Latin America Farm Implements Market Research Report: Growth Drivers & Forecast (2026-2032)

By Product Type (Cultivators, Tillers, Seeders & Planters, Rotavators, Sprayers, Harvesters, Others), By Power Source (Manual Implements, Tractor-Mounted Implements, Self-Propelled ... Implements), By End-Use (Small Farms & Smallholders, Commercial / Large Scale Farms, Custom Service Providers / Contractors), and others Read more

- Environment

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

Latin America Farm Implements Market

Projected 8.41% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 3.08 Billion

Market Size (2032)

USD 5.00 Billion

Base Year

2025

Projected CAGR

8.41%

Leading Segments

By Product Type: Cultivators

Latin America Farm Implements Market Report Key Takeaways:

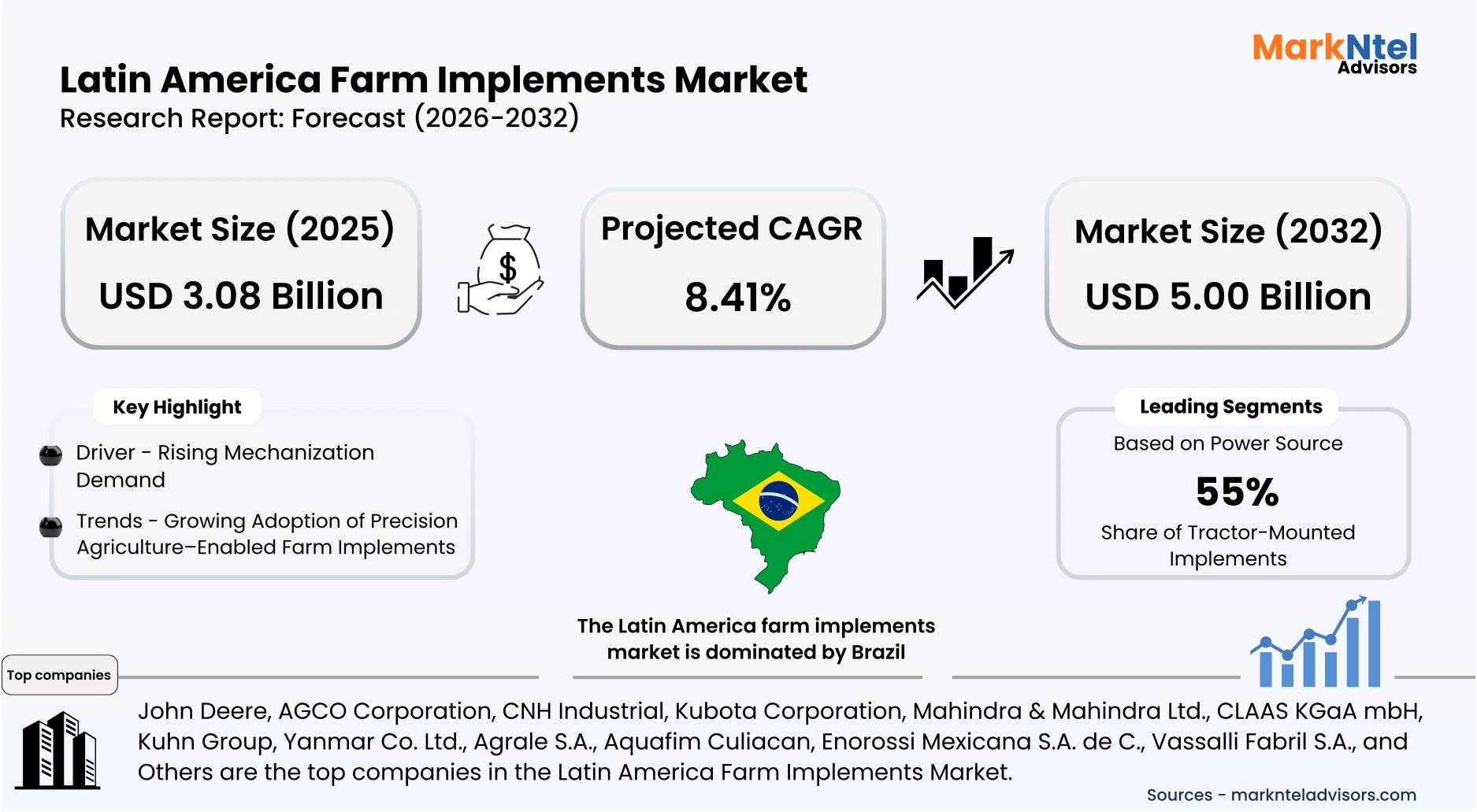

- Market size was valued at around USD 3.08 billion in 2025 and is projected to reach USD 5.00 billion by 2032. The estimated CAGR from 2026 to 2032 is around 8.41%, indicating strong growth.

- By product type, the cultivators represented a significant share of about 32% in the Latin America Farm Implements Market in 2025.

- By power source, the tractor-mounted implements seized a significant share of about 55% in the Latin America Farm Implements Market in 2025.

- Leading Farm Implements companies in Latin America are John Deere, AGCO Corporation, CNH Industrial, Kubota Corporation, Mahindra & Mahindra Ltd., CLAAS KGaA mbH, Kuhn Group, Yanmar Co. Ltd., Agrale S.A., Aquafim Culiacan, Enorossi Mexicana S.A. de C., Vassalli Fabril S.A., and Others.

Market Insights & Analysis: Latin America Farm Implements Market (2026-32):

The Latin America Farm Implements Market size was valued at around USD 3.08 billion in 2025 and is projected to reach USD 5.00 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 7.2% during the forecast period, i.e., 2026-32.

The Latin America farm implements market is expected to grow steadily from 2025 through 2032, supported by ongoing agricultural modernization and institutional investments in mechanization and digital farming services. As traditional labor pools decline and production systems expand, producers increasingly rely on mechanized solutions to improve operational efficiency, reduce costs, and boost yields.

Institutional programs are enhancing access to equipment financing and technical support. For example, the World Bank approved a USD 1.6 billion initiative to support Brazil’s agrifood system, aimed at increasing productivity, market access, and sustainable management for family farmers over the next decade. This investment directly strengthens the farm equipment ecosystem by linking mechanization with broader productivity strategies .

Technology adoption is accelerating. In Uruguay, the Inter‑American Development Bank approved a USD 560,900 precision agriculture project to test the adoption of data‑enabled tools for input efficiency, encouraging the use of modern, precision‑ready implements that reduce water, seed, and fertilizer waste .

Credit access improvements also support smallholder mechanization. Brazil’s rural credit programs under PRONAF allocated approximately USD 14 billion in subsidized loans in 2024, including credit lines for acquiring small tractors and machinery, lowering barriers to equipment ownership .

Across the region, public extension services and digital platforms are strengthening farmers’ capacity to use and maintain machinery, while climate‑risk insurance collaborations aim to protect agricultural investment returns.

As institutional support expands and digital tools integrate with farm implements, the market is poised for broad mechanization gains, improved productivity, and increased sustainability from 2025 to 2032.

Latin America Farm Implements Market Recent Developments:

- 2025: AGCO invested USD 3.2 million to open a Reman Transmissions Center and AGCO Academy headquarters in Jundiaí, Brazil, boosting local production and technician training. The center will start transmission production in 2025, aiming to support farmers with affordable, high-quality parts.

- 2025: At Agrishow 2025 in Brazil, agricultural machinery and implements recorded approximately USD 2.9 billion in business intentions, a 7 % increase year-on-year — showing strong demand optimism for equipment sales.

Latin America Farm Implements Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Cultivators, Tillers, Seeders & Planters, Rotavators, Sprayers, Harvesters, Others), |

| By Power Source | (Manual Implements, Tractor-Mounted Implements, Self-Propelled Implements), |

| By End-Use | (Small Farms & Smallholders, Commercial / Large Scale Farms, Custom Service Providers / Contractors), |

Latin America Farm Implements Market Driver:

Rising Mechanization Demand

Rising mechanization demand in Latin America is a pivotal driver for the farm implements market, driven by structural shifts in agriculture toward higher productivity and cost-effectiveness. Latin America and the Caribbean have historically shown significant mechanization progress; tractor use per 1,000 ha of arable land rose sharply from the 1960s to the 2000s, reflecting increasing adoption of machinery over manual methods.

Brazil alone allocates substantial public funds to agriculture under the Crop Plan 2024/25; nearly USD 54.6 billion was earmarked to support production costs and USD 19.6 billion for modernization investments, including machinery and technological upgrades . These programmes enhance access to tractors, planters, and harvesters, enabling producers to optimize sowing and harvesting cycles more efficiently. Government credit support under programmes such as PRONAF and Plano Safra, which collectively provide nearly USD 70 billion annually, also subsidizes mechanization investments for small and large farmers alike .

Mechanization reduces labor dependency in regions where rural workers are increasingly migrating to cities and where large-scale soybean, maize, and sugarcane farming demands efficient operations. Brazil’s role as a top global exporter of grains underscores the need for mechanized agriculture to sustain yields and competitiveness.

Future Investments Beyond 2025, Governments are expanding rural credit, and precision agriculture tools are receiving infrastructure investments, while Brazil’s ongoing ABC+ and the expanded Crop Plan beyond 2025 will promote sustainable mechanization, including funding for smart implements and low-carbon technologies.

Overall, rising mechanization demand supported by official agricultural financing, modernization programmes, and tractor adoption will continue to elevate farm implement investments, driving market growth as producers seek higher productivity and global export competitiveness.

Latin America Farm Implements Market Trend:

Growing Adoption of Precision Agriculture–Enabled Farm Implements

Latin America is rapidly integrating precision agriculture technologies into farm implements to enhance productivity, sustainability, and resource use efficiency. Public institutions and government programs play a central role in this shift. In Argentina, the National Institute of Agricultural Technology (INTA) reports increased use of precision technologies such as GPS-based planters and electronic sowing control systems, which improve input accuracy and reduce waste in large grain and oilseed operations . Public seminars and field days organized by INTA emphasize tools like variable-rate application and data-driven soil mapping that help farmers refine input application and maximize yields.

A recent example of this trend is the Precision Agriculture Day held at Estación Experimental Agropecuaria Chilecito (May, 2025), under Argentina’s Ministry of Agriculture programs. The event showcased precision farming applications, including machine learning, big data, and AI integration with soil and crop data, demonstrating governmental efforts to accelerate technology adoption among producers facing climate variability and cost challenges .

Similarly, Argentina’s 20th International Precision Agriculture Congress drew over 800 specialists, highlighting innovations in seeders equipped with electronics for precision planting and guidance systems that improve operational accuracy across large farms.

This growing adoption reflects public sector support for digital farming tools, making precision-enabled implements a core trend driving Latin America’s agricultural modernization.

Latin America Farm Implements Market Opportunity:

Service & Maintenance Ecosystem Expansion

A robust service and maintenance ecosystem around farm implements is a key opportunity in the Latin America farm equipment market. As mechanization increases, so does the need for dependable after-sales support, authorized repair centres, and locally available spare parts essential for maximizing equipment uptime and farmer ROI.

Governments and public institutions are advancing extension services and technical assistance that increasingly link machinery servicing with broader agricultural support. For example, Argentina’s National Agricultural Technology Institute (INTA) operates more than 350 rural extension units that provide technical guidance, machinery training, and maintenance advice to farmers across diverse agro-ecological zones, strengthening local service capacity .

In Brazil, public agricultural research and technology institutions such as the Instituto Agronômico de Campinas perform mechanical testing on tractors and engines, contributing to better performance standards and informing maintenance practices . These institutional service functions improve implementation reliability and encourage farmers to invest confidently in mechanized solutions.

Official programmes in Mexico under the Secretariat of Agriculture and Rural Development (SADER) are also geared toward supporting rural extension and technical training, enhancing local service networks, and after-sales support for farm machinery.

As mechanization deepens and more producers acquire tractors and advanced implements, expansion of certified service networks, training centres, and spare-parts distribution hubs will reduce downtime, improve lifecycle value for equipment, and strengthen demand for new implements linked with long-term service contracts, reinforcing overall market growth.

Latin America Farm Implements Market Challenge:

High Capital Cost and Limited Affordability

High capital cost and limited affordability remain central barriers to farm implement adoption in Latin America, especially for small and medium producers. Access to finance is a persistent constraint; many farmers lack sufficient credit for mechanization because financial products tailored to agriculture are limited or unavailable, restricting purchases of tractors and implements. According to World Bank policy research, inadequate access to credit and small farm size are key factors that constrain farm mechanization, as smallholders often cannot afford high initial investment costs without financial support.

Governments and institutions have acknowledged these barriers. For example, at the 2025 World Bank Annual Meetings, the AgriConnect initiative was announced to expand agriculture financing, aiming to scale commitments to USD 9,000 million annually by 2030 and improve smallholder access to credit, technology, and mechanization solutions.

Despite such initiatives, many rural farmers still face high machinery acquisition costs relative to their incomes and limited collateral or credit history to secure loans. Public credit programmes exist in some countries, but they often prioritize larger commercial producers over smaller farms, reducing mechanization uptake among the majority of the rural workforce. Supporting tailored rural finance products, leasing schemes, and accessible credit channels remains essential to overcoming affordability gaps and unlocking broader mechanization adoption across the region.

Latin America Farm Implements Market (2026-32) Segmentation Analysis:

The Latin America Farm Implements Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

-

- Cultivators

- Tillers

- Seeders & Planters

- Rotavators

- Sprayers

- Harvesters

- Others

Cultivators dominate the Latin America farm implements industry with a 32% share, driven by their versatility and critical role in soil preparation. They are widely used for tilling, aeration, and weed management across diverse crops such as maize, soybeans, and sugarcane. Small and medium farms particularly rely on cultivators because they are cost-effective, easy to operate, and compatible with both manual and mechanized power sources.

Government-supported programs promoting sustainable agriculture and soil health have also encouraged the adoption of cultivators. In Brazil and Argentina, public extension services and mechanization initiatives have promoted efficient land preparation, increasing the demand for versatile soil-working tools. Cultivators’ relatively low acquisition cost and compatibility with precision farming add to their widespread use, making them a key revenue contributor in the farm implements market.

Based on Power Source:

- Manual Implements

- Tractor-Mounted Implements

- Self-Propelled Implements

Tractor-mounted implements lead the market with 55% share as mechanization grows across large-scale farms. These implements, including seeders, sprayers, and rotavators, provide efficiency and high productivity, reducing labor dependency while covering extensive agricultural land rapidly. Government credit programs in Brazil and Mexico, such as PRONAF and SADER initiatives, have facilitated tractor ownership and the use of compatible mounted implements, particularly in commercial farms. Tractor-mounted systems also integrate with precision agriculture tools, enabling GPS-guided operations that optimize input use and enhance crop yields. Their scalability, durability, and ability to improve operational efficiency explain their dominant market position.

Latin America Farm Implements Market (2026-32): Regional Projection

The Latin America farm implements market is dominated by Brazil, which accounts for the largest share of regional demand. Brazil’s dominance stems from its extensive agricultural land, high mechanization rates, and large-scale commercial crop production, including soybeans, maize, sugarcane, and coffee. The country’s government programs, such as PRONAF (National Program for Strengthening Family Agriculture), provide subsidized credit for tractors and implements, enabling both smallholders and large farms to invest in modern machinery. Large-scale commercial farms benefit from tractor-mounted and self-propelled implements, while smallholders increasingly adopt manual and cultivator-based tools supported by extension services. Research and technology initiatives from institutions like EMBRAPA promote precision agriculture and mechanization, further driving implementation adoption.

Additionally, Brazil’s infrastructure, rural connectivity, and strong agro-industry ecosystem make it the primary hub for farm machinery in Latin America, creating a multiplier effect on demand, service networks, and maintenance services, solidifying its position as the regional market leader.

Gain a Competitive Edge with Our Latin America Farm Implements Market Report:

- Latin America Farm Implements Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Latin America Farm Implements Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Latin America Farm Implements Market Policies, Regulations, and Product Standards

- Latin America Farm Implements Market Trends & Developments

- Latin America Farm Implements Market Dynamics

- Growth Factors

- Challenges

- Latin America Farm Implements Market Hotspot & Opportunities

- Latin America Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Cultivators

- Tillers

- Seeders & Planters

- Rotavators

- Sprayers

- Harvesters

- Others

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- Manual Implements

- Tractor-Mounted Implements

- Self-Propelled Implements

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Small Farms & Smallholders

- Commercial / Large Scale Farms

- Custom Service Providers / Contractors

- By Country

- Mexico

- Brazil

- Argentina

- Chile

- Peru

- Ecuador

- Colombia

- Guatemala

- Dominican Republic

- Costa Rica

- Honduras

- Rest of Latin America

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Argentina Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Chile Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Peru Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Ecuador Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Colombia Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Guatemala Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Dominican Republic Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Costa Rica Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Honduras Farm Implements Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Power Source - Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Latin America Farm Implements Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- John Deere

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AGCO Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CNH Industrial

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kubota Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mahindra & Mahindra Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- CLAAS KGaA mbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kuhn Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yanmar Co. Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Agrale S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Aquafim Culiacan

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Enorossi Mexicana SA de C.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vassalli Fabril S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- John Deere

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now