Kenya HVAC Market Research Report: Forecast (2026-2032)

By Product Type (Room Air Conditioners, VRF Systems, Chillers, Packaged Air Conditioners, Cassette Air Conditioners, Ducted Split Systems, Boilers, Heat Pump), By Sales Channel (Di ... rect Sales, Authorized Dealers & Distributors, Multi-Brand Stores, Online), By Refrigerant Type (R32, R410A, R134a, R290, R1234ze / R1234yf, Others), By End-User (Residential, Offices, Retail & Malls, Hotels & Hospitality, Hospitals & Healthcare, Educational Institutions, Manufacturing, Pharmaceuticals, Food & Beverage, Data Centers, Others), and others Read more

- Environment

- Mar 2026

- Pages 160

- Report Format: PDF, Excel, PPT

Kenya HVAC Market

Projected 5.80% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 82 Million

Market Size (2032)

USD 115 Million

Base Year

2025

Projected CAGR

5.80%

Leading Segments

By End User: Commercial

Kenya HVAC Market Report Key Takeaways:

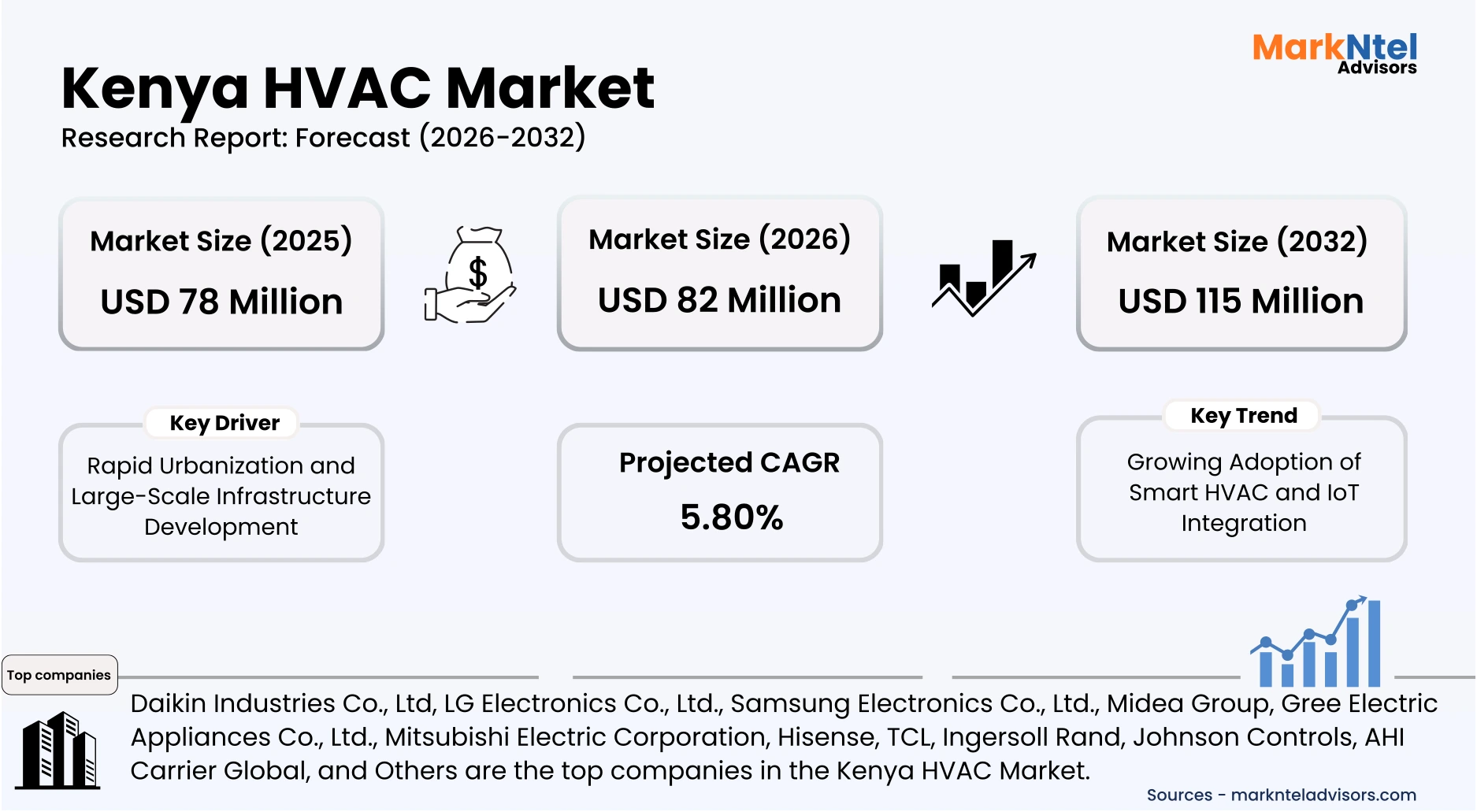

- The Kenya HVAC Market size was valued at USD 78 million in 2025 and is projected to grow from USD 82 million in 2026 to USD 115 million by 2032, exhibiting a CAGR of 5.80% during the forecast period.

- By product type, the room air conditioners segment represented a significant share of about 48% in the Kenya HVAC Market in 2026.

- By end user, the residential segment captured a significant share of about 36% in the Kenya HVAC Market in 2026.

- Leading HVAC companies in Kenya are Daikin Industries Co., Ltd, LG Electronics Co., Ltd., Samsung Electronics Co., Ltd., Midea Group, Gree Electric Appliances Co., Ltd., Mitsubishi Electric Corporation, Hisense, TCL, Ingersoll Rand, Johnson Controls, AHI Carrier Global, and Others.

Market Insights & Analysis: Kenya HVAC Market (2026-32):

The Kenya HVAC Market size was valued at around USD 78 million in 2025 and is projected to grow from USD 82 million in 2026 to USD 115 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.80% during the forecast period, i.e., 2026-32.

The Kenya HVAC Market is projected to expand steadily, driven by rapid urbanization, expanding infrastructure development, and the increasing adoption of smart HVAC technologies integrated with IoT for improved energy efficiency and automated climate control.

Urban population growth is one of the most influential factors shaping the demand for climate-control solutions across residential and commercial buildings. According to data referenced from the World Bank, Kenya’s urban population reached approximately 16.9 million in 2024, representing a 3.8% increase compared to 2023, reflecting continued migration toward urban centers and growing pressure on city infrastructure.

Additionally, the Kenya National Bureau of Statistics (KNBS) reports that 31.2% of the country’s total population currently resides in urban areas, indicating the rapid expansion of cities and the rising need for modern buildings equipped with ventilation and cooling systems .

Urbanization trends are particularly visible across major and emerging cities. In western Kenya, urban growth in cities such as Kisumu and Kakamega is strengthening regional economic activity. Kisumu alone is estimated to have more than 430,532 residents in 2025, highlighting its increasing importance as a commercial and administrative hub. Meanwhile, coastal regions are also experiencing substantial urban expansion.

The city of Mombasa, driven by tourism, port trade, and real estate development, is projected to maintain strong population growth, with around 1.46 million residents in 2025. Such urban growth encourages the construction of residential apartments, hotels, shopping complexes, and office facilities, which directly increases the demand for HVAC installations.

Future population projections further highlight the long-term expansion of Kenya’s urban landscape. For instance, Mombasa’s population is expected to increase to approximately 1.54 million by 2030 and reach about 1.81 million by 2050.

Similarly, Nakuru is projected to grow from 574,091 residents in 2025 to 649,147 by 2030 and approximately 862,724 by 2050, while Kisumu could increase from 430,532 residents in 2025 to 463,820 by 2030 and about 618,843 by 2050. These demographic trends indicate rising demand for residential and commercial infrastructure, thereby strengthening the requirement for reliable HVAC solutions in buildings.

In addition to urban growth, Kenya’s strong renewable energy capacity is also shaping the future of the HVAC sector. The country has significantly expanded clean electricity generation, with renewable energy sources contributing more than 80% of the national grid’s power supply, including geothermal, hydropower, wind, and solar energy. This energy structure provides favorable conditions for deploying energy-efficient and renewable-powered cooling technologies across residential and commercial facilities.

Another emerging development is the increasing adoption of smart HVAC systems integrated with Internet of Things (IoT) technologies, enabling real-time system monitoring, predictive maintenance, and automated temperature control. Such technologies help optimize energy consumption while improving operational efficiency in modern buildings.

Overall, rapid urbanization, population growth in key cities, expanding renewable energy infrastructure, and technological advancements in smart HVAC systems are expected to create strong long-term demand for climate-control solutions in Kenya. These factors collectively position the Kenya HVAC market for sustained growth over the coming decades.

Kenya HVAC Market Recent Developments:

- 2025: LG Electronics launched its ARTCOOL inverter air conditioner in Kenya, designed to deliver energy-efficient cooling for residential and commercial spaces. The unit features LG’s inverter compressor technology capable of reducing energy consumption by up to 70% while improving cooling performance. The launch strengthens LG’s presence in Kenya’s growing demand for modern, efficient HVAC solutions.

Kenya HVAC Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Room Air Conditioners, VRF Systems, Chillers, Packaged Air Conditioners, Cassette Air Conditioners, Ducted Split Systems, Boilers, Heat Pump), |

| By Sales Channel | (Direct Sales, Authorized Dealers & Distributors, Multi-Brand Stores, Online), |

| By Refrigerant Type | (R32, R410A, R134a, R290, R1234ze / R1234yf, Others), |

| By End-User | (Residential, Offices, Retail & Malls, Hotels & Hospitality, Hospitals & Healthcare, Educational Institutions, Manufacturing, Pharmaceuticals, Food & Beverage, Data Centers, Others), |

Kenya HVAC Market Driver:

Rapid Urbanization and Large-Scale Infrastructure Development

Rapid urban expansion and large-scale infrastructure development are major factors driving the demand for HVAC systems in Kenya. Key urban centers such as Nairobi, Mombasa, and Nakuru are witnessing continuous growth in residential housing, commercial buildings, retail complexes, and hospitality facilities.

This ongoing urban development is increasing the requirement for reliable heating, ventilation, and air-conditioning solutions to maintain indoor comfort, air quality, and operational efficiency in modern buildings. Notably, the population of Nairobi has surpassed 6.1 million residents in 2025, reflecting the city’s rapid urbanization and intensifying the need for new residential apartments, office spaces, and mixed-use developments. Such construction activities directly contribute to higher demand for HVAC systems across residential and commercial sectors.

In parallel, the Kenyan government is investing in large-scale infrastructure and urban innovation projects that further stimulate building construction. A notable example is Konza Technopolis, a planned smart city located approximately 64 km from Nairobi and covering nearly 5,000 acres. The project is designed to serve as a technology and innovation hub comprising research institutions, residential communities, commercial facilities, and business parks. Developments of this scale require advanced HVAC installations to support energy-efficient buildings, office environments, and high-capacity commercial spaces.

The accelerating pace of urbanization, combined with strategic infrastructure initiatives and smart-city developments, is significantly expanding Kenya’s construction landscape. This growth is expected to drive sustained demand for HVAC systems, supporting the long-term expansion of the Kenya HVAC market.

Kenya HVAC Market Trend:

Growing Adoption of Smart HVAC and IoT Integration

The integration of Internet of Things (IoT) technologies into HVAC systems is emerging as a structural trend in Kenya’s building infrastructure sector. Rising electricity costs and increasing digital connectivity are accelerating the deployment of smart climate control systems that optimize energy consumption in real time. According to the International Energy Agency (IEA), buildings account for nearly 30% of global final energy consumption, encouraging governments and facility managers to adopt digital energy-management solutions. In Kenya, expanding broadband connectivity and increasing adoption of smart building technologies are supporting the deployment of sensor-enabled HVAC platforms for remote monitoring and predictive maintenance.

This trend is reshaping the HVAC value chain by shifting demand from conventional equipment toward digitally connected systems integrated with building management platforms. Smart HVAC solutions enable automated temperature regulation, fault detection, and energy analytics, significantly improving operational efficiency in large commercial buildings such as hospitals, hotels, and data centers. The Kenyan government’s implementation of the Energy Management Regulations under the Energy Act requires large facilities consuming over 180,000 kWh annually to implement structured energy-efficiency monitoring programs. As a result, enterprises increasingly deploy smart HVAC technologies to comply with energy audits and reduce operational costs.

The persistence of this trend is reinforced by national digital infrastructure initiatives and smart city development programs. Kenya is developing Konza Technopolis, a large smart city project under the Vision 2030 program, designed to integrate ICT infrastructure, digital services, and green urban development. The project emphasizes sustainable and energy-efficient building design that requires advanced building automation and connected HVAC systems for efficient climate control. Smart city developments such as Konza Technopolis are therefore expected to accelerate long-term adoption of IoT-enabled building management and HVAC technologies across Kenya’s urban infrastructure.

Kenya HVAC Market Opportunity:

Growing Adoption of Renewable Energy-Powered HVAC

The adoption of renewable energy–powered HVAC systems represents a compelling opportunity in Kenya as national policies increasingly prioritize sustainable cooling and clean energy integration. Kenya’s National Cooling Action Plan (NCAP) promotes climate-friendly cooling technologies across buildings, agriculture, and healthcare sectors while encouraging energy-efficient refrigeration and renewable energy integration. The policy aligns with global climate commitments and supports the transition toward low-emission cooling solutions. As regulatory frameworks emphasize sustainable infrastructure, demand is expanding for HVAC technologies capable of operating with renewable energy sources such as solar power.

This opportunity is translating into tangible market demand through government-backed projects deploying renewable-powered cooling systems across critical sectors. In 2026, Kenya launched the Kenya Cold Chain Accelerator (KCCA) to fund companies deploying solar-powered refrigeration and cooling infrastructure nationwide. The program supports pilot solar cold storage systems that reduce post-harvest food losses and improve energy efficiency across agricultural supply chains . Such initiatives demonstrate growing institutional demand for renewable cooling technologies and create practical deployment pathways for solar-integrated HVAC systems.

The opportunity is particularly advantageous for new and emerging players because renewable-integrated cooling solutions remain a developing niche within Kenya’s HVAC ecosystem. Smaller technology providers can differentiate themselves by offering solar-powered HVAC systems, modular cooling platforms, and energy-management integrations tailored to agricultural, healthcare, and rural infrastructure needs. Government pilot programs and sustainability initiatives lower entry barriers by creating demonstration projects and procurement channels. These structural conditions enable innovative firms to establish early market presence and scale renewable HVAC solutions across Kenya’s expanding green infrastructure sector.

Kenya HVAC Market Challenge:

High Initial Installation Costs

High upfront installation costs remain a key challenge limiting the wider adoption of HVAC systems in Kenya, particularly among residential consumers and small-scale commercial establishments.

The cost of installing a complete HVAC system varies significantly depending on building size, system capacity, and design complexity. For small residential properties, installation expenses typically range between USD 1,300 – USD 2,500. While these systems provide efficient indoor climate control, the initial capital requirement can be substantial for many households.

The financial burden becomes even higher for commercial properties. Mid-sized commercial HVAC installations generally range from USD 2,900 to USD 10,900, while large commercial or industrial systems can exceed more than USD 75,000, depending on the equipment specifications and building requirements. Such high capital expenditure often forces businesses and property developers to delay or scale down HVAC installations.

The significant upfront investment required for HVAC systems discourages adoption among cost-sensitive consumers and small enterprises. As a result, high installation expenses continue to slow the penetration of advanced climate-control solutions, restraining the overall growth potential of the Kenya HVAC market.

Kenya HVAC Market (2026-32) Segmentation Analysis:

The Kenya HVAC Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Room Air Conditioners

- Window AC

- Upto 1 Ton

- 1 Ton to 2 Ton

- Above 2 Ton

- Split AC

- Upto 1 Ton

- 1 Ton to 1.5 Ton

- Above 1.6 to 2 Ton

- Above 2 Ton

- Window AC

- VRF Systems

- Chillers

- Air-cooled chillers

- Water-cooled chillers

- Others

- Packaged Air Conditioners

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Cassette Air Conditioners

- Upto 2 Tons

- 2.1 to 4 Tons

- 4.1 to 5 Tons

- Above 5 Tons

- Ducted Split Systems

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Boilers

- Heat Pump

- Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.)

The room air conditioners segment dominates the Kenya HVAC market with 48% market share, due to their cost efficiency, ease of installation, and suitability for residential and small commercial environments.

Rapid urban expansion in key metropolitan areas such as Nairobi, Mombasa, and Nakuru has significantly increased the demand for compact cooling solutions across apartments, small offices, retail outlets, and hospitality establishments.

Compared with centralized cooling technologies such as chillers or variable refrigerant flow (VRF) systems, room air conditioners require relatively lower capital investment and simpler installation procedures, making them more accessible to households and small businesses.

Within this segment, split air conditioners account for a substantial portion of demand due to their superior energy efficiency, quieter operation, and enhanced cooling performance compared to window air conditioners. Capacity ranges such as 1 ton to 1.5 tons and above 1.6 to 2 tons are widely adopted because they effectively meet the cooling requirements of typical residential rooms and small commercial spaces.

The ongoing development of residential housing projects, budget hotels, and neighborhood retail facilities further supports the adoption of room air conditioners. Their affordability, flexibility, and suitability for small-scale applications continue to reinforce their leading position within the Kenya HVAC Industry.

Based on End User:

- Residential

- Offices

- Retail & Malls

- Hotels & Hospitality

- Hospitals & Healthcare

- Educational Institutions

- Manufacturing

- Pharmaceuticals

- Food & Beverage

- Data Centers

- Others

The residential segment dominates the Kenya HVAC Market with 36% market share, primarily driven by rapid urban population growth and rising residential construction across major cities. According to the World Bank, Kenya’s urban population has been steadily increasing, with urbanization exceeding 30% of the total population and continuing to rise as people migrate to cities such as Nairobi, Mombasa, and Kisumu. This urban expansion has accelerated the construction of apartment complexes, gated communities, and mixed-use housing developments, increasing the installation of air-conditioning, ventilation, and cooling systems to improve indoor comfort in densely populated urban environments.

Housing development programs and rising household purchasing power further reinforce the segment’s dominance. The Kenyan government’s affordable housing initiative under the Kenya Vision 2030 aims to deliver hundreds of thousands of housing units to address urban housing shortages. These newly constructed homes increasingly incorporate modern ventilation and cooling systems, particularly in middle-income residential developments. Additionally, higher temperatures and changing climate patterns have increased the need for indoor climate control in homes, encouraging greater adoption of split air conditioners and energy-efficient residential HVAC systems.

The residential segment also benefits from the growing availability of compact and cost-effective cooling technologies suited for apartments and smaller homes. Split and ductless HVAC systems require lower installation costs and minimal structural modification, making them ideal for residential use compared with centralized commercial systems. Expanding electricity access across Kenya, supported by national electrification programs, has further enabled households to adopt modern appliances, including air-conditioning units. For instance, in 2025, Daikin Air Conditioning India Pvt. Ltd., a subsidiary of Daikin Industries Ltd., opened a new office and showroom in Nairobi to expand sales, dealer networks, and consumer access to advanced air-conditioning solutions in Kenya’s growing residential market. As residential construction and urban living standards continue to improve, the housing sector remains the largest and most stable source of HVAC demand in Kenya.

Gain a Competitive Edge with Our Kenya HVAC Market Report:

- Kenya HVAC Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Kenya HVAC Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Kenya HVAC Market Policies, Regulations, and Product Standards

- Kenya HVAC Market Trends & Developments

- Kenya HVAC Market Dynamics

- Growth Factors

- Challenges

- Kenya HVAC Market Hotspot & Opportunities

- Kenya HVAC Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Room Air Conditioners

- Window AC

- Upto 1 Ton

- 1 Ton to 2 Ton

- Above 2 Ton

- Split AC

- Upto 1 Ton

- 1 Ton to 1.5 Ton

- Above 1.6 to 2 Ton

- Above 2 Ton

- Window AC

- VRF Systems

- Chillers

- Air-cooled chillers

- Water-cooled chillers

- Others

- Packaged Air Conditioners

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Cassette Air Conditioners

- Upto 2 Tons

- 2.1 to 4 Tons

- 4.1 to 5 Tons

- Above 5 Tons

- Ducted Split Systems

- Upto 5 Tons

- 6 to 10 Tons

- 11 to 20 Tons

- Above 20 Tons

- Boilers

- Heat Pump

- Others (Air Handling Units (AHU) / Fan Coil Units (FCU), etc.)

- Room Air Conditioners

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- Direct Sales

- Authorized Dealers & Distributors

- Multi-Brand Stores

- Online

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- R32

- R410A

- R134a

- R290

- R1234ze / R1234yf

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Residential

- Offices

- Retail & Malls

- Hotels & Hospitality

- Hospitals & Healthcare

- Educational Institutions

- Manufacturing

- Pharmaceuticals

- Food & Beverage

- Data Centers

- Others

- By Region- Market Size & Forecast 2022-2032, USD Million

- East

- West

- South

- North

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Room Air Conditioners Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya VRF Systems Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Chillers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Packaged Air Conditioners Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Cassette Air Conditioners Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Ducted Split Systems Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Boilers Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya Heat Pump Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Sales Channel- Market Size & Forecast 2022-2032, USD Million

- By Refrigerant Type- Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kenya HVAC Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Daikin Industries Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LG Electronics Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bosch

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsung Electronics Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Midea Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gree Electric Appliances Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mitsubishi Electric Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hisense

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- TCL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Trane

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toshiba

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Westpoint

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Unionaire

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Johnson Controls

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Carrier Global

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daikin Industries Co., Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now