Global Next Generation Infantry Rifles Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Weapon Type (Assault Rifles, Battle Rifles, Automatic Rifles / Infantry Automatic Rifles (IAR), Carbines (compact modular rifles), Designated Marksman Rifles (DMR) / Precision I ... nfantry Rifles), By Caliber Type (Multi-caliber / Convertible Systems), By Operating Mechanism (Gas-operated rifles, Short-stroke piston rifles, Hybrid recoil mitigation systems, Suppressor-optimized weapon systems), By End User (Military Infantry Forces, Special Operations Forces, Homeland Security / Law Enforcement, Reserve / National Guard modernization), and others Read more

- Aerospace & Defense

- Feb 2026

- Pages 195

- Report Format: PDF, Excel, PPT

Global Next Generation Infantry Rifles Market

Projected 8.63% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 1.63 Billion

Market Size (2032)

USD 2.91 Billion

Largest Region

North America

Projected CAGR

8.63%

Leading Segments

By End User: Military Infantry Forces

Global Next Generation Infantry Rifles Market Report Key Takeaways:

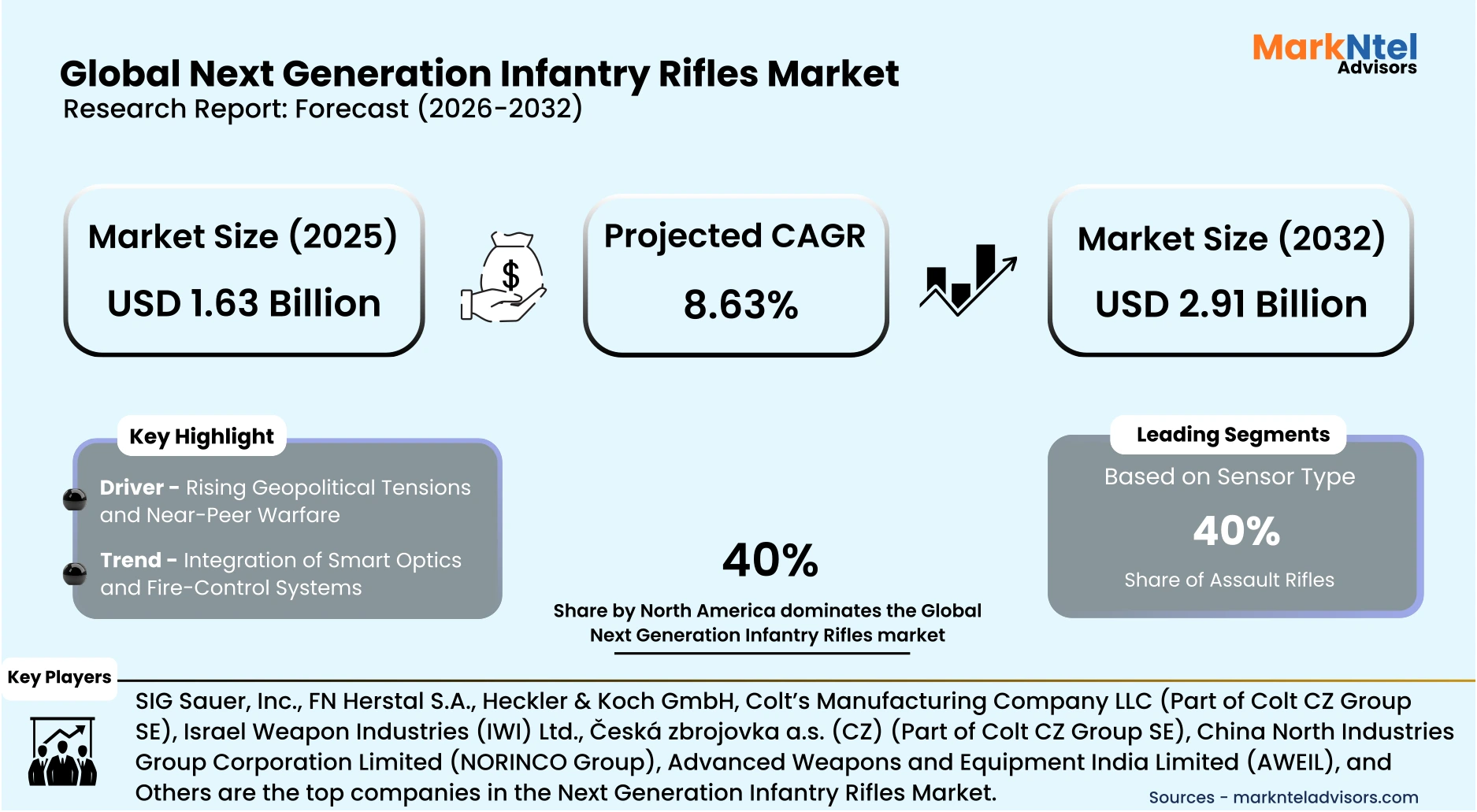

- Market size was valued at around USD 1.63 billion in 2025 and is projected to reach USD 2.91 billion by 2032. The estimated CAGR from 2026 to 2032 is around 8.63%, indicating strong growth.

- North America holds the largest market share of about 40% in the Global Next Generation Infantry Rifles Market in 2025.

- By weapon type, the assault rifles segment represented a significant share of about 40% in the Global Next Generation Infantry Rifles Market in 2025.

- By end user, the military infantry forces segment presented a significant share of about 65% in the Global Next Generation Infantry Rifles Market in 2025.

- Leading next generation infantry rifles companies in the Global Market are SIG Sauer, Inc., FN Herstal S.A., Heckler & Koch GmbH, Colt’s Manufacturing Company LLC (Part of Colt CZ Group SE), Israel Weapon Industries (IWI) Ltd., Rheinmetall AG, General Dynamics Corporation, Beretta Holding S.p.A., Daniel Defense, Inc., Kalashnikov Concern JSC, ST Engineering Land Systems Ltd. (ST Engineering Group), Barrett Firearms Manufacturing, Inc., Česká zbrojovka a.s. (CZ) (Part of Colt CZ Group SE), China North Industries Group Corporation Limited (NORINCO Group), Advanced Weapons and Equipment India Limited (AWEIL), and Others.

Market Insights & Analysis: Global Next Generation Infantry Rifles Market (2026-32):

The Global Next Generation Infantry Rifles Market size was valued at around USD 1.63 billion in 2025 and is projected to reach USD 2.91 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 8.63% during the forecast period, i.e., 2026-32.

The Global Next Generation Infantry Rifles Market is projected to expand steadily, driven by rising geopolitical tensions, near-peer warfare preparedness, and the growing integration of smart optics and advanced fire-control systems.

One of the most significant indicators of long-term demand is NATO’s growing defense spending. According to SIPRI, NATO members collectively spent USD 1.506 trillion in 2024, accounting for 55% of global military expenditure. Defense spending across the alliance rose 8.9% in one year, while 18 of 32 NATO countries met the 2% of GDP defense spending target in 2024, up from 11 in 2023. This shift reflects a major transition toward readiness for large-scale conflict and sustained modernization of ground forces .

The United States continues to prioritize near-peer competition. In 2024, the country allocated USD 246 billion to strengthen deterrence worldwide, including USD 48.4 billion for Ukraine, USD 10.6 billion for Israel, and USD 2.6 billion for Indo-Pacific security and support for Taiwan.

Meanwhile, China is also expanding its military capabilities, with defense spending reaching USD 314 billion in 2024, marking the 30th consecutive year of growth and reinforcing modernization plans through 2035 .

These strategic shifts are translating into direct investment in next-generation infantry weapons. The U.S. Army significantly increased funding for the Next Generation Squad Weapon (NGSW) program, raising its 2025 budget from USD 132.9 million to USD 367.3 million. This funding includes procurement of 39,836 rifles and fire-control systems, reflecting the rapid transition toward new weapon platforms.

The US Army has also awarded a 10-year production contract for the M7 rifle and XM250 automatic rifle, designed to replace legacy M4/M4A1 and M249 systems. These weapons use new 6.8 mm ammunition, developed to enhance lethality and accuracy against advanced threats. Parallel modernization efforts are integrating smart optics, networked targeting, and battlefield connectivity to improve survivability and situational awareness.

Long-term global investments further reinforce the market outlook beyond 2025. For instance, India signed a USD 600 million agreement to manufacture over 610,000 AK-203 rifles, with deliveries continuing through 2026 and beyond, driven by tensions with China and Pakistan.

Germany plans USD 28.7 billion in spending through the 2030s for soldier equipment and force expansion from 280,000 to 460,000 personnel. Meanwhile, Lithuania plans to increase defense spending to 5–6% of GDP from 2026 , while Poland intends to allocate USD 55 billion to defense in 2026, representing 4.8% of GDP.

Sustained military spending, modernization programs, and long-term geopolitical competition are creating a strong growth trajectory for next-generation infantry rifles. Continuous investments in soldier lethality and coalition readiness will drive sustained procurement and technology upgrades across global armed forces.

The integration of Smart Optics and Fire-Control Systems trend will increase the market demand. For example, the U.S. Department of Defense has emphasized digitized soldier lethality within modernization priorities, focusing on integrating weapons into broader battlefield networks. The Army has stated that NGSW technologies are intended to provide improved accuracy, survivability, and situational awareness for future combat scenarios. European and NATO forces are pursuing comparable upgrades, prioritizing optics with thermal imaging, augmented reality overlays, and battlefield connectivity to support multi-domain operations.

Global Next Generation Infantry Rifles Market Recent Developments:

- 2025: India’s Ministry of Defence awarded PLR Systems a contract worth about USD 133 million to supply 170,000 Close Quarter Battle carbines as part of a larger USD 332 million procurement for over 425,000 units. Deliveries begin in 2026 to replace legacy sub-machine guns and strengthen infantry modernization and domestic manufacturing capabilities.

- 2025: The UK Ministry of Defence has advanced Project Grayburn, a long-term programme to replace the SA80 rifle, focusing on domestic production, multiple variants, and improved capability against modern body armour. The initiative remains in the concept phase, with industry engagement planned before procurement decisions.

Global Next Generation Infantry Rifles Market Scope:

| Category | Segments |

|---|---|

| By Weapon Type | (Assault Rifles, Battle Rifles, Automatic Rifles / Infantry Automatic Rifles (IAR), Carbines (compact modular rifles), Designated Marksman Rifles (DMR) / Precision Infantry Rifles), |

| By Caliber Type | (Multi-caliber / Convertible Systems), |

| By Operating Mechanism | (Gas-operated rifles, Short-stroke piston rifles, Hybrid recoil mitigation systems, Suppressor-optimized weapon systems), |

| By End User | (Military Infantry Forces, Special Operations Forces, Homeland Security / Law Enforcement, Reserve / National Guard modernization), |

Global Next Generation Infantry Rifles Market Driver:

Rising Geopolitical Tensions and Near-Peer Warfare

Escalating geopolitical tensions and the return of near-peer conflict are accelerating military modernization programs worldwide, directly increasing demand for next-generation infantry rifles. Governments are prioritizing stronger ground forces, modern soldier equipment, and improved battlefield lethality to address evolving security threats.

According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached USD 2.718 trillion in 2024, representing a 9.4% year-on-year increase and the fastest growth rate since the Cold War. Military spending has now risen for 10 consecutive years and expanded by 37%, reflecting a sustained shift toward long-term defense preparedness and modernization.

Ongoing conflicts are a major catalyst for this spending surge. SIPRI reported that Israel’s military expenditure rose by 65% in 2024, while Russia’s increased by 38%, highlighting how active conflict environments rapidly drive procurement of weapons and soldier systems . Such increases typically translate into accelerated acquisition of small arms, ammunition, and advanced infantry equipment to sustain operational readiness.

Europe is also undergoing a significant rearmament cycle. Germany increased defense spending by 28% in 2024, supported by a USD 105 billion special military modernization fund, signaling sustained investment in force readiness and equipment upgrades. This modernization wave is expected to continue over the coming decade.

Sustained defense spending growth and ongoing conflicts are strengthening long-term procurement pipelines. This global rearmament trend will significantly accelerate demand for next-generation infantry rifles and associated soldier systems.

Global Next Generation Infantry Rifles Market Trend:

Integration of Smart Optics and Fire-Control Systems

Infantry modernization programs are increasingly transforming rifles into digitally enhanced precision platforms by integrating networked optics, ballistic computers, sensors, and advanced fire-control technologies.

This shift is driven by the need to improve lethality, situational awareness, and engagement accuracy in complex and long-range combat environments. Modern combat scenarios, particularly urban warfare and low-visibility operations, are accelerating the adoption of intelligent targeting solutions that reduce soldier workload while improving hit probability.

A leading example of this trend is the U.S. Army’s Next Generation Squad Weapon (NGSW) program, which incorporates the XM157 Fire Control System developed by Vortex Optics and Sheltered Wings. The U.S. Army awarded a contract valued at up to USD 2.7 billion to supply advanced fire-control optics for the XM7 rifle and XM250 automatic rifle.

The XM157 integrates multiple technologies into a single optic, including a laser rangefinder, ballistic calculator, environmental sensors, compass, and a digital display. These features enable soldiers to rapidly calculate firing solutions, accurately engage targets at extended ranges, and maintain effectiveness in low-visibility conditions.

The integration of these systems highlights the broader shift toward digitally connected soldier ecosystems, where weapons, sensors, and targeting systems operate as a unified combat network. As militaries prioritize higher precision and faster decision-making, the demand for rifles equipped with advanced fire-control optics is expected to rise significantly.

Smart optics are redefining infantry weapons as precision, network-enabled systems. Continued investments in digitally enhanced targeting will strongly accelerate the adoption of next-generation infantry rifles worldwide.

Global Next Generation Infantry Rifles Market Opportunity:

Interoperability & Joint Procurement Programs

Multinational defense cooperation is creating a major opportunity for next-generation infantry rifle adoption, as governments increasingly prioritize interoperability and pooled procurement to strengthen coalition readiness and reduce costs.

In 2024, the NATO Support and Procurement Agency (NSPA) signed two multinational framework contracts worth USD 1.2 billion for artillery ammunition on behalf of multiple allied nations, highlighting the rapid expansion of shared procurement frameworks across the alliance. These initiatives are designed to accelerate standardization and strengthen joint logistics, a model now expanding to small arms, optics, and soldier systems.

The European Union’s Act in Support of Ammunition Production (ASAP) further reinforces this shift by mobilizing USD 540 million to expand collaborative defense manufacturing and reduce fragmentation in procurement across member states. The program focuses on shared supply chains and joint acquisition of standardized equipment, which supports long-term adoption of common calibers and next-generation weapon platforms.

NATO’s Defense Production Action Plan also promotes multinational acquisition and industrial cooperation to increase defense production capacity and interoperability across member states. These frameworks are expected to extend beyond ammunition into broader soldier modernization programs.

Joint procurement reduces costs, ensures interoperability, and accelerates modernization across allied forces. As coalition warfare becomes central to defense strategy, multinational acquisition frameworks will significantly boost global demand for next-generation infantry rifles.

Global Next Generation Infantry Rifles Market Challenge:

Regulatory and Export Restrictions

Strict export controls and arms-transfer regulations continue to limit the global expansion of next-generation infantry rifles. The United States’ International Traffic in Arms Regulations (ITAR) governs exports of military firearms, optics, and fire-control technologies, requiring extensive licensing and end-user verification.

In 2024, the U.S. government imposed a policy of denial on defense exports to Nicaragua, restricting sales and brokering of controlled defense articles except for limited humanitarian uses. Such policy actions demonstrate how geopolitical considerations can rapidly close international markets for defense manufacturers and delay ongoing procurement opportunities.

European regulations also illustrate the commercial impact of licensing and political oversight. Switzerland’s State Secretariat for Economic Affairs reported that war-materiel exports declined to approximately USD 790 million in 2023, reflecting tighter export approvals and policy constraints affecting defense trade .

Export controls are increasingly used as geopolitical tools to restrict access to sensitive defense technologies and protect national security. As a result, manufacturers face higher compliance costs, longer approval timelines, and reduced access to certain markets.

Overall, complex export regulations and licensing barriers slow international sales and limit cross-border partnerships. These restrictions can significantly hinder the pace of global adoption and expansion of next-generation infantry rifle programs.

Global Next Generation Infantry Rifles Market (2026-32) Segmentation Analysis:

The Global Next Generation Infantry Rifles Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the global level. Based on the analysis, the market has been further classified as;

Based on Weapon Type:

- Assault Rifles

- Battle Rifles

- Automatic Rifles / Infantry Automatic Rifles (IAR)

- Carbines (compact modular rifles)

- Designated Marksman Rifles (DMR) / Precision Infantry Rifles

The assault rifles segment dominates the Global Next Generation Infantry Rifles Market, holding around 40% market share, due to their central role as the standard-issue firearm for modern infantry forces.

These platforms provide an optimal balance between firepower, accuracy, weight, and operational flexibility, enabling effective performance across diverse combat environments, including urban warfare, counterinsurgency, and conventional battlefield engagements. Their selective-fire functionality allows soldiers to transition seamlessly between semi-automatic precision shooting and automatic suppressive fire, which remains critical for modern combined-arms operations.

Ongoing military modernization programs across North America, Europe, and Asia-Pacific are heavily focused on replacing legacy assault rifles with advanced, modular systems designed for enhanced lethality and survivability.

Next-generation assault rifles are increasingly chambered in improved intermediate calibers that offer extended effective range, superior penetration against modern body armor, and improved ballistic performance without significantly increasing recoil or soldier fatigue.

In addition, assault rifles account for the highest procurement volumes among infantry weapons because they are issued to the majority of frontline personnel. Large-scale replacement initiatives, combined with integration of suppressors, advanced optics, and digital fire-control systems, continue to reinforce their strategic importance.

Consequently, widespread deployment, modernization investments, and their indispensable role in standard infantry operations firmly establish assault rifles as the leading segment within the next-generation infantry rifles market.

Based on End User:

- Military Infantry Forces

- Special Operations Forces

- Homeland Security / Law Enforcement

- Reserve / National Guard modernization

The military infantry forces segment dominates the Global Next Generation Infantry Rifles Market, accounting for about 65% of total market size, due to their central role in land-based combat and the scale of global soldier modernization programs.

Governments are prioritizing the upgrade of standard-issue service rifles as a foundational element of broader military transformation initiatives focused on improving lethality, survivability, and interoperability in high-intensity conflict scenarios. Compared with specialized units, conventional infantry formations represent the largest troop segment, which translates into high-volume, long-term procurement cycles for primary weapons and associated systems.

Many defense ministries are systematically replacing legacy assault rifles with advanced platforms designed to deliver extended range, enhanced accuracy, reduced recoil, and improved ergonomics. These programs often involve multi-year acquisition plans covering hundreds of thousands of weapons, along with integrated optics, suppressors, and digital fire-control technologies.

In addition, the shift toward near-peer warfare and multi-domain operations has reinforced the need for highly capable infantry units equipped for diverse and technologically complex battlefields. Modern service rifles are increasingly viewed as force multipliers that improve squad-level effectiveness and overall combat readiness.

Consequently, the combination of large personnel numbers, continuous replacement of aging inventories, and sustained government funding ensures that military infantry forces remain the dominant end-user segment in the global next-generation infantry rifles market.

Global Next Generation Infantry Rifles Market (2026-32): Regional Projection

North America dominates the Global Next Generation Infantry Rifles market with an estimated 40% share, due to sustained modernization programs, strong procurement pipelines, and the presence of an advanced and vertically integrated defense industrial ecosystem.

The United States is the primary contributor, supported by long-term force modernization strategies focused on replacing legacy small arms with modular, digitally enabled rifle platforms designed for improved lethality, survivability, and interoperability in multi-domain operations.

The region benefits from well-established collaboration between defense agencies, prime contractors, optics developers, ammunition manufacturers, and research institutions. This integrated supply chain accelerates innovation cycles, enabling rapid prototyping, testing, and large-scale production of advanced rifle systems, ammunition, and fire-control technologies. Continuous investments in soldier lethality programs and network-enabled battlefield capabilities further reinforce procurement momentum across military and special operations forces.

Additionally, North America maintains strong export relationships and defense partnerships with allied nations, supporting production scale and global adoption of advanced infantry weapon platforms. Standardization initiatives and interoperability requirements within allied defense frameworks further strengthen regional leadership. Collectively, consistent defense funding, technological leadership, and a mature manufacturing base position North America as the most influential and technologically advanced regional market for next-generation infantry rifles.

Gain a Competitive Edge with Our Global Next Generation Infantry Rifles Market Report:

- Global Next Generation Infantry Rifles Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Global Next Generation Infantry Rifles Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Global Next Generation Infantry Rifles Market Policies, Regulations, and Product Standards

- Global Next Generation Infantry Rifles Market Trends & Developments

- Global Next Generation Infantry Rifles Market Dynamics

- Growth Factors

- Challenges

- Global Next Generation Infantry Rifles Market Hotspot & Opportunities

- Global Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- Assault Rifles

- Battle Rifles

- Automatic Rifles / Infantry Automatic Rifles (IAR)

- Carbines (compact modular rifles)

- Designated Marksman Rifles (DMR) / Precision Infantry Rifles

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- 5.56 mm Next-Gen Platforms

- 6.5 mm Intermediate Caliber

- 6.8 mm Advanced Caliber

- 7.62 mm Advanced Platforms

- Multi-caliber / Convertible Systems

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- Gas-operated rifles

- Short-stroke piston rifles

- Hybrid recoil mitigation systems

- Suppressor-optimized weapon systems

- By End User- Market Size & Forecast 2022-2032, USD Million

- Military Infantry Forces

- Special Operations Forces

- Homeland Security / Law Enforcement

- Reserve / National Guard modernization

- By Region

- North America

- Europe

- The Middle East & Africa

- Asia-Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- North America Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- The US

- Rest of North America

- The US Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Europe Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- The UK Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- The Middle East & Africa Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- Saudi Arabia

- The UAE

- South Africa

- Egypt

- Rest of Middle East & Africa

- Saudi Arabia Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The UAE Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Africa Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Egypt Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Asia-Pacific Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- China Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Korea Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Australia Next Generation Infantry Rifles Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Weapon Type- Market Size & Forecast 2022-2032, USD Million

- By Caliber Type- Market Size & Forecast 2022-2032, USD Million

- By Operating Mechanism- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Global Next Generation Infantry Rifles Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- SIG Sauer, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FN Herstal S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Heckler & Koch GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Colt’s Manufacturing Company LLC (Part of Colt CZ Group SE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Israel Weapon Industries (IWI) Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rheinmetall AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Dynamics Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Beretta Holding S.p.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daniel Defense, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kalashnikov Concern JSC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ST Engineering Land Systems Ltd. (ST Engineering Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Barrett Firearms Manufacturing, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Česká zbrojovka a.s. (CZ) (Part of Colt CZ Group SE)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- China North Industries Group Corporation Limited (NORINCO Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Advanced Weapons and Equipment India Limited (AWEIL)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SIG Sauer, Inc.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now