Saudi Arabia Architectural and Engineering Services Market Research Report: Growth Drivers & Forecast (2026-2032)

By Service Type (Architectural Services, Engineering Services), By End-User (Residential, Commercial, Infrastructure, Industrial, Institutional), By Province (Riyadh, Makkah, Easte ... rn Province, Madinah, Tabuk, Asir, Qassim) Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 140

- Report Format: PDF, Excel, PPT

Saudi Arabia Architectural and Engineering Services Market

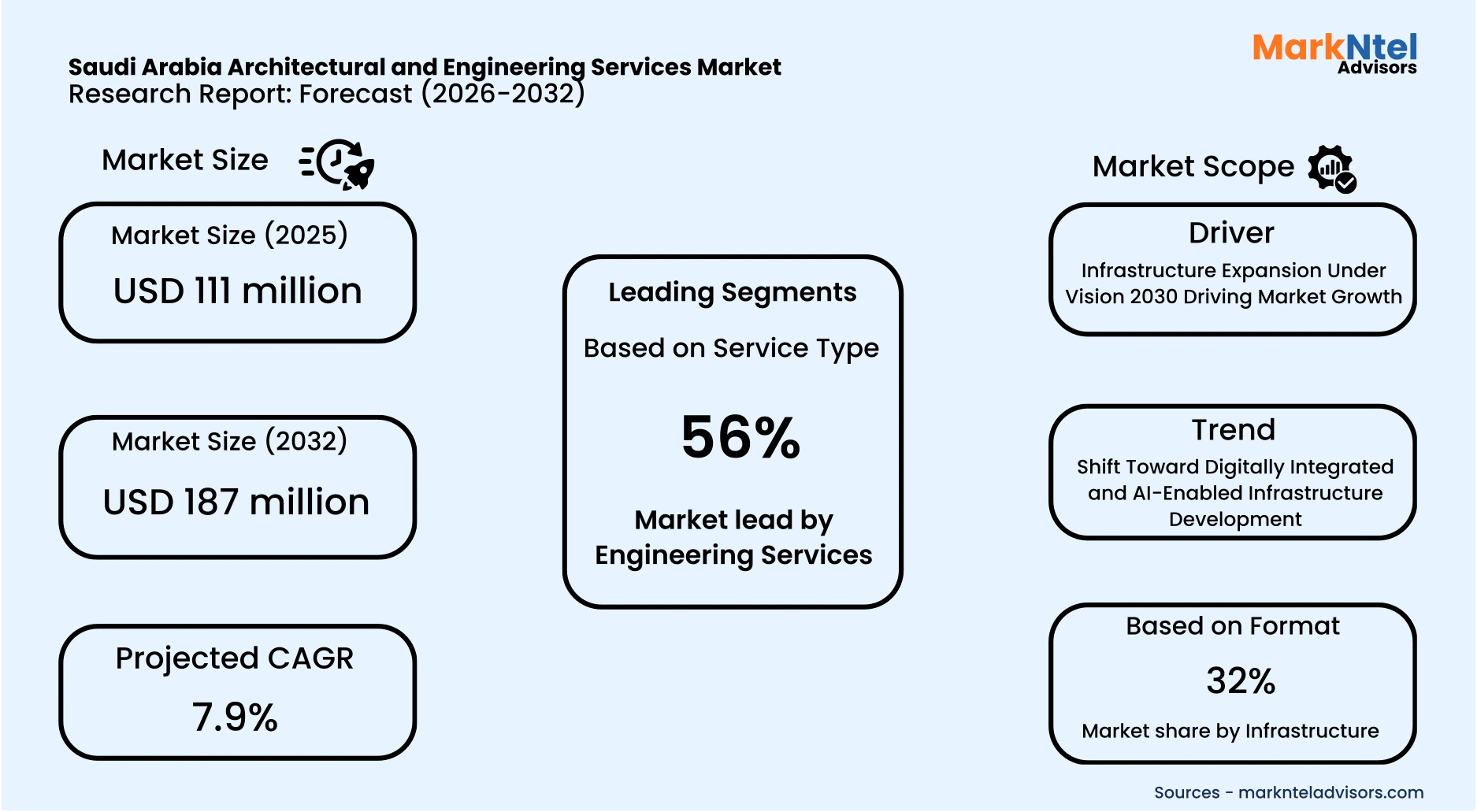

Projected 7.9% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 111 million

Market Size (2032)

USD 187 million

Base Year

2025

Projected CAGR

7.9%

Leading Segments

By End User: Infrastructure

Saudi Arabia Architectural and Engineering Services Market Report Key Takeaways:

- Market size is estimated at USD 111 million in 2025 and is projected to reach USD 187 million by 2032. The estimated CAGR from 2026 to 2032 is around 7.9%, indicating strong growth.

- Riyadh is dominating this market with 32% market share in 2026.

- By Service Type, the Engineering Services seized a significant share of about 56% in the Saudi Arabia Architectural and Engineering Services Market in 2026.

- By End User, the Infrastructure segment represented a significant share of about 32% in the Saudi Arabia Architectural and Engineering Services Market in 2026.

- Leading Architectural and Engineering Services companies in Saudi Arabia are AECOM, Jacobs, WSP, Bechtel, Parsons Corporation, AtkinsRéalis, Fluor Corporation, HDR Inc., and Others.

Market Insights & Analysis: Saudi Arabia Architectural and Engineering Services Market (2026-32):

The Saudi Arabia Architectural and Engineering Services Market size is estimated at USD 111 million in 2025 and is projected to reach USD 187 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 7.9% during the forecast period, i.e., 2026-32.

Saudi Arabia’s Architectural & Engineering Services Market has demonstrated resilient growth supported by sustained fiscal expansion and structural economic reforms under Vision 2030. The Saudi Ministry of Finance announced a 2025 national budget of approximately USD 333 billion, maintaining high capital allocation toward infrastructure, housing, and transport development. Public investment momentum has strengthened project pipelines requiring architectural planning, structural engineering, and technical design services prior to construction execution. Additionally, Saudi Arabia’s total investment volume surpassed approximately USD 400 billion for the first time in 2025 , while FDI inflows are expected between USD 37–40 billion in 2025, reinforcing demand for internationally compliant engineering and consultancy expertise.

Infrastructure-led development remains the primary demand driver, particularly through giga-projects such as NEOM, Diriyah, and Red Sea developments overseen by the Public Investment Fund. These multi-billion-dollar initiatives require master planning, environmental engineering, MEP system design, and advanced structural modeling, intensifying engineering service revenue. The Ministry of Tourism has confirmed a target of 150 million annual visitors by 2030, accelerating hotel construction, airport expansions, and mixed-use commercial districts . Residential programs under the Ministry of Municipal and Rural Affairs further stimulate architectural services aligned with rapid urbanization and population growth.

Regulatory modernization continues to elevate professional design standards across the Kingdom. The Saudi Building Code mandates compliance with structural safety, fire protection, and energy-efficiency regulations, increasing technical design complexity and engineering oversight requirements. Meanwhile, the Saudi Green Initiative’s commitment to achieving net-zero emissions by 2060 is driving adoption of sustainable architecture, environmental modeling, and energy-efficient system integration . Localization incentives encouraging international firms to establish regional headquarters in Riyadh are strengthening knowledge transfer and expanding the professional services ecosystem.

Looking ahead, continued fiscal prioritization of transport corridors, logistics hubs, and smart-city integration is expected to sustain strong demand for architectural and engineering design services. Economic diversification policies aimed at increasing non-oil GDP contribution are expanding commercial and industrial project pipelines. Infrastructure expansion, tourism growth, and sustainability mandates collectively reinforce long-term structural demand across residential, commercial, and institutional segments. These interconnected economic, demographic, and regulatory drivers position the Saudi Architectural & Engineering Services market for stable and sustained expansion through the remainder of the decade.

Saudi Arabia Architectural and Engineering Services Market Recent Developments:

- 2025 : Nemetschek Group, a global AEC software provider, entered a strategic partnership with buildingSMART Saudi Arabia to advance digital transformation and open standards in the Kingdom’s architecture and engineering sector, enhancing interoperability and design efficiency.

- 2025 : AECOM, in joint venture with Jacobs, has been appointed by New Murabba Development Company to deliver design consultancy services for The Mukaab, a landmark mixed-use development in Riyadh under Vision 2030. The scope includes infrastructure, tunnels, the Mukaab Core, and surrounding public realm works.

Saudi Arabia Architectural and Engineering Services Market Scope:

| Category | Segments |

|---|---|

| By Service Type | (Architectural Services, Engineering Services), |

| By End-User | (Residential, Commercial, Infrastructure, Industrial, Institutional), |

| By Province | (Riyadh, Makkah, Eastern Province, Madinah, Tabuk, Asir, Qassim) |

Saudi Arabia Architectural and Engineering Services Market Driver:

Infrastructure Expansion Under Vision 2030 Driving Market Growth

Infrastructure expansion under Vision 2030 remains the most influential structural driver of the Saudi Arabia Architectural and Engineering Services market. Large-scale national development programs across transport, housing, tourism, and logistics are creating sustained demand for architectural planning, structural engineering, and multidisciplinary design services. The acceleration of giga-project execution has significantly expanded the volume of pre-construction planning and technical consultancy assignments. Notably, Saudi Arabia approved approximately USD 350 billion 2026 budget focused on Vision 2030 goals, emphasizing continued spending on infrastructure, public services, and diversification initiatives, reinforcing long-term capital commitment to development .

The impact is visible across major end-user segments including infrastructure, commercial, residential, industrial, and mixed-use developments. Mega urban projects require master planning, environmental assessments, MEP system integration, and advanced engineering modeling prior to construction execution. The expansion of tourism infrastructure, residential communities, logistics hubs, and industrial manufacturing facilities further strengthens project pipelines nationwide. Additionally, Saudi Aramco has achieved 70% local procurement under its iktva program, contributing over USD 280 billion to GDP and targeting 75% local content by 2030, driving new industrial facility development and engineering demand across manufacturing and energy supply chains . As a result, engineering services are increasingly central to project feasibility and compliance requirements.

Unlike temporary policy shifts, infrastructure-led expansion systematically increases the number, scale, and complexity of projects entering the design phase. Regulatory enforcement and sustainability standards further elevate technical requirements across all new developments. This combination of long-term public investment strategy, industrial localization, and urban transformation ensures sustained volume growth in professional architectural and engineering services. Consequently, infrastructure expansion under Vision 2030 remains the primary engine of structural market growth.

Saudi Arabia Architectural and Engineering Services Market Trend:

Shift Toward Digitally Integrated and AI-Enabled Infrastructure Development

Saudi Arabia’s Architectural and Engineering Services Market is undergoing a structural shift toward digitally integrated and AI-enabled infrastructure development. This transition has accelerated under Vision 2030, which emphasizes digital transformation across public infrastructure and smart city programs. In 2025, the partnership between Nemetschek Group and buildingSMART Saudi Arabia formalized the adoption of open BIM standards across major developments . Additionally, NEOM’s strategic pivot toward AI infrastructure and large-scale data centers reflects growing prioritization of digital backbone assets within national planning frameworks.

This shift is reshaping industry operating models by embedding digital coordination, simulation, and lifecycle analysis into project execution. Engineering scope is expanding beyond traditional building design toward data center architecture, intelligent utilities, and digitally managed transport systems. Public infrastructure tenders increasingly require digital documentation and advanced modeling capabilities, raising technical benchmarks across commercial, residential, and infrastructure segments. A&E firms are therefore adapting business models to integrate software-driven design, automation tools, and advanced systems engineering expertise.

The trend is expected to persist as digital and computational assets become central to Saudi Arabia’s long-term economic diversification strategy. In 2026, ITC Infotech launched a Digital and AI Engineering Hub in Riyadh, reinforcing localized capability development in AI-enabled engineering services. Ongoing smart city investments and regulatory modernization further necessitate digitally coordinated project delivery . Consequently, structural digitalization is materially influencing long-term market evolution and competitive positioning within the Kingdom’s A&E sector.

Saudi Arabia Architectural and Engineering Services Market Opportunity:

Expansion of Tourism and Entertainment Infrastructure Projects

The expansion of tourism and entertainment infrastructure under Vision 2030 represents the most compelling market opportunity for new entrants in Saudi Arabia’s Architectural and Engineering Services market. The Ministry of Tourism has reaffirmed its target of attracting 150 million annual visitors by 2030, supported by ongoing investment in hospitality, cultural districts, and destination developments . In 2026, Saudi Arabia approved a national budget of approximately USD 350 billion with continued allocation toward diversification initiatives, including tourism infrastructure. In 2025, the Saudi Fund for Development signed an agreement with FIFA to provide up to USD 1 billion in financing support for football and sports infrastructure projects, reinforcing the Kingdom’s strategic investment in large-scale entertainment and sporting facilities . These structural policy commitments are creating sustained demand for design, planning, and engineering services across emerging urban destinations.

This opportunity translates directly into tangible project pipelines, including hotels, entertainment venues, theme parks, mixed-use waterfront developments, and major sports facilities. Large-scale initiatives such as NEOM, Qiddiya, and Red Sea Global require multidisciplinary architectural design, environmental engineering, and public realm planning prior to construction mobilization. As visitor capacity expands, supporting infrastructure including airports, transport corridors, and utilities must also be engineered and upgraded. This cascading effect multiplies project assignments across commercial, institutional, and infrastructure end-user segments.

The opportunity is particularly advantageous for new and smaller players due to the breadth and geographic spread of tourism-related projects. Unlike core oil and industrial projects dominated by established incumbents, hospitality, sports, and entertainment developments often involve modular, phased construction models that allow specialized firms to compete. Public–private partnerships and regional supplier forums further encourage participation from emerging engineering and design firms. Consequently, tourism infrastructure expansion offers scalable entry pathways with diversified revenue potential across Saudi Arabia’s evolving A&E landscape.

Saudi Arabia Architectural and Engineering Services Market Challenge:

Shortage of Experienced Engineering Professionals

The shortage of experienced engineering professionals represents the most critical structural constraint in Saudi Arabia’s Architectural and Engineering Services market. Rapid acceleration of Vision 2030 giga-projects has significantly increased demand for multidisciplinary engineers specializing in structural systems, MEP integration, digital modeling, and sustainability compliance. According to the Saudi Ministry of Human Resources and Social Development, workforce nationalization policies continue to reshape labor market participation across technical professions. While these initiatives aim to strengthen domestic capability, the pace of infrastructure execution has outstripped the immediate availability of highly specialized local talent.

This constraint is measurable through rising competition for certified engineers and delays in project mobilization reported across major developments. Large-scale projects such as NEOM and Red Sea Global require advanced digital engineering, environmental modeling, and complex systems integration, intensifying demand for globally experienced professionals. The requirement to comply with the Saudi Building Code and increasingly digitized tender documentation further narrows the pool of qualified practitioners. As a result, firms often rely on expatriate expertise, increasing recruitment costs and onboarding timelines.

The shortage materially restricts scalability by limiting the number of projects firms can simultaneously manage. New entrants face barriers in assembling accredited technical teams capable of meeting regulatory and digital competency standards. Extended hiring cycles and higher compensation expectations raise operational expenditure and compress margins. Consequently, talent constraints remain a structural bottleneck affecting long-term capacity expansion within Saudi Arabia’s A&E sector.

Saudi Arabia Architectural and Engineering Services Market (2026-32) Segmentation Analysis:

The Saudi Arabia Architectural and Engineering Services Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Service Type:

- Architectural Services

- Engineering Services

The Engineering Services segment dominates the Saudi Arabia Architectural and Engineering Services market with approximately 56% market share because it is structurally embedded in large-scale infrastructure, transport, and giga-project execution under Vision 2030. Projects such as NEOM, Red Sea Global, Diriyah, and major metro and airport expansions require intensive structural, civil, and MEP engineering prior to construction mobilization. According to the Saudi Ministry of Finance, sustained public capital expenditure toward infrastructure development in 2025 and 2026 continues to prioritize transport corridors, utilities, and industrial facilities. These project categories are engineering-intensive, generating higher billable technical hours compared to conceptual architectural design.

The dominance of engineering services is further supported by regulatory and technical compliance requirements under the Saudi Building Code. Large developments must meet strict structural safety, fire protection, energy efficiency, and environmental standards, all of which require detailed engineering calculations, system integration, and performance modeling. Additionally, digital modeling mandates and BIM-based coordination increase demand for structural and MEP engineers to ensure multidisciplinary integration. This compliance-driven complexity structurally expands engineering scope relative to standalone architectural planning.

Moreover, Saudi Arabia’s industrial localization programs and energy sector investments are driving demand for engineering design in manufacturing plants, logistics hubs, and utility infrastructure. Industrial and infrastructure projects typically allocate a greater proportion of pre-construction budgets to engineering feasibility, systems design, and technical documentation. Unlike architectural services, which are concentrated in building form and aesthetics, engineering services are required across transport, utilities, industrial, and institutional segments. This broad applicability, regulatory intensity, and higher technical workload collectively position engineering services as the leading service type in the Saudi market.

Based on End User:

- Residential

- Commercial

- Infrastructure

- Industrial

- Institutional

The Infrastructure segment dominates the Saudi Arabia Architectural and Engineering Services Market, with 32% market share, because it represents the most capital-intensive, technically complex, and engineering-dependent end-use category in the country. Infrastructure projects such as metro rail systems, airports, highways, power grids, water desalination plants, and digital backbone networks require extensive civil, structural, electrical, and mechanical engineering before construction begins. Unlike residential or commercial buildings, which emphasize architectural form and interior functionality, infrastructure projects are system-driven and engineering-led, making technical design structurally embedded within the project lifecycle.

Saudi Arabia’s national development strategy continues to prioritize transport corridors, logistics hubs, and utility modernization to support economic diversification. The Kingdom’s hotel market is set to add approximately 94,500 rooms to its development pipeline, significantly increasing demand for power distribution, water systems, transport connectivity, and utility engineering support . In parallel, the Ministry of Communications and Information Technology unveiled a National Data Center Strategy targeting up to 1.5 GW of data center capacity by 2030, reinforcing the need for high-load electrical systems, cooling infrastructure, and digital backbone engineering . These infrastructure-linked expansions generate higher engineering hours per project compared to standalone commercial developments.

Additionally, infrastructure functions as the foundational enabler for tourism, residential communities, industrial zones, and smart city developments. Airports support tourism growth, utilities enable housing expansion, and logistics corridors underpin industrial localization initiatives. Because other segments depend on infrastructure rollout, engineering demand originates first within infrastructure planning and system design. The combination of technical complexity, long development cycles, regulatory rigor, and multiplier effects across the broader economy positions infrastructure as the leading end-user segment in the Saudi Architectural and Engineering Services market.

Saudi Arabia Architectural and Engineering Services Market (2026-32): Regional Projection

Riyadh dominates the Saudi Arabia Architectural and Engineering Services Market, holding around 32% of total market size, because it functions as the Kingdom’s administrative, financial, and mega-project execution hub. As the national capital, Riyadh hosts the headquarters of key ministries, the Public Investment Fund (PIF), and major government agencies that oversee infrastructure and urban development programs. The concentration of public-sector decision-making accelerates project approvals, tender issuance, and consultancy contracts within the province . This institutional centralization structurally embeds higher volumes of architectural planning and engineering assignments in Riyadh compared to other provinces.

The province’s dominance is further reinforced by the scale of ongoing urban and mixed-use developments. Projects such as Diriyah Gate, King Salman Park, Riyadh Metro, and the New Murabba development require multidisciplinary engineering, transport integration, and advanced utility system design. Riyadh’s population exceeds 7 million residents, making it the most populous city in the Kingdom and driving sustained demand for residential communities, commercial districts, healthcare facilities, and transport upgrades. High project density and continuous expansion generate recurring design, supervision, and technical consultancy requirements.

Additionally, Riyadh benefits from its position as Saudi Arabia’s primary economic diversification center. The Regional Headquarters Program has encouraged multinational firms to establish offices in the capital, increasing demand for commercial real estate and corporate infrastructure. Major investments in data centers, logistics hubs, and government complexes further elevate engineering workload intensity. Unlike coastal provinces that are more sector-specific, Riyadh’s diversified development pipeline spans infrastructure, institutional, commercial, and smart-city projects. This combination of administrative concentration, project scale, demographic weight, and economic centrality positions Riyadh as the leading provincial contributor to the Saudi Architectural and Engineering Services market.

Gain a Competitive Edge with Our Saudi Arabia Architectural and Engineering Services Market Report:

- Saudi Arabia Architectural and Engineering Services Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Saudi Arabia Architectural and Engineering Services Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia Architectural and Engineering Services Market Policies, Regulations, and Product Standards

- Saudi Arabia Architectural and Engineering Services Market Trends & Developments

- Saudi Arabia Architectural and Engineering Services Market Dynamics

- Growth Factors

- Challenges

- Saudi Arabia Architectural and Engineering Services Market Hotspot & Opportunities

- Saudi Arabia Architectural and Engineering Services Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- Architectural Services

- Building design

- Urban planning

- Master planning

- Landscape architecture

- Interior architectural design

- Engineering Services

- Civil Engineering

- Structural Engineering

- Mechanical Engineering (HVAC)

- Electrical Engineering

- Plumbing & Fire Protection (MEP)

- Environmental Engineering

- Architectural Services

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Residential

- Commercial

- Infrastructure

- Industrial

- Institutional

- By Province - Market Size & Forecast 2022-2032, USD Million

- Riyadh

- Makkah

- Eastern Province

- Madinah

- Tabuk

- Asir

- Qassim

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Architectural Services Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Province - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Engineering Services Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Province - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Architectural and Engineering Services Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- AECOM

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Jacobs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- WSP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bechtel

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Parsons Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AtkinsRéalis

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Fluor Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HDR Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AECOM

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now