Europe Solar Repowering Market Research Report: Forecast (2026-2032)

By Repowering Type (Partial Repowering, Full Repowering), By Technology (Solar Panel Upgrades, Inverters and Power Electronics, Energy Storage Systems), By Project Scale (Small-Sca ... le Repowering, Large-Scale Repowering, Utility-Scale Repowering), By Component Replaced (Modules / Panels, Inverters, Mounting Structures & Trackers, Cables & Balance of System (BoS) Components, Monitoring & Control Systems), By Plant Type (Utility-Scale Solar PV Plants, Commercial & Industrial (C&I) Systems, Residential Rooftop Systems), By Service Type (Engineering, Procurement & Construction (EPC), O&M and Performance Optimization, Repowering Feasibility Studies & Consulting, Asset Management & Financing Support), By End User (Utility Companies, Independent Power Producers (IPPs), Private Developers & Investors, Commercial & Industrial Sector, Residential), and others Read more

- Energy

- Feb 2026

- Pages 260

- Report Format: PDF, Excel, PPT

Europe Solar Repowering Market

Projected 11.01% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 1.63 Billion

Market Size (2032)

USD 3.05 Billion

Base Year

2025

Projected CAGR

11.01%

Leading Segments

By Plant Type: Utility-Scale Solar PV Plants

Europe Solar Repowering Market Report Key Takeaways:

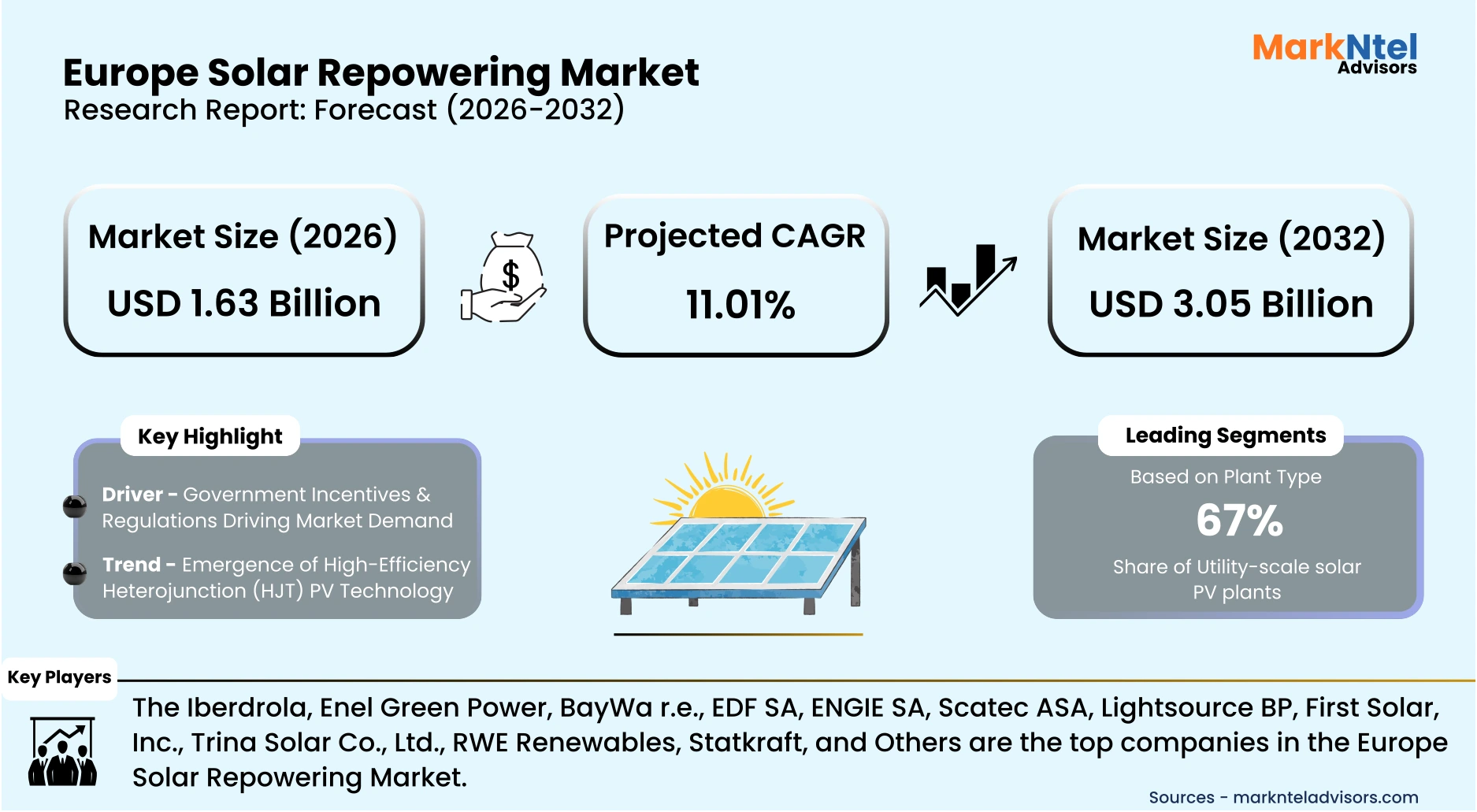

- The Europe Solar Repowering Market size was valued at USD 1.43 billion in 2025 and is projected to grow from USD 1.63 billion in 2026 to USD 3.05 billion by 2032, exhibiting a CAGR of 11.01% during the forecast period.

- By repowering type, the partial repowering segment represented a significant share of about 60% in the Europe Solar Repowering Market in 2026.

- By plant type, the utility-scale solar PV plants segment presented a significant share of about 67% in the Europe Solar Repowering Market in 2026.

- Leading solar repowering companies in Europe are Iberdrola, Enel Green Power, BayWa r.e., EDF SA, ENGIE SA, Scatec ASA, Lightsource BP, First Solar, Inc., Trina Solar Co., Ltd., RWE Renewables, Statkraft, and Others.

Market Insights & Analysis: Europe Solar Repowering Market (2026-32):

The Europe Solar Repowering Market size was valued at around USD 1.43 billion in 2025 and is projected to grow from USD 1.63 billion in 2026 to USD 3.05 billion by 2032. Along with this, the Market is estimated to grow at a CAGR of around 11.01% during the forecast period, i.e., 2026-32.

The Europe Solar Repowering Market is gaining strategic momentum as policymakers, developers, and technology providers aim to extend the life and performance of aging photovoltaic (PV) assets rather than build new installations. As early utility‑scale solar farms approach the end of their original warranties, repowering, upgrading existing infrastructure with advanced modules, inverters, and digital technologies offers a cost‐effective route to meet growing renewable energy targets, improve efficiency, and reduce environmental footprints.

Government incentives and supportive regulatory frameworks are central to the market’s growth. A key driver is the European Union’s REPowerEU initiative, valued at approximately USD 320 billion, which seeks to accelerate renewable deployment, modernize energy infrastructure, and reduce dependence on fossil fuels. This massive investment framework encourages repowering by creating clear pathways for plant modernization financing and streamlined permitting.

Technological advancements are reshaping how repowering is executed. The market is trending toward high‑efficiency Heterojunction (HJT) PV technology, which combines crystalline and amorphous silicon layers to deliver superior performance. HJT modules offer higher energy yields, better temperature performance, and enhanced resistance to degradation compared with older technologies. Under the EU’s broader research and innovation priorities, HJT‑focused startups in Spain, Italy, and Germany received a combined USD 130 million in 2025 to scale high‑efficiency module production, reducing reliance on imports and bolstering domestic supply chains for repowered assets.

Commercialization of next‑generation modules further highlights this trend. At the 2025 Intersolar Europe exhibition, manufacturers such as Huasun showcased 730 W HJT modules with approximately 23.5% efficiency, designed for diverse applications from agrivoltaics to vertical installations. This reflects the rapid adoption of high‑efficiency technologies in both repowering and new project deployments across Europe.

Repowering is not limited to cutting‑edge module technology. On the operational side, improvements in plant efficiency have already been demonstrated through refurbishment projects. For example, EF Solare Italia completed the refurbishment of existing PV plants in Campania, replacing older thin‑film modules with high‑efficiency bifacial panels and advanced inverters. These upgrades boosted annual energy output by around 30% on the same site while reducing CO₂ emissions, a clear example of repowering’s tangible benefits without additional land use.

Overall, as Europe pushes toward its 2030 renewable targets, repowering will play an increasingly pivotal role. Government incentives, large‑scale funding mechanisms, and broad adoption of high‑efficiency technologies are aligned to drive repowering adoption. The combination of policy support, technological innovation, and demonstrable performance gains positions the Europe Solar Repowering Market for strong growth in the coming decade.

Europe Solar Repowering Market Recent Developments:

- 2025: TCL SunPower Global unveiled a new integrated product portfolio at Intersolar Europe 2025, including expandable home energy storage systems (5 kWh) and high‑efficiency back‑contact solar panels (25 % efficiency), designed for residential to utility‑scale repowering and hybrid installations.

- 2025: VSB successfully connected one of Europe’s largest repowering wind‑solar projects (105.6 MW) to the grid in Finland, showcasing integrated repowering technologies that enhance generation capacity through modern turbine tech and hybrid plant upgrades.

Europe Solar Repowering Market Scope:

| Category | Segments |

|---|---|

| By Repowering Type | (Partial Repowering, Full Repowering), |

| By Technology | (Solar Panel Upgrades, Inverters and Power Electronics, Energy Storage Systems), |

| By Project Scale | (Small-Scale Repowering, Large-Scale Repowering, Utility-Scale Repowering), |

| By Component Replaced | (Modules / Panels, Inverters, Mounting Structures & Trackers, Cables & Balance of System (BoS) Components, Monitoring & Control Systems), |

| By Plant Type | (Utility-Scale Solar PV Plants, Commercial & Industrial (C&I) Systems, Residential Rooftop Systems), |

| By Service Type | (Engineering, Procurement & Construction (EPC), O&M and Performance Optimization, Repowering Feasibility Studies & Consulting, Asset Management & Financing Support), |

| By End User | (Utility Companies, Independent Power Producers (IPPs), Private Developers & Investors, Commercial & Industrial Sector, Residential), |

Europe Solar Repowering Market Driver:

Government Incentives & Regulations Driving Market Demand

Government incentives, climate regulations, and renewable energy mandates across Europe are major forces accelerating solar repowering activities. The European Union’s policy framework, particularly the European Green Deal and REPowerEU strategy, aims to achieve climate neutrality by 2050 while reducing dependence on fossil fuels, pushing utilities to upgrade existing renewable assets for higher efficiency rather than building new sites.

Financial support mechanisms are substantial. The EU allocated about USD 21.6 billion in additional REPowerEU funding to accelerate clean-energy deployment, including solar modernization and grid upgrades. Furthermore, EU energy funding programs confirmed around USD 20.6 billion for renewable energy, storage, and network modernization projects since 2021, directly supporting plant upgrades and repowering initiatives.

Regulatory mandates are also creating long-term demand. Under the revised Energy Performance of Buildings Directive and EU Solar Rooftop Strategy, solar installations will become mandatory on new public and commercial buildings by 2026 and on residential buildings by 2029, with requirements extending to renovations of existing structures through 2030. These policies increase the installed solar base, which will eventually require modernization and repowering over time.

Future investments beyond 2025 remain strong. The broader European Green Deal Investment Plan is expected to mobilize roughly USD 543 billion for climate and energy transition initiatives over several years, ensuring sustained upgrades of aging renewable infrastructure.

Overall, government incentives and regulations reduce financial risks while mandating renewable adoption, directly encouraging repowering projects. As policy targets tighten toward 2030 and 2050, modernization of existing solar assets will become essential, significantly accelerating market growth.

Europe Solar Repowering Market Trend:

Emergence of High-Efficiency Heterojunction (HJT) PV Technology

A major trend in the European solar repowering market is the strategic support and scaling of high-efficiency heterojunction (HJT) photovoltaic (PV) technology. In April 2025, the Netherlands-based solar manufacturer MCPV received a USD 10.8 million grant from Spain’s Ministry for Ecological Transition to build a 2.5 GW HJT module factory in Tudela, Navarra, part of Spain’s nearly USD 324 million Clean Energy Transition Fund. This project targets large-scale production of advanced HJT modules in Europe, boosting local manufacturing capacity and reducing dependency on imported PV products.

HJT technology combines crystalline silicon with amorphous silicon layers and offers clear advantages for repowering mass-production efficiencies above 24%, lower temperature coefficients, enhanced bifacial gains, and strong resistance to performance degradation. MCPV’s roadmap includes reaching 15 GW of capacity by 2026 and gaining a significant share of the European PV market by 2030, underscoring the technology’s importance for renewable goals.

This trend reflects broader European policy shifts to strengthen domestic PV value chains through financing, incentives, and industrial policy, positioning high-efficiency HJT modules as a cornerstone of repowering older solar assets and accelerating the energy transition across the EU.

Europe Solar Repowering Market Opportunity:

Expansion of Utility-Scale Repowering Offering Lucrative Growth Opportunities

A significant opportunity in the Europe solar repowering market lies in the expansion of utility‑scale solar repowering projects, driven by both the large installed base of solar capacity and ambitious EU targets for renewable energy expansion. According to the European Commission’s solar strategy, the EU’s total solar photovoltaic capacity grew from about 338 GW in 2024 to approximately 406 GW in 2025, surpassing earlier capacity goals under the REPowerEU plan. This growing fleet of PV assets includes many utility‑scale installations approaching the end of their initial operational warranties, creating a substantial market for repowering activities.

Utility‑scale repowering enables plant owners to replace aging modules, inverters, and balance‑of‑system components with higher‑efficiency technologies while leveraging existing land and grid connections. With EU solar capacity projected to expand further toward at least 700 GW by 2030 as part of longer‑term European energy transition strategies, the need to extend the life and performance of existing large solar plants will grow.

European initiatives to streamline permitting for solar and renewable upgrades, including repowering projects, further enhance this opportunity by lowering regulatory barriers and accelerating project timelines. For example, the EU has agreed on permit‑granting deadlines for renewable equipment installations, which can benefit repowering activities at utility scales.

Overall, as utility‑scale solar capacity continues to increase and older PV plants reach end‑of‑life, upgrading these assets through repowering presents a major opportunity to boost energy yields, improve system reliability, and support Europe’s renewable and decarbonization goals through 2030 and beyond.

Europe Solar Repowering Market Challenge:

Complex Regulatory Framework

A major challenge facing the Europe solar repowering market is lengthy regulatory and permitting processes, which delay project execution and increase costs. Even for upgrades of existing solar plants, developers often must navigate complex approval systems, including grid connection permissions, environmental assessments, and local regulations. These processes can take several years, slowing modernization and repowering timelines.

For instance, SolarPower Europe reports that the average time to connect large‑scale photovoltaic projects to the grid in some EU member states remains around four years, and in certain cases extends up to eight years due to bureaucratic lag and inconsistent permitting standards. This creates uncertainty for investors and can deter timely repowering investment.

Overall, Complex and prolonged permitting and regulatory requirements continue to be a significant challenge in the European solar repowering market, delaying upgrades, increasing development costs, and reducing investor confidence in repowering activities.

Europe Solar Repowering Market (2026-32) Segmentation Analysis:

The Europe Solar Repowering Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the Market has been further classified as;

Based on Repowering Type:

- Partial Repowering

- Full Repowering

The Europe solar repowering market is led by partial repowering, accounting for 60% of all projects in 2025. Partial repowering focuses on upgrading specific components such as solar modules, inverters, or tracking systems without replacing the entire plant infrastructure. This method is highly cost-effective, as it reduces capital expenditure and shortens downtime while improving energy output and operational efficiency. Operators can replace aging panels with high-efficiency monocrystalline or bifacial modules, or upgrade inverters to advanced string or microinverter technologies, increasing annual generation by up to 30%. Utilities and independent power producers prefer partial repowering because it maximizes returns on existing assets and minimizes project complexity.

Additionally, regulatory incentives in several European countries encourage incremental efficiency upgrades, further supporting partial repowering adoption. This approach strikes a balance between financial feasibility and performance optimization, making it the dominant repowering type across Europe’s aging solar PV infrastructure.

Based on Plant Type:

- Utility-Scale Solar PV Plants

- Commercial & Industrial (C&I) Systems

- Residential Rooftop Systems

Utility-scale solar PV plants dominate the Europe solar repowering industry, representing 67% of projects in 2025. These plants typically generate tens to hundreds of megawatts, making them attractive targets for repowering due to the high potential gains in energy yield and grid reliability. Upgrading key components such as modules, inverters, trackers, or balance-of-system equipment allows plant operators to increase generation capacity without expanding the land footprint. The scale of these installations also enables cost efficiencies in procurement, construction, and operation.

Furthermore, regulatory frameworks, long-term power purchase agreements (PPAs), and renewable energy incentives in Europe drive investments toward utility-scale projects. Independent power producers and utilities prioritize these plants for repowering because performance gains translate into significant revenue improvement. The combination of scale, economic benefit, and regulatory support reinforces utility-scale solar PV plants as the leading segment in Europe’s repowering market.

Europe Solar Repowering Market (2026-32): Regional Projection

The Europe solar repowering market is dominated by Western European countries, particularly Germany, Spain, France, and Italy. These countries have the largest installed utility‑scale solar PV capacities, many of which were commissioned between 2005 and 2015 and now require modernization. Germany leads the market with one of the continent’s oldest and largest solar fleets, supported by strong renewable energy policies, advanced grid infrastructure, and high investment capacities. Spain and Italy also feature substantial early-installed capacities, making repowering financially attractive to increase energy output, extend plant lifespan, and optimize efficiency.

Government incentives, such as renewable transition funds and streamlined permitting for repowering projects, further encourage modernization. Western Europe also benefits from established PV manufacturing and technology ecosystems, along with active independent power producers and developers. In contrast, Eastern European countries primarily focus on new solar installations rather than repowering. As a result, Western Europe dominates the solar repowering market, leveraging its aging assets for maximum efficiency and energy generation.

Gain a Competitive Edge with Our Europe Solar Repowering Market Report:

- Europe Solar Repowering Market Report by MarkNtel Advisors provides a detailed & thorough analysis of Market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the Market dynamics & make informed decisions.

- This report also highlights current Market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding Market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Solar Repowering Market Report aids in assessing & mitigating risks associated with entering or operating in the Market. By understanding Market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Solar Repowering Market Policies, Regulations, and Product Standards

- Europe Solar Repowering Market Trends & Developments

- Europe Solar Repowering Market Dynamics

- Growth Factors

- Challenges

- Europe Solar Repowering Market Hotspot & Opportunities

- Europe Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- Partial Repowering

- Full Repowering

- By Technology- Market Size & Forecast 2022-2032, USD Million

- Solar Panel Upgrades

- Monocrystalline Panels

- Polycrystalline Panels

- Bifacial Solar Panels

- Inverters and Power Electronics

- String Inverters

- Microinverters

- Energy Storage Systems

- Solar Panel Upgrades

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- Small-Scale Repowering

- Large-Scale Repowering

- Utility-Scale Repowering

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- Modules / Panels

- Inverters

- Mounting Structures & Trackers

- Cables & Balance of System (BoS) Components

- Monitoring & Control Systems

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- Utility-Scale Solar PV Plants

- Commercial & Industrial (C&I) Systems

- Residential Rooftop Systems

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- Engineering, Procurement & Construction (EPC)

- O&M and Performance Optimization

- Repowering Feasibility Studies & Consulting

- Asset Management & Financing Support

- By End User- Market Size & Forecast 2022-2032, USD Million

- Utility Companies

- Independent Power Producers (IPPs)

- Private Developers & Investors

- Commercial & Industrial Sector

- Residential

- By Country

- The UK

- Germany

- The Netherlands

- France

- Spain

- Italy

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The UK Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- By Technology- Market Size & Forecast 2022-2032, USD Million

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- By Technology- Market Size & Forecast 2022-2032, USD Million

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The Netherlands Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- By Technology- Market Size & Forecast 2022-2032, USD Million

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- By Technology- Market Size & Forecast 2022-2032, USD Million

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- By Technology- Market Size & Forecast 2022-2032, USD Million

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Solar Repowering Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Repowering Type- Market Size & Forecast 2022-2032, USD Million

- By Technology- Market Size & Forecast 2022-2032, USD Million

- By Project Scale- Market Size & Forecast 2022-2032, USD Million

- By Component Replaced- Market Size & Forecast 2022-2032, USD Million

- By Plant Type- Market Size & Forecast 2022-2032, USD Million

- By Service Type- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Europe Solar Repowering Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Iberdrola

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Enel Green Power

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BayWa r.e.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EDF SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ENGIE SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Scatec ASA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lightsource BP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- First Solar, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Trina Solar Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- RWE renewables

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Statkraft

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Iberdrola

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now