Europe Drone Detection Radar Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Radar Type (Short-Range Radar (<5 km), Medium-Range Radar (5–10 km), Long-Range Radar (>10 km), AI-enabled / Cognitive Radar), By Frequency Band (X-Band Radar, Ku-Band Radar, Ka ... -Band Radar, L-Band / S-Band Radar, Multi-band Radar), By Platform (Ground-based Radar, Naval Radar, Airborne Radar, Vehicle-mounted / Portable Radar), By Detection Range (Very Short Range (<2 km), Short Range (2–5 km, Medium Range (5–10 km), Long Range (>10 km)), By End User (Military & Defense, Homeland Security / Border Protection, Airports & Aviation Security, Critical Infrastructure, Government & Public Safety, Commercial & Industrial Facilities, Event & Stadium Security), and others Read more

- Aerospace & Defense

- Feb 2026

- Pages 150

- Report Format: PDF, Excel, PPT

Europe Drone Detection Radar Market

Projected 31.29% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 348 Mllion

Market Size (2032)

USD 1782 Million

Base Year

2025

Projected CAGR

31.29%

Leading Segments

By Radar Type: Medium-Range Radar (5–10 km)

Europe Drone Detection Radar Market Report Key Takeaways:

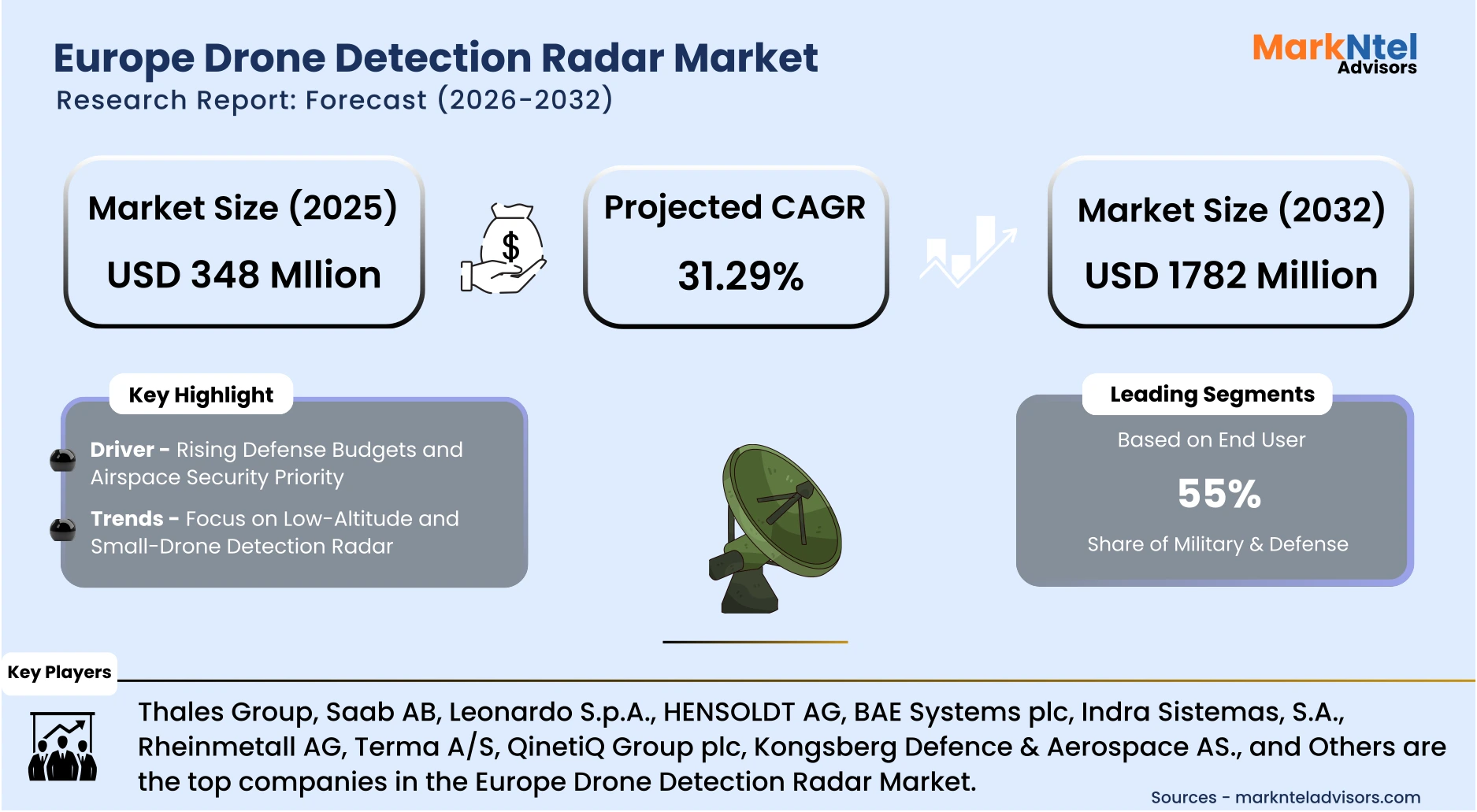

- Market size was valued at around USD 348 million in 2025 and is projected to reach USD 1,782 million by 2032. The estimated CAGR from 2026 to 2032 is around 31.29%, indicating strong growth.

- The United Kingdom holds the largest market share of about 25% in the Europe Drone Detection Radar Market in 2025.

- By radar type, the medium-range radar (5–10 km) segment represented a significant share of about 35% in the Europe Drone Detection Radar Market in 2025.

- By end user, the military & defense segment seized a significant share of about 55% in the Europe Drone Detection Radar Market in 2025.

- Leading drone detection radar companies in the Europe are Thales Group, Saab AB, Leonardo S.p.A., HENSOLDT AG, BAE Systems plc, Indra Sistemas, S.A., Rheinmetall AG, Terma A/S, QinetiQ Group plc, Kongsberg Defence & Aerospace AS., and Others.

Market Insights & Analysis: Europe Drone Detection Radar Market (2026-32):

The Europe Drone Detection Radar Market size was valued at around USD 348 million in 2025 and is projected to reach USD 1,782 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 31.29% during the forecast period, i.e., 2026-32.

The Europe Drone Detection Radar Market is projected to expand steadily, as rising defense budgets and stronger airspace security priorities are increasingly aligned with the need for low-altitude and small-drone detection capabilities, while EU funding programs and cross-border defense collaboration continue to accelerate technology development and deployment across the region.

A major pillar supporting long-term demand is the growing momentum of the European Sky Shield Initiative (ESSI), a cooperative air and missile defense program involving 24 European countries. The initiative prioritizes the development and joint procurement of layered defense systems, including short-range solutions designed to counter low-altitude and small-drone threats. Large-scale acquisition programs further reinforce this trajectory.

Germany’s planned procurement of 500–600 Skyranger 30 air-defense systems demonstrates a significant commitment to counter-drone capabilities and highlights the increasing role of radar-enabled detection and tracking technologies within national defense strategies.

National modernization programs are also accelerating across Europe. For example, Poland has committed over USD 2.17 billion to deploy anti-drone fortifications and surveillance systems along its eastern border, reflecting heightened urgency to strengthen airspace monitoring and frontier security.

Ireland has similarly announced a USD 1.85 billion defense modernization plan, including radar upgrades and counter-drone technologies to enhance national airspace protection and safeguard critical infrastructure. These initiatives illustrate how both large and smaller European nations are prioritizing advanced radar systems as part of broader defense transformation efforts.

Operational deployments further highlight the rising importance of low-altitude and small-drone detection radar. For instance, Spain’s deployment of the Crow counter-drone detection system during NATO Air Policing missions in Lithuania demonstrates the integration of radar with electro-optical sensors, thermal imaging, and electronic warfare tools to detect and track small UAVs in contested environments . Such deployments underscore the growing reliance on multi-sensor radar solutions capable of delivering persistent surveillance and rapid threat identification.

At the European Union level, long-term funding mechanisms continue to strengthen the industrial and innovation landscape. For example, the European Defence Fund is allocating approximately USD 9.5 billion for defense research and development, while the European Defence Industry Programme (2025–2027) will provide about USD 1.6 billion to enhance defense production capacity and collaborative procurement across member states. These investments are expected to accelerate technological innovation, reinforce supply chains, and promote cross-border cooperation in radar and counter-drone solutions.

Overall, the European drone detection radar market is entering a prolonged growth phase supported by coordinated defense initiatives, rising national security spending, and expanding EU-level funding. As drone threats evolve and airspace security becomes increasingly critical, sustained investment in advanced detection radar systems is expected to remain a strategic priority across the region.

Europe Drone Detection Radar Market Recent Developments:

- 2026: Belgium announced a USD 54 million anti-drone procurement program and allocated USD 540 million for radar, jamming, and wider counter-UAS capabilities, alongside the creation of a National Airspace Security Center to coordinate civil-military airspace protection and strengthen drone threat detection across the country.

- 2025: At FEINDEF 2025, Spain’s EM&E Group introduced a Vamtac ST5 counter-UAS vehicle equipped with four radar panels and 360-degree surveillance. The mobile platform enables detection and response to drone incursions during military and homeland security operations, highlighting the shift toward mobile radar-enabled counter-UAS solutions.

| Category | Segments |

|---|---|

| By Radar Type | (Short-Range Radar (<5 km), Medium-Range Radar (5–10 km), Long-Range Radar (>10 km), AI-enabled / Cognitive Radar), |

| By Frequency Band | (X-Band Radar, Ku-Band Radar, Ka-Band Radar, L-Band / S-Band Radar, Multi-band Radar), |

| By Platform | (Ground-based Radar, Naval Radar, Airborne Radar, Vehicle-mounted / Portable Radar), |

| By Detection Range | (Very Short Range (<2 km), Short Range (2–5 km, Medium Range (5–10 km), Long Range (>10 km)), |

| By End User | (Military & Defense, Homeland Security / Border Protection, Airports & Aviation Security, Critical Infrastructure, Government & Public Safety, Commercial & Industrial Facilities, Event & Stadium Security), |

Europe Drone Detection Radar Market Driver:

Rising Defense Budgets and Airspace Security Priority

Europe’s rapidly expanding military expenditure is a major catalyst driving demand for drone detection radar systems. Defense budgets across the region are increasing at the fastest pace since the Cold War, reflecting heightened security concerns and the need to strengthen airspace protection.

Germany has announced plans to increase defense spending from approximately USD 86 billion to USD 108.2 billion, while the United Kingdom aims to raise military spending to 2.5% of GDP by 2027 . These commitments demonstrate a long-term shift toward strengthening national and NATO defense capabilities.

A key factor behind this surge is the growing threat posed by unmanned aerial systems observed during the Russia–Ukraine conflict and across NATO airspace. Drone incursions have highlighted vulnerabilities in border security, military bases, and critical infrastructure, prompting governments to prioritize counter-UAS technologies. As a result, investments in radar-based detection, surveillance, and air-defense systems are accelerating to ensure rapid threat identification and response.

EU-level funding is reinforcing this trend and enabling collaborative capability development. The European Defence Fund (EDF) has already allocated nearly half of its USD 8 billion budget to joint defense research and procurement initiatives, with strong emphasis on drones, air-defense technologies, and cross-border interoperability. This funding supports multinational collaboration and accelerates the deployment of advanced counter-drone solutions across Europe.

Overall, sustained defense spending growth, combined with rising drone threats and strong EU funding support, is creating a robust and long-term procurement pipeline for drone detection radar systems across the European market.

Europe Drone Detection Radar Market Trend:

Focus on Low-Altitude and Small-Drone Detection Radar

European air-defense strategy is rapidly shifting toward radar systems specifically designed to detect low-altitude, small, and slow-moving drones, reflecting lessons learned from recent conflicts and rising incidents of drone incursions across NATO airspace.

Traditional air-defense radar was primarily designed for large aircraft and missiles, leaving a critical capability gap against small unmanned aerial systems (UAS). Governments and defense agencies across Europe are now prioritizing short-range radar, sensor fusion, and integrated counter-UAS networks to close this gap.

NATO has taken a leading role by establishing a Counter-Small UAS procurement framework through the NATO Support and Procurement Agency, enabling member states to jointly acquire detection and mitigation technologies against small drones. This marks a major shift toward collective procurement of low-altitude surveillance and counter-drone capabilities.

The European Defence Agency has further identified counter-UAS and low-level air surveillance as a major collaborative priority, emphasizing integrated sensor networks to protect military bases, borders, and urban infrastructure .

Governments are also strengthening national procurement programs. The UK Ministry of Defence has confirmed investments in counter-drone technologies to protect critical infrastructure and military installations, including advanced sensors capable of detecting small UAVs.

Overall, the growing focus on low-altitude and small-drone radar detection represents a structural transformation in European air-defence priorities. Continued investment in layered surveillance and sensor integration is expected to drive sustained demand for specialized drone detection radar systems across the region.

Europe Drone Detection Radar Market Opportunity

EU Funding Programs and Cross-Border Defense Collaboration

European defense policy is increasingly centered on collaborative procurement and multinational capability development, creating strong opportunities for drone detection radar providers. The European Union is prioritizing joint defense innovation and interoperability to strengthen airspace security and reduce fragmentation across national defense systems.

A major growth catalyst is the European Defence Fund (EDF), which allocated approximately USD 990 million in 2025 to 62 collaborative defense projects. Many of these initiatives focus on advanced surveillance, drone detection, artificial intelligence, and integrated air-defense systems. This funding is designed to accelerate technology development and encourage cross-border industrial partnerships, opening the market to new suppliers and specialized technology firms.

The opportunity is further reinforced by the EU’s Readiness 2030 defense initiative, which aims to expand the EU's defense and space budget to approximately USD 142 billion. This programme promotes joint procurement and shared air-defense infrastructure, creating long-term demand for interoperable drone detection radar solutions capable of operating across multiple national security networks.

In addition, the EU Defence Innovation Scheme, supported by roughly USD 2.2 billion in funding, is helping startups and small-to-medium enterprises develop next-generation defense technologies, including sensor fusion, radar analytics, and AI-enabled airspace monitoring .

Overall, expanding EU funding mechanisms and cross-border collaboration are expected to accelerate innovation, strengthen partnerships, and generate sustained long-term opportunities for the Europe drone detection radar market.

Europe Drone Detection Radar Market Challenge:

High Deployment and Lifecycle Cost Impeding Market Growth

The adoption of advanced drone detection radar systems across Europe is significantly constrained by the high cost of deployment and long-term sustainment. Effective counter-UAS protection requires layered solutions that integrate radar, sensors, electronic warfare, command-and-control networks, and continuous upgrades, creating substantial multi-year financial commitments for governments.

Recent defense modernization programs highlight the scale of required investment. For example, Greece launched a long-term defense modernization program valued at approximately USD 27 billion, representing one of the largest defense spending commitments among mid-sized European economies. Such large-scale funding underscores the substantial financial resources required to strengthen air-defense and surveillance infrastructure.

Similarly, Denmark announced a defense investment package worth roughly USD 8.3 billion focused on missile and drone capabilities to respond to emerging aerial threats. This illustrates the high upfront capital needed to deploy modern counter-drone and radar systems .

Beyond procurement, lifecycle costs further increase financial pressure. Integrated counter-drone networks require ongoing software upgrades, maintenance, training, and cybersecurity protection to remain effective against evolving drone threats. Overall, the high cost of acquisition, integration, and long-term sustainment remains a major barrier to the rapid deployment of drone detection radar systems across Europe.

The deployment of advanced drone detection radar systems across Europe faces a significant constraint due to the exceptionally high cost of building and sustaining integrated air-defense and surveillance networks. Governments increasingly recognize that effective counter-UAS protection requires layered systems combining radar, sensors, electronic warfare, command-and-control infrastructure, and long-term upgrades, creating multi-year financial commitments.

Europe Drone Detection Radar Market (2026-32) Segmentation Analysis:

The Europe Drone Detection Radar Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Radar Type:

- Short-Range Radar (<5 km)

- Medium-Range Radar (5–10 km)

- Long-Range Radar (>10 km)

- AI-enabled / Cognitive Radar

The medium-range radar (5–10 km) segment dominates the Europe Drone Detection Radar Industry, holding around 35% market share, driven by its strong balance between detection capability, deployment flexibility, and cost efficiency.

This range category is particularly suited to the most common counter-UAS mission profiles, where drones typically operate within a few kilometers of intended targets such as military installations, airports, energy facilities, borders, and major public venues.

European defense and homeland security agencies are increasingly adopting layered airspace protection strategies, and medium-range radar systems form a critical detection tier within these architectures. They provide sufficient early-warning range to enable timely electronic warfare, jamming, or interception measures, while remaining more affordable and easier to deploy than long-range air-defense radar systems.

Their operational versatility further strengthens adoption. Medium-range radars are widely integrated into mobile, vehicle-mounted, and rapidly deployable counter-drone platforms used for border surveillance, NATO deployments, and event security operations.

As European governments expand the protection of both civil and military airspace against evolving UAV threats, medium-range radar systems are expected to remain the backbone of counter-drone detection infrastructure across the region.

Based on End User:

- Military & Defense

- Homeland Security / Border Protection

- Airports & Aviation Security

- Critical Infrastructure

- Government & Public Safety

- Commercial & Industrial Facilities

- Event & Stadium Security

The military & defense segment dominates the Europe Drone Detection Radar market, accounting for about 55% of total market size, and represents the largest end-user due to the rapid expansion of counter-UAS capabilities and the growing need to safeguard national airspace against evolving unmanned threats.

European armed forces are prioritizing advanced drone detection radar as a core component of layered air-defense strategies designed to address surveillance drones, loitering munitions, and low-altitude UAVs increasingly observed in modern conflict environments.

Recent operational lessons from the Russia–Ukraine conflict have significantly accelerated this shift, highlighting the operational and strategic risks posed by small, low-cost drones capable of targeting military assets and disrupting battlefield communications. In response, defense ministries across Europe are increasing investments in next-generation radar systems capable of detecting slow, small, and low-flying aerial objects that conventional air-defense platforms often struggle to identify.

Military requirements also demand highly integrated and interoperable solutions that combine radar, electronic warfare, command-and-control, and missile defense networks to ensure rapid response in contested environments. This integration significantly increases procurement value compared with civilian applications and reinforces sustained demand. Together, these factors firmly position the Military & Defense sector as the dominant end-user, forming the foundation of long-term growth in Europe’s drone detection radar market.

Europe Drone Detection Radar Market (2026-32): Regional Projection

The United Kingdom dominates the Europe Drone Detection Radar Market with an estimated 25% share, driven by sustained investments in integrated air and missile defense programs that directly strengthen counter-drone detection and response capabilities.

A major example is the UK Ministry of Defence’s USD 150 million contract with MBDA to procure six additional Land Ceptor air-defense missile systems, effectively doubling the number of Sky Sabre systems available to the armed forces . This expansion reflects a long-term strategy focused on strengthening national airspace protection and ensuring continuous modernization of layered air-defense infrastructure.

The Sky Sabre system forms a critical pillar of the UK’s medium-range ground-based air-defense architecture and integrates advanced Saab Giraffe Agile Multi-Beam 3D radar capable of detecting aerial threats at distances of up to 120 km . Combined with sophisticated command-and-control systems and the MBDA Land Ceptor launcher equipped with CAMM and CAMM-ER missiles, the system delivers a highly networked and rapid-response air-defense capability.

Importantly, the platform is designed to counter a wide spectrum of threats, including cruise missiles, fixed-wing aircraft, and small, low-flying drones that are increasingly challenging for conventional radar systems to detect. This strong focus on modern sensor integration, rapid procurement, and advanced interception capability demonstrates the UK’s proactive approach to airspace security.

Together, these investments highlight the United Kingdom’s leading role in deploying advanced radar-enabled air-defense systems, positioning the country as a dominant contributor to Europe’s evolving drone detection radar landscape.

Gain a Competitive Edge with Our Europe Drone Detection Radar Market Report:

- Europe Drone Detection Radar Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Drone Detection Radar Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Drone Detection Radar Market Policies, Regulations, and Product Standards

- Europe Drone Detection Radar Market Trends & Developments

- Europe Drone Detection Radar Market Dynamics

- Growth Factors

- Challenges

- Europe Drone Detection Radar Market Hotspot & Opportunities

- Europe Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- Short-Range Radar (<5 km)

- Medium-Range Radar (5–10 km)

- Long-Range Radar (>10 km)

- AI-enabled / Cognitive Radar

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- X-Band Radar

- Ku-Band Radar

- Ka-Band Radar

- L-Band / S-Band Radar

- Multi-band Radar

- By Platform - Market Size & Forecast 2022-2032, USD Million

- Ground-based Radar

- Naval Radar

- Airborne Radar

- Vehicle-mounted / Portable Radar

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- Very Short Range (<2 km)

- Short Range (2–5 km

- Medium Range (5–10 km)

- Long Range (>10 km)

- By End User - Market Size & Forecast 2022-2032, USD Million

- Military & Defense

- Homeland Security / Border Protection

- Airports & Aviation Security

- Critical Infrastructure

- Government & Public Safety

- Commercial & Industrial Facilities

- Event & Stadium Security

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Poland

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- United Kingdom Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Netherlands Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Nordics Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Poland Drone Detection Radar Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Radar Type - Market Size & Forecast 2022-2032, USD Million

- By Frequency Band- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Detection Range- Market Size & Forecast 2022-2032, USD Million

- By End User - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Europe Drone Detection Radar Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Thales Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saab AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Leonardo S.p.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HENSOLDT AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Indra Sistemas, S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rheinmetall AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Terma A/S

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- QinetiQ Group plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kongsberg Defence & Aerospace AS

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Thales Group

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now