Saudi Arabia E-Waste Management Market Research Report: Growth Drivers & Forecast (2026-2032)

By Type (Large Household Appliances, Small Household Appliances, IT and Telecommunications Equipment, Consumer Electronics, Lighting Equipment, Electrical and Electronic Tools, Toy ... s, Leisure and Sports Equipment, Medical Devices, Monitoring and Control Instruments, Automatic Dispensers), By Process (Collection and Transportation, Sorting and Dismantling, Recycling and Recovery, Refurbishing and Reuse, Treatment and Disposal), By Technology (Physical Recycling, Chemical Recycling, Biological Recycling, Mechanical Recycling), By Material Type (Metals, Plastics, Glass, Others), By Service (Collection Services, Recycling Services, Refurbishment Services, Disposal Services, Consultancy Services), By Collection Channel (Take-back Programs, Retail Collection, Municipal Collection, Third-party Collection, Direct Producer Collection), By End-User (Residential, Commercial, Industrial, Government and Public Sector), and others Read more

- Environment

- Feb 2026

- Pages 125

- Report Format: PDF, Excel, PPT

Saudi Arabia E-Waste Management Market

Projected 6.30% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 183 million

Market Size (2032)

USD 264 million

Base Year

2025

Projected CAGR

6.30%

Leading Segments

By End User: Residential

Saudi Arabia E-Waste Management Market Report Key Takeaways:

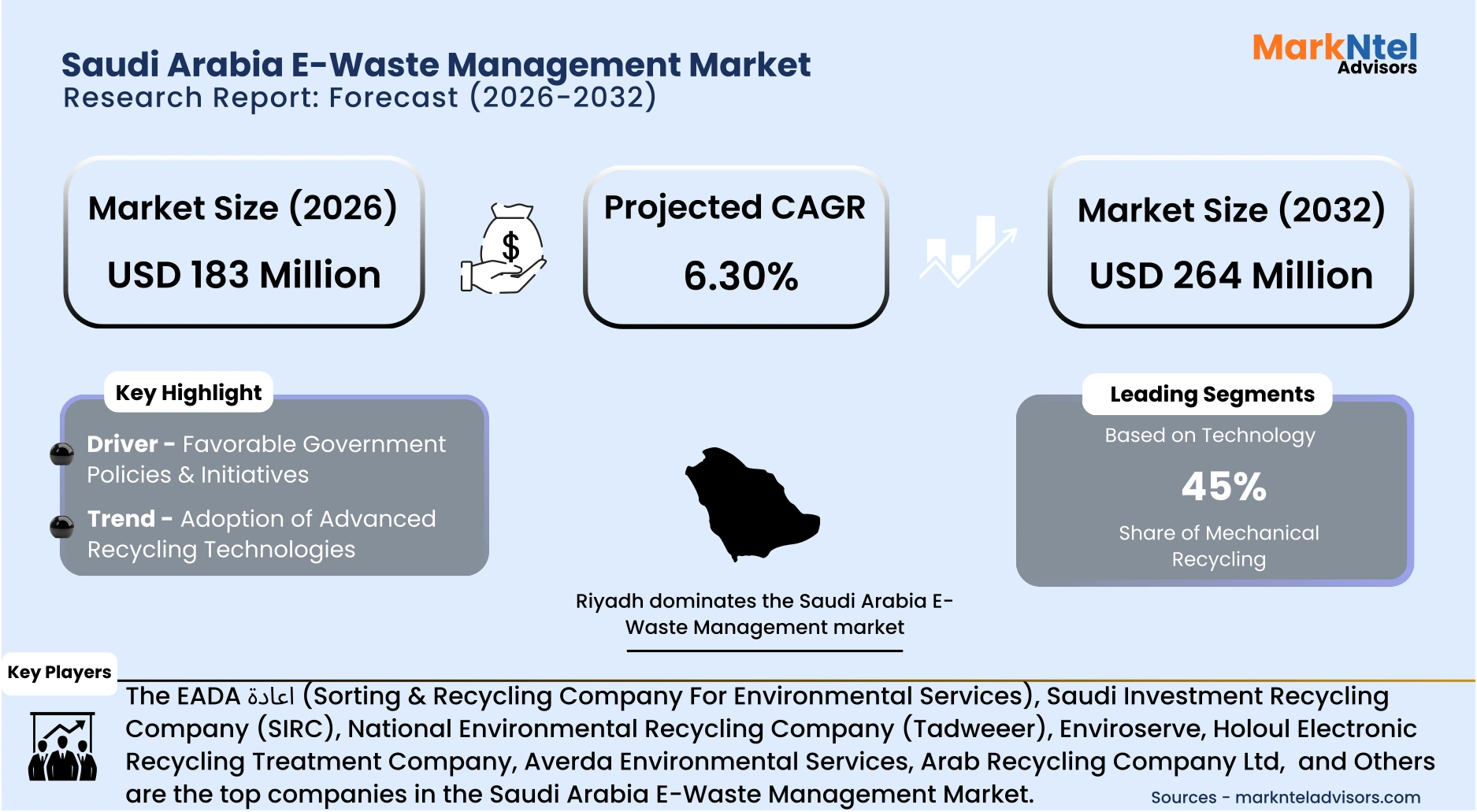

- The Saudi Arabia E-Waste Management market size was valued at USD 161 million in 2025 and is projected to grow from USD 183 million in 2026 to USD 264 million by 2032, exhibiting a CAGR of 6.30% during the forecast period.

- Riyadh holds the largest market share of about 32% in the Saudi Arabia E-Waste Management Market in 2026.

- By technology, the mechanical recycling segment represented a significant share of about 45% in the Saudi Arabia E-Waste Management Market in 2026.

- By end user, the residential segment presented a significant share of about 47% in the Saudi Arabia E-Waste Management Market in 2026.

- Leading E-waste management companies in the Saudi Arabia Market are EADA اعادة (Sorting & Recycling Company For Environmental Services), Saudi Investment Recycling Company (SIRC), National Environmental Recycling Company (Tadweeer), Enviroserve, Holoul Electronic Recycling Treatment Company, Averda Environmental Services, Arab Recycling Company Ltd, First Saudi Recycling, Al Qaryan Group, Waste Collection and Recycling Company (WASCO), REVIVA-JED HO (Reviva), Envac Saudi Arabia, Arabian Environmental Science Limited (ARESL), Blue Eco Waste Management Company, Desert Technologies Environmental Services, and Others.

Market Insights & Analysis: Saudi Arabia E-Waste Management Market (2026-32):

The Saudi Arabia E-Waste Management Market size was valued at approximately USD 161million in 2025 and is projected to grow from USD 183 million in 2026 to USD 264 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 6.30% during the forecast period, i.e., 2026-32.

The Saudi Arabia E-Waste Management Market is projected to expand steadily, driven by supported by strong regulatory direction, capital allocation, and technology adoption aligned with Vision 2030. Government intervention has shifted waste management from a municipal function to a strategic economic and environmental priority, directly influencing the formalization of electronic waste collection, recycling, and recovery systems.

The Ministry of Environment, Water and Agriculture (MEWA) has introduced a comprehensive waste sector transformation plan targeting up to 95% recycling, compared with the historical 3–4% recycling rate. The program is expected to contribute approximately USD 32 billion to GDP and enable recycling of up to 100 million tons annually. This initiative operates under the broader National Environmental Strategy, which includes over 65 initiatives supported by investments exceeding USD 14.7 billion. These measures strengthen hazardous waste regulation, enhance scientific waste handling standards, and reinforce oversight through a centralized national waste authority working in coordination with private operators.

Policy execution is already producing measurable outcomes. For instance, in August 2024, authorities reported the successful recycling of more than 100,000 electronic devices, demonstrating the operational rollout of structured collection and processing mechanisms under regulated frameworks. This milestone reflects improved compliance, public participation, and growing institutional coordination in managing end-of-life electronics.

Technology adoption is further shaping market evolution. For example, Saudi-based firms such as Wastech are deploying AI-enabled sorting systems, IoT-connected smart bins, ultrasonic and RFID monitoring devices, and cloud-based analytics platforms. These solutions support automated waste identification, real-time fill-level tracking, optimized logistics routing, and digital performance monitoring. Such integration enhances source segregation efficiency, reduces contamination, and strengthens upstream collection — critical components for scaling formal e-waste recycling infrastructure.

Long-term commitments reinforce growth visibility. For example, the 2025 ITU policy toolkit highlights a memorandum between the Communications, Space and Technology Commission (CST) and the National Center for Waste Management (MWAN) targeting a 90% e-waste recycling rate by 2040, signaling sustained regulatory planning .

Additionally, the Ministry of Industry and Mineral Resources is developing a national licensing framework to formalize recycling as an industrial sector, aiming to attract approximately USD 10.7 billion in investment and increase material recovery to 4.2 million tonnes by 2035. These measures will expand advanced recycling capacity and industrial-scale e-waste processing.

Saudi Arabia’s e-waste management market outlook is underpinned by regulatory modernization, significant public investment, measurable implementation progress, and technology-driven operational efficiency. Continued policy enforcement and infrastructure expansion are expected to accelerate formalization, increase recovery rates, and position the Kingdom as a regional leader in structured e-waste management.

Saudi Arabia E-Waste Management Market Recent Developments:

- 2025: stc reinforced its environmental leadership by recycling 39,914 electronic devices across Saudi Arabia, of which 25,041 were fully recycled, 1,235 refurbished, and 11,367 redistributed to beneficiaries, including schools and charities. The initiative prevented over 80,000 kg of carbon emissions by recycling approximately 34 tonnes of e-waste, benefiting more than 760 organizations nationwide. This effort underscores stc’s commitment to sustainability and supports broader national goals for responsible e-waste management and circular use of electronics.

Saudi Arabia E-Waste Management Market Scope:

| Category | Segments |

|---|---|

| By Type | (Large Household Appliances, Small Household Appliances, IT and Telecommunications Equipment, Consumer Electronics, Lighting Equipment, Electrical and Electronic Tools, Toys, Leisure and Sports Equipment, Medical Devices, Monitoring and Control Instruments, Automatic Dispensers), |

| By Process | (Collection and Transportation, Sorting and Dismantling, Recycling and Recovery, Refurbishing and Reuse, Treatment and Disposal), |

| By Technology | (Physical Recycling, Chemical Recycling, Biological Recycling, Mechanical Recycling), |

| By Material Type | (Metals, Plastics, Glass, Others), |

| By Service | (Collection Services, Recycling Services, Refurbishment Services, Disposal Services, Consultancy Services), |

| By Collection Channel | (Take-back Programs, Retail Collection, Municipal Collection, Third-party Collection, Direct Producer Collection), |

| By End-User | (Residential, Commercial, Industrial, Government and Public Sector), |

Saudi Arabia E-Waste Management Market Driver:

Favorable Government Policies & Initiatives

Government leadership and structured regional implementation under Vision 2030 are significantly accelerating the development of Saudi Arabia’s e-waste management market. National waste and sustainability policies are being operationalized at the city and provincial levels, translating strategic targets into measurable infrastructure and compliance outcomes.

Riyadh has emerged as a primary execution hub under the Saudi Green Initiative (SGI), which targets diversion of 94% of the city’s waste from landfills and composting of over 1.3 million tons of organic waste, contributing to an estimated reduction of approximately 4.1 million tonnes of CO₂ equivalent emissions. Achieving these benchmarks requires enhanced segregation systems, regulated collection mechanisms, and expanded recycling infrastructure frameworks that inherently support formal e-waste management capacity.

In 2025, the “Recycle Your Device” initiative was relaunched in Riyadh to promote the structured collection of obsolete electronics. The program strengthens formal recycling channels by encouraging refurbishment, reuse, and responsible disposal practices aligned with circular economy objectives.

Similarly, the Eastern Province (including Dammam) is advancing waste sector planning aligned with national targets of 95% landfill diversion across waste streams, under regulatory oversight of the National Centre for Waste Management (MWAN). Municipal compliance and infrastructure development are reinforcing formal recycling pathways, including electronic waste streams.

Regional implementation of national sustainability policies is converting regulatory ambition into operational progress. By strengthening compliance frameworks and expanding diversion infrastructure, Riyadh and the Eastern Province are directly supporting scalable growth in Saudi Arabia’s e-waste management market.

Saudi Arabia E-Waste Management Market Trend:

Adoption of Advanced Recycling Technologies

Saudi Arabia’s strategic transition toward a circular economy under Vision 2030 is significantly accelerating the deployment of advanced recycling technologies within the e-waste management sector. As national landfill diversion targets strengthen and regulatory oversight expands, recycling operations are shifting from basic collection models to technology-intensive processing systems designed to improve material recovery rates, operational efficiency, and environmental compliance.

A leading example is Holoul Electronic Recycling Treatment Company, one of the Kingdom’s specialized e-waste recycling operators. The company manages an industrial-scale facility covering approximately 9,000 square meters, integrating mechanical shredding systems with structured manual dismantling lines. The plant is capable of processing nearly 10,000 tonnes of electronic scrap annually, in addition to around 1,200 tonnes per year of high-value electronic components. Holoul also provides certified secure data destruction services, ensuring adherence to environmental, safety, and information protection standards.

The integration of industrial shredding, controlled material separation, and secure downstream recovery reflects the growing sophistication of Saudi Arabia’s e-waste processing capabilities. Such technological upgrades enhance the extraction of valuable metals, reduce environmental leakage risks, and improve compliance with hazardous waste handling requirements.

The expansion of advanced, industrial-scale recycling facilities demonstrates a structural modernization of Saudi Arabia’s e-waste ecosystem. Continued investment in high-efficiency processing technologies will strengthen recovery performance, regulatory alignment, and long-term sustainability, reinforcing the market’s growth trajectory.

Saudi Arabia E-Waste Management Market Opportunity:

Expansion of Public-Private Partnerships (PPPs)

Public–Private Partnerships (PPPs) are emerging as a high-impact opportunity to strengthen Saudi Arabia’s waste and e-waste management infrastructure while mobilizing long-term private capital. The Saudi Investment Recycling Company (SIRC), a wholly owned subsidiary of the Public Investment Fund, is leading efforts to develop integrated recycling ecosystems through structured partnerships with local and international investors. These initiatives align with national objectives to divert 94% of municipal solid waste from landfills by 2035, creating a strong policy-backed investment environment.

In Riyadh and the Eastern Province, tripartite agreements between the National Center for Waste Management (MWAN), regional municipalities, and SIRC are formalizing PPP models to establish advanced recycling and treatment facilities. These projects aim to recycle 81% of municipal waste and 60% of construction and demolition waste by 2035, reflecting coordinated governance structures and defined private-sector operating roles .

Looking beyond 2025, long-term concession frameworks covering 2025–2035 are expected to catalyze USD 2.7–4.0 billion in municipal waste management projects and USD 0.27–0.53 billion in specialized recycling infrastructure, including e-waste processing and waste-to-energy development .

The institutionalization of PPP models provides a scalable mechanism to expand recycling capacity, integrate advanced technologies, and enhance operational efficiency. By combining regulatory stability with private investment and expertise, PPPs are positioned to significantly accelerate the growth and formalization of Saudi Arabia’s e-waste management market.

Saudi Arabia E-Waste Management Market Challenge:

Insufficient Collection & Recycling Infrastructure

Saudi Arabia’s e-waste management market is materially constrained by underdeveloped collection systems and limited formal recycling capacity, which together restrict efficient resource recovery and environmentally sound disposal. Although national waste strategies have expanded in recent years, dedicated e-waste collection channels remain insufficiently integrated across municipalities, resulting in weak segregation at source and low formal recovery rates.

Studies indicate that nearly 85% of electronic waste is still directed to landfills, reflecting gaps in structured take-back programs, licensed recyclers, and consumer awareness mechanisms. This infrastructure deficit undermines the circular economy objectives embedded within Vision 2030 and limits the ability to extract valuable secondary raw materials from discarded electronics.

Formal processing capacity remains disproportionately low relative to national generation volumes. The National Environmental Recycling Company (Tadweer), recognized as a key licensed recycler, had processed approximately 100 million kilograms of e-waste. However, annual e-waste generation is estimated at 617–620 million kilograms, highlighting a significant capacity gap.

Unless collection networks are expanded and specialized recycling infrastructure is scaled nationwide, this structural imbalance between generation and processing capability will continue to impede the sector’s efficiency, investment attractiveness, and long-term sustainability outcomes.

Saudi Arabia E-Waste Management Market (2026-32) Segmentation Analysis:

The Saudi Arabia E-Waste Management Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Technology:

- Physical Recycling

- Chemical Recycling

- Biological Recycling

- Mechanical Recycling

The mechanical recycling segment dominates the Saudi Arabia E-Waste Management market, accounting for approximately 45% of the market size, primarily due to its operational maturity, scalability, and economic feasibility.

The process involves systematic dismantling, shredding, crushing, and advanced separation techniques such as magnetic and eddy current separation to recover metals and reusable materials from discarded electronic equipment.

In comparison to chemical and biological recycling methods, mechanical recycling requires relatively lower capital investment and limited use of specialized reagents, making it more commercially viable within the Kingdom’s developing recycling ecosystem.

The technology is also well-suited to handling high volumes of heterogeneous electronic waste, enabling efficient recovery of copper, aluminum, ferrous metals, and certain plastics. This capability is particularly critical given the substantial gap between e-waste generation and formal treatment capacity in Saudi Arabia.

Moreover, mechanical recycling supports regulatory compliance by facilitating the controlled removal of hazardous components before further downstream treatment. Its proven industrial performance, shorter implementation timelines, and predictable return on investment make it the preferred foundational technology for newly established and expanding recycling facilities. Collectively, these factors position mechanical recycling as the dominant and most commercially established technology within the Kingdom’s e-waste management landscape.

Based on End User:

- Residential

- Commercial

- Industrial

- Government and Public Sector

The residential segment dominates the Saudi Arabia E-Waste Management market, accounting for about 47% of the total market size, reflecting the substantial volume of consumer electronics circulating within households.

Rapid digitalization, expanding internet penetration, and high smartphone adoption rates have significantly increased device ownership per capita. As households increasingly rely on laptops, tablets, smart televisions, gaming consoles, and connected home appliances, the cumulative stock of electronic products continues to expand.

Frequent product upgrades and shorter replacement cycles further intensify residential e-waste generation. Consumer-driven demand for newer models with enhanced features results in accelerated device obsolescence, particularly in mobile phones and personal computing equipment. This pattern is reinforced by a young, technology-oriented population and strong retail availability of electronic goods across major cities.

Additionally, national sustainability initiatives and awareness campaigns increasingly focus on household-level participation in recycling programs. Structured collection drives and take-back schemes are progressively integrating residential waste streams into formal recycling channels, strengthening traceability and material recovery rates.

Although commercial, industrial, and government entities generate high-value and bulk electronic waste, their procurement and disposal cycles are more centralized and regulated. In contrast, the sheer scale, frequency, and geographic spread of household electronics consumption position the residential segment as the dominant contributor to overall e-waste volumes in the Kingdom.

Saudi Arabia E-Waste Management Market (2026-32): Regional Projection

Riyadh dominates the Saudi Arabia E-Waste Management market with an estimated 32% share, due to its economic scale, population concentration, and institutional centrality. As the Kingdom’s capital and primary administrative hub, the city hosts major government bodies, corporate headquarters, financial institutions, and technology-driven enterprises.

This concentration of economic and public-sector activity generates substantial volumes of electronic equipment consumption and replacement across residential, commercial, and governmental segments. High household incomes, rapid digital transformation, and strong penetration of smart devices further accelerate product turnover, positioning Riyadh as the largest contributor to national e-waste volumes.

Beyond waste generation, Riyadh plays a decisive role in regulatory development and international sustainability engagement. The Communications, Space and Technology Commission (CST), in collaboration with the International Telecommunication Union (ITU), launched the Development of Electronic Waste Management Regulations initiative during Climate Week MENA in Riyadh.

The program will pilot regulatory implementation in Zimbabwe, Rwanda, and Paraguay, supporting the creation of globally harmonized e-waste standards. This initiative followed a prior agreement signed at the ITU Global Symposium for Regulators ahead of preparations for the United Nations Framework Convention on Climate Change COP28.

Through its combined role in waste generation, infrastructure development, and international regulatory leadership, Riyadh maintains a structurally dominant position within Saudi Arabia’s evolving e-waste management ecosystem.

Gain a Competitive Edge with Our Saudi Arabia E-Waste Management Market Report:

- Saudi Arabia E-Waste Management Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Saudi Arabia E-Waste Management Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia E-Waste Management Market Policies, Regulations, and Product Standards

- Saudi Arabia E-Waste Management Market Trends & Developments

- Saudi Arabia E-Waste Management Market Dynamics

- Growth Factors

- Challenges

- Saudi Arabia E-Waste Management Market Hotspot & Opportunities

- Saudi Arabia E-Waste Management Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Large Household Appliances

- Small Household Appliances

- IT and Telecommunications Equipment

- Consumer Electronics

- Lighting Equipment

- Electrical and Electronic Tools

- Toys

- Leisure and Sports Equipment

- Medical Devices

- Monitoring and Control Instruments

- Automatic Dispensers

- By Process- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Collection and Transportation

- Sorting and Dismantling

- Recycling and Recovery

- Refurbishing and Reuse

- Treatment and Disposal

- By Technology- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Physical Recycling

- Chemical Recycling

- Biological Recycling

- Mechanical Recycling

- By Material Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Metals

- Plastics

- Glass

- Others

- By Service- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Collection Services

- Recycling Services

- Refurbishment Services

- Disposal Services

- Consultancy Services

- By Collection Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Take-back Programs

- Retail Collection

- Municipal Collection

- Third-party Collection

- Direct Producer Collection

- By End-User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Residential

- Commercial

- Industrial

- Government and Public Sector

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Riyadh

- Jeddah

- Damam

- Mecca & Madinah

- Others

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Saudi Arabia E-Waste Physical Recycling Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Process- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Technology- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Material Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Service- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Collection Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Saudi Arabia E-Waste Chemical Recycling Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Process- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Technology- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Material Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Service- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Collection Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Saudi Arabia E-Waste Biological Recycling Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Process- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Technology- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Material Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Service- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Collection Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Saudi Arabia E-Waste Mechanical Recycling Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Thousand Tons)

- Market Share & Outlook

- By Process- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Technology- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Material Type- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Service- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Collection Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By End-User- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Tons

- Market Size & Outlook

- Saudi Arabia E-Waste Management Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- EADA اعادة (Sorting & Recycling Company For Environmental Services)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saudi Investment Recycling Company (SIRC)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Environmental Recycling Company (Tadweeer)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Enviroserve

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Holoul Electronic Recycling Treatment Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Averda Environmental Services

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arab Recycling Company Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- First Saudi Recycling

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Qaryan Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Waste Collection and Recycling Company (WASCO)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- REVIVA-JED HO (Reviva)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Envac Saudi Arabia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Arabian Environmental Science Limited (ARESL)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Blue Eco Waste Management Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Desert Technologies Environmental Services

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EADA اعادة (Sorting & Recycling Company For Environmental Services)

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now