Latin America Drywall Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Product Type (Standard Drywall, Moisture-Resistant Drywall, Fire-Resistant Drywall, Others), By Application (Walls/Partitions, Ceilings), By End-Use (Residential, Commercial, In ... stitutional), and others Read more

- Buildings, Construction, Metals & Mining

- Mar 2026

- Pages 200

- Report Format: PDF, Excel, PPT

Latin America Drywall Market

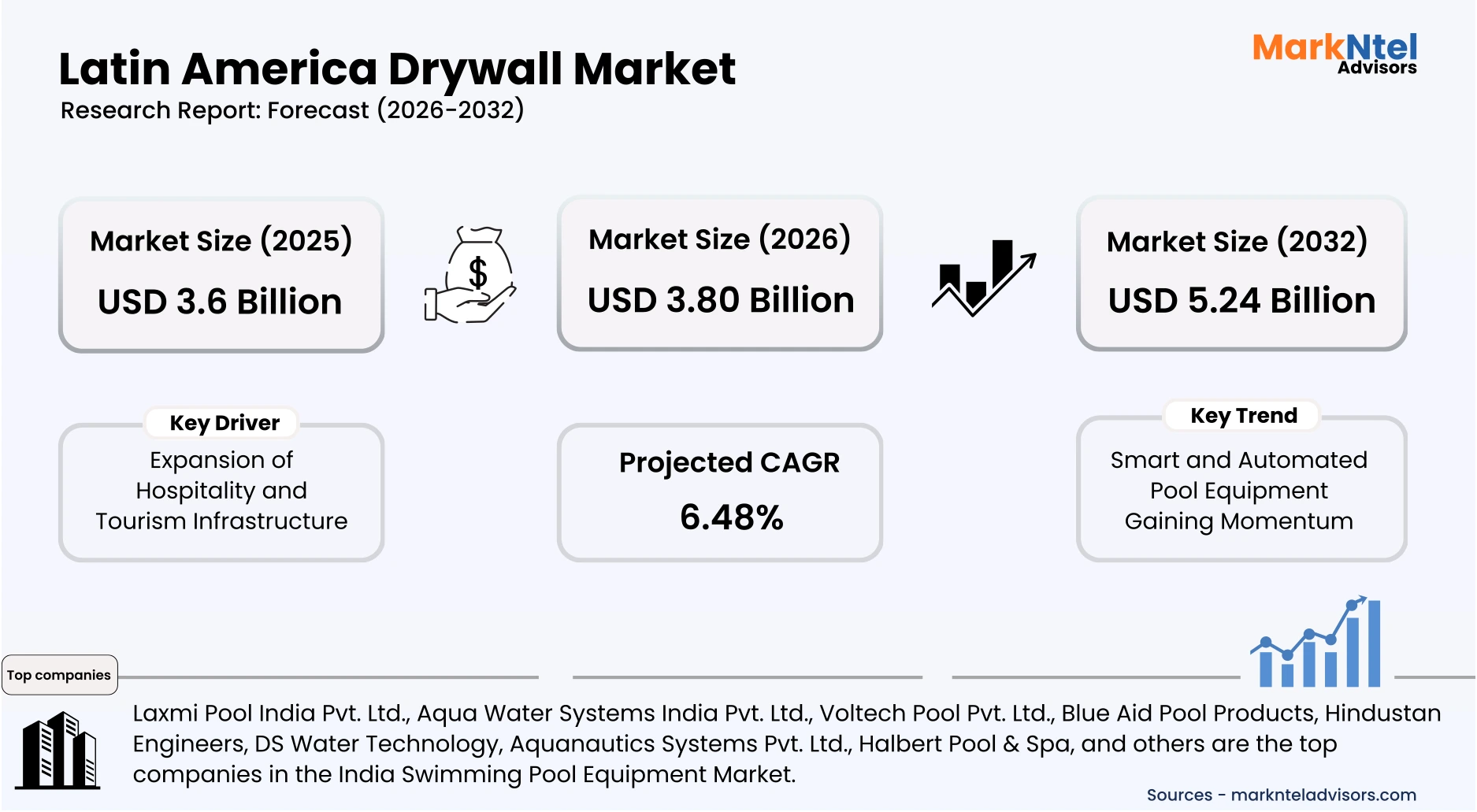

Projected 5.5% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 5.24 Billion

Market Size (2032)

USD 3.80 Billion

Base Year

2025

Projected CAGR

5.5%

Leading Segments

By Product Type: Standard Drywall

Latin America Drywall Market Report Key Takeaways:

- Latin America Drywall Market size was valued at around USD 3.6 billion in 2025 and is projected grow from USD 3.80 billion in 2026 to USD 5.24 billion by 2032, exhibiting a CAGR of 5.5% during 2026-32.

- Brazil holds the largest market share of about 37.53% in the Latin America Drywall Market in 2026.

- By Product Type, the Standard Drywall segment represented a significant share of about 67% in the Latin America Drywall Market in 2026.

- By End Use, the Residential segment seized a significant share of about 56% in the Latin America Drywall Market in 2026.

- Leading Drywall companies in Latin America are Compagnie de Saint-Gobain, Knauf, USG Corporation, Etex Group, National Gypsum Company, Georgia-Pacific LLC, Yoshino Gypsum Co., Ltd., Panel Rey, Volcan S.A., Superboard, and Others.

Market Insights & Analysis: Latin America Drywall Market (2026-32):

The Latin America Drywall Market size was valued at around USD 3.6 billion in 2025 and is projected grow from USD 3.80 billion in 2026 to USD 5.24 billion by 2032, exhibiting a CAGR of 5.5% during the forecast period, i.e., 2026-32.

The Latin America drywall market has demonstrated steady historical expansion, supported by rising residential construction activity and the increasing shift toward efficient building materials across Brazil, Mexico, and Colombia. Recent construction indicators in Brazil highlight sustained momentum, with residential building permits rising from 145,000 units in August 2024 to 175,000 units in September 2024, alongside a 2% year-on-year increase in construction value-added in 2025. In addition, more than 1 million housing units remain under construction nationwide, reflecting strong pipeline visibility. This sustained activity has encouraged developers to adopt drywall systems due to faster installation, reduced labor intensity, and cost efficiency compared to conventional construction methods.

Building on this momentum, current market conditions are being reinforced by strong government-backed housing investments, particularly in Brazil, which remains the region’s largest construction market. In 2026, the government announced approximately USD 39.8 billion in combined housing investments under programs including “Minha Casa, Minha Vida” and the newly launched “Reforma Casa Brasil,” targeting both new construction and urban housing upgrades. According to the Ministry of Cities, this funding includes USD 30.5 billion from FGTS, supported by federal budget allocations and contributions from the Social Fund and Caixa Econômica Federal . These coordinated initiatives are accelerating both new construction and renovation activity, thereby directly increasing drywall demand for interior partitions, ceilings, and refurbishment applications.

At the same time, regulatory frameworks and sustainability initiatives are further strengthening drywall adoption across Latin America by promoting energy-efficient and low-waste construction practices. National policies, including Brazil’s energy efficiency programs, are encouraging improved thermal insulation in buildings, which aligns with the performance advantages of drywall systems. In response, industry participants are expanding localized manufacturing and introducing advanced gypsum boards with fire-resistant and moisture-resistant properties suited to regional climatic conditions. Moreover, increasing investments in healthcare, education, and public infrastructure are supporting institutional construction, further reinforcing demand for modular and lightweight interior solutions.

Looking ahead, the market outlook remains positive, supported by sustained infrastructure development, policy-driven housing demand, and evolving construction methodologies across the region. The Inter-American Development Bank has emphasized continued investment in urban infrastructure and social housing as a key driver of construction activity through the end of the decade. Growing activity in industrial and logistics real estate, along with a gradual recovery in commercial spaces, is expected to further boost drywall consumption. As governments and developers continue to prioritize speed, cost efficiency, and sustainability, drywall systems are well-positioned to achieve broader adoption across residential, commercial, and institutional end-user segments.

Latin America Drywall Market Recent Developments:

- 2025 : Compagnie de Saint-Gobain introduced its first 100% recycled gypsum plasterboard in 2025, supporting circular construction and reducing environmental impact across its global portfolio, including Latin America.

- 2025 : Saint-Gobain completed the acquisition of Cemix (Latin America) in 2025, strengthening its construction materials portfolio and distribution network across the region, indirectly supporting drywall system growth.

Latin America Drywall Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Standard Drywall, Moisture-Resistant Drywall, Fire-Resistant Drywall, Others), |

| By Application | (Walls/Partitions, Ceilings), |

| By End-Use | (Residential, Commercial, Institutional), |

Latin America Drywall Market Driver:

Rising Urbanization and Housing Demand

Urbanization has intensified across Latin America, creating a structural surge in housing requirements and construction activity. According to the United Nations Department of Economic and Social Affairs, over 81% of the region’s population resides in urban areas, compared to approximately 75% in 2000 . This sustained rural-to-urban migration has significantly increased pressure on housing infrastructure. As cities expand, governments are compelled to accelerate residential development at scale.

This demographic shift is directly translating into measurable construction activity across key economies such as Brazil and Mexico. In 2025, Brazil expanded its ‘Minha Casa, Minha Vida’ housing program, with the government targeting approximately 3 million housing units by 2026, significantly increasing investment and construction activity . Similarly, public housing initiatives and urban development policies across the region are driving new residential project pipelines. These developments are significantly increasing the volume of construction activity in urban centers.

The growing scale and urgency of housing development are materially expanding drywall consumption across new construction projects. Drywall systems enable faster installation and reduced labor dependency, making them highly suitable for large-scale housing programs. As developers prioritize speed, efficiency, and cost control, drywall adoption is increasing across residential construction. This positions urbanization as a long-term structural driver directly contributing to market volume growth.

Latin America Drywall Market Trend:

Growing Adoption of Lightweight Construction Materials

The adoption of lightweight construction materials has accelerated across Latin America as developers seek faster and more efficient building methods. This trend has emerged alongside rapid urban expansion and increasing pressure to reduce construction timelines. According to the International Energy Agency, buildings account for nearly 30% of global energy consumption, driving a shift toward materials that improve efficiency. Lightweight systems such as drywall reduce structural load and construction time, making them increasingly preferred.

This shift is reshaping construction practices and value chains across residential and commercial sectors. Governments are promoting industrialized construction to address housing shortages more efficiently, as seen in Brazil’s housing programs and urban development policies. Lightweight materials enable prefabrication and modular construction, reducing labor requirements and project delays. This transition is further evidenced by USG Corporation’s projects in Mexico, where residential and commercial structures are being built entirely using lightweight systems, enabling a 110-square-meter house to be completed in approximately 15 days. As a result, contractors and developers are increasingly integrating drywall systems into standardized building designs and procurement processes.

The trend is expected to persist due to its direct impact on cost efficiency, sustainability, and scalability of construction projects. Lightweight materials reduce material wastage, transportation costs, and overall carbon footprint, aligning with evolving environmental regulations. As urban construction volumes rise and developers prioritize faster project delivery, the adoption of drywall and similar systems will continue expanding. This establishes lightweight construction as a long-term structural trend influencing market evolution.

Latin America Drywall Market Opportunity:

Growth in Renovation and Remodeling Activities

Renovation and remodeling activities are emerging as a compelling opportunity in Latin America due to the region’s aging building stock and increasing urban densification. According to the Inter-American Development Bank, nearly 55 million households in Latin America live in housing with quality-related deficiencies, highlighting the need for upgrades rather than new construction. Governments are increasingly prioritizing urban regeneration and housing improvement programs. This structural shift is creating sustained demand for interior construction materials such as drywall systems.

This opportunity is translating into tangible demand as refurbishment projects require faster, less disruptive construction solutions. Drywall systems are widely adopted in renovation due to their ease of installation and minimal structural impact. This is further supported by Etex’s 2025 investment of approximately USD 70 million across Peru, Chile, and Argentina to expand plasterboard production capacity in response to growing regional demand. Such developments indicate rising consumption across residential and commercial retrofitting activities.

The renovation segment offers a favorable entry point for new and emerging players due to its fragmented and localized nature. Unlike large-scale construction projects dominated by established firms, renovation activities are smaller and contractor-driven. This allows new entrants to compete through flexible distribution, cost-effective offerings, and installation services. As urban refurbishment demand expands, smaller players can scale operations by targeting niche markets and specialized applications.

Latin America Drywall Market Challenge:

Competition from Substitute Materials

Competition from substitute materials remains a critical structural challenge for the drywall market in Latin America, driven by the continued dominance of traditional construction methods. Materials such as brick, concrete block, and plaster remain deeply embedded in regional building practices due to familiarity and perceived durability. According to the World Bank, a significant share of housing in the region continues to rely on conventional masonry techniques. This entrenched preference limits the transition toward drywall systems despite their efficiency advantages.

This challenge is further reinforced by cost dynamics and emerging alternative materials across the region. In many Latin American markets, locally sourced masonry materials are relatively inexpensive and widely available, reducing the incentive to adopt drywall systems. For instance, in 2025, Brazil witnessed the adoption of cellular concrete solutions such as Ecopore, offering up to 60% cost reduction and significantly faster application, highlighting growing competition from alternative materials. These developments intensify pressure on drywall adoption, particularly in cost-sensitive projects.

The presence of both traditional and emerging substitutes materially restricts drywall market expansion by slowing adoption rates and influencing investment decisions. Manufacturers must invest in awareness, contractor training, and distribution to shift established construction practices. This increases operational costs and extends market penetration timelines, especially for new entrants. Consequently, competition from substitute materials acts as a persistent barrier, limiting the scalability and broader adoption of drywall systems across the region.

Latin America Drywall Market (2026-32) Segmentation Analysis:

The Latin America Drywall Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Product Type:

- Standard Drywall

- Moisture-Resistant Drywall

- Fire-Resistant Drywall

- Others

The standard drywall segment dominates the Latin America drywall market, accounting for approximately 67% of total demand, primarily due to its cost efficiency and widespread applicability across high-volume residential construction. According to the United Nations Department of Economic and Social Affairs, over 81% of the region’s population resides in urban areas, driving large-scale housing demand. This results in significant consumption of basic wall partition systems, where standard drywall offers an economical and practical solution compared to specialized variants.

Construction cost sensitivity across Latin America further reinforces this dominance, particularly in mass housing and mid-income residential projects. Governments in countries such as Brazil and Mexico continue to promote affordable housing programs, prioritizing materials that balance performance with affordability. Standard drywall meets these requirements by offering adequate strength, ease of installation, and lower upfront costs compared to moisture- or fire-resistant boards. Its compatibility with conventional construction practices also supports widespread contractor adoption.

Additionally, manufacturing scalability and distribution networks favor standard drywall production across the region. Major manufacturers operate large-scale facilities focused on high-volume output of regular gypsum boards, ensuring a consistent supply and competitive pricing. This availability supports contractors and developers working on time-sensitive projects, where standardized materials reduce procurement complexity. As a result, the combination of cost advantage, high-volume demand, and supply chain efficiency continues to position standard drywall as the leading product segment in Latin America.

Based on End Use:

- Residential

- Commercial

- Institutional

The residential segment dominates the Latin America drywall market, accounting for approximately 56% of total demand, primarily due to the region’s strong reliance on housing-led construction activity. Across Latin America, residential construction consistently represents the largest share of total building output, driven by ongoing housing requirements and population expansion. This results in high-volume demand for interior partitioning and ceiling systems, where drywall is widely used.

Government-led housing initiatives further reinforce this dominance by accelerating large-scale residential development. Programs such as Brazil’s “Minha Casa, Minha Vida” focus on mass housing delivery, requiring cost-efficient and fast-installation materials. This is further supported by international cooperation initiatives, such as the 2025 housing agreement between Brazil and Cuba aimed at strengthening affordable residential construction capacity. Drywall systems are increasingly preferred in these projects due to their ability to reduce construction time and optimize labor usage.

Additionally, residential construction is highly fragmented and continuous, ensuring steady material consumption across both urban and semi-urban areas. Unlike commercial projects, which are cyclical and capital-intensive, residential developments occur at a higher frequency and volume. The widespread use of drywall in apartments, multi-family housing, and renovation projects further strengthens demand, positioning the residential segment as the leading end-use category.

Latin America Drywall Market (2026-32): Regional Projection

Brazil dominates the Latin America drywall market, accounting for approximately 37.53% of total regional demand, primarily due to its extensive building construction activity and large-scale residential development. The country consistently records the highest volume of housing and commercial projects in the region, driving significant demand for interior construction materials such as drywall systems. This high frequency of building activity directly translates into greater material consumption compared to other Latin American countries.

This dominance is further reinforced by strong residential construction momentum and sustained housing demand across urban areas. Additionally, data from the Instituto Brasileiro de Geografia e Estatística indicates that Brazil’s construction sector recorded growth of approximately 4.3% in 2024, reflecting increasing building activity . This is further supported by 2025 data showing a 49% increase in housing project launches and a 13% rise in sales, highlighting robust demand and high project volumes in the residential sector . These factors collectively result in significant drywall consumption across building projects.

Brazil also benefits from a well-established manufacturing and supply chain ecosystem for construction materials. Major drywall manufacturers operate local production facilities, supported by strong distribution networks and raw material availability. This ensures a consistent supply and competitive pricing for large-scale building projects. As a result, the combination of strong building construction activity, high residential demand, and industrial capacity positions Brazil as the leading country in the Latin America drywall market.

Gain a Competitive Edge with Our Latin America Drywall Market Report:

- Latin America Drywall Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Latin America Drywall Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Latin America Drywall Market Policies, Regulations, and Product Standards

- Latin America Drywall Market Trends & Developments

- Latin America Drywall Market Dynamics

- Growth Factors

- Challenges

- Latin America Drywall Market Hotspot & Opportunities

- Latin America Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Standard Drywall

- Moisture-Resistant Drywall

- Fire-Resistant Drywall

- Others

- By Application- Market Size & Forecast 2022-2032, USD Million

- Walls/Partitions

- Ceilings

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Residential

- Commercial

- Institutional

- By Country

- Mexico

- Brazil

- Argentina

- Chile

- Peru

- Columbia

- Rest of Latin America

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Brazil Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Argentina Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Chile Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Peru Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Columbia Drywall Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End-Use- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Latin America Drywall Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Compagnie de Saint-Gobain

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Knauf

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- USG Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Etex Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- National Gypsum Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Georgia-Pacific LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yoshino Gypsum Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Panel Rey

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Volcan S.A.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Superboard

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Compagnie de Saint-Gobain

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now