Qatar Healthcare Market Research Report: Growth Drivers & Forecast (2026-2032)

By Healthcare Expenditure Type (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), By Pharmaceutical Segment (Prescription Drugs, Over-the-C ... ounter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), By Therapeutic Area (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), By Medical Device Type (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), By Technology Type (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), By Healthcare Workforce (Physicians, Nurses, Dentists, Allied Health Professionals), By Insurance Type (Public Health Insurance, Private Health Insurance), By Disease Category (Chronic Diseases, Infectious Diseases, Mental Health Disorders), By End User (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) Read more

- Healthcare

- Mar 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Qatar Healthcare Market

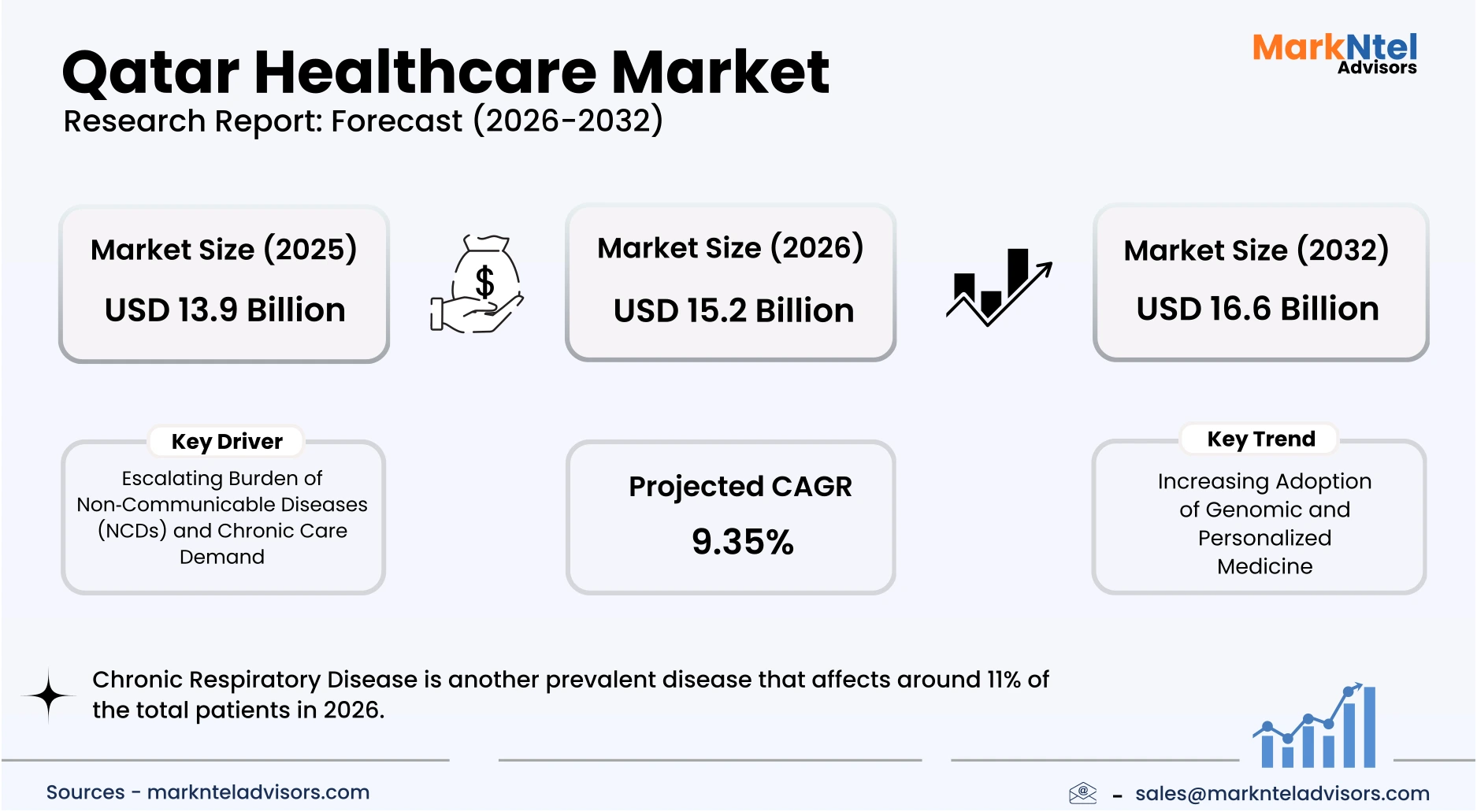

Projected 9.35% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 15.2 Billion

Market Size (2032)

USD 16.6 Billion

Base Year

2025

Projected CAGR

9.35%

Leading Segments

By Therapeutic Area: Cardiovascular Diseases

Qatar Healthcare Market Report Key Takeaways:

- The Qatar Healthcare Market size was valued at USD 13.9 billion in 2025 and is projected to grow from USD 15.2 billion in 2026 to USD 16.6 billion by 2032, exhibiting a CAGR of 9.35% during the forecast period.

- About 4.61% of the total patients in the Qatar healthcare system are affected by cardiovascular diseases,

- Chronic Respiratory Disease is another prevalent disease that affects around 11% of the total patients in 2026.

- Qatar’s healthcare system comprises approximately 29 hospitals, has a total bed capacity of over 5,000 beds, and is supported by more than 58,000 healthcare professionals, including physicians and nurses, highlighting the nation’s steadily expanding and well‑developed healthcare infrastructure.

Market Insights & Analysis: Qatar Healthcare Market (2026-32):

The Qatar Healthcare Market size was valued at USD 13.9 billion in 2025 and is projected to grow from USD 15.2 billion in 2026 to USD 16.6 billion by 2032, exhibiting a CAGR of 9.35% during the forecast period. i.e., 2026-32.

Qatar’s healthcare landscape has exhibited robust expansion, driven by government prioritization of accessible care, infrastructure scaling, and demographic changes. In the first half of 2025, the public flagship provider recorded over 1.35 million outpatient visits and 761,303 emergency visits, alongside 152,573 inpatient stays and 37,051 surgeries, indicating strong utilization across clinical services. Official data also show a modernized network of 12 public hospitals under Hamad Medical Corporation (HMC), including specialist and community centers, which collectively respond to rising demand across urban and regional catchments. Concurrently, primary care engagement via health centers continues to underpin routine, preventive, and chronic care delivery, reinforcing system-wide responsiveness to shifting population health needs.

Chronic disease burdens, particularly diabetes and associated risk factors, have significantly shaped healthcare utilization patterns. National estimates indicate over 400,000 adults living with diabetes, positioning Qatar among the countries with the highest diabetes preval ence globally, with nearly a quarter of adults affected. Cardiovascular diseases and cancers also contribute markedly to morbidity and service demand, with cancer incidence elevated across several major sites, necessitating advanced diagnostic and oncology services. These trends underscore the increasing weight of non-communicable diseases (NCDs) on clinical workloads and long-term care trajectories, intensifying requirements for specialist interventions and chronic disease management programmes.

Healthcare innovation and digital transformation have been catalyzed by national strategies, enhancing service delivery, efficiency, and patient access. Investments in telemedicine platforms, national electronic health records, and AI‑assisted diagnostics have expanded care reach and data‑driven clinical decision support. Strategic deployment of these technologies has improved continuity of care and operational agility, especially for remote consultations and chronic condition management, aligning with Qatar’s Vision 2030 objectives on sustainability and quality of care. Moreover, research partnerships and biomedical research initiatives have bolstered capabilities in precision medicine and chronic disease research, contributing to evidence‑informed policy and service evolution.

Government policy frameworks and regulatory actions have provided a foundation for sustained market growth. The National Health Strategy 2024–30 prioritizes clinical excellence, integrated service delivery, and preventive health, while significant budgetary allocations to healthcare have underpinned capital investments and workforce development. Regulatory emphasis on quality standards, digital integration, and international accreditation has elevated system performance benchmarks and incentivized private sector participation, shaping an enabling ecosystem for market expansion and heightened demand across residential, institutional, and specialized care segments.

Qatar Healthcare Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Expenditure Type | (Public Healthcare Expenditure, Private Healthcare Expenditure, Out-of-Pocket Expenditure), |

| By Pharmaceutical Segment | (Prescription Drugs, Over-the-Counter (OTC) Drugs, Generic Drugs, Branded Drugs, Biologics & Biosimilars), |

| By Therapeutic Area | (Cardiovascular Diseases, Oncology, Diabetes, Respiratory Diseases, Neurology, Infectious Diseases, Others), |

| By Medical Device Type | (Diagnostic Imaging Devices, Patient Monitoring Devices, Surgical Equipment, In-vitro Diagnostics, Orthopedic Devices, Cardiovascular Devices, Others), |

| By Technology Type | (Artificial Intelligence in Healthcare, Telemedicine & Remote Monitoring, Electronic Health Records (EHR), Healthcare Analytics, Robotic Surgery, Wearables & Health Apps), |

| By Healthcare Workforce | (Physicians, Nurses, Dentists, Allied Health Professionals), |

| By Insurance Type | (Public Health Insurance, Private Health Insurance), |

| By Disease Category | (Chronic Diseases, Infectious Diseases, Mental Health Disorders), |

| By End User | (Hospitals, Clinics, Diagnostic Centers / Laboratories, Ambulatory Surgical Centers, Home Healthcare, Research Institutes, Pharmacies, Others) |

Qatar Healthcare Market Driver:

Escalating Burden of Non‑Communicable Diseases (NCDs) and Chronic Care Demand

The most influential driver expanding Qatar’s healthcare market is the rapidly rising burden of non‑communicable diseases (NCDs), notably cardiovascular conditions, diabetes, cancers, and chronic respiratory illnesses, exerting a structural and sustained increase in healthcare demand. According to the World Health Organization (WHO) Eastern Mediterranean Office, NCDs account for approximately 72% of all deaths in Qatar, driven by lifestyle changes, urbanization, and sedentary behavior, which have intensified the prevalence of obesity and hypertension in adults. This systemic health transition has compelled expanded service provision across all levels of care, generating recurring demand across preventive, diagnostic, therapeutic, and long‑term management segments.

The intensification of NCD prevalence has directly translated into measurable service utilization and capacity expansions, reflecting elevated demand volumes rather than temporary shifts. Publicly reported figures from Hamad Medical Corporation show millions of outpatient visits and hundreds of thousands of emergency department encounters, indicating broad service uptake aligned with chronic disease care needs and general population growth . This sustained burden encourages deployment of chronic disease monitoring programmes, specialized clinics, and integrated care pathways that collectively expand system throughput year over year. The linkage between NCD prevalence and expanded healthcare utilization demonstrates that demand generation is structural, affecting multiple end‑user segments, including residential populations requiring ongoing management and institutional users supporting advanced treatment modalities.

Government policy responses further expand market size by embedding long-term NCD control and chronic care within national planning frameworks rather than through episodic initiatives. Qatar’s National Health Strategy 2024–2030 and broader development programs prioritise prevention, early detection, and patient‑centered management of chronic conditions, mandating expanded primary care services, enhanced screening, and community outreach. These regulatory imperatives strengthen systemic capacity and scale of services, increasing healthcare consumption across public and private segments and sustaining long‑term demand volumes.

Qatar Healthcare Market Trend:

Increasing Adoption of Genomic and Personalized Medicine

Qatar’s healthcare sector is witnessing a structural shift toward genomic medicine and personalized healthcare solutions, driven by the Qatar Genome Programme (QGP) and national precision medicine initiatives. QGP has mapped the genomes of over 30,000 residents by 2025, enabling disease-risk profiling, early diagnosis, and individualized treatment plans. This focus on genomics has accelerated in recent y ears due to the rising prevalence of genetic disorders and chronic diseases, prompting systematic integration of genomic data into public health strategies and hospital protocols.

The trend is reshaping healthcare delivery and operational models by promoting targeted therapies, pharmacogenomics, and predictive diagnostics, reducing reliance on generalized treatment approaches. Hospitals and research institutions are increasingly collaborating to develop patient-specific care pathways, while end-users, including residential patients and institutional programs, benefit from enhanced preventive care and reduced incidence of adverse drug reactions. For example, Hamad Medical Corporation (HMC) introduced Whole Exome Sequencing (WES) testing in September 2025, enabling advanced genetic diagnostics and personalized treatment planning within Qatar’s public health system, eliminating the need to send samples abroad. Sidra Medicine has implemented clinical‑grade Whole Genome Sequencing (WGS) for patients, transforming pediatric and rare disease diagnostics and supporting personalized approaches to care locally.

This structural shift is expected to persist because Qatar’s long-term health strategy prioritizes precision medicine, innovation, and research-driven care. Continued investment in genomic infrastructure, training of specialized personnel, and integration of AI analytics for genomics ensures sustainable adoption. For example, the Precision Medicine & Functional Genomics (PMFG) Summit 2025 showcased the adoption of AI and long‑read sequencing technologies and emphasized translating genomic science into clinical practice and diagnostics, reinforcing the sustained evolution of precision medicine in the health system. Personalized medicine not only enhances clinical outcomes but also strengthens the country’s position as a regional hub for advanced healthcare services, fundamentally influencing healthcare market growth, technology deployment, and service design in the medium to long term.

Qatar Healthcare Market Opportunity:

Expansion of Health‑Tech Innovation and Digital Health Solutions

Qatar’s healthcare market presents a compelling opportunity for new entrants in digital health technology, health‑tech platforms, and e‑health solutions due to recent regulatory enhancements and structured support for innovation. The government, as part of the National Health Strategy 2024–2030, has prioritized digital transformation, interoperability, and technology‑enabled care delivery, creating an environment conducive to scalable, technology‑led healthcare offerings. This digital push aligns with broader national goals to improve service efficiency, patient outcomes, and integration of advanced clinical tools across care settings.

This opportunity translates into tangible demand because healthcare institutions and stakeholders are actively adopting AI, telemedicine, and integrated digital platforms to support remote monitoring, patient engagement, and data management. Events like Qatar Medicare 2025 and strategic partnerships between healthcare providers and venture capital firms signal structured market openings for health‑tech innovations, showcasing demand for solutions such as digital triage, patient‑centric apps, and analytics‑driven care tools. These initiatives reinforce ecosystem readiness for new digital entrants and create measurable routes to market validation, pilot scaling, and institutional procurement.

For new and smaller players, this opportunity is particularly advantageous because established incumbents face higher operational inertia and legacy system constraints, while agile digital innovators can leverage supportive partnerships, pilot programs, and interoperability initiatives to differentiate offerings. Frameworks encouraging public‑private collaboration and national exhibitions facilitate early adoption, knowledge exchange, and access to clinical validation partnerships. For example, in August 2025, Ooredoo Qatar, a major telecommunications provider, signed a strategic Memorandum of Understanding (MoU) with The View Hospital to advance integrated, technology‑driven healthcare solutions in Qatar. This partnership is designed to use Ooredoo’s IT infrastructure, cloud services, and digital capabilities to support healthcare access, digital platforms, and innovation initiatives, including expanded diagnostic and preventive services as well as telehealth‑enabled care pathways.

Qatar Healthcare Market Challenge:

Regulatory Barriers for Private Digital Health Startups

A key structural challenge limiting growth for new entrants in Qatar’s healthcare industry is the complex regulatory environment for private digital health providers, including telemedicine, AI-enabled diagnostics, and health apps. The Ministry of Public Health (MoPH) licensing framework requires startups to comply with multiple layers of approval covering facility registration, digital platform security, patient data management, and professional accreditation, often taking up to 90 days or more for full authorization.

These regulatory requirements directly affect operational scalability and market entry. Startups face high compliance costs, mandatory cybersecurity protocols, and data privacy audits, which can divert resources from product development or delay go-to-market strategies. For example, AI diagnostic platforms must undergo separate evaluation for clinical efficacy and safety before integration into hospital workflows, limiting rapid adoption by institutions and end-users.

This structural challenge materially restricts the expansion of digital health solutions by raising entry barriers, increasing time-to-market, and reducing operational flexibility for smaller or emerging players. While large incumbents can absorb compliance costs, startups may struggle to secure approvals and partnerships, slowing innovation deployment. As a result, the regulatory environment acts as a critical bottleneck, impacting the adoption rates of advanced digital healthcare technologies and the overall growth trajectory of Qatar’s digital health ecosystem.

Qatar Healthcare Market Epidemiology Profile:

Chronic Respiratory Diseases:

Chronic respiratory diseases, including chronic obstructive pulmonary disease (COPD), asthma, and bronchitis, represent a growing public health concern in Qatar, affecting around 11% of the total patients. Rapid urbanization, high prevalence of smoking among adults, and environmental factors such as dust storms and air pollution contribute to rising incidence and exacerbations. The Ministry of Public Health has introduced targeted awareness programs and early diagnostic initiatives, increased detection, and reinforced healthcare engagement across both primary and tertiary care facilities.

Investment in specialized respiratory care units and pulmonology clinics has expanded treatment capacity, with modern interventions such as spirometry testing, inhalation therapy, and home-based monitoring devices enhancing patient management. In Qatar, chronic respiratory diseases such as asthma and chronic obstructive pulmonary disease (COPD) are managed through a comprehensive clinical approach that integrates advanced diagnostics, personalized therapies, and long‑term self‑management support. Primary care providers and specialized pulmonology clinics are the front line for diagnosis and ongoing treatment of respiratory conditions, with emphasis on tailored care plans and monitoring. At the tertiary care level, Hamad Medical Corporation (HMC), the country’s principal public healthcare provider, has adopted state‑of‑the‑art treatment protocols for asthma, incorporating advanced biologic therapies for severe cases, smart inhalers, digital symptom‑monitoring tools, and structured self‑ management education for patients.

The dominance of chronic respiratory diseases in Qatar is sustained by the intersection of environmental risk factors, rising prevalence, continuous policy and awareness initiatives, and significant infrastructure investment. The combination of high patient demand, long-term care requirements, and specialized treatment availability ensures that CRD remains a critical segment in the healthcare landscape, influencing resource allocation, clinical service planning, and technology adoption through 2032.

Cardiovascular Diseases:

Cardiovascular diseases represent the most dominant chronic disease segment in Qatar, largely due to their high prevalence and substantial contribution to overall mortality. Epidemiological studies indicate that 4.61% of the country’s total patients is living with some form of cardiovascular condition, including coronary artery disease, hypertension-related heart disorders, and heart failure. Rapid urbanization, sedentary lifestyles, and high rates of obesity and metabolic risk factors have contributed to rising incidence levels. National screening initiatives led by Qatar’s health authorities have expanded early detection, increasing the number of diagnosed patients seeking regular cardiovascular monitoring and treatment services.

Government policy and institutional investment further reinforce the segment’s leadership within the healthcare system. Qatar’s National Health Strategy and non-communicable disease prevention programs emphasize cardiovascular risk reduction through large-scale screening, early intervention, and integrated disease management. Public healthcare providers and private hospitals have responded with significant investments in advanced cardiology infrastructure, including specialized cardiac centers, catheterization laboratories, and digital diagnostic technologies. For example, A leading private healthcare provider that introduced Transcatheter Aortic Valve Implantation (TAVI), a minimally invasive treatment for severe aortic stenosis, is demonstrating the adoption of advanced structural heart interventions in Qatar’s private sector .

Strong end-user demand continues to sustain the dominance of cardiovascular care across the healthcare ecosystem. Patients require frequent clinical consultations, diagnostic imaging, and long-term pharmacological management, creating continuous utilization of hospital and outpatient services. Insurance coverage expansion and government-funded treatment programs further support patient access to cardiac services. The combined effect of high disease burden, supportive public health policy, sustained infrastructure investment, and long-term patient management requirements ensures that cardiovascular diseases remain the leading epidemiological segment shaping healthcare demand in Qatar through 2032.

Gain a Competitive Edge with Our Qatar Healthcare Market Report:

- The Qatar Healthcare Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competition, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Qatar Healthcare Market Landscape Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Introduction

- Executive Summary

- Key Insights

- Key Findings (2020–2024)

- Market Outlook Snapshot (2025–2032F)

- Strategic Imperatives

- Macro Environment Analysis

- Qatar at a Glance

- Geographic Overview

- Political Structure

- Trade & Regional Alliances

- Others

- Demographic Profile (2020–2032F)

- Population Trends

- Age Structure

- Urban vs Rural Distribution

- Fertility Rate Trends

- Migration Trends

- Ethnic Composition

- Economic Profile (2020–2032F)

- GDP (Current & Constant USD)

- GDP by Sector

- Working Population & Labor Participation

- Per Capita Income & Purchasing Power

- Unemployment & Underemployment

- Inflation Rate & Healthcare Cost Impact

- Foreign Direct Investment Trends

- Country PESTLE Analysis

- Qatar at a Glance

- Qatar Healthcare Sector Analysis, 2026

- Healthcare System Overview

- Structure of Healthcare System

- Public vs Private Healthcare

- Governance & Regulatory Authorities

- Others

- Healthcare Ecosystem & Infrastructure (2020–2026)

- Healthcare Expenditure

- Healthcare Expenditure as % of GDP

- Per Capita Healthcare Expenditure

- Healthcare Facilities

- Number of Hospitals

- Number of Clinics

- Number of Pharmacies

- Number of Diagnostic Centres

- Public vs Private Distribution

- Bed Availability & Utilization

- Beds per 1,000 Population

- Beds Specialty

- Regional Disparities

- Healthcare Workforce

- Physicians per 1,000 Population

- Physicians by Specialty

- Nurses

- Dentists

- Allied Health Professionals

- Healthcare Expenditure

- Healthcare System Overview

- Health Outcomes & Public Health Indicators (2020–2026)

- Life Expectancy (Male vs Female)

- Infant Mortality Rate

- Maternal Mortality Ratio

- Immunization Coverage Rates (Measles, DPT, HPV, COVID-19)

- Overall Disease Burden Trends

- Healthcare Reforms & Large-Scale Projects (2020-2026)

- Government Reforms

- Public-Private Partnerships

- Infrastructure Expansion Projects

- Private Sector Investments

- Others

- Insurance Framework

- Public Health Insurance Programs

- Private Health Insurance Market

- Insurance Penetration & Coverage Gaps

- Payer Landscape

- Reimbursement Models (FFS, Bundled, Value-Based Care)

- Claims Management & Transparency Issues

- Out-of-Pocket Expenditure Trends (2020-2026)

- Regulatory Environment (Healthcare Sector)

- Market Authorisation for Pharmaceuticals

- Market Authorisation for Medical Devices

- Licensing for Manufacturing, Import & Export

- Clinical Trial Regulations

- Intellectual Property & Patent Protection

- Advertising, Labeling & Packaging Regulations

- Pharmacy & Hospital Licensing Rules

- Others

- Market Dynamics & Technology

- Healthcare Market Dynamics

- Growth Drivers

- Challenges & Barriers

- Emerging Opportunities

- Value Chain Analysis

- Healthcare Technology Trends

- Digital Health Maturity

- Telemedicine & Remote Monitoring

- Artificial Intelligence & Machine Learning

- Health Apps & Wearables

- Robotic Surgery

- EHR, Data Interoperability & Cybersecurity

- Others

- Healthcare Market Dynamics

- Epidemiology Profile (By Age & By Gender) (2020–2032F)

- Chronic Diseases

- Cardiovascular Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Diabetes

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cancer

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Respiratory Diseases

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Chronic Kidney Disease

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Cardiovascular Diseases

- Infectious Diseases

- Tuberculosis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- HIV

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Hepatitis

- Prevalence

- Incidence

- Mortality Rate

- Risk Factors

- Healthcare & Economic Burden

- Infrastructure Challenges

- Treatment Landscape

- Others

- Others

- Tuberculosis

- Mental Health

- Prevalence of Mental Health Disorders

- Suicide Rates & Trends

- Urban-Rural & Gender Disparities

- Infrastructure Gaps

- Economic & Social Burden

- Chronic Diseases

- Qatar Healthcare System Stakeholders Analysis, 2026

- Qatar Pharmaceutical Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- Prescription vs OTC

- Generics vs Branded

- Therapeutic Category Distribution

- Manufacturing Landscape

- Distribution & Supply Chain

- Major Distributors

- Major Suppliers

- Major Local and Multinational Players

- Pharmaceutical sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Pharmaceutical Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- Qatar Medical Devices Market Outlook (2020–2030F)

- Market Size & Growth

- Market Size (USD Million), 2020-2030F

- Market by Key Segments

- By Device Type

- By Risk Class

- By End-User

- Manufacturing Landscape

- Distribution & Supply Chain

- Distributors

- Supply Chain

- Major Local and Multinational Players

- Medical Devices Sector (Top 5–10 companies, % market share)

- Imports & Exports (Value in USD Million) (2020-2026)

- Key Medical Device Clusters (if there)

- Investments and R&D (2020-2026)

- Others

- Market Size & Growth

- Qatar Pharmaceutical Market Outlook (2020–2030F)

- Qatar Strategic & Investments in Healthcare Outlook (2025-2032F)

- High-Growth Segments

- Foreign Investment Opportunities

- Government Incentives & Ease of Doing Business

- Risk Assessment & Mitigation

- Trade Associations & Industry Bodies

- Pharmaceutical Associations

- Medical Device Associations

- Healthcare Provider Associations

- Regulatory & Standards Bodies

- Healthcare Trade Fairs & Conferences (2024–2026)

- National Healthcare Exhibitions

- Medical Technology Events

- Pharmaceutical Conferences

- Regional Latin America Events Relevant to Qatar

- Impact of Global Health Events

- COVID-19 Impact (2020–2022)

- Post-Pandemic Recovery

- Emergency Preparedness Evolution

- Strategic Recommendations

- Market Entry Strategy

- Partnership Models

- Pricing Strategy

- Regulatory Navigation

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now