Asia Pacific Insulation Paper Market Research Report: Trends & Forecast (2026-2032)

By Type (Cream Pressboard, Cable Insulation Paper, Transformer Insulation Paper, Aramid Fibre Paper, Others), By Application (Power Cable Insulation, Conductor Insulation, Barrier ... Insulation, Transformer Winding Insulation, Motor and Generator Insulation, Switchgear Insulation, Others), By End-User Industry (Power Utilities, Electrical and Electronics, Automotive, Industrial Machinery, Renewable Energy, Others), By Form (Roll Insulation Paper, Sheet Insulation Paper, Coil and Spool Paper, Laminated Paper Form), By Grade (Low Voltage Grade, Medium Voltage Grade, High Voltage Grade, Extra High Voltage Grade), By Material (Cellulose Fiber, Aramid Fiber, Polyester Fiber, Composite Fiber, Others), Read more

- Buildings, Construction, Metals & Mining

- Mar 2026

- Pages 285

- Report Format: PDF, Excel, PPT

Asia Pacific Insulation Paper Market

Projected 4.49% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 2.25 Billion

Market Size (2032)

USD 4.16 Billion

Base Year

2025

Projected CAGR

4.49%

Leading Segments

By Material: Cellulose Fiber

Asia Pacific Insulation Paper Market Report Key Takeaways:

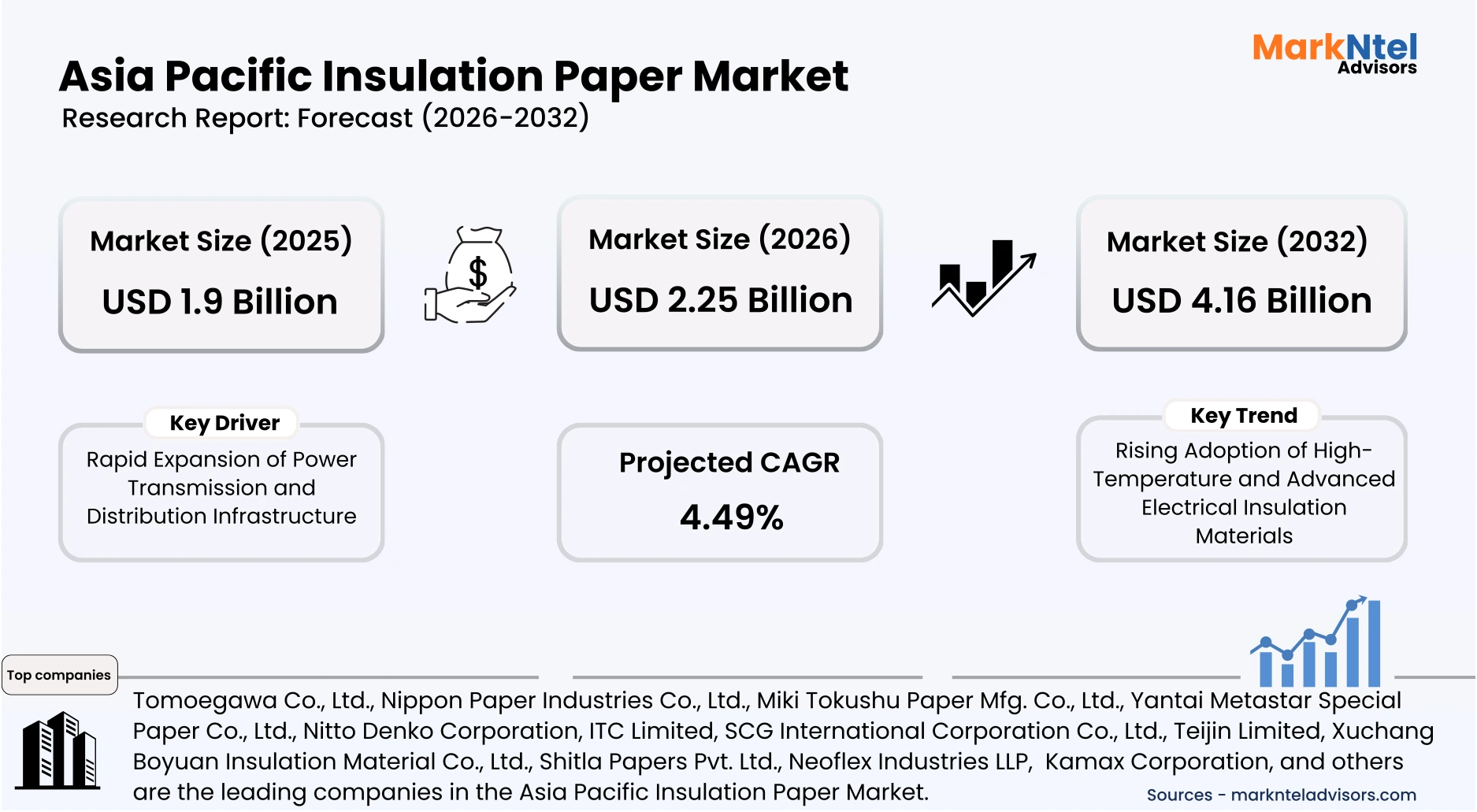

- The Asia Pacific Insulation Paper Market size was valued at USD 1.9 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to USD 4.16 billion by 2032, exhibiting a CAGR of 4.49% during the forecast period.

- China is the leading country with a significant share of 42% in 2026.

- By Material Type, the cellulose fiber represented a significant share of about 63% in the Asia Pacific Insulation Paper Market in 2026.

- By Form Type, the roll Insulation paper segment seized a significant share of about 54% in the Asia Pacific Insulation Paper Market in 2026.

- Leading companies are Tomoegawa Co., Ltd., Nippon Paper Industries Co., Ltd., Miki Tokushu Paper Mfg. Co., Ltd., Yantai Metastar Special Paper Co., Ltd., Nitto Denko Corporation, ITC Limited, SCG International Corporation Co., Ltd., Teijin Limited, Xuchang Boyuan Insulation Material Co., Ltd., Shitla Papers Pvt. Ltd., Neoflex Industries LLP, Hokuetsu Corporation, Siam Nippon Industrial Paper Co., Ltd., Asia Honour Paper Co., Ltd., Kamax Corporation, and others.

Market Insights & Analysis: Asia Pacific Insulation Paper Market (2026-32):

The Asia Pacific Insulation Paper Market size was valued at USD 1.9 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to USD 4.16 billion by 2032, exhibiting a CAGR of 4.49% during the forecast period. i.e., 2026-32.

The Asia-Pacific insulation paper market has expanded steadily as electricity demand and industrial electrification accelerate across major regional economies. According to the International Energy Agency, electricity consumption in the Asia-Pacific is projected to grow by over 4% annually through the mid-2020s, ne cessitating continuous investment in transmission and distribution equipment. Insulation paper remains a core dielectric component in transformers, motors, and cables, supporting reliability across expanding electrical networks. Strong industrial activity in power equipment manufacturing hubs across China, India, and Japan has therefore sustained demand for specialized cellulose and synthetic insulation materials.

Government-driven grid modernization programs have further reinforced market expansion by encouraging the installation of advanced transmission equipment requiring high-performance insulation materials. The Government of India introduced the Revamped Distribution Sector Scheme (RDSS) with a total outlay of about USD 36–37 billion to modernize electricity distribution networks, reduce technical losses, and strengthen power infrastructure across states. Upgrades to substations, feeder lines, and transformer fleets under such national programs increase the need for electrical insulation components. As utilities replace ageing equipment and deploy higher-capacity networks, the procurement of insulation paper products rises proportionally.

Industrial end-user sectors also contribute significantly to demand growth as electrification spreads across manufacturing and energy generation facilities. According to the International Renewable Energy Agency, Asia accounted for around 72% of global renewable power capacity additions in 2024, reflecting the region’s dominant role in renewable energy deployment and electricity infrastructure expansion. Wind turbines, solar inverters, and grid-connected converters require insulated generators and electrical components where insulation paper or composite insulating materials are commonly used. Rising renewable installations, therefore, stimulate demand from power electronics manufacturers and generator producers across emerging energy markets.

Corporate investments and technology development are also shaping market outlook through innovation in high-temperature and environmentally sustainable insulation materials. For example, Nitto Denko Corporation has expanded development of advanced electrical insulation materials designed to improve thermal resistance and operational durability in modern electrical equipment.

Asia Pacific Insulation Paper Market Scope:

| Category | Segments |

|---|---|

| By Type | (Cream Pressboard, Cable Insulation Paper, Transformer Insulation Paper, Aramid Fibre Paper, Others), |

| By Application | (Power Cable Insulation, Conductor Insulation, Barrier Insulation, Transformer Winding Insulation, Motor and Generator Insulation, Switchgear Insulation, Others), |

| By End-User Industry | (Power Utilities, Electrical and Electronics, Automotive, Industrial Machinery, Renewable Energy, Others), |

| By Form | (Roll Insulation Paper, Sheet Insulation Paper, Coil and Spool Paper, Laminated Paper Form), |

| By Grade | (Low Voltage Grade, Medium Voltage Grade, High Voltage Grade, Extra High Voltage Grade), |

| By Material | (Cellulose Fiber, Aramid Fiber, Polyester Fiber, Composite Fiber, Others), |

Asia Pacific Insulation Paper Market Driver:

Rapid Expansion of Power Transmission and Distribution Infrastructure

The most influential structural driver of the Asia-Pacific insulation paper market is the rapid expansion and modernization of electricity transmission and distribution infrastructure. Governments across the region are accelerating power network upgrades to accommodate rising electricity demand and improve grid reliability. According to the International Energy Agency, electricity demand in emerging Asian economies increased significantly in recent years and continues to grow due to industrialization and electrification. China and India alone account for around 60% of global electricity demand growth, highlighting the scale of power system expansion. Expanding transmission networks requires new transformers , switchgear, and high-voltage cables that incorporate insulation materials such as cellulose and composite insulation paper.

Infrastructure investment programs introduced in the mid-2020s have intensified this trend by prioritizing power system modernization and resilience. For example, the Asian Development Bank approved billions of dollars in financing for electricity grid expansion and modernization projects across Southeast Asia between 2024 and 2026. These investments focus on upgrading substations, expanding transmission corridors, and strengthening distribution networks to support urbanization and industrial growth. Each installed transformer or cable system contains multiple insulation layers used for winding, barrier, and conductor insulation, thereby creating a consistent demand for insulation paper materials.

Large-scale infrastructure programs are also being implemented by national governments to strengthen electricity access and reliability across densely populated regions. According to the World Bank, infrastructure investment in power transmission and distribution networks across developing Asia continues to rise as governments pursue electrification and energy security objectives. Grid reinforcement projects involve the installation of thousands of kilometers of transmission lines and new substations, significantly expanding the installed base of electrical equipment. Because insulation paper is a fundamental dielectric component used in high-voltage equipment, these structural investments directly increase material consumption and support sustained growth in the Asia-Pacific insulation paper market.

Asia Pacific Insulation Paper Market Trend:

Rising Adoption of High-Temperature and Advanced Electrical Insulation Materials

A key structural trend shaping the Asia-Pacific insulation paper market is the increasing adoption of high-temperature and advanced insulation materials designed for modern electrical equipment. Electrical systems operating in renewable energy installations, electric mobility infrastructure, and high-capacity transformers require insulation capable of withstanding elevated thermal and electrical stress, accelerating the adoption of aramid-based insulation materials. According to the International Energy Agency, the rapid electrification of energy systems and expansion of power electronics across Asia is increasing demand for durable and efficient electrical components. These operational conditions are accelerating the shift from conventional insulation solutions toward advanced insulation paper materials with improved thermal endurance.

This trend has triggered structural adjustments across the insulation material value chain, particularly in product development and manufacturing technologies. Companies are investing in specialty insulation materials, including aramid-based and composite insulation papers that offer enhanced dielectric strength and higher temperature tolerance. For example, Teijin Limited manufactures aramid fiber materials used in high-performance electrical insulation applications for motors and transformers. Such innovations allow equipment manufacturers to design compact, high-efficiency electrical systems while maintaining insulation reliability in demanding operating environments.

The transition toward advanced insulation materials is expected to persist as governments and utilities upgrade electricity infrastructure and integrate renewable energy sources. According to the International Renewable Energy Agency, global renewable power capacity continued expanding rapidly through 2025, requiring resilient electrical equipment capable of operating under variable power conditions. This evolution is increasing reliance on high-performance insulation materials within transformers, generators, and power converters. Consequently, the shift toward advanced insulation paper technologies is becoming a long-term structural trend influencing product innovation and demand patterns across the Asia-Pacific market.

Asia Pacific Insulation Paper Market Opportunity:

Localization of Electrical Insulation Material Manufacturing

A major opportunity for new entrants in the Asia-Pacific insulation paper market lies in the localization of electrical component supply chains across emerging economies. Governments are encouraging domestic manufacturing to reduce reliance on imported electrical equipment and materials. For example, the Government of India has expanded its production-linked incentive programs and manufacturing initiatives to strengthen domestic industrial supply chains. Such policies stimulate local production of electrical components, including transformers and cables, which rely heavily on insulation materials.

The opportunity has emerged as electricity infrastructure investment accelerates across developing Asian markets. For example, in 2025, Hitachi Energy announced an investment of about USD 36 million to expand its manufacturing facility in Mysuru, India. The expansion focuses on producing extra-high-voltage transformer insulation materials such as pressboard and laminated insulation components used in power transformers. The project aims to increase domestic production capacity and strengthen local supply chains for electrical infrastructure equipment. As infrastructure deployment expands geographically, demand for locally available insulation materials increases across new manufacturing clusters.

This environment particularly benefits smaller and emerging players because localised production can reduce transportation costs, lead times, and dependency on foreign suppliers. Governments are also promoting regional industrial ecosystems that enable domestic companies to participate in electrical component supply chains. DuPont has expanded production and applications of its Nomex® aramid insulation paper, which is widely used in transformers, motors, and electrical equipment. The company has collaborated with transformer manufacturers such as Yunnan Transformer Company in China to develop hybrid insulation systems using Nomex paper and pressboard for high-reliability power equipment.

Asia Pacific Insulation Paper Market Challenge:

Stringent Electrical Safety Norms and Material Certification Requirements

A major structural barrier in the Asia Pacific insulation paper market is the increasingly stringent electrical safety norms and performance certification requirements applied to materials used in transformers, cables, and high-voltage equipment. Insulation papers must meet strict thermal endurance, dielectric strength, and fire resistance standards before commercial deployment. According to the International Electrotechnical Commission, electrical insulation materials used in power equipment must comply with internationally recognized standards such as IEC thermal classification and insulation coordination guidelines. Compliance testing and certification processes significantly increase product development timelines and technical validation costs for manufacturers.

This regulatory burden has intensified as governments across the Asia Pacific strengthen power equipment safety frameworks to improve grid reliability. For example, national electrical standards in countries such as India increasingly align with international IEC performance standards for transformer and cable insulation systems. Electrical utilities and equipment manufacturers require certified insulation materials that meet long-term thermal ageing and dielectric reliability tests. Meeting these technical requirements requires advanced testing laboratories, specialized material engineering capabilities, and extended product validation cycles before insulation papers can be approved for commercial use.

These compliance requirements create significant operational barriers for smaller manufacturers and new market entrants. According to the International Energy Agency, modernization of electricity networks and increasing voltage levels require higher-performance insulation materials with strict reliability benchmarks. Companies unable to invest in specialized testing infrastructure or certification processes face delays in product commercialization and limited access to utility procurement contracts. As a result, regulatory compliance complexity and certification costs remain a critical constraint affecting scalability and market entry in the Asia Pacific insulation paper industry.

Asia Pacific Insulation Paper Market (2026-32) Segmentation Analysis:

The Asia Pacific Insulation Paper Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as:

Based on Material:

- Cellulose Fiber

- Aramid Fiber

- Polyester Fiber

- Composite Fiber

- Others

Cellulose fiber insulation paper holds the dominant share in the Asia-Pacific insulation paper market with a market share of 63% due to its cost-efficiency, abundant raw material availability, and compatibility with high-volume electrical applications. Countries such as China and India benefit from strong domestic pulp and paper industries, ensuring stable supply chains and lower production costs compared to synthetic alternatives like aramid or polyester fibers . This structural advantage directly supports large-scale transformer and cable manufacturing ecosystems across the region.

Government-led electrification programs and grid modernization initiatives further reinforce cellulose fiber demand. Policies promoting rural electrification and renewable energy integration, particularly in India and Southeast Asia, drive the installation of transformers and switchgear, where cellulose-based insulation remains the industry standard due to its proven dielectric strength and thermal performance in oil-filled systems. For example, India Revamped Distribution Sector Scheme (RDSS) & Deen Dayal Upadhyaya Gram Jyoti Yojana (DDUGJY)

These programs focus on strengthening distribution infrastructure, reducing AT&C losses, and expanding rural electrification. They drive large-scale deployment of distribution transformers and substations, where cellulose-based insulation paper is widely used due to cost efficiency and reliability.

From an end-user perspective, utilities and power equipment manufacturers prioritize reliability and cost optimization, making cellulose fiber the preferred material. For instance, large transformer manufacturers in China continue to scale production using cellulose insulation to meet export and domestic grid expansion needs. This sustained industrial demand, combined with favorable policy support and investment in transmission infrastructure, ensures the continued dominance of cellulose fiber in the regional market.

Based on Form:

- Roll Insulation Paper

- Sheet Insulation Paper

- Coil and Spool Paper

- Laminated Paper Form

Roll insulation paper dominates the Asia-Pacific market with a market share of 54%, owing to its operational efficiency in automated manufacturing processes and suitability for continuous winding applications in transformers and cables. Its format enables seamless integration into high-speed production lines, reducing material wastage and labor costs, which is critical in cost-sensitive, high-output markets like China, Japan, and South Korea.

Industrial expansion and increasing investments in power equipment manufacturing hubs have accelerated the adoption of roll formats. Government-backed industrial policies, particularly in China’s electrical equipment sector, encourage scale manufacturing, where roll insulation paper offers clear advantages in productivity and consistency over sheet or laminated forms. For instance, China’s government (NDRC & NEA) is actively promoting smart grid expansion and renewable integration, with State Grid investing USD 11.1billion annually in transmission & distribution upgrades. This aligns with rising demand for standardized, high-performance insulation materials.

End-user industries such as power transmission and distribution heavily favor roll insulation paper due to its adaptability in coil winding and large transformer applications. For example, leading cable and transformer producers across the Asia-Pacific utilize roll formats to streamline production and maintain uniform insulation quality. The resulting efficiency gains and alignment with mass manufacturing requirements solidify the segment’s leadership and long-term growth trajectory.

Asia Pacific Insulation Paper Market (2026-32) Regional Analysis:

China represents the largest and most dominant market for insulation paper in the Asia Pacific region, with a market share of 42% due to its extensive electricity infrastructure, large-scale manufacturing ecosystem, and significant investment in power grid expansion. China’s electricity consumption rose by about 7% in 2024 and is projected to grow around 6% annually through 2027. T his continuous increase in electricity consumption has driven large-scale deployment of transformers, cables, and electrical equipment that rely on specialized insulation materials such as transformer and cable insulation paper.

Government-led infrastructure programs further strengthen China’s leadership in this market. The Chinese government has prioritized modernization of national power networks and ultra-high-voltage (UHV) transmission corridors to improve long-distance electricity transport and grid stability. According to the National Energy Administration of China, China continues to expand its UHV transmission network to integrate power from renewable energy bases and remote generation sites into major consumption centers. These projects require high-performance insulation systems for transformers, switchgear, and transmission equipment, thereby increasing demand for electrical insulation paper.

China’s dominance is also supported by its strong domestic manufacturing base for electrical equipment and power components. Several Chinese insulation paper suppliers are featured in industry lists of top domestic producers. These include companies like Sichuan Ruisong Paper Co., Ltd. and Huisheng Group Co., Ltd., which are described as leading enterprises with large-scale production and advanced equipment. The presence of these companies, combined with extensive industrial supply chains for pulp processing and specialty paper manufacturing, enables large-scale production and consumption of insulation paper materials within the Chinese electrical equipment sector.

Gain a Competitive Edge with Our Asia Pacific Insulation Paper Market Report:

- The Asia Pacific Insulation Paper Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competition, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Asia Pacific Insulation Paper Market Landscape Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Asia Pacific Insulation Paper Market Policies, Regulations, and Product Standards

- Asia Pacific Insulation Paper Market Trends & Developments

- Asia Pacific Insulation Paper Market Dynamics

- Growth Factors

- Challenges

- Asia Pacific Insulation Paper Market Hotspot & Opportunities

- Asia Pacific Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Cream Pressboard

- Cable Insulation Paper

- Transformer Insulation Paper

- Aramid Fibre Paper

- Others

- By Application- Market Size & Forecast 2022-2032, USD Million

- Power Cable Insulation

- Conductor Insulation

- Barrier Insulation

- Transformer Winding Insulation

- Motor and Generator Insulation

- Switchgear Insulation

- Others

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- Power Utilities

- Electrical and Electronics

- Automotive

- Industrial Machinery

- Renewable Energy

- Others

- By Form- Market Size & Forecast 2022-2032, USD Million

- Roll Insulation Paper

- Sheet Insulation Paper

- Coil and Spool Paper

- Laminated Paper Form

- By Grade- Market Size & Forecast 2022-2032, USD Million

- Low Voltage Grade

- Medium Voltage Grade

- High Voltage Grade

- Extra High Voltage Grade

- By Material- Market Size & Forecast 2022-2032, USD Million

- Cellulose Fiber

- Aramid Fiber

- Polyester Fiber

- Composite Fiber

- Others

- By Country

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Indonesia

- Malaysia

- Thailand

- Rest of Asia Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- China Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Korea Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Australia Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- New Zealand Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Malaysia Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Thailand Insulation Paper Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-User Industry- Market Size & Forecast 2022-2032, USD Million

- By Form- Market Size & Forecast 2022-2032, USD Million

- By Grade- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Asia Pacific Insulation Paper Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Tomoegawa Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nippon Paper Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Miki Tokushu Paper Mfg.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yantai Metastar Special Paper

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Nitto Denko Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ITC Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SCG International

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Teijin Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Xuchang Boyuan Insulation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shitla Papers Pvt. Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Neoflex Industries LLP

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hokuetsu Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Siam Nippon Industrial Paper

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Asia Honour Paper

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kamax Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tomoegawa Co., Ltd.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now