Brazil Defense Software Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Type (Command & Control Software, ISR & Analytics Software, Cybersecurity Software, Communications Software, Training & Simulation Software), By Deployment (On-Premises Secure N ... etworks, Cloud-Enabled Platforms, Edge / Tactical Deployments), By End User (Ministry of Defense, Army, Navy, Air Force, Homeland Security Agencies, Intelligence Organizations), and others Read more

- Aerospace & Defense

- Feb 2026

- Pages 140

- Report Format: PDF, Excel, PPT

Brazil Defense Software Market

Projected 10.34% CAGR from 2026 to 2032

Study Period

2026-2032

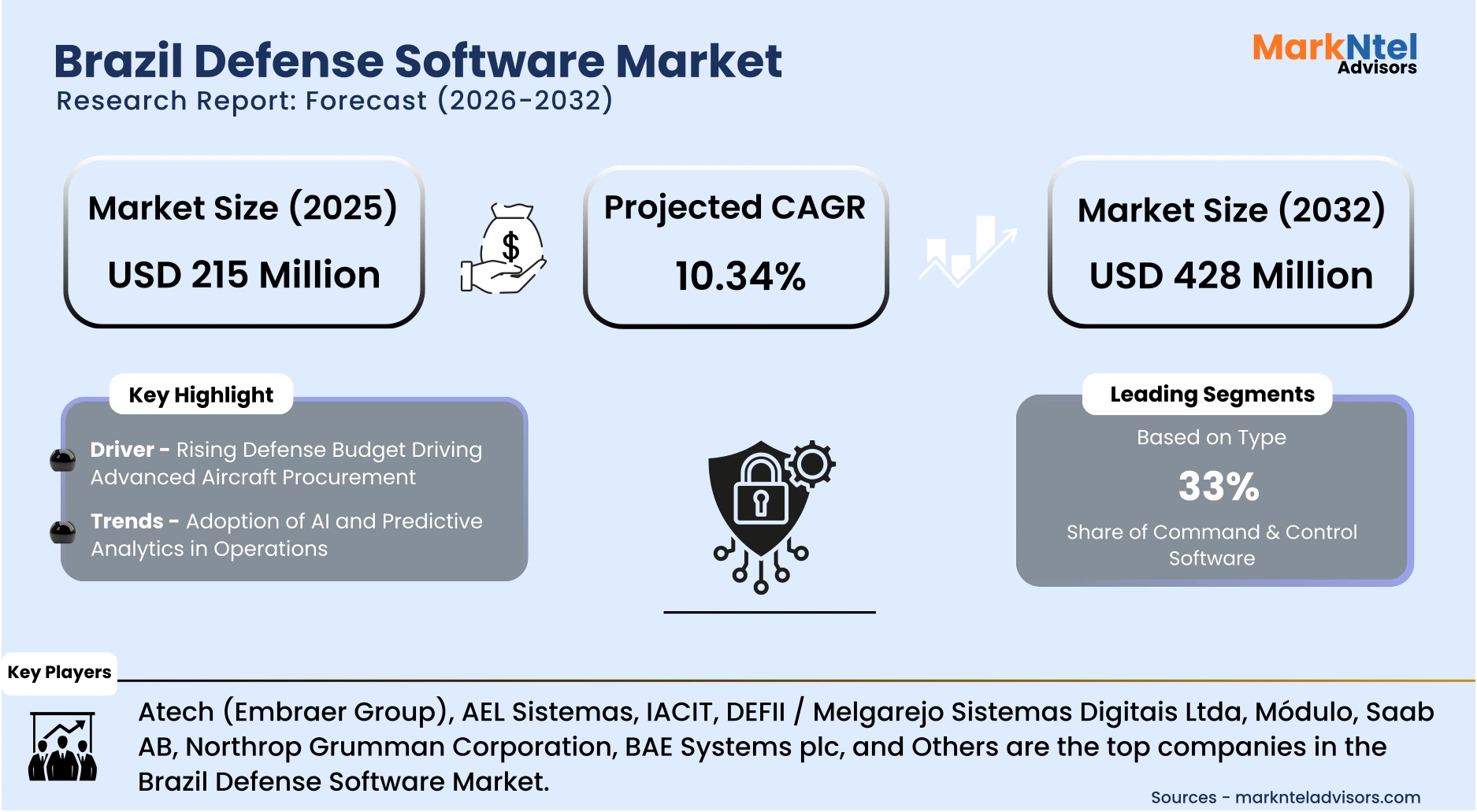

Market Size (2025)

USD 215 Million

Market Size (2032)

USD 428 Million

Base Year

2025

Projected CAGR

10.34%

Leading Segments

By Type: Command & Control Software

Brazil Defense Software Market Report Key Takeaways:

- Market size was valued at around USD 215 million in 2025 and is projected to reach USD 428 million by 2032. The estimated CAGR from 2026 to 2032 is around 10.34%, indicating strong growth.

- By Type, the Command & Control Software segment captured a significant share of about 33% in the Brazil Defense Software Market in 2025.

- By End user, the Ministry of Defense seized a substantial share of about 28% in 2025.

- Leading Defense Software Companies in Brazil are Atech (Embraer Group), AEL Sistemas, IACIT, DEFII / Melgarejo Sistemas Digitais Ltda, Módulo, Saab AB, Northrop Grumman Corporation, BAE Systems plc, and Others.

Market Insights & Analysis: Brazil Defense Software Market (2026-32):

The Brazil Defense Software Market size was valued at around USD 215 million in 2025 and is projected to reach USD 428 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 10.34% during the forecast period, i.e., 2026-32.

Brazil’s defense software ecosystem has evolved in step with national strategic policy emphasizing technological autonomy, cybersecurity, and digital interoperability. In 2025, updated National Defense Policy (PND) and National Defense Strategy (END) documents explicitly prioritized cyber and space domains alongside traditional capabilities, reinforcing software’s role in command, control, and integrated system operations across the armed forces . These frameworks link defense digitalization directly to sovereignty and national security objectives.

Current market conditions are shaped by robust government support for domestic technology development under the New Industry Brazil action programme, particularly “Mission 6,” which allocates approximately USD19.5 billion by 2026 to strategic defense technologies that include cyber and digital systems infrastructure . This investment signals a sustained effort to increase local content and reduce dependence on imported systems, a key driver for domestic software demand.

Regulatory developments in cybersecurity are also fueling defense software uptake. The E‑Ciber National Cybersecurity Strategy (Decree No. 12,573/2025) strengthens governance, oversight, and minimum security standards for critical infrastructure and public services, which in turn increases demand for secure software platforms across defense networks and sensitive government systems . This policy explicitly encourages the private sector to adopt higher cybersecurity standards and supports public‑private collaboration on digital security solutions.

Future market prospects for Brazil’s defense software sector remain strong as defense spending is projected to rise with federal budget documents indicating a 6.23% increase in defense appropriations for 2026, including funds earmarked for cyber‑defense, border systems such as SISFRON, and integrated air and maritime surveillance initiatives . These expenditures reflect sustained institutional demand for software‑centric systems in operational, training, and security functions across the Ministry of Defense and individual services.

Brazil Defense Software Market Recent Developments:

- 2025 : Atech, an Embraer Group company, has opened its first office outside Brazil in Lisbon to expand into defense, security, and air traffic management. The firm develops systems such as the N-TDMS for AH-15B helicopters, SUBTICS submarine consoles, and supports Brazil’s nuclear-powered submarine and Tamandaré-class frigate programs.

Brazil Defense Software Market Scope:

| Category | Segments |

|---|---|

| By Type | (Command & Control Software, ISR & Analytics Software, Cybersecurity Software, Communications Software, Training & Simulation Software), |

| By Deployment | (On-Premises Secure Networks, Cloud-Enabled Platforms, Edge / Tactical Deployments), |

| By End User | (Ministry of Defense, Army, Navy, Air Force, Homeland Security Agencies, Intelligence Organizations) |

Brazil Defense Software Market Driver:

Rising Defense Budget Driving Advanced Aircraft Procurement

Brazil has steadily increased federal defense spending to enhance technological and digital capabilities. According to official government releases, the 2026 defense budget was set at approximately USD 26.4 billion, a 6.23 % increase over 2025, with significant allocations for cyber-defense and command-and-control software systems. These funds reflect a strategic focus on software-intensive platforms across the Army, Navy, and Air Force .

Government initiatives such as the New Industry Brazil (NIB) Mission 6 emphasize domestic development of strategic defense technologies, including secure communications, ISR analytics, and digital training systems . By supporting local software capabilities, these programs aim to reduce dependence on imported systems and strengthen operational autonomy across military operations.

The impact of rising budgets extends beyond procurement, driving investments in software integration, secure networks, and digital infrastructure upgrades. Future frameworks, including the National Cybersecurity Legal Framework (Bill No. 4752/2025), will further increase adoption of mission-critical software . These budgetary commitments directly fuel demand for advanced defense software, enabling improved efficiency, cybersecurity resilience, and modernization of Brazil’s armed forces.

Brazil Defense Software Market Trend:

Adoption of AI and Predictive Analytics in Operations

The adoption of artificial intelligence (AI) and predictive analytics is becoming a defining trend in Brazil’s defense software landscape as military and aerospace stakeholders integrate data‑driven capabilities into operational systems. For instance, Embraer’s Smart Planning platform, developed with Brazilian data specialist Aquarela Analytics , which leverages AI to analyze more than two terabytes of production data to forecast material needs, optimize inventory, and support strategic decision‑making in aircraft manufacturing and logistics, underscoring AI’s role in enhancing complex operational workflows.

Brazil’s broader national commitment to AI adoption is further demonstrated by the Brazilian Artificial Intelligence Plan (PBIA 2024–2028), a government initiative earmarking approximately USD 4 billion to advance AI research, infrastructure , and public‑sector applications, establishing a policy environment that indirectly supports defense software development in areas such as predictive analytics, autonomous systems, and secure data processing.

Looking beyond 2025, Brazil’s strategic direction includes enhancing computational infrastructure and climate resilience for AI systems, including upgrades to the Santos Dumont supercomputer to support high‑performance analytics . Such national initiatives will increasingly enable defense agencies to deploy AI for real‑time threat assessment, autonomous mission support, and predictive maintenance of defense assets.

In conclusion, the integration of AI and predictive analytics into defense software operations is a sustained trend driven by both corporate innovation and national policy, and it is poised to significantly elevate Brazil’s defense operational effectiveness and software market expansion through the latter half of the decade.

Brazil Defense Software Market Opportunity:

Growing Demand for Cybersecurity and Critical Infrastructure Software

Brazil is witnessing a growing need for cybersecurity and critical infrastructure software as the Armed Forces and defense agencies modernize digital systems. Government initiatives, such as the E-Ciber National Cybersecurity Strategy (Decree No. 12,573/2025), set strict security standards for critical defense networks, communications, and operational platforms, creating a clear demand for secure, software-based solutions .

The trend is reinforced by increasing integration of command and control, ISR analytics, and automated operational systems, which require robust cybersecurity frameworks to protect sensitive military data. Investments in network protection, encrypted communications, and threat detection platforms present opportunities for software providers to deliver solutions that enhance resilience and operational continuity across Army, Navy, and Air Force digital systems.

Looking ahead, planned upgrades to border surveillance (SISFRON), naval vessels, and air defense platforms will further expand the need for critical infrastructure software, including AI-assisted monitoring and secure data analytics. This growing demand positions cybersecurity solutions as a key growth segment, enabling Brazilian defense software companies to develop innovative platforms that protect national security assets and support digital transformation initiatives.

Brazil Defense Software Market Challenge:

Escalating Cybersecurity Threats and Network Vulnerabilities

Brazil’s defense software landscape is increasingly challenged by complex cybersecurity threats and vulnerabilities as digital systems become more central to military operations. In September 2025, Brazil’s Ministry of Defence reported that the Guardião Cibernético 7.0 exercise brought together 169 organizations and around 750 participants from 20 countries to strengthen resilience against attacks targeting national critical infrastructure, highlighting how cyber threats have become a strategic concern requiring collaborative responses .

The need for robust defense software is underscored by the expanding digital attack surface across defense and critical infrastructure sectors. For instance, studies have shown that many Brazilian organizations lack sophisticated cyber defenses, as estimated that a substantial portion of Brazilian companies do not have adequate incident response plans, indicating wider systemic vulnerabilities that could also impact defense networks.

Looking ahead, the complexity and frequency of cyber threats are expected to rise as defense systems incorporate AI, networked sensors, and integrated command platforms. In response, Brazil is enhancing institutional capabilities, including cyber defense training and operational centers, but persistent threats will require significant investment in secure software development, real‑time monitoring, and rapid incident mitigation to protect national security assets.

Brazil Defense Software Market (2026-32) Segmentation Analysis:

The Brazil Defense Software Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Type:

- Command & Control Software

- ISR & Analytics Software

- Cybersecurity Software

- Communications Software

- Training & Simulation Software

The Command & Control Software segment dominates the Brazil Defense Software Market, holding around 33% market share, because it serves as the central backbone for operational decision-making across the Armed Forces. These systems integrate real-time intelligence, surveillance, reconnaissance, and communication data, enabling coordinated responses across the Army, Navy, and Air Force. As a result, demand for command and control software is higher and more consistent compared to other segments, such as training & simulation or communications software.

Brazil’s defense modernization programs, including updates to border surveillance networks, air defense command systems, and naval operations platforms, rely heavily on command and control software for secure data management and mission execution. This operational dependency ensures that the installed user base remains large and engaged, similar to the way fleet vehicles maintain continuous replacement demand in other industries. Leading defense initiatives such as integrated ISR operations and AI-assisted battlefield monitoring further reinforce the segment’s centrality in national defense infrastructure.

Additionally, the standardized nature of command and control platforms across multiple branches of the military allows for efficient software deployment, upgrades, and maintenance, supporting higher volume adoption than specialized or niche systems. The combination of strategic importance, consistent operational usage, and integration across multiple platforms positions the Command & Control Software segment as the dominant contributor to Brazil’s defense software market.

Based on End User:

- Ministry of Defense

- Army

- Navy

- Air Force

- Homeland Security Agencies

- Intelligence Organizations

The Ministry of Defense dominates the Brazil Defense Software Market, accounting for approximately 28% market share, because it represents the primary institutional buyer for software solutions across all branches of the armed forces. The Ministry directly funds and oversees procurement of command and control systems, ISR analytics platforms, cybersecurity tools, and mission planning software, ensuring a large and consistent volume demand compared to other end-user segments, such as the Army, Navy, or Air Force individually.

Government-led defense modernization programs, including border surveillance upgrades, air defense systems, and naval operational platforms, are primarily orchestrated through the Ministry of Defense. This centralized approach guarantees predictable procurement cycles and structured budgets, similar to how large-scale institutional purchases maintain steady market demand in other sectors. The Ministry’s extensive operational scope ensures continuous software deployment, updates, and integration across multiple services, reinforcing its dominant position as an end user.

Additionally, the Ministry of Defense sets technical standards, regulatory compliance requirements, and interoperability mandates, which drive widespread adoption of standardized software solutions. This combination of high-volume procurement, institutional control, and systemic influence allows the Ministry to maintain a leading share in the market, positioning it as the dominant contributor to Brazil’s defense software end-user demand.

Gain a Competitive Edge with Our Brazil Defense Software Market Report:

- Brazil Defense Software Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Brazil Defense Software Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Brazil Defense Software Market Policies, Regulations, and Product Standards

- Brazil Defense Software Market Trends & Developments

- Brazil Defense Software Market Dynamics

- Growth Factors

- Challenges

- Brazil Defense Software Market Hotspot & Opportunities

- Brazil Defense Software Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type- Market Size & Forecast 2022-2032, USD Million

- Command & Control Software

- ISR & Analytics Software

- Cybersecurity Software

- Communications Software

- Training & Simulation Software

- By Deployment- Market Size & Forecast 2022-2032, USD Million

- On-Premises Secure Networks

- Cloud-Enabled Platforms

- Edge / Tactical Deployments

- By End User- Market Size & Forecast 2022-2032, USD Million

- Ministry of Defense

- Army

- Navy

- Air Force

- Homeland Security Agencies

- Intelligence Organizations

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Command & Control Software Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil ISR & Analytics Software Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Cybersecurity Software Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Communications Software Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Training & Simulation Software Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Deployment- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Defense Software Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Atech (Embraer Group)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AEL Sistemas

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- IACIT

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DEFII / Melgarejo Sistemas Digitais Ltda

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Módulo

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Saab AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Northrop Grumman Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Atech (Embraer Group)

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now