Angola Generator Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Power Rating (Upto 5 KVA, 6 KVA to 20 KVA, 21 KVA to 75 KVA, 76 KVA to 375 KVA, 376 KVA to 750 KVA, 751 KVA to 2000 KVA, Above 2000 KVA), By Application (Standby, Prime & Contin ... uous, Peak Shaving), By End User (Residential, Commercial Offices, Hospitality, Retail, Data Centers, Telecom, Oil & Gas, Government & Transport, Equipment Rental Companies, Mining, Defense), By Fuel Type (Diesel, Ethanol, Methane, Natural Gas, Gasoline, Hybrid (DG + Natural Gas), Others) Read more

- Energy

- Feb 2026

- Pages 180

- Report Format: PDF, Excel, PPT

Angola Generator Market

Projected 3.34% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 78 Million

Market Size (2032)

USD 95 Million

Base Year

2025

Projected CAGR

3.34%

Leading Segments

By Application: Standby

Angola Generator Market Report Key Takeaways:

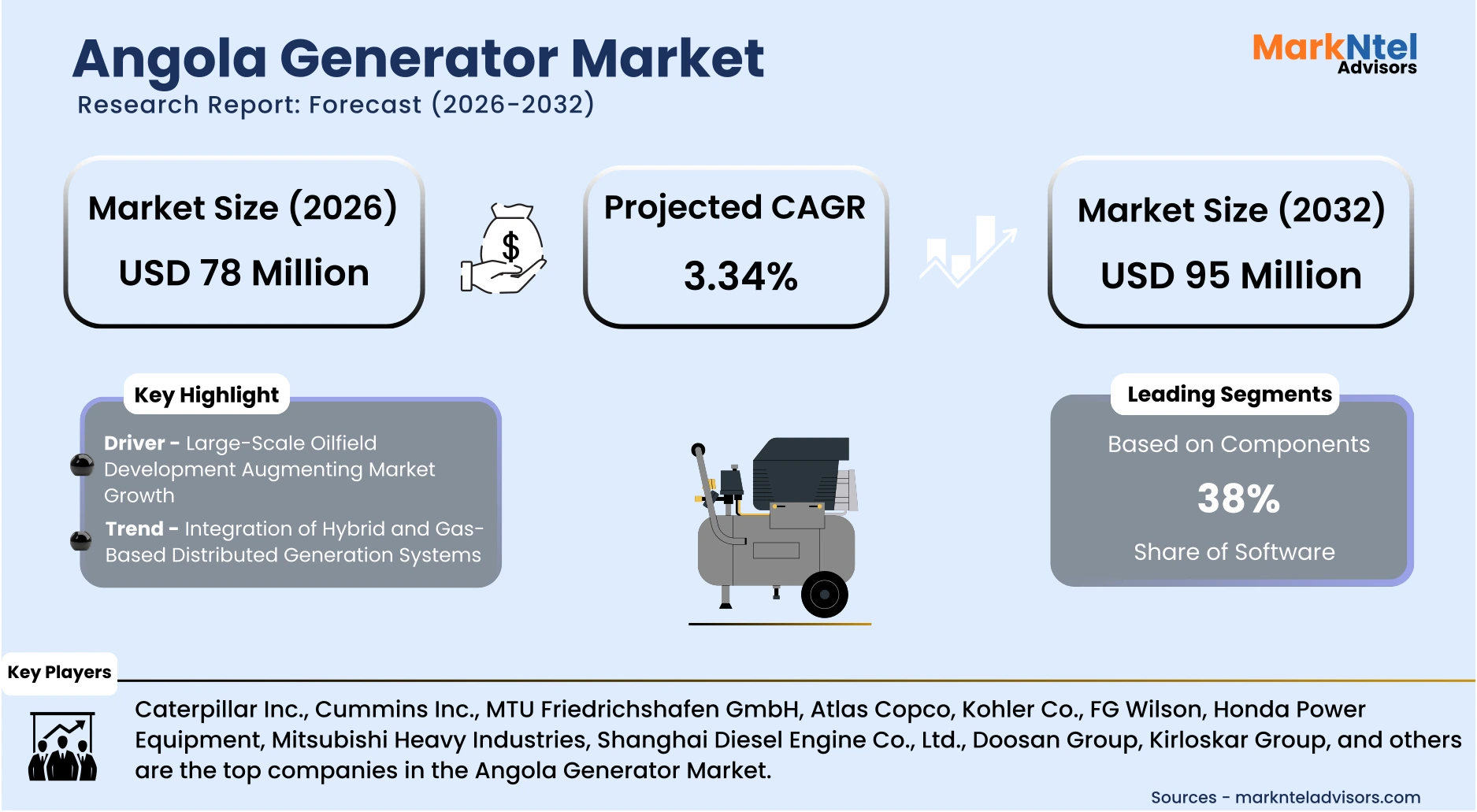

- The Angola Generator market size was valued at around USD 70 million in 2025 and is projected to grow from USD 78 million in 2026 to USD 95 million by 2032, exhibiting a CAGR of 3.34% during the forecast period.

- By Application Type, the Standby generators segment represented a significant share of about 80% in the Angola Generator Market in 2026.

- By Fuel type, the diesel segment presented a significant share of about 85% in the Angola Generator Market in 2026.

- Leading generator companies in Angola are Caterpillar Inc., Cummins Inc., MTU Friedrichshafen GmbH, Atlas Copco, Kohler Co., FG Wilson, Honda Power Equipment, Mitsubishi Heavy Industries, Shanghai Diesel Engine Co., Ltd., Doosan Group, Kirloskar Group, and others.

Market Insights & Analysis: Angola Generator Market (2026-32):

The Angola Generator market size was valued at USD 70 million in 2025 and is projected to grow from USD 78 million in 2026 to USD 95 million by 2032, exhibiting a CAGR of 3.34% during the forecast period, i.e., 2026-32.

Angola’s generator market has expanded alongside structural reforms in the national power system under the Government’s 2025–2026 energy modernization agenda. According to the Ministry of Energy and Water’s 2025 sector update, national installed capacity surpassed 9.9 GW, reflecting sustained investment in hydro and thermal assets. Despite capacity additions , transmission bottlenecks and regional load imbalances continue to create localized supply constraints, indirectly supporting distributed generation demand. This environment has historically positioned generators as complementary infrastructure supporting commercial continuity and industrial reliability.

Industrial and extractive sectors have materially influenced equipment demand growth over the past five years. Angola’s 2025 National Development Plan highlights continued investment in downstream oil logistics, construction materials, and agro-processing zones, which require dedicated on-site power resilience during operational ramp-up phases. Manufacturing clusters in Luanda and Benguela Provinces report expanded facility commissioning, creating an incremental need for mid-capacity backup systems. These industry-led expansions translate into measurable procurement activity for standby and prime-rated generators across commercial estates and production facilities.

Demographic and urban expansion trends further reinforce underlying market momentum. Government statements and energy statistics confirm that Angola aims to increase electricity access to around 50% of the population by 2027, with significant ongoing challenges in rural access. This highlights the structural demand environment where supplemental or backup power, e.g., generators, remain relevant for reliability. Rapid housing development and the expansion of private health and education institutions have increased the installation of small- to medium-capacity units for contingency power. Institutional users prioritize operational continuity due to rising service digitization and electronic transaction adoption, strengthening long-term generator deployment patterns.

Forward-looking prospects remain supported by regulatory and investment initiatives introduced in 2026 to strengthen grid stability and private participation. Angola’s revised Electricity Law framework encourages public–private partnerships in generation and distribution, attracting diversified capital inflows. Simultaneously, international financing commitments from multilateral institutions in 2025 target substation rehabilitation and rural electrification, which indirectly stimulate demand for interim power solutions. As infrastructure expansion progresses, generators are expected to remain integral to business continuity strategies and phased industrial development through the medium term.

Angola Generator Market Recent Developments:

- 2025: Angola’s new Cabinda oil refinery started output of refined diesel and other fuels by year's‑end, reducing import dependence and supporting local fuel availability.

This development is expected to lower diesel fuel costs and improve generator operating economics for both industrial and standby power customers .

- 2025: Desco Angola sustained its role as a major supplier, marketing, and maintaining thousands of high‑performance generator sets (including FG Wilson) across commercial and industrial customers. It also supports remote monitoring and service programs, boosting reliability and after‑sales support for generator fleets in Angola’s demanding energy market.

Angola Generator Market Scope:

| Category | Segments |

|---|---|

| By Power Rating | (Upto 5 KVA, 6 KVA to 20 KVA, 21 KVA to 75 KVA, 76 KVA to 375 KVA, 376 KVA to 750 KVA, 751 KVA to 2000 KVA, Above 2000 KVA), |

| By Application | (Standby, Prime & Continuous, Peak Shaving), |

| By End User | (Residential, Commercial Offices, Hospitality, Retail, Data Centers, Telecom, Oil & Gas, Government & Transport, Equipment Rental Companies, Mining, Defense), |

| By Fuel Type | (Diesel, Ethanol, Methane, Natural Gas, Gasoline, Hybrid (DG + Natural Gas), Others) |

Angola Generator Market Driver:

Large-Scale Oilfield Development Augmenting Market Growth

The most influential structural driver of Angola’s generator market is the renewed expansion of oil and gas production capacity under national upstream revitalization programs. Angola’s National Oil, Gas & Biofuels Agency (ANPG) has continued its multi-year licensing strategy, positioning the country to award up to 60 oil and gas concessions by the end of 2025 and attract significant upstream capital expenditure between 2025 and 2030. These efforts are designed to sustain and diversify Angola’s hydrocarbon resource development, which clearly underpins industrial power demand. New offshore tie-backs and brownfield upgrades require temporary and backup power solutions during drilling, processing, and support operations. This industrial intensification directly increases demand for medium- and high-capacity diesel generators across production and logistics zones.

The driver has strengthened over recent years due to regulatory reforms introduced under Angola’s hydrocarbons strategy to attract foreign direct investment . Government approvals for new marginal field developments and extended production-sharing contracts in 2025 stimulated renewed capital expenditure from international operators. These projects involve construction camps, offshore supply bases, and equipment yards that require dedicated prime and standby power installations. Unlike speculative growth, this investment translates into measurable procurement volumes for generator suppliers serving oilfield contractors and service providers.

This driver materially expands market volume because oil and gas operations require multi-unit deployments across drilling rigs, processing sites, accommodation blocks, and port facilities. Each upstream or midstream project necessitates scalable power systems during both construction and steady-state production phases. Angola is advancing major offshore exploration agreements with global majors such as Shell, which agreed to acquire interests in undeveloped blocks as part of the government’s effort to maintain energy sector investment and sustain hydrocarbon output into the 2030s. Such developments raise corporate activity and project timelines that drive substantial equipment procurement cycles.

Angola Generator Market Trend:

Integration of Hybrid and Gas-Based Distributed Generation Systems

A significant structural trend reshaping Angola’s generator market is the gradual integration of hybrid and gas-based distributed generation systems alongside traditional diesel units. The inauguration of a USD 4 billion gas processing facility in Soyo signals Angola’s shift toward monetizing natural gas and supplying it for domestic power generation, industrial users, and LNG export. This facility strengthens the supply base for technologies that use gas to support electricity generation, reducing sole reliance on diesel. As domestic gas utilization policies advance to support economic diversification, industrial operators are increasingly evaluating gas-compatible generator systems. This shift has accelerated due to regulatory efforts to reduce flaring and optimize associated gas use in upstream operations.

The trend is structurally altering procurement and system design practices across industrial and commercial value chains. Oilfield service providers and large facilities are adopting dual-fuel or hybrid generator configurations to improve fuel flexibility and operational efficiency. International energy institutions have highlighted Angola’s focus on gas-to-power initiatives in 2025 as part of broader energy transition strategies . This policy direction is encouraging equipment suppliers to introduce adaptable generator platforms capable of operating on both diesel and natural gas.

The persistence of this trend is reinforced by Angola’s long-term gas development roadmap and export-linked infrastructure investments extending beyond 2026. The gradual but steady incorporation of hybrid and gas-compatible systems, therefore, represents a durable transformation in technology adoption patterns. Over time, this shift influences the supplier portfolios, maintenance ecosystems, and capital allocation decisions across the market.

Angola Generator Market Opportunity:

Decentralized Electrification and Mini-Grid Deployment in Underserved Provinces

Angola’s electrification gap presents a structural opportunity for decentralized power solutions, particularly mini-grids and modular generator systems. As per the reports, Angola’s national electrification rate remains well below universal access levels, with rural access substantially lower than urban coverage.

The government’s rural electrification programs under the Ministry of Energy and Water prioritize distributed generation to accelerate connections beyond major urban centers.

This shift reflects grid expansion constraints and growing public investment in off-grid and hybrid systems to meet rising provincial demand.

The opportunity exists now due to sustained public capital expenditure and regulatory openness to private participation in power generation. Angola’s 2025–2026 energy strategy emphasizes decentralized infrastructure and provincial electrification, supported by multilateral financing commitments exceeding several hundred million USD for transmission and local distribution upgrades. These initiatives directly generate demand for modular diesel-gas hybrid generators, containerized systems, and EPC services tailored to remote communities. As grid rollout timelines remain extended, decentralized systems provide immediate and scalable electrification solutions.

Angola has secured significant finance for renewable mini‑grid deployment, solar PV, and storage that operates independently from the main grid, with external financing approximating USD 1.4 billion to install 48 mini‑grids and expand national network capacity. This reflects demand for decentralized generation models and creates fertile conditions for smaller participants offering hybrid power systems.

Unlike established incumbents focused on large utility-scale assets, emerging players can target underserved municipalities with lower capital intensity deployments. Consequently, decentralized electrification represents a scalable and structurally supported pathway for competitive market entry.

Angola Generator Market Challenge:

Persistent Infrastructure Gaps and Grid Reliability Limitations

A critical structural challenge for Angola’s generator market is the ongoing inadequacy and unreliability of the national electricity infrastructure. While the government has invested in expanding generation capacity, transmission networks remain constrained, particularly outside Luanda, limiting stable grid supply. According to Angola’s Ministry of Energy and Water, frequent load-shedding events and distribution bottlenecks continue to occur, forcing commercial and industrial users to rely heavily on backup generators, increasing operational complexity and cost.

This infrastructural limitation materially impacts market participants by requiring higher-capacity or redundant generator deployments, increasing capital expenditure and maintenance burdens. Industries such as oil & gas, mining, and large-scale manufacturing report operational delays due to inconsistent power supply, while rural electrification initiatives face extended timelines. The US Energy Information Administration (EIA) Country Analysis highlights that Angola’s grid faces capacity constraints and regional disparities in service quality, with frequent outages in secondary cities and rural areas supporting continued use of distributed generation, reflecting structural inefficiencies that constrain both market expansion and service reliability.

The persistence of this challenge restricts the adoption of advanced generation technologies and deters investment in grid-dependent solutions. Generators are often deployed as stopgap measures, with limited integration into smart or hybrid energy systems. Until grid modernization, network expansion, and distribution reliability improve through ongoing projects such as Luanda’s transmission reinforcement programs and planned provincial network upgrades, generator demand will remain fragmented, and operational scalability for both incumbents and new entrants will be structurally constrained.

Angola Generator Market (2026-32) Segmentation Analysis:

The Angola Generator Market study of MarkNtel Advisors evaluates and highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as follows:

Based on Application:

- Standby

- Prime & Continuous

- Peak Shaving

Standby power solutions dominate the target market with a market share of 80% due to the persistent inadequacy of grid reliability, prompting businesses and households to invest heavily in backup generation. Regulatory frameworks in many regions provide tax incentives for the installation of standby systems, particularly for critical infrastructure like hospitals and data centers, reinforcing investment flows toward this application. The consistent demand from manufacturing, telecommunications, and commercial real estate, which cannot tolerate unscheduled outages, sustains long-term revenue confidence for standby offerings. Utility disruptions and increasing sensitivity to downtime costs have solidified standby as the most resilient application category.

Capital expenditure patterns reveal that enterprises prioritize standby capabilities in asset planning, allocating budgets earlier in the investment cycle compared to prime or peak shaving solutions. Small gensets 20 kVA often cost in the range of about USD 1,199 – USD 2,189 according to local listings for generators sold in Luanda . End‑user demand is characterized by risk aversion and zero‑tolerance for operational interruptions, steering procurement toward tested, scalable standby generator sets. These combined forces policy reinforcement, investment priority, and mission-critical demand underpin the sustained leadership of standby applications in the forecast period.

Continued infrastructure modernization and stricter service‑level agreements in core industries elevate the strategic importance of standby systems. With predictable revenue streams and lower operating unpredictability relative to peak shaving or continuous use, vendors also channel R&D and sales focus into this segment. The competitive advantage further strengthens as ancillary services, such as remote monitoring and fast maintenance, integrate into standby offerings, attracting broader market adoption.

Based on Fuel type:

- Diesel

- Ethanol

- Methane

- Natural Gas

- Gasoline

- Hybrid (DG + Natural Gas)

- Others

Diesel remains the leading fuel type in the target market with a market share of 85% because of its well‑entrenched supply infrastructure and high energy density, making it the preferred choice for reliable power generation across sectors. Policy environments in many regions continue to implicitly support diesel through established fuel supply chains and standards, even as renewable mandates grow, enabling steady investment into diesel gensets. End‑user demand from construction, mining, and heavy industry gravitates toward diesel due to its proven durability under harsh operating conditions, reinforcing its dominance. The existing aftermarket ecosystem for service and parts also reduces total cost of ownership concerns, further solidifying diesel’s market leadership.

In countries with fluctuating grid performance, diesel gensets are perceived as the most cost‑effective hedge. Recent news reports that diesel generation in large power plants in Angola account for thermal/diesel plants for around 36% of generation capacity as of 2023, highlighting ongoing reliance on diesel-based power infrastructure. The ability of diesel units to provide both standby and prime power without complex infrastructure accelerates adoption, particularly where alternative fuel distribution is limited. This deep integration across applications and sectors creates robust demand consistency.

While hybrids and cleaner fuels are emerging, diesel retains an advantage due to scalability and predictable performance. Its ubiquity in logistics and maintenance networks ensures minimal operational disruption, appealing to risk‑averse buyers. As a result, investment, policy orientation, and persistent end‑user reliance converge to sustain diesel’s leadership through the forecast horizon.

Gain a Competitive Edge with Our Angola Generator Market Report:

- The Angola Generator Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Angola Generator Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Angola Generator Supply Chain Analysis

- Angola Generator Import-Export Analysis

- Angola Generator Market Trends & Developments

- Angola Generator Market Dynamics

- Drivers

- Challenges

- Angola Generator Market Hotspot & Opportunities

- Angola Generator Market Policies & Regulations

- Angola Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- Upto 5 KVA

- 6 KVA to 20 KVA

- 21 KVA to 75 KVA

- 76 KVA to 375 KVA

- 376 KVA to 750 KVA

- 751 KVA to 2000 KVA

- Above 2000 KVA

- By Application- (USD Million & Thousand Units)

- Standby

- Prime & Continuous

- Peak Shaving

- By End User- (USD Million & Thousand Units)

- Residential

- Commercial Offices

- Hospitality

- Retail

- Data Centers

- Telecom

- Oil & Gas

- Government & Transport

- Industrial (Manufacturing Facilities, Assembly Units, etc.)

- Equipment Rental Companies

- Mining

- Defense

- Others (Agriculture, Healthcare, Educational Institutes, etc.)

- By Fuel Type- (USD Million & Thousand Units)

- Diesel

- Ethanol

- Methane

- Natural Gas

- Gasoline

- Hybrid (DG + Natural Gas)

- Others

- By Competition

- Competition Characteristics

- Market Share of Top Companies

- By Power Rating- (USD Million & Thousand Units)

- Market Size & Analysis

- Angola Diesel Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- By End User- (USD Million & Thousand Units)

- By Application- (USD Million & Thousand Units)

- Market Size & Analysis

- Angola Ethanol Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- By End User- (USD Million & Thousand Units)

- By Application- (USD Million & Thousand Units)

- Market Size & Analysis

- Angola Methane Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- By End User- (USD Million & Thousand Units)

- By Application- (USD Million & Thousand Units)

- Market Size & Analysis

- Angola Natural Gas Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- By End User- (USD Million & Thousand Units)

- By Application- (USD Million & Thousand Units)

- Market Size & Analysis

- Angola Gasoline Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- By End User- (USD Million & Thousand Units)

- By Application- (USD Million & Thousand Units)

- Market Size & Analysis

- Angola Hybrid (DG + Natural Gas) Generator Market Outlook, 2022-32F

- Market Size & Analysis

- By Revenues (USD Million)

- By Unit Sold (Thousand)

- Market Segmentation & Analysis

- By Power Rating- (USD Million & Thousand Units)

- By End User- (USD Million & Thousand Units)

- By Application- (USD Million & Thousand Units)

- Market Size & Analysis

- Competitive Outlook

- Company Profiles

- Caterpillar Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Cummins Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- MTU

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Atlas Copco

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Kohler Co.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- FG Wilson

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Honda Power Equipment

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Mitsubishi Heavy Industries

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Shanghai Diesel Engine Co., Ltd.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Doosan Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Kirloskar

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Caterpillar Inc.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now