Saudi Arabia Islamic Banking Software & Services Market Research Report Forecast (2026-2032)

Saudi Arabia Islamic Banking Software & Services Market - By Component Software (By type of banking, Retail Banking, Wholesale Banking, Private Banking, Universal Banking), By typ ... e of Solution, (Core Banking Solutions, Customer Relationship Management, Payment Processing & Digital Channels, Risk & Compliance Management, Trade & Treasury Management, Liquidity & Asset Management, Wealth & Fund Management, Analytics & Reporting Tools), Services, (Professional Services, Managed Services), By Deployment (On-premises, Cloud- Based), By Bank Type (Tier 1 Bank (Asset Size > USD 200 Bn), Tier 2 Bank (USD 100-200 Bn), Tier 3 Bank (Less Than USD 200 Bn), and others Read more

- FinTech

- Jan 2026

- Pages 138

- Report Format: PDF, Excel, PPT

Saudi Arabia Islamic Banking Software & Services Market

Projected 8.67% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 323 Million

Market Size (2032)

USD 578 Million

Base Year

2025

Projected CAGR

8.67%

Leading Segments

By Solution: Software

Saudi Arabia Islamic Banking Software & Services Market Report Key Takeaways:

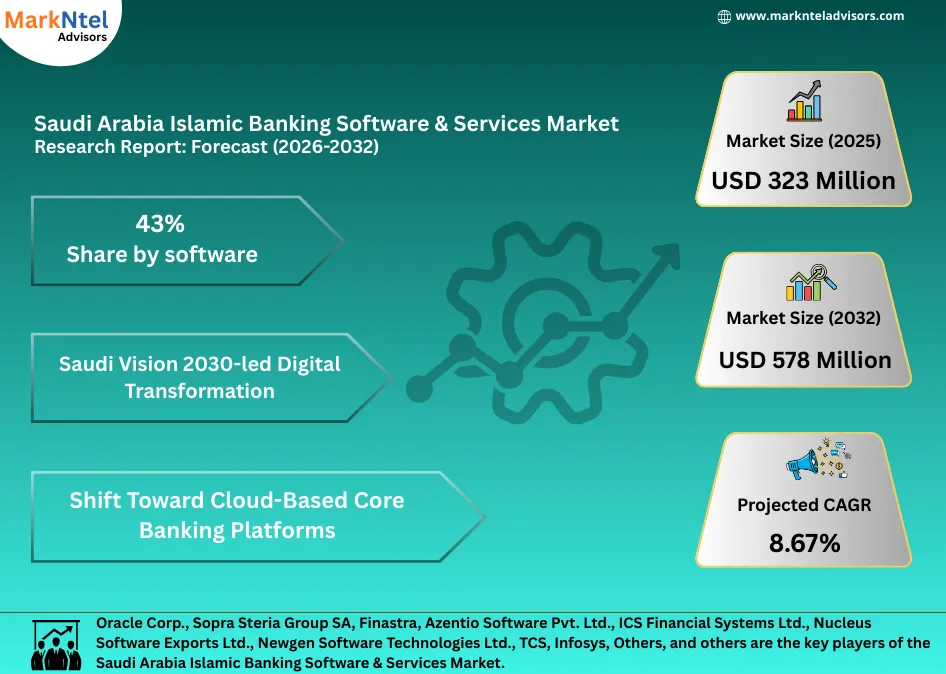

- The Saudi Arabia Islamic Banking Software & Services Market size was valued at around USD 323 million in 2025 and is projected to reach USD 578 million by 2032. The estimated CAGR from 2026 to 2032 is around 8.67%, indicating strong growth.

- By Component, the Software represented 43% of the Saudi Arabia Islamic Banking Software & Services Market size in 2025.

- By Deployment, the on-premises represented 63% of the Saudi Arabia Islamic Banking Software & Services Market size in 2025.

- The leading Islamic banking software & services companies are Oracle Corp., Sopra Steria Group SA, Finastra, Azentio Software Pvt. Ltd., ICS Financial Systems Ltd., Nucleus Software Exports Ltd., Codebase Technologies FZE, AutoSoft Dynamics Pvt. Ltd., Newgen Software Technologies Ltd., TCS, Infosys, Others, and others.

Market Insights & Analysis: Saudi Arabia Islamic Banking Software & Services Market (2026-2032):

The Saudi Arabia Islamic Banking Software & Services Market size was valued at around USD 323 million in 2025 and is projected to reach USD 578 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 8.67% during the forecast period, i.e., 2026-32. The Saudi Arabia Islamic Banking Software & Services Market is driving expansion as the Kingdom accelerates digital transformation under its national development agenda. The Saudi Central Bank (SAMA) launched the eSAMA portal in 2025, providing 23 electronic services for individuals, businesses, and government entities, digitizing regulatory interactions and reducing manual processes, which encourages financial institutions to integrate advanced software ecosystems.

The broader financial landscape reflects rapid growth in fintech activity. By the end of 2024, the number of fintech firms operating in the Kingdom reached 261, exceeding interim Vision 2030 targets and demonstrating robust momentum in digital financial services adoption, including Islamic and Sharia‑compliant solutions. Strategic collaborations such as the ACI‑iNet partnership are strengthening digital payment infrastructure to handle an anticipated 1 million cashless transactions annually by 2028, underpinning the need for scalable, secure Islamic banking platforms and compliance tools.

Core system modernization through cloud‑enabled platforms is gaining traction in Saudi financial institutions. Alinma Bank is modernizing its digital banking via IBM Cloud Pak® and Red Hat OpenShift, enabling API marketplaces for fintech integration, while Saudi EXIM Bank deployed Temenos’ cloud‑native core banking solution to modernize transaction processing and enhance customer experience trends that inevitably spill over into Islamic banking demands.

Overall, expansion of digital regulatory infrastructure, increased fintech participation, and scalable cloud core banking platforms will continuously elevate demand for Sharia‑compliant software from digital onboarding and risk engines to API‑driven products, driving long‑term market growth. The market is thus poised for accelerated adoption, higher innovation, and deeper integration between fintech and Islamic financial institutions.

Saudi Arabia Islamic Banking Software & Services Market Recent Developments:

- October 2025: Saudi Arabia reached a 79% cashless transaction rate, exceeding targets. With over 280 fintech firms, many offering Sharia-compliant services, demand for Islamic banking software surged, including payment gateways, wallets, digital onboarding, risk management, and AML solutions, as banks upgraded systems to support growing digital transactions.

- November 2025: Mambu, a cloud-native core banking platform, teamed up with Saudi Islamic fintech Ta3meed to power its automated Purchase Order (PO) financing platform. The collaboration accelerates Islamic fintech adoption by integrating digital core technology with Sharia-compliant SME financing, supporting Vision 2030’s financial inclusion goals.

Saudi Arabia Islamic Banking Software & Services Market Scope:

| Category | Segments |

|---|---|

| By Component | Software (By type of banking, Retail Banking, Wholesale Banking, Private Banking, Universal Banking) |

| By type of Solution, | Core Banking Solutions, Customer Relationship Management, Payment Processing & Digital Channels, Risk & Compliance Management, Trade & Treasury Management, Liquidity & Asset Management, Wealth & Fund Management, Analytics & Reporting Tools), Services, (Professional Services, Managed Services) |

| By Deployment | On-premises, Cloud- Based) |

| By Bank Type | Tier 1 Bank (Asset Size > USD 200 Bn), Tier 2 Bank (USD 100-200 Bn), Tier 3 Bank (Less Than USD 200 Bn), and others |

Saudi Arabia Islamic Banking Software & Services Market Drivers:

Saudi Vision 2030-led Digital Transformation

Saudi Vision 2030, the Kingdom’s long-term strategic roadmap, is fundamentally reshaping the financial services landscape by aggressively promoting digital transformation across sectors, particularly banking and financial technology. Under the Financial Sector Development Program, a core Vision 2030 initiative, Saudi Arabia aims to position itself as a leading FinTech hub with 525 fintech companies operating by 2030, creating around 18,000 jobs and contributing significantly to GDP growth.

A key measurable outcome has been the dramatic shift toward digital payments. Retail digital transactions surpassed 79% of total payments by 2024, exceeding the original Vision 2030 target of 70% by 2025 ahead of schedule, according to the Saudi Central Bank (SAMA). This transformation has been supported by strategic infrastructure upgrades, including the national payment systems and open banking frameworks that enable secure, Sharia-compliant digital transactions.

In line with this agenda, SAMA launched Google Pay in September 2025 and has committed to accepting Alipay+ by 2026, enhancing cross-border digital payment options and aligning with global standards.

In 2025, Vision 2030 continues to prioritize investments in digital identity services, real-time payment systems, and international payment integrations, all of which will sustain demand for advanced Islamic banking software and services in the coming decade.

In addition, Saudi Vision 2030’s digital transformation framework not only underpins current growth in fintech and Islamic banking software but also establishes a robust, long-term foundation for continuous market expansion.

Saudi Arabia Islamic Banking Software & Services Market Trends:

Shift Toward Cloud-Based Core Banking Platforms

Saudi Arabia’s Islamic Banking Software & Services Market is adopting cloud-based core banking and financial systems to support digital transformation under Vision 2030. For example, Vision Bank, a Sharia-compliant digital bank which implemented Finastra’s cloud-native Islamic banking treasury and risk management solution as its core platform. This deployment on the cloud enhanced its asset/liability management, liquidity, foreign exchange, and capital adequacy capabilities, aligning technology with modern customer expectations and operational scalability.

The broader Saudi banking sector is witnessing a push away from traditional legacy infrastructure, driven by the growth of digital-only banks like D360 Bank, STC Bank, and Vision Bank, all of which rely on advanced digital platforms that can integrate with mobile, API, and cloud services.

According to international tech research, annual public cloud spending in Saudi Arabia is expected to reach around USD 3.9 million by 2027, growing at a CAGR of 23.4%, supported by regulatory and government cloud-enablement policies. This broader cloud adoption trend underpins core banking modernization by providing cost-effective scalability, cybersecurity enhancements, and real-time data processing needed for Islamic fintech growth.

Overall, moving core banking to cloud infrastructure enables faster product releases, greater compliance flexibility, and improved digital customer experiences essential for Islamic banks competing in the Kingdom’s digital economy.

Saudi Arabia Islamic Banking Software & Services Market Challenges:

Complex and Evolving Sharia Compliance Requirements

One of the most significant challenges facing the Saudi Arabia Islamic Banking Software & Services market is navigating complex and evolving Sharia compliance requirements. In Saudi Arabia, Islamic financial institutions must maintain internal Sharia boards that certify and govern all Sharia-compliant products and digital services, with SAMA requiring approval of board members and oversight of compliance frameworks. This decentralized model means each institution follows its own interpretation of Islamic principles, leading to variations in compliance criteria and operational complexity across banks and fintechs.

Unlike jurisdictions with a centralized Sharia authority, Saudi Arabia’s Sharia governance is framed by SAMA’s Shariah Governance Framework and related disclosure requirements. These rules demand rigorous documentation, separate accounting for Sharia-compliant operations, internal audits, and compliance mechanisms that must be updated regularly to reflect changing interpretations and market practices.

Further complicating matters, there is no unified national Sharia standard in the Kingdom, requiring institutions to continually align digital products such as Islamic fintech platforms and software modules with diverse internal board decisions and regulatory expectations. Fragmented disclosures and differing interpretations have been noted as persisting issues despite improvements in governance standards.

The need to frequently update software logic to reflect varying Sharia rulings, ensure audit trails, and meet multiple compliance criteria increases development costs and time-to-market for Islamic banking solutions. This complexity remains a key constraint on product innovation and seamless software deployment across the market.

Saudi Arabia Islamic Banking Software & Services Market (2026-32) Segmentation Analysis:

The Saudi Arabia Islamic Banking Software & Services Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on the Solution

- Software

- By Type of Banking

- Retail Banking

- Wholesale Banking

- Private Banking

- Universal Banking

- By Type of Solution

- Core Banking Solutions

- Customer Relationship Management

- Payment Processing & Digital Channels

- Risk & Compliance Management

- Trade & Treasury Management

- Liquidity & Asset Management

- Wealth & Fund Management

- Analytics & Reporting Tools

- By Type of Banking

- Services

- Professional Services

- Managed Services

The software component dominates the market with a 43% share due to its central role in enabling end-to-end digital banking operations. Banks increasingly rely on advanced software platforms to manage Sharia-compliant products, customer data, transactions, and regulatory reporting efficiently. Within software, universal banking solutions hold nearly 40% share as they support multiple banking models, retail, wholesale, and private banking, on a single integrated platform. This reduces operational complexity while ensuring consistent compliance across diverse Islamic financial products. Growing demand for core banking modernization, real-time payment processing, risk and compliance automation, and analytics-driven decision-making further strengthens software adoption. Additionally, regulatory pressure for transparency and accurate reporting has increased investments in compliance and reporting tools. Software solutions also offer scalability, faster product launches, and improved customer experience, making them essential for banks aiming to remain competitive. As digital transformation accelerates, software continues to receive higher budget allocations than services.

Based on Deployment

- On-premises

- Cloud-Based

On-premises deployment leads the market with a 63% share primarily due to data security, regulatory control, and customization requirements. Many banks prefer on-premises systems to maintain full ownership of sensitive financial and customer data, especially in markets with strict data residency and Sharia governance regulations. On-premises infrastructure allows banks to customize systems extensively to align with complex Islamic finance structures, approval workflows, and internal Sharia board requirements. Large and established banks with legacy systems also find on-premises deployment more compatible with existing IT architectures, reducing migration risks and operational disruptions. Additionally, concerns around cybersecurity, third-party cloud dependence, and long-term compliance assurance encourage banks to retain in-house systems. Despite higher upfront costs, on-premises solutions offer predictable performance, lower regulatory uncertainty, and greater control over upgrades and audits. These factors collectively sustain strong demand for on-premises deployment across the banking sector.

Saudi Arabia Islamic Banking Software & Services Market (2026-32): Regional Projection

The market for Islamic banking software and services in Saudi Arabia is dominated by the Central Region, particularly Riyadh. This region hosts the headquarters of major Islamic banks, regulators, and technology decision-makers, making it the primary hub for large-scale digital transformation investments. Institutions such as Al Rajhi Bank, Saudi National Bank, and Riyadh Bank manage complex Sharia-compliant operations that require advanced core banking, risk, and compliance software. Riyadh also houses key regulatory bodies, including the Saudi Central Bank and Vision 2030 program offices, accelerating software adoption through regulatory reforms and digital mandates.

The presence of global and local IT service providers further strengthens implementation capabilities and managed services demand. Higher IT budgets, early adoption of cloud and analytics, and large Tier-1 bank concentration give the Central Region a clear advantage. As national digital finance initiatives expand, Riyadh continues to drive the market.

Gain a Competitive Edge with Our Saudi Arabia Islamic Banking Software & Services Market Report

- Saudi Arabia Islamic Banking Software & Services Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Saudi Arabia Islamic Banking Software & Services Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Saudi Arabia Islamic Banking Software & Services Market Policies, Regulations, and Product Standards

- Saudi Arabia Islamic Banking Software & Services Market Trends & Developments

- Saudi Arabia Banking Software Deals Signed, 2022-2025

- By Software Provider

- Deal Size

- Bank Involved

- Deal Inclusions

- Type of Software Signed

- Saudi Arabia Islamic Banks Technology Providers Details, 2025

- Core Banking Software

- Payment Platforms

- Digital Banking

- AI & Analytics

- Others

- Saudi Arabia Islamic Banking Software & Services Market Dynamics

- Growth Drivers

- Challenges

- Saudi Arabia Islamic Banking Software & Services Market Hotspot & Opportunities

- Saudi Arabia Islamic Banking Software & Services Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Component- Market Size & Forecast 2022-2032F, USD Million

- Software

- By type of banking

- Retail Banking

- Wholesale Banking

- Private Banking

- Universal Banking

- By type of Solution

- Core Banking Solutions

- Customer Relationship Management

- Payment Processing & Digital Channels

- Risk & Compliance Management

- Trade & Treasury Management

- Liquidity & Asset Management

- Wealth & Fund Management

- Analytics & Reporting Tools

- By type of banking

- Services

- Professional Services

- Managed Services

- Software

- By Deployment

- On-premises- Market Size & Forecast 2022-2032F, USD Million

- Cloud- Based- Market Size & Forecast 2022-2032F, USD Million

- By Bank Type

- Tier 1 Bank (Asset Size > USD 200 Bn)- Market Size & Forecast 2022-2032F, USD Million

- Tier 2 Bank (USD 100-200 Bn)- Market Size & Forecast 2022-2032F, USD Million

- Tier 3 Bank (Less Than USD 200 Bn)- Market Size & Forecast 2022-2032F, USD Million

- By Region

- Riyadh

- Jeddah

- Damam

- Rest of Saudi Arabia

- By Company

- Company Revenue Shares

- Competitor Characteristics

- By Component- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Outlook

- Saudi Arabia Tier 1 Bank (Asset Size > USD 200 Bn) Islamic Banking Software & Services Market Outlook, 2022-2032

- Market Size & Analysis

- Market Share & Analysis

- By Component - Market Size & Forecast 2022-2032, USD Million

- By Bank Type- Market Size & Forecast 2022-2032, USD Million

- Saudi Arabia Tier 2 Bank (USD 100-200 Bn) Islamic Banking Software & Services Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- Market Share & Analysis

- By Component - Market Size & Forecast 2022-2032, USD Million

- By Bank Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Saudi Arabia Tier 3 Bank (Less Than USD 200 Bn) Islamic Banking Software & Services Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- Market Share & Analysis

- By Component - Market Size & Forecast 2022-2032, USD Million

- By Bank Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Saudi Arabia Islamic Banking Software & Services Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Oracle Corp.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Sopra Steria Group SA

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Finastra

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Azentio Software Pvt. Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- ICS Financial Systems Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Nucleus Software Exports Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Codebase Technologies FZE

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- AutoSoft Dynamics Pvt. Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Newgen Software Technologies Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- TCS

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Infosys

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Oracle Corp.

- Imal

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now