GCC Bottled Water Market Research Report: Trends & Forecast (2026-2032)

By Category (Still Bottled Water, Functional Bottled Water, Flavored Bottled Water, Carbonated Bottled Water), By Packaging (Flexible Packaging, (Aluminum, Pouches, Glass, Rigid Pl ... astic, PET Bottles, Thin Wall Plastic Containers), By Sub Types (Purified, Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other), By Price Category (Budget, Economy, Premium), By Pack Size (100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others), By Sales Channel (Direct Sales/On Trade, (Restaurants, Hotels, Cafes, Other), Retail Sales, (Grocery Retailers, Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer, Non-Grocery Retailers, General Merchandise Stores, Health and Beauty Specialists, Vending, E-commerce),and others Read more

- FMCG

- Feb 2026

- Pages 250

- Report Format: PDF, Excel, PPT

GCC Bottled Water Market

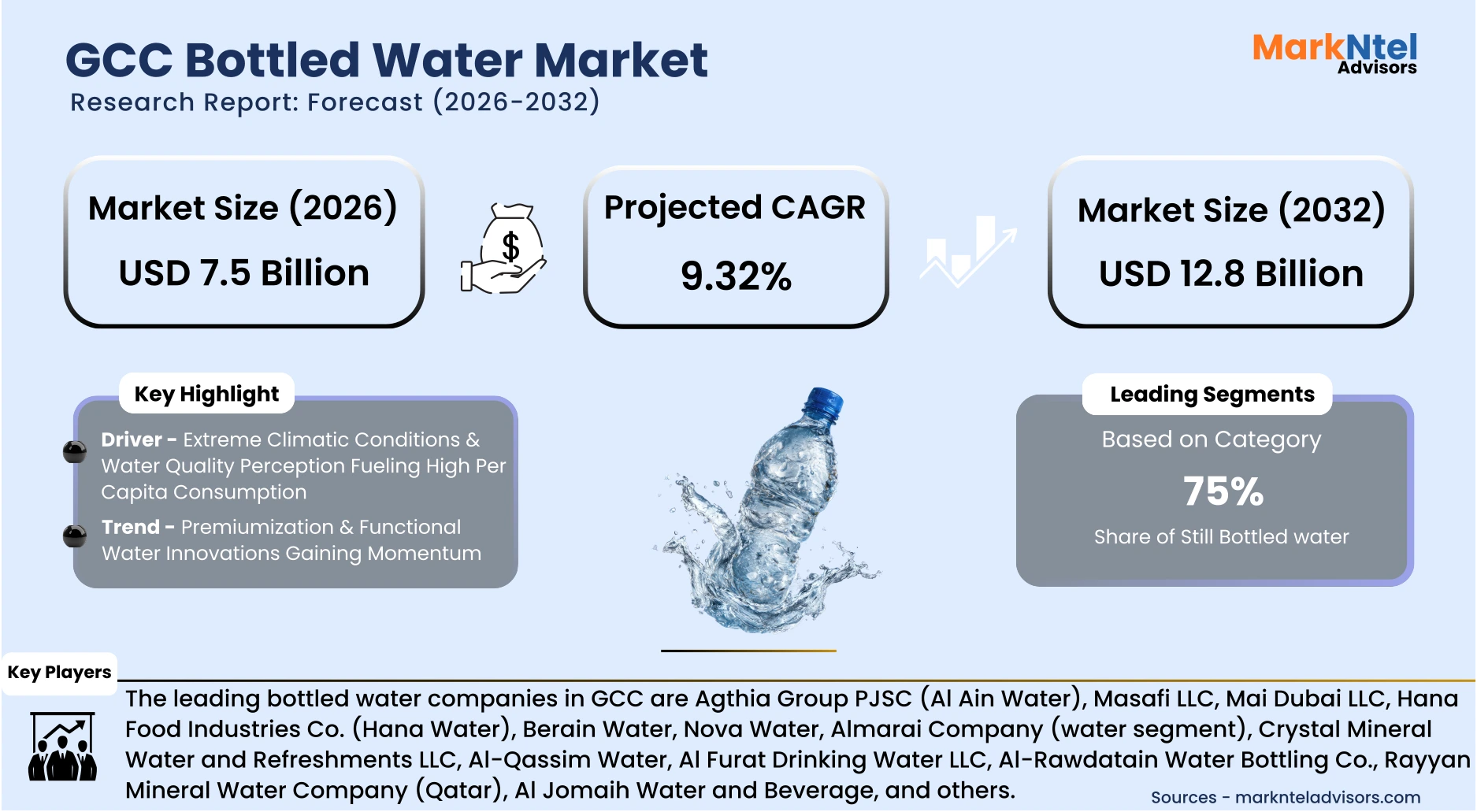

Projected 9.32% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 7.5 Billion

Market Size (2032)

USD 12.8 Billion

Base Year

2025

Projected CAGR

9.32%

Leading Segments

By Category: Still Bottled Water

GCC Bottled Water Market Report Key Takeaways:

- The GCC Bottled Water market size was valued at USD 5.8 billion in 2025 and is projected to grow from USD 7.5 billion in 2026 to USD 12.8 billion by 2032. The estimated CAGR from 2026 to 2032 is around 9.32%, indicating strong growth.

- By Category, the still bottled water dominates the GCC Bottled Water Market, accounting for approximately 75% of the total market size in 2026, due to strong consumer preference for plain hydration, widespread availability, and affordability.

- By Packaging, the rigid plastic packaging leads the market in 2026, owing to its lightweight nature, durability, and cost efficiency.

- The leading bottled water companies in GCC are Agthia Group PJSC (Al Ain Water), Masafi LLC, Mai Dubai LLC, Hana Food Industries Co. (Hana Water), Berain Water, Nova Water, Almarai Company (water segment), Crystal Mineral Water and Refreshments LLC, Al-Qassim Water, Al Furat Drinking Water LLC, Al-Rawdatain Water Bottling Co., Rayyan Mineral Water Company (Qatar), Al Jomaih Water and Beverage, and others.

Market Insights & Analysis: GCC Bottled Water Market (2026-32):

The GCC Bottled Water market size was valued at USD 5.8 billion in 2025 and is projected to grow from USD 7.5 billion in 2026 to USD 12.8 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 9.32% during the forecast period, i.e., 2026-32.

The market growth is significantly supported by large-scale infrastructure and tourism investments under national diversification strategies. In Saudi Arabia, the government’s Saudi Vision 2030 framework has catalyzed a broad pipeline of giga-projects reshaping the country’s economic and built environment. Major initiatives such as Red Sea Global (USD 23.6 billion) and Qiddiya (USD 9.8 billion), alongside other large hospitality and residential developments, are expanding tourism infrastructure, entertainment districts, and mixed-use communities. These projects significantly increase demand for packaged drinking water across construction activities, workforce accommodations, hotels, and commercial establishments.

In the United Arab Emirates, strategic economic frameworks such as the Dubai Economic Agenda (D33) and UAE Vision 2031 outline long-term plans to double economic output by 2033 and 2031, respectively. Under D33, Dubai targets approximately USD 8.7 trillion in cumulative economic output, aims to expand foreign trade to nearly USD 7 trillion, and seeks to attract around USD 177 billion in foreign direct investment over the decade. These initiatives include more than 100 transformational projects across logistics, tourism, real estate, and digital infrastructure, reinforcing consumption demand in retail outlets, hospitality facilities, corporate offices, and large-scale events, key channels for bottled water distribution.

Furthermore, Saudi Arabia’s Saline Water Conversion Corporation (SWCC), the world’s largest producer of desalinated water, reported daily production exceeding 11.5 million cubic meters in 2024, strengthening national water security amid limited natural freshwater resources. While large-scale desalination enhances municipal supply resilience across GCC countries, bottled water continues to maintain strong demand, particularly among tourists, expatriates, and mobile populations. Factors such as convenience, portability, assured quality standards, and preference for branded drinking water sustain consumption growth despite improved public water infrastructure. Collectively, infrastructure investments, tourism expansion, population mobility, and desalination capacity upgrades are reinforcing long-term bottled water demand across the GCC region.

GCC Bottled Water Industry Recent Developments:

- June 2025: Almarai Company completed the acquisition of Pure Beverages Industry Company for USD 277 million. Pure Beverages, known for its Ival and Oska bottled water brands, holds a strong position in the Saudi bottled water segment. The acquisition expands Almarai’s beverage portfolio and reinforces its market presence in Saudi Arabia, the largest bottled water market in the GCC.

- 2024: Nova, a brand of Health Water Bottling Co. Ltd., entered into a partnership agreement to serve as a support partner for the SAL Jeddah GT Race 2024. This collaboration enhances brand visibility through association with a high-profile motorsport event, reflecting evolving marketing strategies within the bottled water sector.

- 2024: Nova introduced water bottles made entirely from recycled materials, aligning with environmental sustainability goals under Saudi Vision 2030 and the Saudi Green Initiative. This packaging innovation highlights growing industry emphasis on sustainability and circular-economy initiatives in the GCC bottled water market.

GCC Bottled Water Market Scope:

| Category | Segments |

|---|---|

| By Category | Still Bottled Water, Functional Bottled Water, Flavored Bottled Water, Carbonated Bottled Water |

| By Packaging | Flexible Packaging, (Aluminum, Pouches, Glass, Rigid Plastic, PET Bottles, Thin Wall Plastic Containers |

| By Sub Types | Purified, Desalinated, Atmospheric Generated, Others), Mineral, Other (Spring, Alkaline, Other) |

| By Price Category | Budget, Economy, Premium |

| By Pack Size | 100 ml, 125 ml, 200 ml, 250 ml, 330 ml, 370 ml, 450 ml, 500 ml, 591 ml, 750 ml, 1,000 ml, 1,500 ml, 4,000 ml, 5,000 ml, Others |

| By Sales Channel | Direct Sales/On Trade, (Restaurants, Hotels, Cafes, Other Retail Sales, (Grocery Retailers, Convenience Retail, Supermarkets, Hypermarkets, Small Local Grocer, Non-Grocery Retailers, General Merchandise Stores, Health and Beauty Specialists, Vending, E-commerce),and others |

GCC Bottled Water Market Driver:

Extreme Climatic Conditions & Water Quality Perception Fueling High Per Capita Consumption

The foremost driver of the GCC bottled water market is the region’s extreme climatic conditions, combined with consumer perception of superior safety and quality compared to tap or desalinated water. GCC countries such as Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain experience prolonged summers with temperatures frequently exceeding 45°C. Such climatic intensity directly increases hydration needs, driving structurally high per capita bottled water consumption across residential, workplace, and on-the-go settings.

Additionally, although municipal water is largely desalinated and regulated, a strong consumer preference for packaged water persists due to concerns about taste, storage tank contamination in buildings, and perceived mineral imbalance. In urban centers such as Riyadh, Dubai, and Doha, bottled water is often treated as a daily essential rather than a discretionary purchase. The region’s high disposable income and hospitality-driven culture further institutionalize bottled water consumption in offices, hotels, restaurants, and religious gatherings. This climate-driven, perception-backed demand creates a stable and non-cyclical growth foundation for the GCC bottled water market.

GCC Bottled Water Market Trend:

Premiumization & Functional Water Innovations Gaining Momentum

A major evolving trend in the GCC bottled water market is premiumization, particularly the rising demand for mineral-rich, alkaline, flavored, and functional bottled water variants. Consumers are increasingly associating hydration with wellness, immunity support, and lifestyle positioning rather than mere thirst satisfaction. This shift is especially visible among urban millennials and expatriate populations in cities such as Dubai, Doha, and Abu Dhabi, where demand for differentiated and value-added hydration products is accelerating.

The expansion of fitness culture, boutique gyms, and health-focused retail chains across the region is further driving interest in electrolyte-enhanced, vitamin-infused, and low-calorie flavored water options. Hospitality establishments and premium dining outlets are also promoting glass-packaged and source-differentiated water to align with luxury branding and sustainability positioning. As a result, bottled water brands are increasingly leveraging packaging aesthetics, mineral composition claims, and functional attributes to strengthen brand loyalty and improve margins. For instance:

November 2025: Al Ain Water launched a new line of flavored bottled water in the UAE, marking its strategic move beyond conventional still water into lifestyle-oriented and healthier beverage segments. The development underscores the region’s growing demand for taste-enhanced, wellness-driven hydration formats.

The premium and functional segment is therefore expanding at a faster pace than standard bulk water, significantly enhancing revenue realization and market differentiation across the GCC.

GCC Bottled Water Market Opportunity:

Expansion of Sustainable & Refillable Packaging Ecosystems

A significant forward-looking opportunity in the GCC bottled water market lies in the rapid transition toward sustainable packaging and refill-based distribution ecosystems. Governments across the region, particularly in the United Arab Emirates and Saudi Arabia, are embedding circular economy mandates and plastic reduction targets within national sustainability frameworks, compelling beverage manufacturers to redesign packaging strategies.

This regulatory momentum is accelerating the adoption of 100% recyclable PET, rPET incorporation, biodegradable alternatives, and institutional bulk water dispensers across commercial buildings, airports, hospitality chains, and residential communities. For instance:

- In February 2025, Agthia Group received the ‘Supplier of the Year – Most Sustainable’ award at Gulfood 2025 for developing 100% recyclable PET bottles, reinforcing the commercial viability of circular packaging innovation in the GCC bottled water market.

- January 2025: VOSS Water launched a 250 ml still water bottle made from 100% recycled PET for the UAE market, targeting premium on-the-go consumers and reflecting growing demand for compact, environmentally responsible hydration solutions in the GCC.

Such developments indicate that sustainability is becoming a competitive differentiator rather than merely a compliance requirement. Additionally, the emergence of IoT-enabled refill stations and subscription-based bulk water delivery platforms offers scalable, lower-plastic distribution models. As ESG-linked procurement policies gain traction among corporates and hospitality operators, early movers investing in recyclable materials and closed-loop systems are expected to secure long-term market advantage, reinforcing sustainability as a structural growth opportunity in the GCC bottled water market.

GCC Bottled Water Market Challenge:

Rising Environmental Scrutiny & Plastic Waste Regulations

The most pressing challenge facing the GCC bottled water market is intensifying environmental scrutiny related to plastic waste generation and carbon footprint concerns. The region records one of the highest per capita plastic consumption rates globally, with bottled water being a major contributor to single-use PET waste streams.

Governments are gradually tightening packaging regulations, introducing plastic taxes, and encouraging reusable alternatives. Public awareness campaigns and sustainability mandates in retail chains are reshaping procurement behavior. Additionally, desalination-dependent water production already carries high energy intensity, raising broader environmental debates about the bottled water lifecycle footprint.

Large retail buyers and hospitality chains are increasingly demanding recyclable content and supplier sustainability disclosures. Compliance with evolving ESG standards increases operational costs for manufacturers, especially smaller domestic players. Failure to align with environmental expectations could result in reputational risks and reduced shelf space in premium retail channels. Balancing hydration demand with environmental accountability remains a critical strategic challenge for the GCC bottled water industry.

GCC Bottled Water Market (2026-32): Segmentation Analysis

The GCC Bottled Water Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–2032 at the regional level. Based on the analysis, the market has been further classified as:

Based on Category:

- Still Bottled Water

- Functional Bottled Water

- Flavored Bottled Water

- Carbonated Bottled Water

Still Bottled water is presently the dominant category in the GCC bottled water market, representing about 75% of the total market size in 2026, driven by its essential role in daily hydration, wide availability across retail and HoReCa channels, and strong consumer preference over sugary or tap water alternatives in the region’s hot, arid climate. This segment’s large share reflects both high consumption volumes and broad appeal, making it the backbone of industry revenues and distribution strategies. Although functional, flavored, and carbonated bottled waters are gaining traction with health and lifestyle trends, still water remains the core market leader due to its affordability, convenience, and fundamental necessity for everyday use across households and commercial settings in the GCC.

Based on Packaging:

- Flexible Packaging

- Aluminum

- Pouches

- Glass

- Rigid Plastic

- PET Bottles

- Thin-Wall Plastic Containers

Rigid plastic packaging, particularly PET bottles, firmly dominates the bottled water packaging segment, accounting for the largest share of total market revenue. This dominance is primarily driven by PET’s lightweight structure, durability, shatter resistance, and cost efficiency, which make it highly suitable for mass production and large-scale distribution. In addition, PET bottles offer strong design flexibility, allowing manufacturers to produce various sizes ranging from small single-serve packs to bulk containers, thereby catering to both household and commercial demand.

Moreover, the well-established recycling infrastructure and advancements in lightweight and recycled PET (rPET) technologies further strengthen rigid plastic’s market position by aligning with evolving sustainability goals. Its compatibility with automated filling lines and lower transportation costs compared to heavier materials also enhances operational efficiency for producers. Owing to these combined economic and functional advantages, rigid plastic continues to lead the industry and is expected to maintain its dominant position in the foreseeable future.

GCC Bottled Water Market (2026-32): Regional Projection

Geographically, the GCC Bottled Water Market expands across:

- Saudi Arabia

- United Arab Emirates

- Qatar

- Oman

- Kuwait

- Bahrain

In 2026, Saudi Arabia leads the GCC bottled water industry, primarily driven by its large population base, high urban concentration, and strong consumer purchasing power. According to the General Authority for Statistics (GASTAT), the Kingdom’s population exceeded 35 million by mid-2024, while the average Saudi household spends approximately USD 4,812 per month. This relatively high monthly expenditure reflects improved income stability and stronger consumption capacity, which directly supports higher per-capita spending on essential packaged goods such as bottled drinking water. In a region characterized by extreme climatic conditions and limited natural freshwater resources, bottled water remains a daily necessity rather than a discretionary purchase, further reinforcing consistent demand levels. This strong consumption environment has also encouraged multinational beverage companies to deepen their presence in the Kingdom.

- 2025: PepsiCo announced a USD 8 million investment to establish a regional research and development centre in Riyadh, aimed at advancing product innovation and packaging solutions tailored to local consumer preferences, including bottled water offerings.

Such strategic corporate investments are closely aligned with Saudi Arabia’s robust consumer demand, thereby strengthening its position as the leading bottled water market within the GCC in 2026.

Gain a Competitive Edge with Our GCC Bottled Water Market Report:

- GCC Bottled Water Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- GCC Bottled Water Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- GCC Bottled Water Market Policies, Regulations, and Product Standards

- GCC Bottled Water Market Supply Chain Analysis

- GCC Bottled Water Market Trends & Developments

- GCC Bottled Water Market Dynamics

- Growth Drivers

- Challenges

- GCC Bottled Water Market Hotspot & Opportunities

- GCC Bottled Water Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Volume (Million Liters)

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032F, USD Million

- Still Bottled Water

- Functional Bottled Water

- Flavored Bottled Water

- Carbonated Bottled Water

- By Packaging- Market Size & Forecast 2022-2032F, USD Million

- Flexible Packaging

- Aluminum

- Pouches

- Glass

- Rigid Plastic

- PET Bottles

- Thin Wall Plastic Containers

- Flexible Packaging

- By Sub Types- Market Size & Forecast 2022-2032F, USD Million

- Purified

- Desalinated

- Atmospheric Generated

- Others

- Mineral

- Other (Spring, Alkaline, Other)

- Purified

- By Price Category- Market Size & Forecast 2022-2032F, USD Million

- Budget

- Economy

- Premium

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- 100 ml

- 125 ml

- 200 ml

- 250 ml

- 330 ml

- 370 ml

- 450 ml

- 500 ml

- 591 ml

- 750 ml

- 1,000 ml

- 1,500 ml

- 4,000 ml

- 5,000 ml

- Others

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- Direct Sales/On Trade

- Restaurants

- Hotels

- Cafes

- Other

- Retail Sales

- Grocery Retailers

- Convenience Retail

- Supermarkets

- Hypermarkets

- Small Local Grocer

- Non-Grocery Retailers

- General Merchandise Stores

- Health and Beauty Specialists

- Vending

- Grocery Retailers

- E-commerce

- Direct Sales/On Trade

- By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Oman

- Kuwait

- Bahrain

- By Company

- Company Revenue Shares

- Competitor Characteristics

- By Category- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Outlook

- Saudi Arabia Bottled Water Market Outlook, 2022-2032

- Market Size & Analysis

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Packaging- Market Size & Forecast 2022-2032, USD Million

- By Sub Types- Market Size & Forecast 2022-2032, USD Million

- By Price Category- Market Size & Forecast 2022-2032, USD Million

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- UAE Bottled Water Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- By Volume (Million Liters)

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Packaging- Market Size & Forecast 2022-2032, USD Million

- By Sub Types- Market Size & Forecast 2022-2032, USD Million

- By Price Category- Market Size & Forecast 2022-2032, USD Million

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Analysis

- Qatar Bottled Water Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- By Volume (Million Liters)

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Packaging- Market Size & Forecast 2022-2032, USD Million

- By Sub Types- Market Size & Forecast 2022-2032, USD Million

- By Price Category- Market Size & Forecast 2022-2032, USD Million

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Analysis

- Oman Bottled Water Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- By Volume (Million Liters)

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Packaging- Market Size & Forecast 2022-2032, USD Million

- By Sub Types- Market Size & Forecast 2022-2032, USD Million

- By Price Category- Market Size & Forecast 2022-2032, USD Million

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Analysis

- Kuwait Bottled Water Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- By Volume (Million Liters)

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Packaging- Market Size & Forecast 2022-2032, USD Million

- By Sub Types- Market Size & Forecast 2022-2032, USD Million

- By Price Category- Market Size & Forecast 2022-2032, USD Million

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Analysis

- Bahrain Bottled Water Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Million)

- By Volume (Million Liters)

- Market Segmentation & Outlook

- By Category- Market Size & Forecast 2022-2032, USD Million

- By Packaging- Market Size & Forecast 2022-2032, USD Million

- By Sub Types- Market Size & Forecast 2022-2032, USD Million

- By Price Category- Market Size & Forecast 2022-2032, USD Million

- By Pack Size- Market Size & Forecast 2022-2032F, USD Million

- By Sales Channel- Market Size & Forecast 2022-2032F, USD Million

- Market Size & Analysis

- GCC Bottled Water Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Agitha Group PJSC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Masafi LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- The Coca-Cola Company

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Mai Dubai LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Hana Food Industries Co.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Berain Water

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Nova Water

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Almarai Company

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Crystal Mineral Water and Refreshments LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Al Furat Drinking Water LLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Al-Rawdatain Water Bottling Co.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Rayyan Mineral Water Company (Qatar)

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Al Jomaih Water and Beverage

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Agitha Group PJSC

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now