GCC Diagnostic Labs Market Research Report: Forecast (2026-2032)

GCC Diagnostic Labs Market - By Test Type (Pathology, Radiology & Imaging), By Pathology Test Type (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathol ... ogy & Cytopathology, Molecular Diagnostics, Genetic Testing), By Radiology Type (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), By Service Delivery Mode (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), By Disease Type (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), By End-User (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), and others Read more

- Healthcare

- Feb 2026

- Pages 138

- Report Format: PDF, Excel, PPT

GCC Diagnostic Labs Market

Projected 4.87% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 4.65 Billion

Market Size (2032)

USD 7.69 Billion

Base Year

2025

Projected CAGR

4.87%

Leading Segments

By End-User: Hospitals

GCC Diagnostic Labs Market Report Key Takeaways:

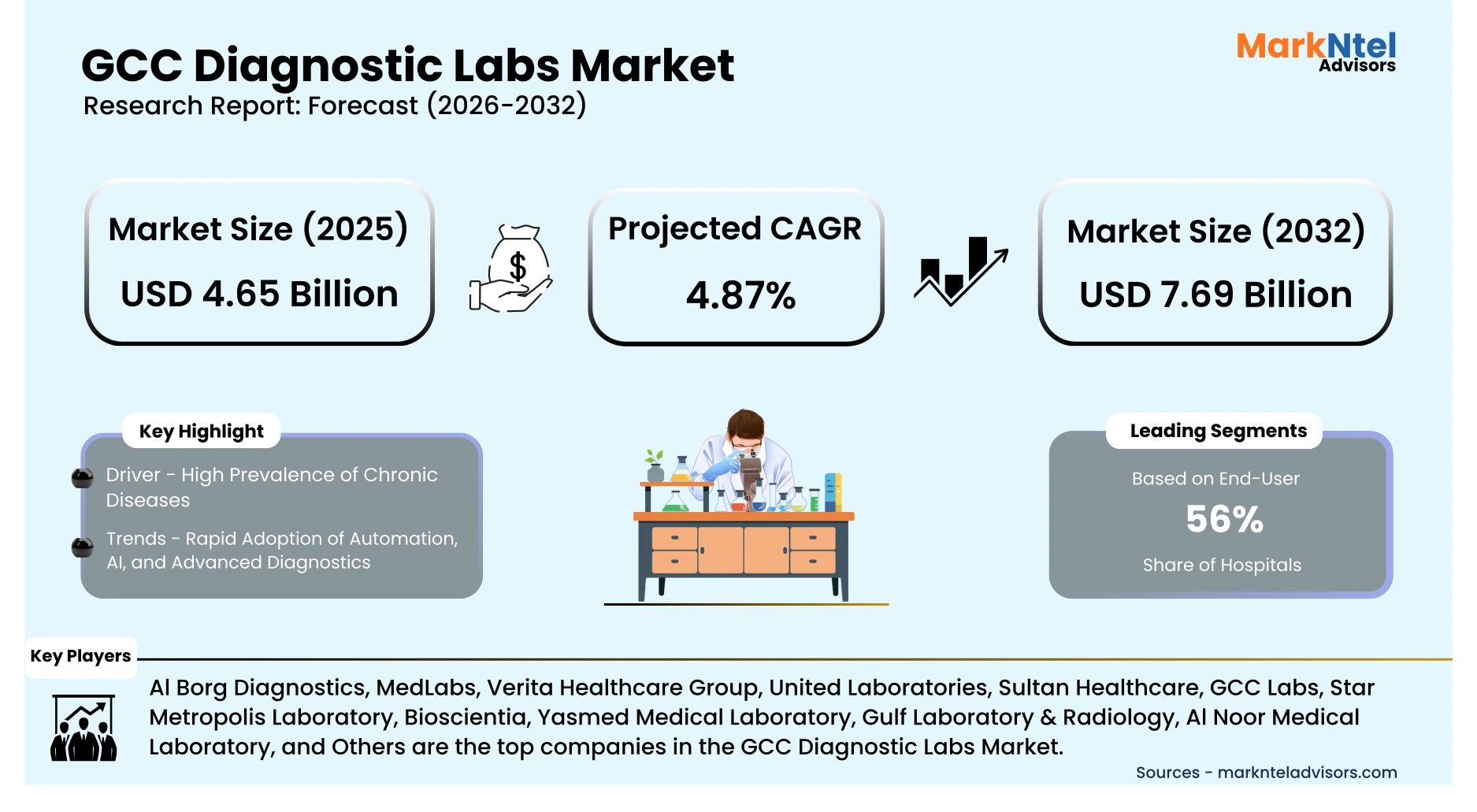

- Market size was valued at around USD4.65 billion in 2025 and is projected to reach USD7.69 billion by 2032. The estimated CAGR from 2026 to 2032 is around 4.87%, indicating strong growth.

- Saudi Arabia holds the largest market share of about 48% in the GCC Diagnostic Labs Market in 2025.

- By Pathology Type, the Clinical Chemistry segment represented a significant share of about 52% in the GCC Diagnostic Labs Market in 2025.

- By End-User, the Hospitals presented a significant share of about 56% in the GCC Diagnostic Labs Market in 2025.

- Leading Diagnostic Labs Companies in the GCC Market are GC Labs, Al Borg Diagnostics, MedLabs, Verita Healthcare Group, United Laboratories, Sultan Healthcare, GCC Labs, Star Metropolis Laboratory, Thumbay Labs, Thyrocare Gulf Laboratories WLL, Bioscientia, Yasmed Medical Laboratory, Gulf Laboratory & Radiology, Al Noor Medical Laboratory, and Others.

Market Insights & Analysis: GCC Diagnostic Labs Market (2026-32):

The Diagnostic Labs Market size was valued at around USD4.65 billion in 2025 and is projected to reach USD7.69 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 4.87% during the forecast period, i.e., 2026-32.

The market is witnessing strong expansion due to rising chronic disease prevalence, growing preventive screening uptake, and structural healthcare reforms across Saudi Arabia, the UAE, Qatar, and Oman. According to Saudi Arabia’s Ministry of Health, non-communicable diseases account for over 73% of total deaths, significantly driving routine pathology and biochemistry testing demand.

Additionally, GCC governments are increasing healthcare expenditure to reduce diagnostic outsourcing and improve local capacity. As per the UAE Federal Budget 2024 data, healthcare allocations exceeded USD5.7 billion , with diagnostics identified as a core service under hospital modernization programs. Likewise, large hospital groups are centralizing lab operations to optimize costs and improve turnaround time.

Manufacturing and infrastructure investments further strengthen market momentum. For instance, Saudi Vision 2030 has enabled multi-million-dollar greenfield diagnostic hubs linked to tertiary hospitals, supporting high-throughput testing platforms. Similarly, Qatar’s Public Works Authority continues healthcare infrastructure expansion under its National Vision 2030, boosting laboratory demand.

The growth is supported by automation adoption, molecular diagnostics penetration, and hospital-led testing volumes. Increasing deployment of automated analyzers, LIS integration, and molecular platforms for oncology and infectious disease testing is structurally reshaping diagnostic workflows across the region.

GCC Diagnostic Labs Market Recent Developments:

- 2025 : Thumbay Labs launched the Thumbay Lab for AI in Healthcare within Gulf Medical University, a major initiative in the UAE advancing AI-driven diagnostic innovation and research, and signed new AI collaboration MOUs, reinforcing tech integration in the region.

- 2024 : Al-Borg showcased advanced genetic testing technologies and the first electronic microscope unit in the private health sector at the Global Health Forum in Riyadh, reinforcing tech adoption in the GCC.

GCC Diagnostic Labs Market Scope:

| Category | Segments |

|---|---|

| By Test Type | Pathology, Radiology & Imaging |

| By Pathology Test Type | Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecular Diagnostics, Genetic Testing |

| By Radiology Type | X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others |

| By Service Delivery Mode | Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units |

| By Disease Type | Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others |

| By End-User | Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions |

GCC Diagnostic Labs Market Driver:

High Prevalence of Chronic Diseases

The steadily rising prevalence of chronic diseases such as diabetes, cancer, cardiovascular diseases, etc., across GCC countries is creating a continuous and long-term demand cycle for diagnostic laboratory services, as these conditions require lifelong monitoring rather than one-time diagnosis. Diabetes represents the strongest volume driver, with adult prevalence rates remaining among the highest globally.

According to recent International Diabetes Federation data, diabetes affects approximately 25.6% of adults in Kuwait, 24.6% in Qatar, 23.1% in Saudi Arabia, 23.1% in Bahrain, 20.7% in the UAE, and 17.0% in Oman . This widespread prevalence directly translates into recurring demand for glucose, HbA1c, lipid profiles, renal panels, and electrolyte testing, anchoring high utilization of clinical chemistry laboratories.

As diabetes prevalence increases, it simultaneously accelerates cardiovascular disease (CVD) incidence, strengthening another major diagnostic demand stream. Regional health studies identify cardiovascular diseases as the leading cause of chronic disease, related morbidity, and mortality across Saudi Arabia, the UAE, Kuwait, and Oman. Management of CVD requires repeated lipid testing, coagulation assays, and cardiac biomarkers, which are largely processed through hospital-based and centralized laboratories, reinforcing hospital dominance in diagnostic utilization.

GCC Diagnostic Labs Market Trend:

Rapid Adoption of Automation, AI, and Advanced Diagnostics

The market is actively transforming due to the rapid adoption of automation, artificial intelligence (AI), and advanced diagnostic technologies to manage rising test volumes, workforce constraints, and increasing clinical complexity. The growing burden of chronic diseases, expanding preventive screening programs, and higher hospital patient inflows are collectively pushing laboratories away from manual and semi-automated workflows toward fully automated, digitalized, and centralized testing models.

For instance, in December 2025, the region’s largest AI-powered standalone diagnostic laboratory was inaugurated in Abu Dhabi. The facility can process over 30 million tests annually and uses AI-driven systems for real-time quality control, workflow optimization, and result validation. It also supports a network of more than 140 accredited laboratories, demonstrating how AI-enabled centralization improves turnaround time, accuracy, and scalability across the diagnostic ecosystem.

GCC Diagnostic Labs Market Opportunity:

Rising Investments in Healthcare Infrastructure

The expansion of centralized high-throughput reference laboratories is a natural outcome of rising healthcare demand and increasing public investment across the GCC diagnostic labs market. As chronic disease prevalence and preventive screening volumes continue to rise, governments are prioritizing infrastructure models that can process large test volumes efficiently, pushing healthcare systems away from fragmented hospital laboratories toward centralized diagnostic hubs.

In Saudi Arabia, this shift is structurally supported by large-scale public funding. Under recent national budget frameworks aligned with Vision 2030, healthcare and social development allocations reached approximately USD69 billion , positioning healthcare among the country’s highest public spending priorities. These allocations are funding new hospitals, medical cities, and regional health clusters that are designed with centralized laboratory services capable of serving multiple facilities simultaneously. As a result, routine clinical chemistry and hematology testing, along with advanced molecular diagnostics, are increasingly consolidated into shared reference laboratories, improving utilization rates and reducing per-test costs.

A similar investment-driven model is evident in Oman, where the government invested approximately USD47 million in establishing a national Central Public Health Laboratory . This facility supports high-complexity molecular, virology, and surveillance testing for public hospitals, reinforcing centralized diagnostics as a core component of national healthcare delivery. These allocations are increasing the potential market growth.

GCC Diagnostic Labs Market Challenge:

Rising Operating Costs Constraining Profitability and Scalability

Rising operating costs are a significant challenge limiting the expansion of diagnostic laboratories across the GCC, as cost pressures are increasing faster than reimbursement growth. One of the largest contributors is labour cost inflation. According to Gulf labour market data and healthcare workforce studies, salaries for skilled laboratory technologists and pathologists in Saudi Arabia and the UAE have risen due to workforce shortages and localization policies, increasing payroll expenses for diagnostic providers. In Saudi Arabia, average monthly wages for laboratory professionals translate to annual personnel costs approaching USD12,000–25,000 per technologist , excluding benefits and training.

In parallel, heavy reliance on imported diagnostic equipment and reagents further raises operating expenses. Government and regulatory publications indicate that a majority of advanced medical devices and in-vitro diagnostic consumables used in GCC countries are imported, exposing laboratories to foreign exchange fluctuations, shipping costs, customs duties, and longer procurement cycles. These factors increase per-test costs, particularly for molecular diagnostics, immunoassays, and genetic testing.

Additionally, regulatory compliance and accreditation requirements add recurring operational costs. Maintaining ISO 15189 or CAP accreditation requires continuous audits, documentation, validation studies, and external quality assessments, increasing administrative and service contract expenses. Combined with price caps and insurance reimbursement controls, these rising cost components compress margins, slow capacity expansion, and make scale, automation, and centralization essential for financial sustainability in the GCC diagnostic labs market.

GCC Diagnostic Labs Market (2026-32) Segmentation Analysis:

The GCC Diagnostic Labs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Pathology Test Type:

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

Clinical chemistry forms the core of diagnostic testing in GCC countries, with a market share of about 52%, because it directly supports the most common and recurring clinical needs across healthcare systems. The region’s high burden of chronic and lifestyle-related diseases means that diagnosis alone is not sufficient; patients require continuous biochemical monitoring. Clinical chemistry enables this by analyzing blood and urine samples to measure glucose, electrolytes, enzymes, lipids, proteins, and metabolic by-products that are essential for tracking disease progression and treatment response in conditions such as diabetes, kidney disease, liver disorders, and cardiovascular illnesses.

This clinical reliance translates into consistent demand for standardized chemistry panels across care settings. Tests such as complete metabolic panels, liver function tests, kidney function tests, and lipid profiles are routinely ordered during outpatient visits, hospital admissions, pre-operative assessments, and preventive health check-ups. Because the same patients often undergo repeated testing over long periods, clinical chemistry generates high-frequency, repeat test volumes, unlike more episodic diagnostic categories.

Based on End-User:

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

Hospitals dominate the GCC Diagnostic Laboratories Market with a market share of about 56% because healthcare delivery, funding, and referral pathways across the region are structurally hospital-centric. Additionally, GCC public hospitals such as King Faisal Specialist Hospital & Research Centre, Cleveland Clinic Abu Dhabi, Hamad General Hospital, Sidra Medicine, and Sheikh Khalifa Medical City increasingly operate centralized core labs and imaging hubs that serve multiple facilities, reinforcing hospitals as the anchor for diagnostic demand.

Moreover, the United Arab Emirates operates 173 hospitals, and these hospitals act as the first point of care for inpatient, emergency, oncology, and surgical cases, all of which require continuous laboratory and imaging support . Likewise, national hospital systems such as Qatar’s Hamad Medical Corporation function as both care providers and national referral centers, concentrating advanced diagnostics, including molecular testing, histopathology, and high-end imaging, within hospital settings rather than stand-alone labs.

Similarly, WHO-EMRO documentation highlights that GCC governments prioritize strengthening public hospital laboratory networks to ensure quality control, biosafety, and rapid turnaround for complex testing. As a result, while private diagnostic chains are expanding, hospitals remain the dominant diagnostic end-users because they control patient inflow, clinical decision-making, and government-backed infrastructure across the GCC.

Saudi Arabia Diagnostic Labs Market (2026-32): Regional Projection

Saudi Arabia dominates the GCC diagnostic laboratories market because scale, public financing, hospital capacity, and demographic change reinforce each other within a single healthcare system. For instance, Saudi Arabia accounts for around 48% of total GCC healthcare expenditure, giving the Kingdom the largest patient base, hospital footprint, and diagnostic demand in the region. Additionally, public sources remain the primary healthcare financiers, ensuring that most diagnostic testing is routed through government-funded and government-regulated hospital networks rather than fragmented stand-alone laboratories.

Additionally, Saudi Arabia operated about 499 hospitals with nearly 80,000 beds in 2023, enabling large hospitals to host high-throughput clinical chemistry, hematology, pathology, molecular diagnostics, and advanced imaging units easily accessible in one place.

Similarly, demographic trends are strengthening this dominance. For instance, Saudi Arabia’s population aged 60 years and above reached around 1.7 million people in 2025, and the share of those aged more than 65 continues to rise. Older populations require more frequent and complex diagnostic testing for oncology, cardiovascular disease, diabetes, and chronic conditions. As a result, the combination of hospital-centric delivery, rising elderly demand, and sustained public investment positions Saudi Arabia as the largest and most influential diagnostic laboratories market in the GCC.

Gain a Competitive Edge with Our GCC Diagnostic Labs Market Report:

- GCC Diagnostic Labs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Diagnostic Labs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Diagnostic Labs Market Policies, Regulations, and Product Standards

- GCC Diagnostic Labs Market Trends & Developments

- GCC Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- GCC Diagnostic Labs Market Hotspot & Opportunities

- GCC Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Pathology

- Radiology & Imaging

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- Walk-in Testing

- Home Sample Collection

- Mobile Diagnostic Units

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- Infectious Diseases

- Oncology

- Diabetes & Endocrinology

- Cardiology

- Neurology

- Nephrology

- Gastroenterology

- Gynecology & Obstetrics

- Respiratory Disorders

- Orthopedics

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

- By Country

- Saudi Arabia

- UAE

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of GCC

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Saudi Arabia Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Qatar Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Kuwait Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Oman Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Bahrain Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- GCC Diagnostic Labs Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Al Borg Diagnostics, MedLabs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Verita Healthcare Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- United Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sultan Healthcare

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GCC Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Star Metropolis Laboratory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thumbay Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thyrocare Gulf Laboratories WLL

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bioscientia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yasmed Medical Laboratory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gulf Laboratory & Radiology

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Noor Medical Laboratory

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Borg Diagnostics, MedLabs

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now