India Alcoholic Drinks Market Research Report: Forecast (2026-2032)

India Alcoholic Drinks Market - By Product Type (Indian Made Foreign Liquor (IMFL), Beer, Wine, Spirits, Whisky, Rum, Vodka, Others, Others), By Distribution Channel (On-trade, Off ... -trade, Online Retailers), By End-User (Household, Commercial), and others Read more

- Food & Beverages

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

India Alcoholic Drinks Market

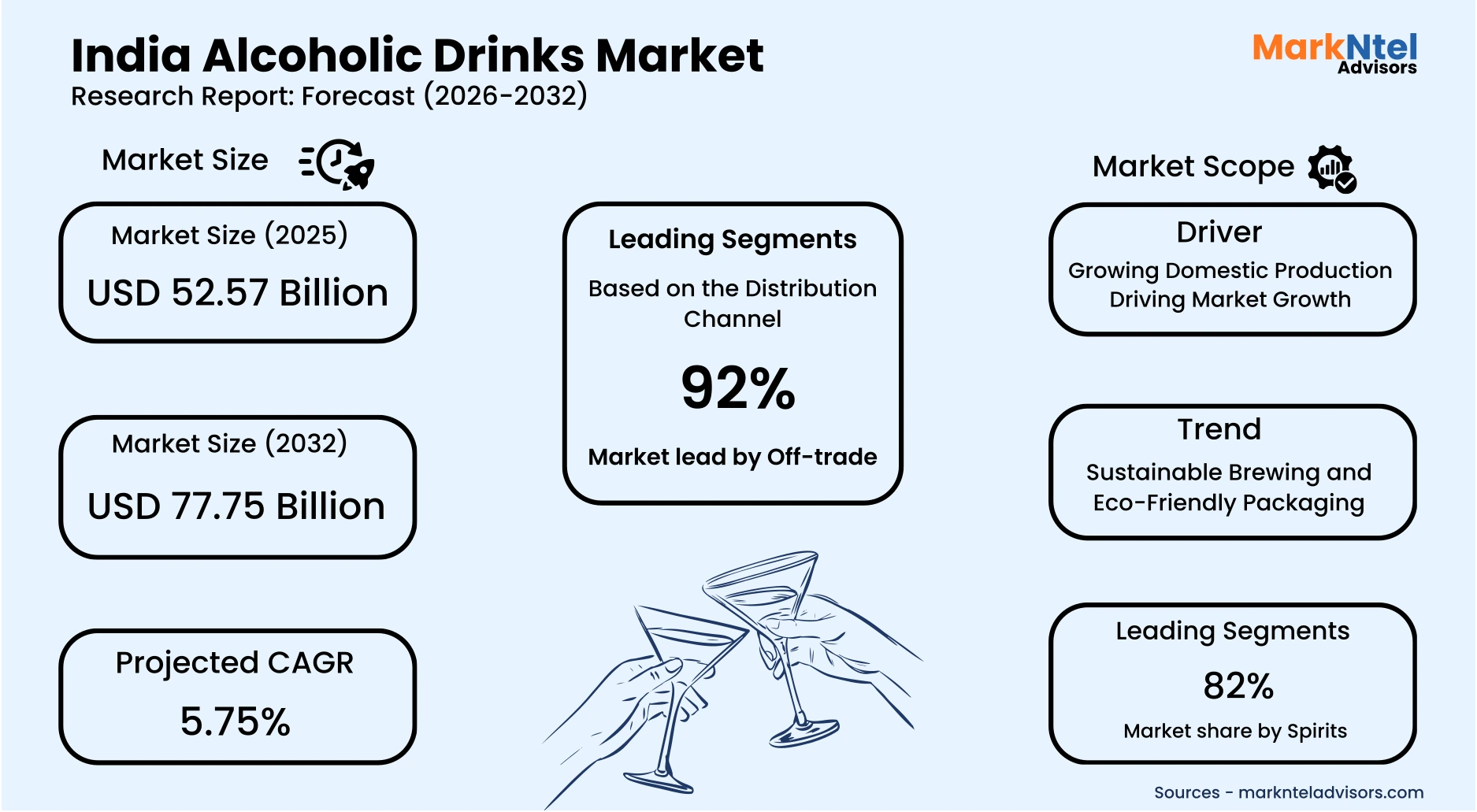

Projected 5.75% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 52.57 Billion

Market Size (2032)

USD 77.75 Billion

Base Year

2025

Projected CAGR

5.75%

Leading Segments

By Distribution Channel: Off-trade

India Alcoholic Drinks Market Report Key Takeaways:

- Market size was valued at around USD52.57 billion in 2025 and is projected to reach USD77.75 billion by 2032. The estimated CAGR from 2026 to 2032 is around 5.75%, indicating strong growth.

- The western region holds the largest market share of about 32% in the India Alcoholic Drinks Market in 2025.

- By Product Type, the Spirits segment represented a significant share of about 82% in the India Alcoholic Drinks Market in 2025.

- By Distribution Channel, the Off-Trade segment presented a significant share of about 92% in the India Alcoholic Drinks Market in 2025.

- Leading Alcoholic Drinks Companies in India are United Spirits Ltd., Radico Khaitan Ltd., Sula Vineyards Ltd., Pernod Ricard India Pvt. Ltd., Amrut Distilleries Pvt. Ltd., Allied Blenders & Distillers Pvt. Ltd., United Breweries Ltd., Tilaknagar Industries Ltd., Piccadily Agro Industries Ltd., and Others.

Market Insights & Analysis: India Alcoholic Drinks Market (2026-32):

The India Alcoholic Drinks Market size was valued at around USD52.57 billion in 2025 and is projected to reach USD77.75 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.75% during the forecast period, i.e., 2026-32.

India’s Alcoholic Drinks sector is expanding steadily, supported by rising disposable incomes, urban lifestyles, and a visible shift toward premium and branded drinks. For instance, in 2023, as per the U.S. Department of Agriculture, FAS 2024, India’s imports of alcoholic beverages reached about USD1 billion, marking a 74 % year-on-year increase, largely driven by growing consumer interest in quality and international brands. Similarly, recorded pure alcohol consumption in India touched nearly 3.24 billion liters in 2023, reflecting strong domestic demand across beer, wine, and other alcoholic categories.

Whereas, per-capita consumption remains modest, averaging around 3.2 liters of pure alcohol per adult per year, which is below the global average of 5 liters, indicating substantial long-term growth potential. Additionally, the sector plays a crucial fiscal role, which includes state excise duties on alcohol, forming one of the largest sources of tax revenue, with several states reporting annual earnings exceeding USD5–6 billion from this segment.

Furthermore, the market’s value is expected to expand faster than volumes as consumers opt for higher-quality options, ready-to-drink formats, and premium beer and wine categories. However, fragmented state regulations, high taxation, and complex licensing frameworks continue to challenge consistent nationwide growth. Overall, this market stands on a strong growth trajectory, supported by demographic trends, rising affluence, and expanding product innovation.

India Alcoholic Drinks Market Recent Developments:

- April 2025: Amrut Distilleries expanded its production capacity by around 35%, boosting its distillation output from 900,000 to about 1.4 million liters. This expansion strengthens the premium whisky manufacturing base in India, supporting export growth and increasing the share of India in the global single-malt segment, while encouraging domestic premiumization trends.

- July 2025: Tilaknagar Industries received regulatory approval to acquire Imperial Blue whisky division of Pernod Ricard, marking a major portfolio expansion. This deal enhances the position of this company in the mass-premium whisky category, boosts competition among domestic producers, and supports consolidation within the spirits market, fostering stronger local brand presence against global players.

India Alcoholic Drinks Market Scope:

| Category | Segments |

|---|---|

| By Product Type | Indian Made Foreign Liquor (IMFL), Beer, Wine, Spirits, Whisky, Rum, Vodka, Others, Others), |

| By Distribution Channel | On-trade, Off-trade, Online Retailers |

| By End-User | Household, Commercial), and others |

India Alcoholic Drinks Market Driver:

Growing Domestic Production Driving Market Growth

India’s alcoholic drinks industry is gaining momentum through large-scale production expansion and rising international visibility. For reference, in April 2025, Amrut Distilleries Pvt. Ltd. announced a 35% boost in distillation capacity, increasing annual output from 900,000 to 1.4 million liters to cater to rising domestic and export demand (Ambrosia India, 2025). Similarly, Allied Blenders & Distillers Ltd. committed around USD60 million toward setting up a single-malt whisky facility and enhancing in-house malt and packaging operations.

Additionally, Indian premium whisky brands such as Amrut and Rampur have earned prestigious international awards, elevating India’s image as a producer of world-class spirits. These developments highlight how strategic investments and global recognition are transforming India into a key producer and exporter in the global alcoholic beverages industry.

Government Support and Policy Reforms

Government initiatives play a crucial role in shaping and supporting India’s Alcoholic Drinks Industry, primarily through fiscal frameworks and industrial policy reforms. Alcohol excise remains a major state revenue source, contributing between 10–15 % of total state tax receipts, as reported by the Reserve Bank of India’s State Finances in 2024. Consequently, state governments like Maharashtra, Uttar Pradesh, and Karnataka are reforming excise structures to enhance transparency, simplify licensing, and attract private investment. For instance, Delhi’s revised 2025 excise model increased retail sales revenue by nearly 85 % year-on-year.

Similarly, the Ministry of Food Processing Industries (2024) has encouraged ethanol and grain-based distilleries under the Atmanirbhar Bharat initiative, supporting modernization and value addition in the beverage sector. These policy measures, focused on formalization, infrastructure, and investment, collectively strengthen the regulatory and industrial ecosystem, driving sustainable growth in India’s alcoholic beverage industry.

India Alcoholic Drinks Market Trend:

Sustainable Brewing and Eco-Friendly Packaging

Sustainability is becoming a defining trend in India’s Alcoholic Drinks Market, as producers align with national environmental goals. Under the Government of India’s “Green Manufacturing” Mission (2024), major beverage companies are integrating renewable energy and water-saving systems into their operations. For instance, United Breweries Ltd. reports that over 55% of its energy now comes from renewable sources, and it recycles nearly 3.5 billion liters of water annually across its breweries.

Likewise, Pernod Ricard India has introduced 100% recyclable glass bottles and aims to achieve net-zero carbon emissions by 2030, in line with its global sustainability roadmap. Several state governments, including Karnataka and Maharashtra, have also introduced incentives for low-carbon manufacturing and waste reduction in beverage units. These combined efforts highlight a shift toward greener production, positioning sustainability as a long-term competitive advantage in India’s Alcoholic Drinks Industry.

India Alcoholic Drinks Market Challenge:

Illicit Trade and Restrictive State Policies

A major challenge in the alcoholic drinks market stems from illicit trade and restrictive state-level policies. According to a 2023 report by the Transnational Alliance to Combat Illicit Trade (TRACIT), nearly 30–35% of alcohol consumed in India is unrecorded, leading to government revenue losses exceeding USD3 billion annually and posing serious health risks due to unsafe production. Additionally, several states, such as Bihar and Gujarat, maintain total prohibition, while others periodically tighten or alter liquor sale regulations. For instance, Bihar’s ban on alcohol since 2016 has not only curtailed formal market expansion but also spurred the growth of illegal supply networks. These combined factors distort market competition, reduce legitimate sales, and deter investment from organized players.

India Alcoholic Drinks Market (2026-32) Segmentation Analysis:

The India Alcoholic Drinks Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the India level. Based on the analysis, the market has been further classified as;

Based on Product Type

- Indian Made Foreign Liquor (IMFL)

- Beer

- Wine

- Spirits

- Whisky

- Rum

- Vodka

- Others

Spirits dominate India’s Alcoholic Drinks Market, both in volume and value terms, accounting for more than 82% market share, reflecting strong cultural preference and established domestic production. According to the U.S. Department of Agriculture (FAS, 2024), whisky alone accounts for nearly two-thirds of all spirits sales in India, making it the largest alcoholic beverage category nationwide.

Similarly, over 82% of India’s total recorded pure-alcohol consumption originates from distilled spirits, compared with less than 15% from beer and wine combined. The dominance of Indian Made Foreign Liquor (IMFL), including whisky, rum, vodka, and brandy, stems from robust local manufacturing networks and strong demand in urban and semi-urban regions.

Based on the Distribution Channel

- On-trade

- Off-trade

- Online Retailers

The off-trade distribution channel, which holds the largest market share of about 92%, encompassing licensed retail outlets and state-authorized liquor stores, remains the primary driver of alcohol sales in India. This dominance stems from strong consumer dependence on retail purchases, competitive pricing, and widespread market accessibility. For instance, excise data from Delhi’s government (2025) reported an 85% year-on-year increase in revenue from retail liquor outlets, rising from approximately USD312 million to USD366 million, underscoring the channel’s fiscal and commercial significance.

Additionally, ahead of major festivals such as Diwali, retail stores across India recorded a 25–30% surge in whisky and rum sales, reflecting strong seasonal consumption patterns. Moreover, in Telangana, the overwhelming 95,000 applications for about 2,000 retail shop licenses further highlight the economic weight of this channel. Collectively, these indicators affirm that off-trade retail remains the dominant and most resilient distribution network in India’s alcoholic drinks market.

India Alcoholic Drinks Market (2026-32): Regional Projection

The western region, led by Maharashtra, remains the powerhouse of India’s Alcoholic Drinks Market with a market share of about 32% due to its high production capacity, strong fiscal base, and growing consumer demand. In FY 2023–24, Maharashtra generated approximately USD2.8 billion in excise revenue from alcohol, marking an 8% annual increase. Additionally, districts such as Nashik, Sambhaji Nagar, and Pune together contributed nearly USD1.95 billion, reflecting widespread consumption and an efficient distribution network. Moreover, in 2025, the state government revised excise duties, increasing levies on Indian-Made Foreign Liquor (IMFL) by up to 4.5 times the manufacturing cost, which is projected to add about USD1.7 billion in yearly revenue. This fiscal policy not only enhances state earnings but also strengthens regulatory control and encourages responsible, formalized trade.

Additionally, Maharashtra’s industrial ecosystem hosts major producers such as United Breweries and Radico Khaitan, enabling a consistent supply across western India. Together, these economic, policy, and production strengths firmly establish the western region as the central growth driver of India’s Alcoholic Drinks Industry.

Gain a Competitive Edge with Our India Alcoholic Drinks Market Report

- India Alcoholic Drinks Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- India Alcoholic Drinks Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- India Alcoholic Drinks Market Policies, Regulations, and Product Standards

- India Alcoholic Drinks Market Supply Chain Analysis

- India Alcoholic Drinks Market Supply Strategic Insights

- India Alcoholic Drinks Market Supply Pricing Analysis

- India Alcoholic Drinks Market Trends & Developments

- India Alcoholic Drinks Market Dynamics

- Growth Drivers

- Challenges

- India Alcoholic Drinks Market Hotspot & Opportunities

- India Alcoholic Drinks Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Product Type

- Indian Made Foreign Liquor (IMFL) – Market Size & Forecast 2022–2032, Million Tons

- Beer – Market Size & Forecast 2022–2032, Million Tons

- Wine – Market Size & Forecast 2022–2032, Million Tons

- Spirits– Market Size & Forecast 2022–2032, Million Tons

- Whisky – Market Size & Forecast 2022–2032, Million Tons

- Rum – Market Size & Forecast 2022–2032, Million Tons

- Vodka – Market Size & Forecast 2022–2032, Million Tons

- Others– Market Size & Forecast 2022–2032, Million Tons

- Others – Market Size & Forecast 2022–2032, USD Million

- By Distribution Channel

- On-trade– Market Size & Forecast 2022–2032, Million Tons

- Off-trade– Market Size & Forecast 2022–2032, Million Tons

- Online Retailers – Market Size & Forecast 2022–2032, Million Tons

- By End-User

- Household – Market Size & Forecast 2022–2032, Million Tons

- Commercial– Market Size & Forecast 2022–2032, Million Tons

- By Region

- North

- West

- South

- East

- Central

- By Product Type

- Market Size & Outlook

- India On-Trade Alcoholic Drinks Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Distribution Channel-Market Size & Forecast 2022–2032, Million Tons

- By Product Type-Market Size & Forecast 2022–2032, Million Tons

- Market Size & Outlook

- India Off-Trade Alcoholic Drinks Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Distribution Channel-Market Size & Forecast 2022–2032, Million Tons

- By Product Type-Market Size & Forecast 2022–2032, Million Tons

- Market Size & Outlook

- India Online Alcoholic Drinks Market Outlook, 2022–2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Tons)

- Market Share & Outlook

- By Distribution Channel-Market Size & Forecast 2022–2032, Million Tons

- By Product Type-Market Size & Forecast 2022–2032, Million Tons

- Market Size & Outlook

- India Alcoholic Drinks Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- United Spirits Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Radico Khaitan Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Sula Vineyards Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Pernod Ricard India Pvt Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Amrut Distilleries Pvt Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Allied Blenders & Distillers Pvt Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- United Breweries Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Tilaknagar Industries Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Piccadily Agro Industries Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- United Spirits Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now