Middle East & North Africa Air Conditioners Market Research Report: Forecast (2026-2032)

Middle East & North Africa Air Conditioners Market - By Product Type Room Air Conditioners (Window AC, Split AC), VRF Systems, Chillers, Packaged Air Conditioners, Cassette Air Con ... ditioners, Ducted Split Systems, Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.), By Refrigerant Type (R32, R410A, R134a, R1234ze / R1234yf, R744, Others), By Distribution Channel (Direct Sales, Authorized Dealers & Distributors, Multi-Brand Stores, Online), By End-User (Residential, Offices, Retail & Malls, Hotels & Hospitality, Hospitals & Healthcare, Educational Institutions, Manufacturing, Pharmaceuticals, Food & Beverage, Data Centers, Others), and others Read more

- Environment

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Middle East & North Africa Air Conditioners Market

Projected 5.57% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 12.45 Billion

Market Size (2032)

USD 18.19 Billion

Base Year

2025

Projected CAGR

5.57%

Leading Segments

By End User: Residential

Middle East & North Africa Air Conditioners Market Report Key Takeaways:

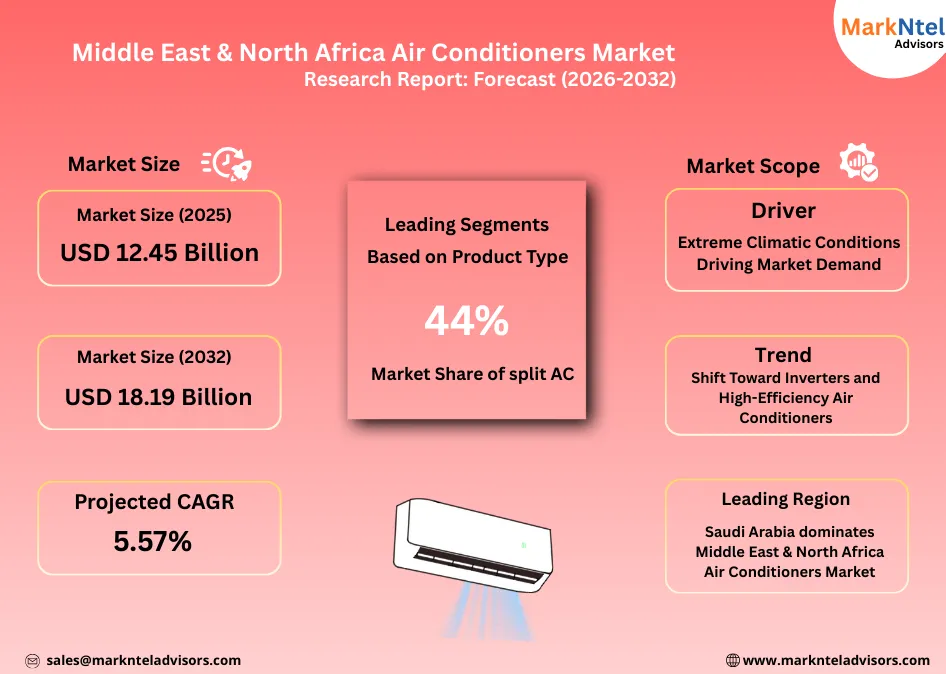

- The Middle East & North Africa Air Conditioners Market size was valued at around USD 12.45 billion in 2025 and is projected to reach USD 18.19 billion by 2032. The estimated CAGR from 2026 to 2032 is around 5.57%, indicating strong growth.

- By product type, the split AC segment represented 44% of the Middle East & North Africa Air Conditioners Market size in 2025.

- By end user, the residential sector seized around 23% of the Middle East & North Africa Air Conditioners Market size in 2025.

- Saudi Arabia leads the Middle East & North Africa Air Conditioners Market with a 21% market share in 2025.

- The leading air conditioner companies in the Middle East & North Africa are Panasonic Holdings Corporation, LG Electronics Inc., Daikin Industries, Ltd., Haier Group Corporation, Carrier Global Corporation, Samsung Electronics Co., Ltd., Johnson Controls International plc., Voltas Limited, Gree Electric Appliances, Inc., Robert Bosch GmbH, AB Electrolux, Mitsubishi Electric Corporation, Hitachi, Ltd., Guangdong Chigo Air Conditioning Co., Ltd., Rheem Manufacturing Company, SKM, Zamil and others.

Market Insights & Analysis: Middle East & North Africa Air Conditioners Market (2026- 2032):

The Middle East & North Africa Air Conditioners Market size was valued at around USD 12.45 billion in 2025 and is projected to reach USD 18.19 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.57% during the forecast period, i.e., 2026-32.

The Middle East & North Africa Air Conditioners Market is experiencing rapid growth, driven by worsening extreme heat conditions and a market-wide transition toward energy-efficient, inverter-driven cooling solutions.

According to the International Energy Agency (IEA), air conditioning currently accounts for approximately half of peak electricity demand across the MENA region. This substantial share highlights the direct linkage between rising ambient temperatures and electricity consumption patterns, as summer temperatures frequently exceed 40 °C across much of the region. As extreme heat events intensify, cooling demand increasingly defines peak load dynamics, compelling utilities and policymakers to reassess grid capacity, energy efficiency standards, and cooling technologies.

Country-specific climate developments further reinforce this outlook. In 2025, the United Arab Emirates experienced multiple days with temperatures exceeding 50 °C in desert regions such as Sweihan, following the hottest spring recorded nationally. These conditions significantly increased cooling requirements across residential, commercial, and industrial segments, particularly in urban and logistics-intensive zones.

Similarly, Qatar and Kuwait recorded temperature extremes above 50 °C during 2024, according to regional assessments by the World Meteorological Organization (WMO). Furthermore, Kuwait’s historical maximum of 53.2 °C at Al-Nuwaiseeb underscores the persistent severity of the region’s climate and the resulting structural reliance on air conditioning across households and workplaces .

Parallel to climatic pressures, the market is being reshaped by a pronounced shift toward inverter-based and high-efficiency air conditioning systems. Manufacturers are increasingly aligning product development with energy efficiency imperatives and grid sustainability concerns. For instance, inverter-equipped window air conditioners such as Midea’s Wonder Window series commercially available across the UAE and Saudi retail channels, are designed to deliver consistent cooling performance while reducing electricity consumption relative to conventional fixed-speed models. These solutions are particularly relevant for high-density urban housing, where efficiency and operating cost considerations are becoming increasingly critical.

Looking beyond 2025, climate projections suggest further intensification of cooling demand. The World Meteorological Organization (WMO) has warned that average temperatures across the Arab region are rising at approximately twice the global average, a trend expected to persist for decades.

Complementing this, the IEA projects that regional temperatures could rise by 2.5 °C under low-emissions scenarios and up to 6.4 °C under high-emissions pathways by the late 21st century. Such increases will substantially expand cooling degree days, reinforcing air conditioning as a baseline requirement rather than a seasonal necessity.

Overall, escalating thermal extremes, mounting peak electricity pressures, and climate-driven technology adoption collectively position air conditioning as critical infrastructure across MENA. These structural factors will continue to underpin strong and resilient market growth over the long term.

Middle East & North Africa Air Conditioners Market Recent Developments:

- December 2025: Bosch Home Comfort Group highlighted advanced air-conditioning technologies at HVACR World 2025, focusing on high-efficiency VRF and commercial AC systems, smart control integration, and low-GWP refrigerant solutions. The showcased air-conditioning portfolio emphasized improved energy performance, system reliability, and sustainability.

- October 2025: TCL showcased its latest air-conditioning innovations at the Middle East & Africa Air Conference 2025, featuring the flagship VoxIN JetMax for extreme climates, energy-efficient SaveIN Series, and advanced commercial and residential cooling solutions. The event underlined TCL’s strategic focus on intelligent, sustainable, and high-performance air solutions tailored for the MENA region.

Middle East & North Africa Air Conditioners Market Scope:

| Category | Segments |

|---|---|

| By Product Type | Room Air Conditioners (Window AC, Split AC), VRF Systems, Chillers, Packaged Air Conditioners, Cassette Air Conditioners, Ducted Split Systems, Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.), |

| By Refrigerant Type | R32, R410A, R134a, R1234ze / R1234yf, R744, Others |

| By Distribution Channel | Direct Sales, Authorized Dealers & Distributors, Multi-Brand Stores, Online |

| By End-User | Residential, Offices, Retail & Malls, Hotels & Hospitality, Hospitals & Healthcare, Educational Institutions, Manufacturing, Pharmaceuticals, Food & Beverage, Data Centers, Others), and others |

Middle East & North Africa Air Conditioners Market Driver:

Extreme Climatic Conditions Driving Market Demand

Extreme climatic conditions represent one of the most powerful structural drivers shaping the growth of the Middle East and North Africa (MENA) air conditioners market. The region is experiencing a sustained intensification of heat stress, driven by climate change and accelerated regional warming trends.

According to the World Meteorological Organization (WMO), the MENA region recorded its hottest year on record in 2024, with several locations witnessing temperatures exceeding 50 °C during prolonged heatwaves. Notably, UN-backed assessments indicate that temperatures across the region are rising at nearly twice the global average, amplifying pressure on public health systems, urban infrastructure, and electricity networks.

The severity of heat exposure was starkly demonstrated during the 2024 Hajj pilgrimage, when extreme temperatures above 50 °C in Mecca resulted in at least 1,301 fatalities and thousands of heat-related medical emergencies. This event highlighted the lethal risks associated with prolonged heat exposure in densely populated settings and reinforced the critical role of air conditioning in safeguarding human life, particularly in residential, healthcare, hospitality, and public gathering environments.

As heatwaves become more frequent, longer in duration, and more intense, air conditioning systems are transitioning from discretionary appliances to essential infrastructure across the MENA region. Consequently, sustained temperature escalation is expected to continue driving strong demand for air conditioners, supporting long-term market expansion.

Middle East & North Africa Air Conditioners Market Trend:

Shift Toward Inverters and High-Efficiency Air Conditioners

The Middle East & North Africa air conditioners market is undergoing a structural transition toward inverter-driven and high-efficiency cooling systems as governments and utilities seek to address escalating electricity consumption and heat-driven peak demand pressures.

Intensifying summer temperatures and longer cooling seasons have significantly increased the operational load on regional power grids, exposing the inefficiencies of conventional fixed-speed air conditioners. Inverter technology, which modulates compressor speed based on real-time cooling demand, is increasingly favored for its ability to deliver stable thermal comfort while substantially reducing energy consumption and peak load stress.

Regulatory enforcement is a central catalyst accelerating this trend. In Saudi Arabia, the Saudi Standards, Metrology and Quality Organization (SASO) mandates minimum energy performance requirements under SASO 2663 for split and window air conditioners. The regulation specifies Energy Efficiency Ratio (EER) and Seasonal Energy Efficiency Ratio (SEER) thresholds that effectively promote inverter-ready and high-efficiency configurations. Periodic tightening of these benchmarks has compelled manufacturers and importers to redesign product portfolios to ensure compliance, thereby accelerating market-wide adoption of inverter-based systems .

At the manufacturer level, product innovation is increasingly aligned with regulatory and climatic realities. For example, Rheem’s Comfort Master Inverter Series exemplifies this shift, incorporating inverter compressors and intelligent control systems engineered to maintain performance stability in extreme ambient temperatures reaching up to 54 °C.

Collectively, regulatory mandates, grid reliability concerns, and climate-adaptive product innovation are firmly positioning inverter and high-efficiency air conditioners as a defining growth trend across the MENA market.

Middle East & North Africa Air Conditioners Market Challenge:

Increasing Costs and Operational Risks

High energy consumption from widespread air conditioner usage poses a structural challenge to the Middle East & North Africa (MENA) air conditioners market, directly straining electricity grids and raising infrastructure sustainability concerns.

According to the International Energy Agency (IEA), electricity demand across MENA has tripled since 2000, exceeding 1,000 terawatt-hours (TWh) by 2024, making the region one of the fastest-growing electricity markets globally. Cooling demand is a primary contributor to this surge .

The IEA reports that air conditioning represents nearly 50% of peak electricity demand and about 25% of annual consumption in MENA. Rapidly rising temperatures intensify peak loads, forcing utilities to add capacity used mainly during short summer periods, reducing overall system efficiency.

The challenge is further amplified by projections indicating that electricity demand in MENA could rise by an additional 50% by 2035 without strong efficiency interventions. While efficiency improvements could reduce peak demand growth by up to 35 gigawatts, slow replacement of legacy, inefficient air conditioners continues to exacerbate grid stress.

Overall, persistent grid load pressure and rising energy consumption from air conditioning increase infrastructure costs and operational risks. Without accelerated efficiency adoption and grid modernization, these constraints may limit market scalability and slow long-term growth.

Middle East & North Africa Air Conditioners Market (2026-32) Segmentation Analysis:

The Middle East & North Africa Air Conditioners Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on Product Type:

- Room Air Conditioners- USD Million & Thousand Units

- Window AC - USD Million & Thousand Units

- By Tonnage Capacity

- Window AC - USD Million & Thousand Units

- Upto 1 Ton

- 1 Ton to 2 Ton

- Above 2 Ton

- Split AC - USD Million & Thousand Units

- By Tonnage Capacity

- Split AC - USD Million & Thousand Units

- Upto 1 Ton

- 1 Ton to 1.5 Ton

- Above 1.6 to 2 tons

- Above 2 Ton

- VRF Systems

- Chillers

- Air-cooled chillers

- Water-cooled chillers

- Others

- Packaged Air Conditioners

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Cassette Air Conditioners

- Upto 2 Tons

- 2.1 to 4 Tons

- 4.1 to 5 Tons

- Above 5 Tons

- Ducted Split Systems

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.)

The split AC segment holds the top spot in the Middle East & North Africa Air Conditioners Market, with a market share of around 44%. This segment is maintaining its leadership due to its focus on functional flexibility, superior efficiency, and broad applicability across residential and light-commercial environments.

Their two-unit configuration enables quieter indoor operation and improved thermal performance compared to window systems, making them particularly suitable for modern housing developments, offices, retail outlets, and hospitality facilities.

The segment’s strength is reinforced by its extensive tonnage range, spanning below 1 ton to above 2 tons, which allows precise capacity selection based on room size and occupancy patterns. Demand is especially concentrated in the 1 ton to 1.5 ton and above 1.6 to 2 ton categories, as these capacities align closely with standard room configurations prevalent in urban residential and small commercial buildings across the region.

Technological advancements have further consolidated the dominance of split ACs. Increasing integration of inverter technology has enhanced energy efficiency, reduced operating costs, and supported compliance with evolving energy performance regulations.

Combined with sustained residential construction activity and steady replacement demand for older units, these factors collectively underpin the leading position of split air conditioners within the overall market structure.

Based on End User:

- Residential

- Offices

- Retail & Malls

- Hotels & Hospitality

- Hospitals & Healthcare

- Educational Institutions

- Manufacturing

- Pharmaceuticals

- Food & Beverage

- Data Centers

- Others

The residential sector leads the Middle East & North Africa Air Conditioners Industry, with 23% market share, and continues to lead due to a combination of climatic necessity, demographic expansion, and housing sector growth.

Persistently high temperatures and extended summer seasons across the region have made air conditioning an essential household utility, resulting in widespread penetration across urban and suburban residences.

At the same time, rising household incomes are supporting a gradual shift toward higher-capacity and energy-efficient systems, contributing to both first-time installations and upgrade-driven demand.

Residential cooling usage has also intensified due to changing living patterns, including longer hours spent indoors and increased home-based activities, which elevate daily operating requirements compared to commercial environments with fixed occupancy schedules. In addition, residential air conditioners typically experience higher utilization rates and faster replacement cycles because of continuous operation during prolonged heat periods.

Supportive policy frameworks, including national housing programs and broad electrification coverage, further underpin residential demand. Collectively, structural climate conditions, sustained housing expansion, and frequent replacement needs firmly establish the residential sector as the dominant end-user segment in the MENA air conditioners market.

Middle East & North Africa Air Conditioners Market (2026-32): Regional Projection

The Middle East & North Africa Air Conditioners Market is dominated by Saudi Arabia, which holds a commanding 21% share, supported by its severe climatic conditions, large domestic demand base, and sustained investment in urban and infrastructure development.

Extended periods of extreme heat, with summer temperatures frequently surpassing 45 °C, make air conditioning a fundamental requirement across households, commercial buildings, and industrial facilities.

The country’s demographic scale and rapid urbanization further strengthen demand fundamentals. Ongoing residential expansion and large-scale mixed-use developments associated with national transformation initiatives are significantly increasing the installed base of air conditioning systems. In parallel, continued growth in sectors such as hospitality, healthcare, retail, and public infrastructure is driving demand for both centralized and room-based cooling solutions.

Saudi Arabia’s regulatory environment also supports market leadership. Energy efficiency standards enforced by the Saudi Standards, Metrology and Quality Organization (SASO) have raised minimum performance thresholds for air conditioners, accelerating the replacement of legacy systems with higher-efficiency and inverter-based models. This regulatory push has sustained demand even in mature urban markets.

Moreover, rising electricity consumption linked to cooling requirements has elevated air conditioning to a strategic infrastructure priority, encouraging technology upgrades and capacity additions. Collectively, climatic severity, population size, construction activity, and regulatory enforcement firmly position Saudi Arabia as the dominant country market within the MENA air conditioners landscape.

Gain a Competitive Edge with Our Middle East & North Africa Air Conditioners Market Report:

- Middle East & North Africa Air Conditioners Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Middle East & North Africa Air Conditioners Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Middle East & North Africa Air Conditioners Market Regulations, Policies & Standards

- Middle East & North Africa Air Conditioners Market Trends & Developments

- Middle East & North Africa Air Conditioners Market Supply Chain Analysis

- Middle East & North Africa Air Conditioners Market Imports/Exports

- Middle East & North Africa Air Conditioners Market Dynamics

- Growth Drivers

- Challenges

- Middle East & North Africa Air Conditioners Market Hotspots & Opportunities

- Middle East & North Africa Air Conditioners Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Room Air Conditioners- USD Million & Thousand Units

- Window AC - USD Million & Thousand Units

- By Tonnage Capacity

- Upto 1 Ton

- 1 Ton to 2 Ton

- Above 2 Ton

- By Tonnage Capacity

- Split AC - USD Million & Thousand Units

- By Tonnage Capacity

- Upto 1 Ton

- 1 Ton to 1.5 Ton

- Above 1.6 to 2 Ton

- Above 2 Ton

- By Tonnage Capacity

- Window AC - USD Million & Thousand Units

- VRF Systems

- Chillers

- Air-cooled chillers

- Water-cooled chillers

- Others

- Packaged Air Conditioners

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Cassette Air Conditioners

- Upto 2 Tons

- 2.1 to 4 Tons

- 4.1 to 5 Tons

- Above 5 Tons

- Ducted Split Systems

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.)

- Room Air Conditioners- USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- R32

- R410A

- R134a

- R290

- R1234ze / R1234yf

- Others

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- Direct Sales

- Authorized Dealers & Distributors

- Multi-Brand Stores

- Online

- By End User – Market Size & Forecast 2022-2032, USD Million

- Residential

- Offices

- Retail & Malls

- Hotels & Hospitality

- Hospitals & Healthcare

- Educational Institutions

- Manufacturing

- Pharmaceuticals

- Food & Beverage

- Data Centers

- Others

- By Country

- Saudi Arabia

- UAE

- Qatar

- Oman

- Kuwait

- Bahrain

- Egypt

- Morocco

- Algeria

- Tunisia

- Rest of Middle East & North Africa

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Analysis

- Saudi Arabia Air Conditioners Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- UAE Air Conditioners Market Outlook, 2022-2032

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Qatar Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Oman Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Kuwait Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Bahrain Africa Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Egypt Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Morocco Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Algeria Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Tunisia Air Conditioners Market Outlook, 2022-2032F

- Market Size & Analysis

- By Revenue (USD Million)

- Market Share & Analysis

- By Product Type – Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Refrigerant Type – Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel – Market Size & Forecast 2022-2032, USD Million

- By End User – Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Middle East & North Africa Air Conditioners Market Key Strategic Imperatives for Growth & Success

- Competitive Outlook

- Company Profiles

- Panasonic Holdings Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- LG Electronics Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Daikin Industries, Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Haier Group Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Carrier Global Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Samsung Electronics Co., Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Johnson Controls International plc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Voltas Limited

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances, Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Robert Bosch GmbH

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- AB Electrolux

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Mitsubishi Electric Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Hitachi, Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Guangdong Chigo Air Conditioning Co., Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- SKM

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Zamil

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Rheem Manufacturing Company

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Panasonic Holdings Corporation

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now