Europe Cosmetic Ingredients Market Research Report: Trends & Forecast (2026-2032)

By Ingredient Type (Natural, Synthetic, Bio-based / hybrid), By Product Type (Emulsifies, UV Absorbers, Surfactants, Antimicrobials, Emollients, Polymer, Oleo-chemical, Others), By ... Functionality (Cleansing Agents & Foamers, Aroma, Moisturizing, Specialty, Others), By End Use (Skin Care, Oral Care, Hair Care, Body Care), and others Read more

- Chemicals

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Europe Cosmetic Ingredients Market

Projected 11.18% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 7.53 Billion

Market Size (2032)

USD 14.22 Billion

Base Year

2025

Projected CAGR

11.18%

Leading Segments

By End-Use: Skin Care

Europe Cosmetic Ingredients Market Report Key Takeaways:

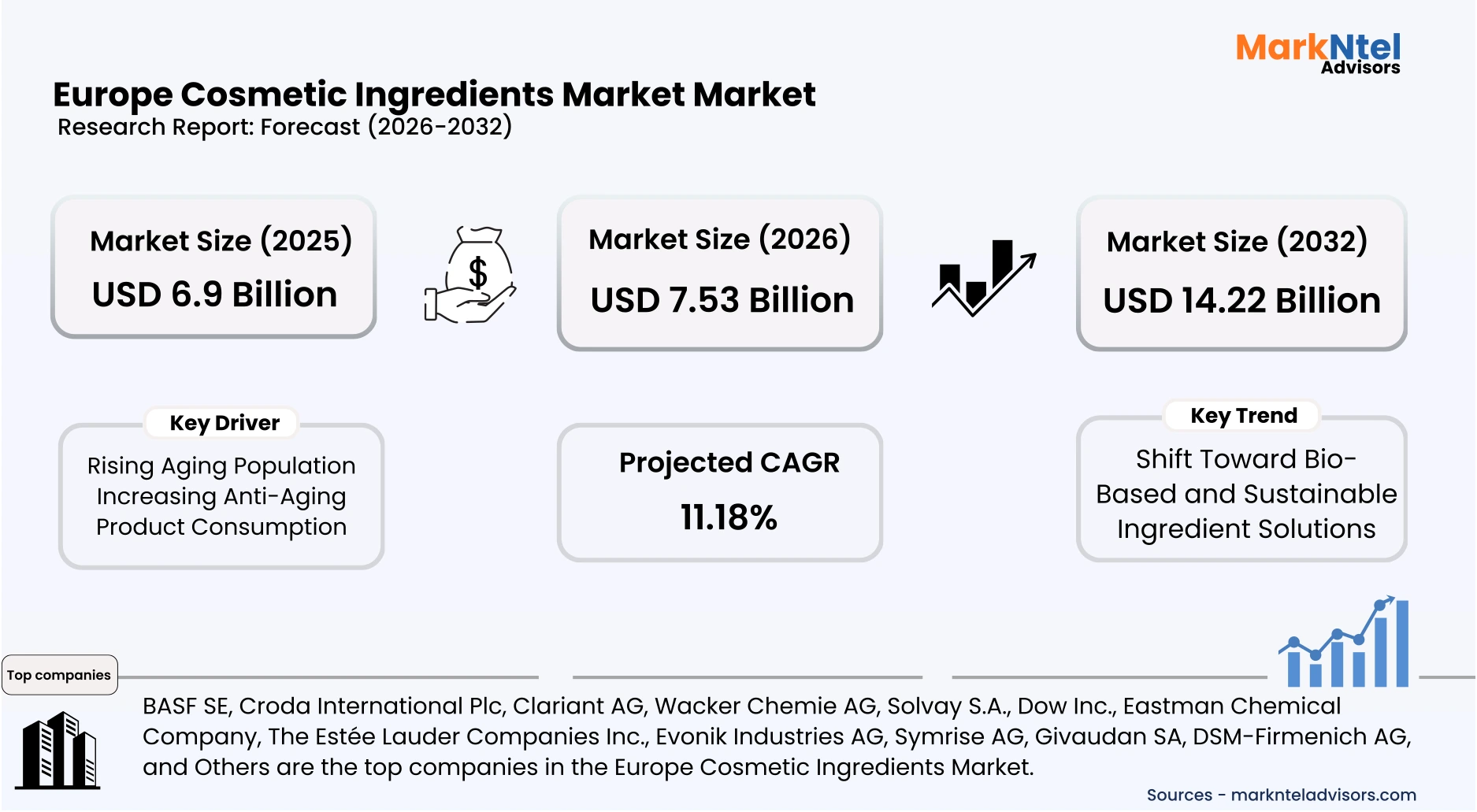

- Market size was valued at around USD 6.9 billion in 2025 and is projected to grow from USD 7.53 billion in 2026 to USD 14.22 billion by 2032, exhibiting a CAGR of 11.18% during the forecast period.

- The Germany is dominating this market with 24% market share in 2026.

- By Ingredient Type, the Synthetic segment represented a significant share of about 54% in the Europe Cosmetic Ingredients Market in 2026.

- By End-Use, the Skin Care segment represented a significant share of about 38% in the Europe Cosmetic Ingredients Market in 2026.

- Leading Cosmetic Ingredients companies in Europe are BASF SE, Croda International Plc, Clariant AG, Wacker Chemie AG, Solvay S.A., Dow Inc., Eastman Chemical Company, The Estée Lauder Companies Inc., Evonik Industries AG, Symrise AG, Givaudan SA, DSM-Firmenich AG, and Others.

Market Insights & Analysis: Europe Cosmetic Ingredients Market (2026-32):

The Europe Cosmetic Ingredients Market size was valued at around USD 6.9 billion in 2025 and is projected to grow from USD 7.53 billion in 2026 to USD 14.22 billion by 2032, exhibiting a CAGR of 11.18% during the forecast period., i.e., 2026-32.

The Europe cosmetic ingredients market has expanded steadily over the past decade, supported by the region’s strong specialty chemicals base and resilient personal care consumption. Historical growth has been reinforced by rising urbanization, higher disposable incomes, and sustained demand for skin care and hair care products across residential end users. Eurostat data shows personal consumption expenditure on personal care products in major EU economies continued to rise through 2024, underpinning ingredient demand . This structural demand base has enabled ingredient suppliers to scale production while investing in formulation performance, safety, and compliance.

In 2025, the market operates within a tightly regulated but supportive framework shaped by the EU Cosmetics Regulation (EC No. 1223/2009) and the REACH regulation, both administered by the European Commission and ECHA . Updated REACH restrictions on intentionally added microplastics, entering phased implementation from 2025, are accelerating reformulation activity and demand for alternative polymers and biodegradable ingredients. These regulatory actions have increased innovation spending while maintaining high consumer trust in cosmetic safety. Industrial and commercial end users, including contract manufacturers and professional salons, are driving higher-volume ingredient procurement to meet reformulation and compliance timelines.

Industry-led initiatives are reinforcing market momentum through sustainability and localization strategies. Leading European chemical producers have announced investments in bio-based surfactants, fermentation-derived actives, and energy-efficient manufacturing upgrades to align with the EU Green Deal and Circular Economy Action Plan. Publicly reported capacity expansions and renewable energy integration at ingredient production sites in Germany and France during 2025 have improved supply security and reduced emissions intensity . These actions directly support institutional buyers and multinational cosmetic brands seeking lower-carbon and regulation-ready ingredient portfolios.

Looking ahead, the market outlook remains positive as demographic aging, premiumization of skin care, and preventive personal care habits sustain ingredient intensity per product. Policy-driven sustainability targets, including climate neutrality objectives under EU climate law, are expected to further favor advanced, high-value ingredients over commodity inputs. Residential consumers will continue to anchor demand volumes, while commercial and industrial users drive value growth through specialized formulations. Collectively, regulatory clarity, industrial investment, and stable end-use consumption position the Europe cosmetic ingredients market for continued expansion beyond 2026.

Europe Cosmetic Ingredients Market Recent Developments:

2025: Estonian biotech firm Äio announced it completed production of the first tonne of its yeast-derived palm oil substitute, targeting cosmetic ingredient applications by year-end 2025. The sustainable substitute aims to replace tropical fats and petroleum-derived oils in formulations, aligning with eco-friendly trends in the cosmetic value chain and reducing reliance on conventional raw materials.

Europe Cosmetic Ingredients Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Fruit Juice (Fresh Juice, Fortified Juice, Fruit Nectars (High Concentration (40%–50% fruit content), Medium Concentration (30%–39% fruit content), Low Concentration (25%–29% fruit content))), Vegetable Juice, Fruit and Vegetable Blends), |

| By Source | (Not from Concentrate (NFC), From Concentrate (FC)), |

| By Packaging | (Cartons (Tetra Pak) (Single-Serve Packs, Family Packs), PET Bottles (Small-Size Bottles, Large-Size Bottles), Glass Bottles, Cans, Others), |

| By Distribution Channel | (Off-Trade (Retail) (Supermarkets & Hypermarkets, Convenience Stores, Traditional Grocery), On-Trade (HoReCa) (Hotels, Restaurants & Cafes), Online Retail), |

| By End User | (Household, Hotels, Restaurants, and Cafes (HoReCa), Institutional, Industrial), |

Europe Cosmetic Ingredients Market Driver:

Rising Aging Population Increasing Anti-Aging Product Consumption

Population aging in Europe has intensified over recent years, creating a structural and measurable expansion in demand for age-targeted cosmetic formulations. Eurostat reports that as of 2024, more than 21% of the European Union population is aged 65 or above, with the old-age dependency ratio continuing to rise. The United Nations projects that Europe will remain the world’s oldest region through 2030, reflecting sustained demographic pressure. This structural aging trend has directly expanded the consumer base for anti-aging skin care and dermo-cosmetic products, thereby increasing ingredient demand.

The impact is visible across residential end users, particularly in high-income Western European countries where older consumers maintain strong purchasing power. OECD data indicates that disposable income levels among households headed by individuals aged 55–64 remain comparatively stable across advanced European economies, supporting continued discretionary spending . Age-related skin concerns, including reduced collagen production and skin barrier weakening, increase demand for retinoids, peptides, hyaluronic acid, and antioxidant actives. This translates into higher ingredient intensity per formulation rather than merely price inflation, expanding volume requirements across skin care manufacturing.

Regulatory and institutional developments further reinforce this demand trajectory by promoting safe and clinically validated products for aging populations. The European Commission’s ongoing updates under the EU Cosmetics Regulation and chemical safety frameworks ensure controlled use of active ingredients, strengthening consumer confidence in efficacy-driven formulations. Public health discussions around healthy aging within EU policy agendas also emphasize preventive personal care and well-being . Collectively, demographic expansion of the senior population, sustained purchasing capacity, and regulatory-backed product safety create a durable, volume-driven growth driver for the Europe cosmetic ingredients market.

Europe Cosmetic Ingredients Market Trend:

Shift Toward Bio-Based and Sustainable Ingredient Solutions

The transition toward bio-based and sustainable cosmetic ingredients has accelerated due to binding European environmental and chemical policies in recent years. The EU Green Deal and Circular Economy Action Plan continue to promote lower-carbon industrial production, while the phased implementation of REACH microplastics restrictions from 2025 is driving reformulation away from certain synthetic inputs . These regulatory measures are compelling ingredient manufacturers to invest in biodegradable, renewable, and biotechnology-derived alternatives.

This shift is structurally reshaping the value chain by altering sourcing strategies, production technologies, and capital allocation patterns. In 2024, an international consortium led by Evonik Venture Capital and L’Oréal’s investment arm committed approximately USD38 million to Abolis Biotechnologies to scale biobased ingredient production using microbial fermentation . Complementing this movement, in 2026, Eastman and Kolmar Korea signed a strategic agreement to advance commercialization of biodegradable personal care materials, including Eastman’s cellulose ester technology designed to meet EU biodegradation standards, further demonstrating industrial-scale alignment with sustainable ingredient platforms . Such investments reflect long-term industrial repositioning toward biomanufacturing platforms capable of replacing fossil-based raw materials at commercial scale.

The persistence of this transformation is reinforced by legally binding EU climate objectives and sustained corporate commitments to decarbonization and sustainable sourcing. Major ingredient suppliers are integrating renewable feedstocks and enzymatic processes into core manufacturing operations, signaling structural rather than cosmetic change. As regulatory compliance, investor expectations, and consumer sustainability preferences converge, bio-based and sustainable ingredient solutions are becoming foundational to Europe’s long-term cosmetic ingredient market evolution.

Europe Cosmetic Ingredients Market Opportunity:

Growth of Dermatology-Backed and Clinical-Grade Cosmetic Ingredients

The structural opportunity for dermatology-backed and clinical-grade cosmetic ingredients is driven by rising consumer demand for scientifically substantiated efficacy and stringent EU regulatory requirements on cosmetic claims. Under EU Regulation (EC) No 1223/2009 and associated common criteria, any cosmetic claim must be supported by adequate and verifiable evidence, strengthening the need for clinically evaluated actives rather than unsubstantiated claims . This environment has increased demand for validated, performance-based ingredients that fit within rigorous safety and efficacy frameworks.

Tangible demand stems from widespread dermatological conditions across Europe, where population-based studies show that roughly 43% of adults experienced at least one skin condition over a 12-month period, including acne, eczema, and dermatitis, creating a ready market for clinical-grade formulations with therapeutic benefit . Ingredient suppliers with clinically tested actives can meet both consumer needs and regulatory expectations, thereby expanding procurement volumes in skin and scalp formulations.

This opportunity is especially favorable for new and smaller entrants because niche clinical expertise, rapid innovation in biotechnology, and specialized dermatological testing can serve as differentiators against incumbent commodity producers. Startups can collaborate with clinical research bodies and dermatologists to generate compelling evidence, enabling premium positioning and scalable growth where incumbents may be slower to adapt. In 2025, French deep-tech startup Byome Labs raised approximately USD 4.2 million to industrialize a dermatologist-informed skin microbiome analysis platform for personalized skincare , illustrating how emerging players are leveraging clinical science and data-driven validation to strengthen credibility and accelerate commercialization. Emerging players can capture high-margin segments in performance-driven personal care.

Europe Cosmetic Ingredients Market Challenge:

Lengthy Regulatory Approval Timelines for New Ingredients

Lengthy regulatory approval timelines remain a structural barrier in the Europe cosmetic ingredients market due to the stringent safety, toxicological, and documentation requirements under EU Regulation (EC) No 1223/2009 and the REACH framework. Any new cosmetic ingredient must undergo comprehensive safety assessment, toxicological profiling, and, where relevant, registration under REACH before commercial use , a process compounded by amendments such as Regulation (EU) 2025/877, which added multiple carcinogenic, mutagenic, or reproductive toxicants (CMRs) to the prohibited list effective September 1, 2025 . This adds layers of compliance and documentation for ingredient developers, extending overall approval timelines.

These regulatory requirements materially affect ingredient developers, particularly small and mid-sized enterprises lacking in-house regulatory expertise and testing infrastructure. Under REACH, registrants must submit extensive physicochemical, environmental, and toxicological data, often requiring costly laboratory studies and third-party validation. Public European Chemicals Agency (ECHA) guidance highlights that incomplete dossiers can trigger additional data requests, further extending approval timelines and increasing compliance expenditure .

The extended timelines directly restrict market scalability by delaying return on research and development investments and increasing financial risk for new entrants. Investors may hesitate to fund ingredient innovation when regulatory clearance is uncertain or prolonged. While these safeguards enhance consumer protection and environmental safety, they simultaneously constrain rapid market expansion. Consequently, regulatory approval complexity remains a systemic challenge limiting the pace of innovation and competitive entry within Europe’s cosmetic ingredients landscape.

Europe Cosmetic Ingredients Market (2026-32) Segmentation Analysis:

The Europe Cosmetic Ingredients Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Ingredients Type:

- Natural

- Synthetic

- Bio-based / hybrid

The synthetic segment dominates the Europe Cosmetic Ingredients Market, holding around 54% of total demand, primarily because high-volume personal care categories rely on engineered functional materials. Eurostat reports that the EU population exceeded 449 million in 2024, sustaining large-scale consumption of daily-use products such as shampoos, cleansers, and oral care formulations. These categories require stable surfactants, emulsifiers, and preservatives that can withstand varied storage and transport conditions, a performance profile more consistently achieved through synthetic chemistry.

Industrial capacity further reinforces this dominance. According to the European Chemical Industry Council (Cefic), Europe remains one of the world’s largest chemical production regions, with Germany as the leading producer. This strong specialty chemicals infrastructure supports continuous, standardized synthesis of cosmetic intermediates at competitive cost and scale. Such manufacturing depth allows synthetic ingredients to maintain supply reliability across multiple EU markets, which is critical for multinational cosmetic brands operating high-volume production lines.

Additionally, synthetic ingredients benefit from decades of toxicological validation and well-documented safety dossiers, reducing formulation uncertainty. Established preservatives, UV filters, and conditioning polymers have long-standing inclusion in EU safety assessments, enabling smoother product development cycles compared to newer natural alternatives. While sustainable and bio-based ingredients are growing, the combination of performance consistency, scalable production, and supply-chain resilience continues to position synthetics as the leading ingredient category in Europe.

Based on the End-Use:

- Skin Care

- Oral Care

- Hair Care

- Body Care

The skin care segment dominates the Europe Cosmetic Ingredients Market with approximately 38% of total end-use demand, largely reflecting its leadership in retail value and consumption frequency. According to Cosmetics Europe 2024, skin care represents the largest product category within the European cosmetics market, generating approximately USD33 billion in annual sales, ahead of hair care and toiletries . This strong retail base directly translates into elevated demand for emollients, UV filters, antioxidants, and active ingredients used in moisturizers, serums, and sun care products.

Demographic and consumer behavior patterns further reinforce this dominance. Europe has one of the world’s oldest populations, with a rising share of individuals aged 65 and above, which increases demand for anti-aging, hydration, and dermo-cosmetic formulations. Additionally, heightened awareness of sun protection and pollution-related skin damage has strengthened daily usage of SPF products and protective skincare solutions. These factors expand both volume and frequency of product usage, directly stimulating ingredient procurement across active, preservative, and stabilizing categories.

Premiumization and clinical positioning also contribute to the segment’s leadership. Skin care products increasingly emphasize efficacy-backed formulations, requiring specialized actives and multifunctional systems at higher inclusion rates. Compared to rinse-off categories like shampoos or body washes, leave-on skin care products demand greater formulation sophistication and higher-value ingredients. Consequently, the combined effect of demographic demand, daily-use frequency, and elevated formulation complexity positions skin care as the dominant end-use segment within Europe’s cosmetic ingredients market.

Europe Cosmetic Ingredients Market (2026-32): Regional Projection

Germany dominates the Europe Cosmetic Ingredients Market, holding around 24% of total regional demand, because it remains the largest industrial producer within the European Union. According to Eurostat industrial production statistics, Germany recorded the highest value of sold industrial output in the EU in 2024 , underscoring its position as Europe’s manufacturing backbone. This industrial strength extends into specialty chemicals, enabling Germany to supply high-volume cosmetic intermediates such as surfactants, polymers, and stabilizers at a scale unmatched by other European countries.

This dominance is reinforced by Germany’s deep-rooted chemical sector, historically accounting for a substantial portion of European chemical output and exports. The German chemical industry consistently produces an outsized share of EU chemical products, with industry analyses indicating that Germany remains a central hub for chemical manufacturing infrastructure. This capacity supports reliable ingredient supply chains feeding into skin care, hair care, and sun protection formulations across Europe, enhancing Germany’s competitive position relative to other markets.

Germany’s leadership is further maintained despite broader European industry challenges, as chemical producers continue to benefit from established industrial clusters, logistics networks, and technological expertise. Even as energy and global competitive pressures test European chemical sectors, Germany’s ability to sustain output and export capabilities supports ongoing ingredient demand. As a result, the depth of manufacturing infrastructure, export orientation, and overall industrial output synergistically position Germany ahead of other European countries in cosmetic ingredient production and market share.

Gain a Competitive Edge with Our Europe Cosmetic Ingredients Market Report:

- Europe Cosmetic Ingredients Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Europe Cosmetic Ingredients Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Cosmetic Ingredients Market Policies, Regulations, and Product Standards

- Europe Cosmetic Ingredients Market Trends & Developments

- Europe Cosmetic Ingredients Market Dynamics

- Growth Factors

- Challenges

- Europe Cosmetic Ingredients Market Hotspot & Opportunities

- Europe Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- Natural

- Synthetic

- Bio-based / hybrid

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Emulsifies

- UV Absorbers

- Surfactants

- Antimicrobials

- Emollients

- Polymer

- Oleo-chemical

- Others

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- Cleansing Agents & Foamers

- Aroma

- Moisturizing

- Specialty

- Others

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Skin Care

- Oral Care

- Hair Care

- Body Care

- By Country

- Germany

- The UK

- France

- Italy

- Spain

- BENELUX

- Switzerland

- Rest of Europe

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- The UK Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- BENELUX Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Switzerland Cosmetic Ingredients Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Ingredient Type- Market Size & Forecast 2022-2032, USD Million

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Functionality- Market Size & Forecast 2022-2032, USD Million

- By End Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Europe Cosmetic Ingredients Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- BASF SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Croda International Plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Clariant AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Wacker Chemie AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Solvay S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dow Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Eastman Chemical Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Estée Lauder Companies Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Evonik Industries AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Symrise AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Givaudan SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DSM-Firmenich AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BASF SE

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now