China Bags & Luggage Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Product Type (Bags, Luggage), By Price Category (Luxury, Mass/Economy, Premium), By Application (Travel, Business), By Distribution Channel (Dealers & Distributors, Retail Store ... s, Online), Read more

- FMCG

- Mar 2026

- Pages 150

- Report Format: PDF, Excel, PPT

China Bags & Luggage Market

Projected 3.91% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 34.72 Billion

Market Size (2032)

USD 43.71 Billion

Base Year

2025

Projected CAGR

3.91%

Leading Segments

By Product Type: Bags

China Bags & Luggage Market Report Key Takeaways:

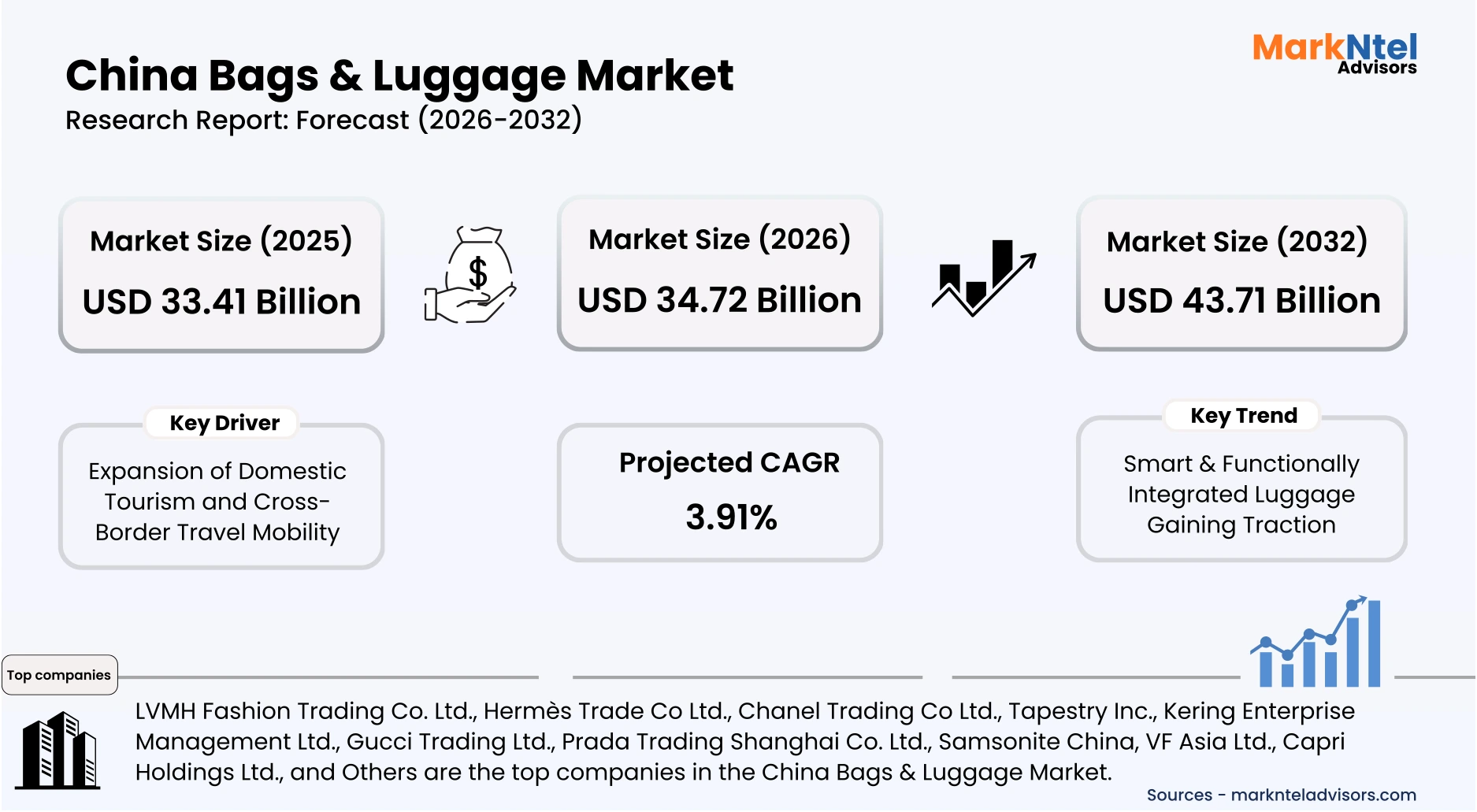

- The China Bags & Luggage Market size was valued at USD 33.41 billion in 2025 and is projected to grow from USD 34.72 billion in 2026 to USD 43.71 billion by 2032, exhibiting a CAGR of 3.91% during the forecast period.

- Southern China is the leading region with a significant share of 35% in 2026.

- By Product Type, the Bags segment represented a significant share of about 88% in the China Bags & Luggage Market in 2026.

- By Distribution Channel, the Retail stores segment presented a significant share of about 60% in the China Bags & Luggage Market in 2026.

- Leading Bags and luggage Companies in China are LVMH Fashion Trading Co. Ltd., Hermès Trade Co Ltd., Chanel Trading Co Ltd., Tapestry Inc., Kering Enterprise Management Ltd., Gucci Trading Ltd., Prada Trading Shanghai Co. Ltd., Samsonite China, VF Asia Ltd., Capri Holdings Ltd., and Others.

Market Insights & Analysis: China Bags & Luggage Market (2026-32):

The China Bags & Luggage Market size was valued at USD 33.41 billion in 2025 and is projected to grow from USD 34.72 billion in 2026 to USD 43.71 billion by 2032, exhibiting a CAGR of 3.91% during the forecast period. i.e., 2026-32.

China’s bags and luggage industry has expanded consistently alongside broader shifts in domestic consumption patterns, driven by strategic government support for household spending and retail growth. Retail sales of consumer goods in early 2025 recorded a 4% increase, reflecting a gradual rebound in demand for fashion and everyday utility products that include bags and accessories. National policies unveiled in 2025 focused on boosting income for urban and rural residents through targeted consumption incentives and improved social support measures, which strengthen overall purchasing capacity for consumer goods. These measures have contributed to a resilient demand base that underpins the historical growth trajectory of personal goods markets.

Demographic and economic forces continue to support market expansion through 2026 and beyond, as China’s urban population increases and household spending structures evolve. Consumer expenditure patterns in early 2025 indicate a continued shift toward discretionary categories such as leisure and travel. This transition toward experience-oriented spending reflects growing household confidence and mobility recovery across urban China. As tourism and short-distance travel activity expand, demand for travel-related goods, including luggage and travel accessories, tends to strengthen in parallel. The expansion of leisure travel and intra-regional mobility, facilitated by improvements in transport infrastructure, enhances the visibility of luggage demand among both domestic and inbound travellers. Growing middle-income cohorts in inland and coastal urban centres further diversify consumption drivers across market segments.

China’s retail sales of consumer goods grew significantly and are expected to exceed USD 7 trillion in 2025, indicating rising consumer demand. China’s departure tax refund policy was revised in 2025, lowering the minimum purchase threshold to USD 27 and raising cash refund ceilings to incentivize inbound tourist spending and broaden the range of eligible stores. These policies encourage the establishment of new retail formats and improve accessibility for quality consumer products, thereby expanding competitive retail landscapes. Concurrently, consumer-focused initiatives such as national shopping campaigns and expanded tax refund policies for departing travellers enhance market participation by lowering costs and incentivising discretionary spending.

Industry responses to policy actions include localised brand promotions, enhanced distribution networks, and strategic participation in nationally supported retail events that attract domestic and international shoppers. Enhanced infrastructural investment in duty-free zones and high-traffic travel hubs improves the reach of luggage and accessory retailers, aligning business expansion with broader tourism growth. With China’s continued pursuit of consumption-led economic balance and ongoing urbanisation trends, demand for bags and luggage is expected to sustain its contribution to overall retail value in the near and medium term.

China Bags & Luggage Market Recent Developments:

- 2026: Celine 2026 Spring Handbag Launch in China: Luxury brand Celine rolled out its 2026 Spring New Luggage small-size handbag, bringing lighter, lambskin-textured options and multiple colorways tailored for urban everyday use. Thi s release reflects the brand's broadening handbag offerings in key Asian markets, including China.

China Bags & Luggage Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Bags, Luggage), |

| By Price Category | (Luxury, Mass/Economy, Premium), |

| By Application | (Travel, Business), |

| By Distribution Channel | (Dealers & Distributors, Retail Stores, Online), |

China Bags & Luggage Market Driver:

Expansion of Domestic Tourism and Cross-Border Travel Mobility

The most influential structural driver of China’s bags and luggage market is the sustained expansion of domestic and outbound travel, which directly generates repeat demand for travel gear. According to the Ministry of Culture and Tourism, China recorded over 5 billion domestic tourist trips in 2024, with tourism revenue exceeding USD 700 billion , reflecting a strong recovery in mobility intensity. In 2025, authorities further expanded visa-free entry policies and optimised port clearance procedures to stimulate inbound and outbound travel flows. These measures structurally increase luggage replacement cycles and first-time purchases, creating measurable volume growth rather than temporary demand spikes.

The Civil Aviation Administration of China reported continued growth in passenger throughput in early 2025, with major airports surpassing pre-pandemic operational capacity levels. Higher passenger volumes translate directly into greater demand for suitcases, duffel bags, and travel accessories across both mass and premium categories. Unlike fashion-driven handbag purchases, travel-linked luggage demand is usage-dependent, meaning increased mobility mechanically drives unit sales. This cause-and-effect relationship ensures that every incremental rise in trip frequency expands product turnover in quantifiable terms.

China expanded its visa-waiver program to include 50+ countries in 2026, enabling up to 30-day visa-free stays for tourism, business, and transit a broader effort to boost inbound travel. Government initiatives supporting regional tourism clusters and holiday travel incentives have broadened participation beyond tier-one cities, expanding the consumer base geographically. As travel normalises into a high-frequency lifestyle behaviour among middle-income households, luggage demand scales proportionally with passenger traffic. Consequently, tourism expansion functions as a systemic volume catalyst, materially enlarging market size rather than merely elevating product prices.

China Bags & Luggage Market Trend:

Smart & Functionally Integrated Luggage Gaining Traction

A defining structural trend in China’s bags and luggage market is the integration of smart and multifunctional features into mainstream travel products. Companies such as Samsonite International S.A., through its premium brand Tumi, have introduced tracking-enabled solutions like the TUMI Global Locator to enhance travel security and monitoring . These developments reflect a structural transition from purely design-led differentiation toward technology-driven performance value.

The trend has accelerated alongside China’s rapid digital infrastructure expansion and widespread smartphone penetration. Domestic technology-oriented manufacturers such as Cowarobot have launched smart suitcases featuring follow-me robotics, Bluetooth-enabled anti-loss alerts, and integrated security systems. Similarly, Echolac introduced app-linked locking and self-weighing smart luggage models to enhance functional convenience. This shift is reshaping product development processes by integrating software, battery compliance engineering, and digital ecosystem compatibility into traditional manufacturing models.

The structural implications extend beyond feature upgrades, raising research and development intensity and creating higher technological entry barriers within the industry. Airlines’ lithium battery safety regulations have encouraged removable power banks and certified battery designs, prompting compliance-focused innovation. Functional enhancements such as impact-resistant shells and modular compartments broaden applicability to both leisure and business travellers. Because these features address security, connectivity, and efficiency needs tied to long-term mobility patterns, smart and functional luggage is positioned to remain a sustained force in market evolution. China also exports smart luggage products with features like GPS, weight sensors, and USB charging. Rapidly increasing market share, capturing significant proportions of luggage exports, and demonstrating widespread integration of smart functionality in travel gear.

China Bags & Luggage Market Opportunity:

Expansion of Wholesale and OEM/ODM Manufacturing for Export Diversification

A significant market opportunity for new entrants in China’s bags and luggage sector lies in wholesale and OEM/ODM manufacturing aligned with export diversification strategies. China remains the world’s largest luggage exporter, with customs data showing luggage and similar containers exports exceeding USD 34 billion in 2024, affirming the substantial production and export scale that underpins OEM/ODM business potential. In 2025, authorities continued to support foreign trade stabilisation through export credit insurance expansion and cross-border trade facilitation measures. These structural policies sustain overseas order flows, creating consistent demand for contract manufacturing services.

The opportunity exists because global brands increasingly seek flexible sourcing models that reduce concentration risk and enable shorter production cycles. China’s mature supply chain clusters in provinces such as Guangdong and Zhejiang provide integrated access to materials, hardware components, and logistics infrastructure. OEM and ODM arrangements allow foreign retailers and emerging labels to outsource design, prototyping, and bulk production while focusing on branding and distribution. This demand directly translates into scalable factory utilisation and volume-based revenue streams for capable manufacturers.

The model is particularly advantageous for smaller or new players because OEM/ODM entry requires lower marketing expenditure than launching proprietary brands. Producers can leverage standardised production lines, adopt modular customisation, and build long-term contracts with international buyers. The 2025 Government Work Report and related policy guidance explicitly commit to strengthening foreign trade stability, expanding export credit insurance, improving financial services related to foreign exchange and settlement , and boosting cross-border e-commerce logistics. These actions support overseas orders and help manufacturers scale export production. As global sourcing strategies continue to emphasise reliability and cost efficiency, wholesale and customisation services present a structurally durable growth pathway. Several Policies on Promoting Service Exports issued by the Ministry of Commerce and other departments in late 2025 expanded export credit insurance coverage and financing support for exporters, including risk mitigation and premium optimization advantages for OEM /ODM companies with global clients.

China Bags & Luggage Market Challenge:

Rising Raw Material & Labor Costs Limiting Competitive Production

China’s manufacturing cost structure has been rising due to higher raw material prices for key inputs, e.g., leather, textiles, plastics, metal hardware, and structural increases in labor wages.

Urban manufacturing wages in China have continued to rise, with average annual salaries for manufacturing workers increasing over recent years. In 2024, the average annual wage in China’s manufacturing sector reached about USD 14,700 in the public sector and USD 9,900 in the private sector, reflecting structural labor cost increases. In addition, global commodity price volatility for inputs such as synthetic textiles and metal hardware, driven by supply chain disruptions and energy price fluctuations, has raised production expenses. These cost increases are not temporary but reflect medium-term structural adjustments in China’s manufacturing landscape.

Higher input costs strain profit margins for bag and luggage producers, especially OEM/ODM manufacturers operating on thin contract margins. Producers face a direct price impact on essential materials such as textiles and coated fabrics, which are key components of luggage shells and bag linings. Smaller manufacturers, in particular, find it difficult to absorb price increases without raising product prices, which undermines competitiveness in low-margin export contracts and domestic price-sensitive segments. This trade-off between cost pressures and pricing flexibility directly affects production scalability and investment decisions.

Rising production costs discourage capacity expansion and new factory investment, particularly among SMEs that lack large financial buffers. Higher labor costs can lead manufacturers to relocate production to lower-cost regions, fragmenting supply chain clusters within China.

China’s textile and fibrous industries, major suppliers of fabrics used in bags, show continued raw material cost pressures, e.g., increasing polyester yarn imports and fabric dynamics in 2025, signaling persistent input cost complexities . As cost pressures persist, production competitiveness weakens, slowing growth in volume and innovation relative to regional peers.

China Bags & Luggage Market (2026-2032) Segmentation Analysis:

The China Bags & Luggage Market study of MarkNtel Advisors evaluates and highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as follows:

Based on Product Type:

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Handbags

- Wallets & Coin Pouches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

- Others

Bags represent the leading product segment in China’s market with a market share of 88%, driven by sustained urban consumption and fashion-oriented demand. Official data from the National Bureau of Statistics shows that retail sales of consumer goods excluding automobiles grew 4.4 % in 2025, demonstrating resilient spending in physical goods , which include fashion items such as bags. Urban consumers increasingly purchase handbags, crossbody bags, and backpacks as lifestyle and professional essentials.

Unlike travel-driven luggage demand, bags benefit from frequent replacement cycles linked to fashion trends and daily utility. Policy measures encouraging domestic consumption further reinforce this segment’s leadership. Backpacks are evolving with urban tech and minimalist designs appealing to students and young professionals. Younger Chinese consumers increasingly view handbags not only as fashion accessories but also as expressions of personal identity and lifestyle preferences. This behavioral shift supports recurring purchases across seasonal collections.

Clutches and wallets remain significant within the premium and gifting segments. These small leather goods often serve as entry-level luxury purchases, particularly during major shopping festivals and holiday seasons. Overall, diversified end-user applications ranging from education and employment to fashion and travel are reinforcing the structural dominance of multiple bag sub-categories within China’s broader market landscape. Bags cater to diverse end users, students, professionals, and commuters, ensuring broad demand coverage. The segment’s adaptability to both fashion and utility trends enhances resilience across economic cycles. Consequently, bags maintain structural dominance supported by consumption, policy, and supply chain advantages.

Based on the Distribution Channel:

- Dealers & Distributors

- Retail Stores

- Online

Retail stores remain the dominant distribution channel with a market share of 60% due to strong consumer preference for in-person evaluation of quality and design. Official retail data from the National Bureau of Statistics of China indicate continued growth in brick-and-mortar apparel and accessory sales in major cities. Physical stores allo w customers to assess material durability, stitching, and size-critical factors in bag purchases.

This tactile evaluation supports higher conversion rates compared to purely digital channels. Government-backed urban commercial development policies in 2025 encouraged modernization of shopping districts and experiential retail formats.

Recently, multiple global luxury brands, including Dior, Louis Vuitton, Tiffany & Co., and others, have opened flagship stores at Taikoo Li Sanlitun following a major renovation of the shopping district, boosting foot traffic and elevating retail presence. Such initiatives strengthen foot traffic in malls and specialty stores. Premium and luxury brands particularly rely on flagship retail outlets to reinforce brand positioning.

Retail stores also provide after-sales service, repairs, and warranty support, increasing consumer trust. Franchise networks and department store partnerships extend geographic reach into emerging urban clusters. For mid-to-premium bags, in-store merchandising and brand storytelling remain influential purchasing drivers. Therefore, retail stores sustain dominance through experiential value, policy support, and structured distribution networks.

China Bags & Luggage Market (2026-2032) Regional Analysis:

Southern China, with a market share of 35%, is one of the largest bag and luggage manufacturing hub in the world. Cities in Guangdong province and surrounding areas have developed industrial clusters where many suppliers, factories, and designers are located close together. This allows manufacturers to get materials like textiles, zippers, and hardware quickly and cheaply, reducing costs and speeding up production. Around Guangzhou and nearby cities, thousands of bag and luggage factories make products ranging from backpacks and handbags to travel suitcases, with an annual output value of 100 billion .

Because all the parts and raw materials are nearby, leather, fabrics, metal fittings, packaging, etc., companies can make products quickly and scale up for large orders. This is a big advantage over countries that have to import parts from far away . The industry has moved beyond just basic bags: Chinese manufacturers are creating smart luggage like suitcases with GPS tracking and USB charging and using eco-friendly or high-performance materials. For example, some smart luggage models combine automatic weighing with anti-loss Bluetooth features, setting new trends that other countries are also adopting.

Local and regional implementation measures under the Greater Bay Area initiative also include specific promotion of integration between manufacturing and service sectors, digital transformation of quality management, and infrastructure support to facilitate industrial competitiveness, again highlighting how national and local levels reinforce policy advantages for companies in the region.

Gain a Competitive Edge with Our China Bags & Luggage Market Report:

- The China Bags & Luggage Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The China Bags & Luggage Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- China Bags & Luggage Market Policies, Regulations, and Product Standards

- China Bags & Luggage Market Trends & Developments

- China Bags & Luggage Market Dynamics

- Growth Factors

- Challenges

- China Bags & Luggage Market Hotspot & Opportunities

- China Bags & Luggage Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Outlook

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Bags

- Cross Body Bags

- Bags and Backpacks

- Business Bags

- Duffle Bags

- Clutches

- Handbags

- Wallets & Coin Pouches

- Others

- Luggage

- Soft Luggage

- Hard Luggage

- Wheeled Luggage

- Non-Wheeled Luggage

- Others

- Bags

- By Price Category- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Luxury

- Mass/Economy

- Premium

- By Application- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Travel

- Business

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Dealers & Distributors

- Retail Stores

- Online

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- North

- East

- Southwest

- Northwest

- North East

- South

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- China Luxury Bags & Luggage Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Outlook

- By Price Category- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Application- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- China Mass/Economy Bags & Luggage Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Outlook

- By Price Category- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Application- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- China Premium Bags & Luggage Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- By Units Sold (Thousand Units)

- Market Share & Outlook

- By Price Category- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Application- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- By Region- Market Size & Forecast 2022-2032, USD Million & Thousand Units

- Market Size & Outlook

- China Bags & Luggage Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- LVMH Fashion Trading Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hermès Trade Co Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chanel Trading Co Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tapestry Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kering Enterprise Management Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gucci Trading Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prada Trading Shanghai Co. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Samsonite China

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- VF Asia Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Capri Holdings Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- LVMH Fashion Trading Co. Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now