportunity:

Expansion of Domestic Pharmaceutical and Biotechnology Manufacturing

Saudi Arabia’s strategy to localize pharmaceutical and biotechnology production presents a significant market opportunity for new entrants and emerging healthcare companies. The government has intensified localization efforts through national industrial policies that aim to reduce reliance on imported medicines and strengthen domestic supply chains. According to the Saudi Ministry of Industry and Mineral Resources, the Kingdom launched the National Biotechnology Strategy in 2024, targeting investments of approximately USD 34.6 billion by 2040 to develop biotechnology innovation, vaccine manufacturing, and advanced therapeutic production.

This policy framework creates favorable conditions for pharmaceutical startups, research firms, and biotechnology manufacturers seeking entry into the expanding healthcare ecosystem. The biotechnology strategy is expected to generate 11,000 jobs by 2030 and 55,000 by 2040, while positioning Saudi Arabia as a regional biotechnology hub that attracts investment and research partnerships, while positioning Saudi Arabia as a regional biotechnology hub that attracts investment and research partnerships.

The opportunity is further reinforced by strong domestic demand for pharmaceuticals and medical technologies, supported by population growth and increasing healthcare utilization. Government programs are encouraging the establishment of pharmaceutical manufacturing facilities and research partnerships through regulatory facilitation, investment incentives, and industrial cluster development. For example, the Saudi Authority for Industrial Cities and Technology Zones (MODON) has been expanding specialized industrial zones designed for pharmaceutical production and medical technology manufacturing. These initiatives are enabling smaller biotechnology and pharmaceutical companies to establish l ocal production capabilities while benefiting from infrastructure, logistics networks, and regulatory support.

As Saudi Arabia continues to prioritize domestic healthcare production capacity and biotechnology research, new entrants are likely to benefit from a rapidly developing ecosystem that supports innovation, technology transfer, and long-term industrial growth within the healthcare sector.

Saudi Arabia Healthcare Market Challenge:

Complex Regularity Framework Impeding Smooth Progression

Saudi Arabia’s healthcare sector operates under a comprehensive regulatory framework that requires providers, pharmaceutical companies, and medical technology firms to obtain multiple approvals before entering the market. Regulatory oversight is primarily managed by authorities such as the Saudi Food and Drug Authority (SFDA) and the Ministry of Health, which enforce strict licensing, clinical evaluation, and quality assurance requirements . Medical products must undergo detailed registration procedures, including safety documentation, manufacturing verification, and compliance with national standards, before commercialization. While these measures are designed to protect patient safety and product quality, they can significantly lengthen approval timelines for new healthcare technologies and pharmaceuticals.

The regulatory burden has become more visible as Saudi Arabia has introduced updated compliance rules and digital submission systems to strengthen healthcare product oversight. For example, the Saudi Food and Drug Authority requires pharmaceutical manufacturers and medical device companies to submit comprehensive regulatory dossiers, clinical data, and manufacturing certifications for product approval . Companies must also comply with post-market surveillance, pricing regulations, and localization policies introduced under national industrial strategies. These requirements increase operational complexity, particularly for smaller companies that may lack the regulatory expertise or financial resources required to navigate approval processes efficiently.

As a result, regulatory complexity can slow the pace of innovation adoption and delay the introduction of new treatments or technologies in the healthcare system. High-risk medical devices may require 6–12 months or longer for approval due to detailed regulatory evaluation and clinical data review. Although regulatory reforms are gradually improving transparency and digitalizing approval systems, compliance obligations remain a key structural challenge influencing operational planning and market entry strategies within the Saudi healthcare sector.

Saudi Arabia Healthcare Market Epidemiology Profile:

Cardiovascular Diseases:

Cardiovascular diseases represent the dominant chronic disease burden in Saudi Arabia due to the growing prevalence of metabolic risk factors and demographic shifts. According to the World Health Organization, cardiovascular diseases account for nearly 37% of total deaths in the country, reflecting their significant contribution to national healthcare demand. Rising obesity levels, hypertension, and sedentary lifestyles have increased the prevalence of ischemic heart disease, heart failure, and stroke across adult populations. As a result, cardiovascular care remains a primary focus of healthcare providers and public health initiatives.

The increasing incidence of cardiovascular diseases has also generated substantial healthcare and economic pressures on the national health system. Long-term treatment requirements, including cardiac surgeries, diagnostic imaging, and continuous medication management, drive healthcare spending across hospitals and specialty cardiac centers. The Saudi Ministry of Health has expanded national screening and prevention programs to address cardiovascular risk factors such as hypertension and obesity. These initiatives aim to improve early diagnosis while supporting population-level disease management strategies.

Infrastructure expansion and specialized treatment capabilities further reinforce the dominance of cardiovascular disease management in the healthcare system. Saudi Arabia has invested in advanced cardiology units, catheterization laboratories, and tertiary care hospitals to improve treatment outcomes. Hospitals and specialized cardiac institutes increasingly deploy advanced technologies for interventional cardiology and cardiac imaging. Hospitals such as Dallah Al Nakheel Hospital’s Cardiac Centre have been recognized for their advanced cardiac care capabilities, including open-heart surgery and catheterization services, illustrating institutional investment in specialized cardiac services. Consequently, the high dise ase burden, combined with sustained investment in cardiac infrastructure and preventive healthcare programs, ensures that cardiovascular diseases remain the leading segment shaping healthcare demand in Saudi Arabia.

Diabetes:

Diabetes represents one of the most prevalent chronic diseases in Saudi Arabia, driven by lifestyle changes, dietary patterns, and increasing obesity levels. According to the International Diabetes Federation, approximately 23.1% of adults in Saudi Arabia live with diabetes, placing the country among the highest prevalence rates globally. Type 2 diabetes c onstitutes the majority of cases, particularly among middle-aged and elderly populations. The rapid growth of the diabetic population has intensified the need for continuous disease management, screening, and preventive care.

The rising incidence of diabetes has created significant healthcare and economic burdens across the national healthcare system. Patients frequently require long-term medical monitoring, pharmaceutical therapy, and treatment of complications such as kidney disease, neuropathy, and cardiovascular disorders. Public health programs led by the Saudi Ministry of Health focus on improving early diagnosis through nationwide screening and chronic disease management initiatives. These efforts aim to reduce complications while strengthening healthcare capacity for long-term diabetes care.

The treatment landscape for diabetes in Saudi Arabia has evolved significantly with the expansion of specialized endocrinology clinics and diabetes care centers. Hospitals and outpatient clinics increasingly integrate digital monitoring systems, advanced insulin therapies, and multidisciplinary care models to support patients. King Saud University Medical City Diabetes and Chronic Diseases unit provides comprehensive diabetes evaluation and treatment services, including multidisciplinary care involving specialists, nutri tionists, and education for patients with type 1 and type 2 diabetes. Saudi Arabia launched a digital diabetes command and control center to monitor patient data in real time, representing a major digital health investment in diabetes care.

Gain a Competitive Edge with Our Saudi Arabia Healthcare Market Report:

- The Saudi Arabia Healthcare Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competition, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Saudi Arabia Healthcare Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Introduction

- Executive Summary

- Key Insights

- Key Findings (2020–2024)

- Market Outlook Snapshot (2025–2032F)

- Strategic Imperatives

- Macro Environment Analysis

- Saudi Arabia at a Glance

- Geographic Overview

- Political Structure

- Trade & Regional Alliances

- Others

- Demographic Profile (2020–2032F)

- Population Trends

- Age Structure

- Urban vs Rural Distribution

- Fertility Rate Trends

- Migration Trends

- Ethnic Composition

- Economic Profile (2020–2032F)

- GDP (Current & Constant USD)

- GDP by Sector

- Working Population & Labor Participation

- Per Capita Income & Purchasing Power

- Unemployment & Underemployment

- Inflation Rate & Healthcare Cost Impact

- Foreign Direct Investment Trends

- Country PESTLE Analysis

- Saudi Arabia at a Glance

- Saudi Arabia Healthcare Sector Analysis, 2026

- Healthcare System Overview

- Structure of Healthcare System

- Public vs Private Healthcare

- Governance & Regulatory Authorities

- Others

- Healthcare Ecosystem & Infrastructure (2020–2026)

- Healthcare Expenditure

- Healthcare Expenditure as % of GDP

- Per Capita Healthcare Expenditure

- Healthcare Facilities

- Number of Hospitals

- Number of Clinics

- Number of Pharmacies

- Number of Diagnostic Centres

- Public vs Private Distribution

- Bed Availability & Utilization

- Beds per 1,000 Population

- Beds Speciality

- Regional Disparities

- Healthcare Workforce

- Physicians per 1,000 Population

- Physicians by Speciality

- Nurses

- Dentists

- Allied Health Professionals

- Healthcare Expenditure

- Healthcare System Overview

- Health Outcomes & Public Health Indicators (2020–2026)

- Life Expectancy (Male vs Female)

- Infant Mortality Rate

- Maternal Mortality Ratio

- Immunisation Coverage Rates (Measles, DPT, HPV, COVID-19)

- Overall Disease Burden Trends

- Healthcare Reforms & Large-Scale Projects (2020-2026)

- Government Reforms

- Public-Private Partnerships

- Infrastructure Expansion Projects

- Private Sector Investments

- Others

- Insurance Framework

- Public Health Insurance Programs

- Private Health Insurance Market

- Insurance Penetration & Coverage Gaps

- Payer Landscape

- Reimbursement Models (FFS, Bundled, Value-Based Care)

- Claims Management & Transparency Issues

- Out-of-Pocket Expenditure Trends (2020-2026)

- Regulatory Environment (Healthcare Sector)

- Market Authorisation for Pharmaceuticals

- Market Authorisation for Medical Devices

- Licensing for Manufacturing, Import & Export

- Clinical Trial Regulations

- Intellectual Property & Patent Protection

- Advertising, Labeling & Packaging Regulations

- Pharmacy & Hospital Licensing Rules

- Others

- Market Dynamics & Technology

- Healthcare Market Dynamics

- Growth Drivers

- Challenges & Barriers

- Emerging Opportunities

- Value Chain Analysis

- Healthcare Technology Trends

- Digital Health Maturity

- Telemedicine & Remote Monitoring

- Artificial Intelligence & Machine Learning

- Health Apps & Wearables

- Robotic Surgery

- EHR, Data Interoperability & Cybersecurity

- Others

- Healthcare Market Dynamics

- Epidemiology Profile (By Age & By Gender) (2020–2032F)

- Chronic Diseases

- Cardiovascular Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Diabetes

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cancer

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Respiratory Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Kidney Disease

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cardiovascular Diseases

- Infectious Diseases

- Tuberculosis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- HIV

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Hepatitis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Others

- Tuberculosis

- Mental Health

- Prevalence of Mental Health Disorders

- Suicide Rates & Trends

- Urban-Rural & Gender Disparities

- Infrastructure Gaps

- Economic & Social Burden

- Chronic Diseases

- Saudi Arabia Healthcare System Stakeholders Analysis, 2026

- Saudi Arabia Pharmaceutical Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- Prescription vs OTC

- Generics vs Branded

- Therapeutic Category Distribution

- Manufacturing Landscape

- Distribution & Supply Chain

- Major Distributors

- Major Suppliers

- Major Local and Multinational Players

- Fresenius SE & Co. KGaA

- Helios Kliniken GmbH

- Asklepios Kliniken

- Sana Kliniken AG

- Rhön-Klinikum AG

- Siemens Healthineers

- Schön Klinik SE

- Klinikum Stuttgart

- University Medical Centre Hamburg

- Charité – Universitätsmedizin

- Pharmaceutical sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Pharmaceutical Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- Saudi Arabia Medical Devices Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- By Device Type

- By Risk Class

- By End-User

- Manufacturing Landscape

- Distribution & Supply Chain

- Distributors

- Supply Chain

- Major Local and Multinational Players

- Fresenius SE & Co. KGaA

- Helios Kliniken GmbH

- Asklepios Kliniken

- Sana Kliniken AG

- Rhön-Klinikum AG

- Siemens Healthineers

- Schön Klinik SE

- Klinikum Stuttgart

- University Medical Centre Hamburg

- Charité – Universitätsmedizin

- Medical Devices Sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Medical Device Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- Saudi Arabia Pharmaceutical Market Outlook (2020–2030F)

- Saudi Arabia Strategic & Investments in Healthcare Outlook (2025-2032F)

- High-Growth Segments

- Foreign Investment Opportunities

- Government Incentives & Ease of Doing Business

- Risk Assessment & Mitigation

- Trade Associations & Industry Bodies

- Pharmaceutical Associations

- Medical Device Associations

- Healthcare Provider Associations

- Regulatory & Standards Bodies

- Healthcare Trade Fairs & Conferences (2024–2026)

- National Healthcare Exhibitions

- Medical Technology Events

- Pharmaceutical Conferences

- Regional Latin America Events Relevant to Saudi Arabia

- Impact of Global Health Events

- COVID-19 Impact (2020–2022)

- Post-Pandemic Recovery

- Emergency Preparedness Evolution

- Strategic Recommendations

- Market Entry Strategy

- Partnership Models

- Pricing Strategy

- Regulatory Navigation

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now