Global Additive Manufacturing in Aerospace & Defense Market Research Report: Trends & Forecast (2026-2032)

By Technology Type (Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Stereolithography (SLA), Selective laser si ... ntering (SLS), Others), By Material Type (Metals, Polymers, Ceramics, Composites, Others), By Platform (Aircraft, Spacecraft & Launch Vehicles, Unmanned Aerial Vehicles (UAVs), Missiles & Munitions, Military Vehicles & Naval Systems, Maintenance, Repair & Overhaul (MRO)), By Application (Prototyping & Rapid Design Validation, Tooling & Fixtures, Functional Parts Manufacturing, Engine Components, Structural Airframe Parts, Interior Cabin Components, Spare Parts & On-Demand Manufacturing), By End User (Commercial Aerospace OEMs, Defense Contractors, Space Agencies & Private Space Companies, MRO Service Providers, Military & Defense Forces), and others Read more

- Aerospace & Defense

- Feb 2026

- Pages 215

- Report Format: PDF, Excel, PPT

Global Additive Manufacturing in Aerospace & Defense Market

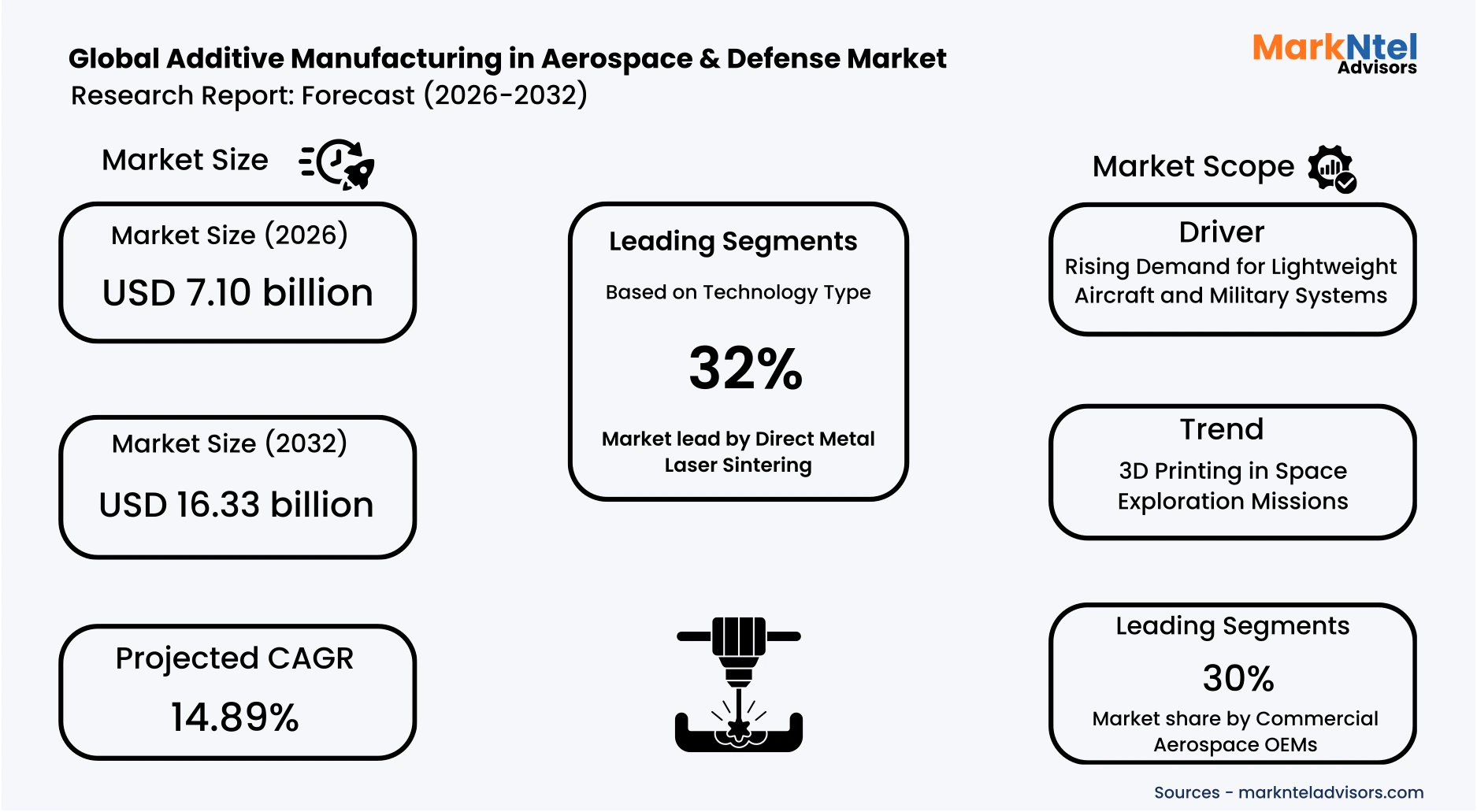

Projected 14.89% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 7.10 billion

Market Size (2032)

USD 16.33 billion

Largest Region

North America

Projected CAGR

14.89%

Leading Segments

By Technology Type: Direct Metal Laser Sintering

Global Additive Manufacturing in Aerospace & Defense Market Report Key Takeaways:

- The Global Additive Manufacturing in Aerospace & Defense Market size was valued at USD 6.18 billion in 2025 and is projected to grow from USD 7.10 billion in 2026 to USD 16.33 billion by 2032, exhibiting a CAGR of 14.89% during the forecast period.

- North America holds the largest market share of about 40% in the Global Additive Manufacturing in Aerospace & Defense Market in 2026.

- By technology type, the direct metal laser sintering (DMLS) segment represented a significant share of about 32% in the Global Additive Manufacturing in Aerospace & Defense Market in 2026.

- By end user, the commercial aerospace OEMs segment presented a significant share of about 30% in the Global Additive Manufacturing in Aerospace & Defense Market in 2026.

- Leading additive manufacturing in aerospace & defense companies in the Global Market are 3D Systems, Inc., EnvisionTEC GmbH, EOS GmbH Electro Optical Systems, The ExOne Company, Stratasys Ltd., SLM Solutions Group AG, Renishaw plc, Ultimaker B.V., Optomec, Inc., Prodways Group, Höganäs AB, General Electric Company, The Boeing Company, Airbus SE, Lockheed Martin Corporation, Northrop Grumman Corporation, BAE Systems plc, Safran SA, Rolls-Royce Holdings plc, Honeywell International Inc., Moog Inc., and Others.

Market Insights & Analysis: Global Additive Manufacturing in Aerospace & Defense Market (2026-32):

The Global Additive Manufacturing in Aerospace & Defense Market size was valued at approximately USD 6.18 billion in 2025 and is projected to grow from USD 7.10 billion in 2026 to USD 16.33 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 14.89% during the forecast period, i.e., 2026-32.

The Global Additive Manufacturing in Aerospace & Defense Market is projected to expand steadily, driven by increasing demand for lightweight aircraft and military systems alongside expanding adoption of 3D printing in space exploration missions.

Government investment is accelerating industrial readiness. The U.S. Department of Defense awarded USD 23.4 million under the Defense Production Act to expand domestic production of advanced metals used in aircraft structures, turbine blades, rocket engines, and radar systems . The initiative is designed to strengthen critical aerospace and defense supply chains while reducing reliance on foreign materials.

Growing air travel demand is further increasing the need for lighter and more efficient aircraft. The International Energy Agency reports aviation emissions reached 950 Mt CO₂ in 2023, more than 90% of pre-pandemic levels, highlighting the urgent need for efficiency improvements. The agency emphasizes that aviation efficiency must improve 2.6% annually through 2030, requiring advanced airframe designs, lightweight materials, and innovative propulsion systems such as hydrogen and electric aircraft .

Aircraft manufacturers are already scaling additive manufacturing adoption. Airbus produces over 25,000 flight-ready 3D-printed parts annually, with more than 200,000 certified polymer components currently in service across aircraft platforms, including the A320, A350, and A400M. The company also reported that 3D-printed parts used on the A350 reduced component weight by 43% and cut lead times by 85%, demonstrating strong operational and sustainability benefits .

Defense modernization programs are also accelerating AM deployment. The U.S. Air Force awarded USD 10.8 million to develop large-format metal additive manufacturing technologies for high-temperature structures used in hypersonic flight, highlighting the strategic role of 3D printing in next-generation military platforms.

Space exploration is emerging as another major growth pillar. The Indian Space Research Organisation successfully hot-tested a 3D-printed liquid rocket engine, reducing part count from 14 components to a single unit and cutting production time by 60%, showcasing the efficiency of AM in launch systems.

Long-term investments reinforce strong future demand. For example, the UK government confirmed over USD 6.3 billion in aerospace technology investment through 2030, targeting hydrogen aircraft infrastructure, next-generation engines, and large-scale additive manufacturing deployment.

Similarly, at the 2025 Paris Air Show, an additional USD 315 million funding package was announced, including USD 61 million dedicated to additive manufacturing projects led by Airbus and GKN Aerospace, signaling strong manufacturing expansion beyond 2025 .

Furthermore, the follow-on USD 7.65 million defense contract extending through 2027 further demonstrates long-term military commitment to additive manufacturing for high-speed flight platforms.

Rising aviation demand, defense modernization, and large-scale government investments are collectively accelerating additive manufacturing adoption. These long-term programs will sustain strong market expansion and position AM as a critical production technology across aerospace and defense.

Global Additive Manufacturing in Aerospace & Defense Market Recent Developments:

- 2025: 3D Systems announced strong momentum in its aerospace and defense business, supported by U.S. policy tailwinds and facility expansion. The company is adding up to 80,000 sq. ft. to its Colorado Application Center to scale qualified additive manufacturing production and accelerate adoption in defense, aviation, and space programs, reinforcing domestic supply chain resilience.

- 2025: RTX’s Pratt & Whitney announced that it developed an additive manufacturing repair process for geared turbofan engine components, reducing repair time by over 60% and helping recover USD 100 million worth of parts over five years, while lowering tooling costs and easing supply-chain constraints.

Global Additive Manufacturing in Aerospace & Defense Market Scope:

| Category | Segments |

|---|---|

| By Technology Type | (Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Stereolithography (SLA), Selective laser sintering (SLS), Others), |

| By Material Type | (Metals, Polymers, Ceramics, Composites, Others), |

| By Platform | (Aircraft, Spacecraft & Launch Vehicles, Unmanned Aerial Vehicles (UAVs), Missiles & Munitions, Military Vehicles & Naval Systems, Maintenance, Repair & Overhaul (MRO)), |

| By Application | (Prototyping & Rapid Design Validation, Tooling & Fixtures, Functional Parts Manufacturing, Engine Components, Structural Airframe Parts, Interior Cabin Components, Spare Parts & On-Demand Manufacturing), |

| By End User | (Commercial Aerospace OEMs, Defense Contractors, Space Agencies & Private Space Companies, MRO Service Providers, Military & Defense Forces), |

Global Additive Manufacturing in Aerospace & Defense Market Driver:

Rising Demand for Lightweight Aircraft and Military Systems

The aerospace and defense sector is under growing pressure to reduce fuel consumption, emissions, and operating costs while improving payload capacity and range. As a result, lightweight design has become a strategic priority, and additive manufacturing (AM) is increasingly used to produce complex, weight-optimized components that conventional manufacturing cannot easily deliver.

Commercial aviation recovery is a major catalyst. The International Air Transport Association reported that global passenger traffic recovered to 94.1% of pre-pandemic levels by late 2024, forcing airlines to modernize fleets with lighter and more fuel-efficient aircraft. The industry also notes that every 1% reduction in aircraft weight can cut fuel consumption by approximately 0.75%, creating a strong economic incentive for lightweight manufacturing and advanced materials.

Modern aircraft increasingly rely on lightweight materials such as aluminum alloys, titanium, and carbon-fiber composites. Aviation engineering research shows that carbon-fiber-reinforced polymers are 20–30% lighter than aluminum, enabling major structural weight reduction and long-term fuel savings across an aircraft’s lifecycle .

Recent scientific research further highlights the impact of advanced composites, reporting that carbon-fiber technologies can reduce aircraft weight by 30–50% and improve fuel efficiency by 20–25%, significantly lowering lifecycle operating costs and emissions .

Growing aviation demand and the push for fuel efficiency are accelerating the shift toward lightweight aircraft design. This trend will continue driving strong adoption of additive manufacturing across aerospace and defense in the coming years.

Global Additive Manufacturing in Aerospace & Defense Market Trend:

3D Printing in Space Exploration Missions

Additive manufacturing is rapidly emerging as a strategic enabler for next-generation space missions, particularly as agencies prioritize long-duration exploration and reduced dependence on Earth-based supply chains.

NASA has been at the forefront of this transition, demonstrating in-orbit manufacturing through the Additive Manufacturing Facility installed aboard the International Space Station. This capability allows astronauts to produce tools and spare parts on demand, significantly lowering the need for costly resupply missions while improving operational resilience and mission continuity.

The agency has further strengthened its additive manufacturing adoption by integrating 3D-printed components into the RS-25 engines powering the Space Launch System for the Artemis program missions. These components help reduce production costs, shorten manufacturing timelines, and enhance supply-chain flexibility for large-scale rocket programs.

Similarly, the European Space Agency achieved a significant milestone by successfully producing the first metal 3D-printed component aboard the ISS in 2024. This breakthrough validates the feasibility of manufacturing structural parts directly in orbit, a capability considered critical for deep-space missions where spare-part logistics become complex and prohibitively expensive.

Overall, additive manufacturing is transitioning from experimental use to mission-critical deployment in space exploration. As agencies intensify efforts toward lunar and deep-space missions, in-orbit production capabilities are expected to play a central role in improving sustainability, reducing mission risk, and enabling self-sufficient space operations.

Global Additive Manufacturing in Aerospace & Defense Market Opportunity:

Sustainability and Greener Aircraft Manufacturing

Sustainability regulations are reshaping aerospace manufacturing priorities and accelerating the adoption of resource-efficient technologies such as additive manufacturing. Under the European Union’s ReFuelEU Aviation initiative, aviation fuel suppliers must blend 2% Sustainable Aviation Fuel (SAF) by 2025, increasing to 6% by 2030, 20% by 2035, and 70% by 2050, creating a long-term pathway toward low-carbon aviation .

The regulation also introduces a dedicated mandate for synthetic aviation fuels (e-fuels), requiring 1.2% adoption by 2030 and 35% by 2050, which is expected to accelerate investments in hydrogen, power-to-liquid fuels, and next-generation aircraft technologies .

The European Union Aviation Environmental Report identifies SAF as one of the most effective near- and mid-term solutions for reducing lifecycle aviation emissions without requiring major infrastructure changes, reinforcing the urgency for lighter and more efficient aircraft platforms.

These regulatory targets are prompting aircraft manufacturers to prioritize lightweight materials, optimized designs, and low-waste production methods. Additive manufacturing plays a crucial role by reducing material waste, enabling lightweight components, and supporting rapid design innovation aligned with decarbonization goals.

Binding SAF mandates through 2050 provide long-term demand certainty, encouraging sustained investment in sustainable aircraft technologies. This policy momentum will significantly accelerate additive manufacturing adoption across aerospace and defense supply chains, driving long-term market expansion.

Global Additive Manufacturing in Aerospace & Defense Market Challenge:

High Cost of Certification and Production Scaling

The high cost of certification, validation, and process control continues to restrict large-scale adoption of additive manufacturing in aerospace and defense. A U.S. Department of Defense–supported study by the Defense Systems Information Analysis Center highlights that qualifying aerospace components can exceed USD 130 million and take up to 15 years, reflecting the stringent safety, testing, and airworthiness requirements applied to flight-critical parts .

The same analysis notes that additive manufacturing introduces more than 100 process variables that must be tightly monitored to ensure repeatability and structural reliability. This complexity increases the need for extensive inspection, testing, and documentation before components can be approved for operational aircraft and defense platforms.

Additionally, the lack of mature industry standards and consistent material datasets forces manufacturers to invest heavily in validation infrastructure, specialized workforce training, and quality-assurance systems. These requirements significantly raise the cost per part and slow the transition from prototyping to high-volume production.

Costly certification, complex process control, and high validation investments continue to limit large-scale deployment of additive manufacturing. Without faster certification pathways and lower production costs, this challenge will slow broader market expansion in the near term.

Global Additive Manufacturing in Aerospace & Defense Market (2026-32) Segmentation Analysis:

The Global Additive Manufacturing in Aerospace & Defense Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the global level. Based on the analysis, the market has been further classified as;

Based on Technology Type:

- Direct Metal Laser Sintering (DMLS)

- Fused Deposition Modeling (FDM)

- Continuous Liquid Interface Production (CLIP)

- Stereolithography (SLA)

- Selective laser sintering (SLS)

- Others

The direct metal laser sintering (DMLS) segment dominates the Global Additive Manufacturing in Aerospace & Defense Market, accounting for approximately 32% of market size, due to its ability to produce mission-critical metal components with exceptional strength, precision, and reliability.

Aerospace and defense platforms operate in extreme environments involving high temperatures, pressure variations, and mechanical stress, requiring advanced materials such as titanium, aluminum alloys, Inconel, and stainless steel. DMLS enables the direct fabrication of these high-performance materials while maintaining stringent engineering tolerances and structural integrity.

A major factor behind its dominance is the technology’s capability to create highly complex, topology-optimized geometries that are not feasible with conventional subtractive manufacturing. This allows engineers to significantly reduce component weight while maintaining strength and durability, directly supporting industry priorities such as fuel efficiency, payload optimization, and extended operational range.

The technology also aligns well with the production economics of aerospace and defense programs, which typically involve low-volume, high-value manufacturing and frequent design iterations. By eliminating the need for specialized tooling and enabling rapid prototyping and on-demand spare part production, DMLS shortens development timelines and improves supply-chain resilience. These advantages collectively reinforce its strong and sustained leadership in the market.

Based on End User:

- Commercial Aerospace OEMs

- Defense Contractors

- Space Agencies & Private Space Companies

- MRO Service Providers

- Military & Defense Forces

The commercial aerospace OEMs segment dominates the Global Additive Manufacturing in Aerospace & Defense Market, holding around 30% market share, due to their continuous push for fuel efficiency, cost optimization, and high-volume aircraft production.

Aircraft manufacturers operate in an environment defined by strict emission targets, rising fuel prices, and increasing passenger demand, making lightweight and performance-optimized components a strategic necessity. Additive manufacturing enables the production of complex geometries and lightweight parts that are difficult or uneconomical to achieve using conventional manufacturing methods.

The steady recovery of global air travel and the expansion of airline fleets are accelerating aircraft production programs. OEMs are integrating 3D-printed components across engines, airframes, cabin interiors, environmental control systems, and fuel systems to reduce weight and improve performance.

In addition, additive manufacturing shortens design cycles and enables rapid prototyping, allowing manufacturers to accelerate new aircraft development and improve time-to-market. The technology also supports digital inventory and on-demand spare part production, reducing supply chain risks and lowering long-term maintenance costs.

With increasing certification of additively manufactured parts and rising aircraft production rates, commercial aerospace OEMs are expected to remain the primary drivers of demand, reinforcing their leading position in the market.

Global Additive Manufacturing in Aerospace & Defense Market (2026-32): Regional Projection

North America dominates the Global Additive Manufacturing in Aerospace & Defense Market with an estimated 40% share, due to its strong aerospace manufacturing ecosystem, large defense spending, and rapid adoption of advanced production technologies.

The region hosts leading aircraft manufacturers, defense contractors, and space agencies that actively integrate additive manufacturing into mission-critical production, testing, and maintenance workflows. Continuous government funding and private-sector investment further accelerate industrial deployment and certification of 3D-printed flight components.

A key 2025 example highlighting this leadership is the partnership between Velo3D and Vaya Space to accelerate additive manufacturing of propulsion systems. The two-year USD 4 million agreement focuses on producing rocket engine parts such as turbopumps, injectors, and nozzles using advanced metal printers and NASA-developed copper alloys, enabling faster and more cost-efficient propulsion production. This collaboration demonstrates how North American companies are scaling additive manufacturing for next-generation launch systems and commercial space missions.

The region also benefits from extensive defense modernization and aircraft fleet renewal programs, which require lightweight, high-performance, and rapidly manufactured components. With strong R&D infrastructure, certification frameworks, and deep supply-chain integration, North America continues to lead the industrialization of additive manufacturing across aviation, defense, and space exploration.

Gain a Competitive Edge with Our Global Additive Manufacturing in Aerospace & Defense Market Report:

- Global Additive Manufacturing in Aerospace & Defense Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Global Additive Manufacturing in Aerospace & Defense Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Global Additive Manufacturing in Aerospace & Defense Market Policies, Regulations, and Product Standards

- Global Additive Manufacturing in Aerospace & Defense Market Trends & Developments

- Global Additive Manufacturing in Aerospace & Defense Market Dynamics

- Growth Factors

- Challenges

- Global Additive Manufacturing in Aerospace & Defense Market Hotspot & Opportunities

- Global Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- Direct Metal Laser Sintering (DMLS)

- Fused Deposition Modeling (FDM)

- Continuous Liquid Interface Production (CLIP)

- Stereolithography (SLA)

- Selective laser sintering (SLS)

- Others

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- Metals

- Titanium Alloys

- Aluminum Alloys

- Nickel-Based Superalloys

- Stainless Steel

- Others

- Polymers

- High-Performance Thermoplastics (PEEK, PEKK, ULTEM)

- Nylon & Engineering Plastics

- Ceramics

- Composites

- Carbon Fiber Reinforced

- Glass Fiber Reinforced

- Others

- Metals

- By Platform - Market Size & Forecast 2022-2032, USD Million

- Aircraft

- Spacecraft & Launch Vehicles

- Unmanned Aerial Vehicles (UAVs)

- Missiles & Munitions

- Military Vehicles & Naval Systems

- Maintenance, Repair & Overhaul (MRO)

- By Application- Market Size & Forecast 2022-2032, USD Million

- Prototyping & Rapid Design Validation

- Tooling & Fixtures

- Functional Parts Manufacturing

- Engine Components

- Structural Airframe Parts

- Interior Cabin Components

- Spare Parts & On-Demand Manufacturing

- By End User- Market Size & Forecast 2022-2032, USD Million

- Commercial Aerospace OEMs

- Defense Contractors

- Space Agencies & Private Space Companies

- MRO Service Providers

- Military & Defense Forces

- By Region

- North America

- South America

- Europe

- The Middle East & Africa

- Asia-Pacific

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- North America Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- The US

- Canada

- Mexico

- Rest of North America

- The US Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Canada Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Mexico Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- South America Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- Brazil

- Argentina

- Rest of South America

- Brazil Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Argentina Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Europe Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- The UK

- Germany

- France

- Italy

- Spain

- Benelux

- Rest of Europe

- The UK Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Germany Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- France Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Italy Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Spain Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Benelux Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- The Middle East & Africa Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- Turkey

- Israel

- South Africa

- Rest of Middle East & Africa

- Turkey Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Israel Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Africa Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Asia-Pacific Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- By Country

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- China Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Japan Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- India Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- South Korea Additive Manufacturing in Aerospace & Defense Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Technology Type- Market Size & Forecast 2022-2032, USD Million

- By Material Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Application- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Market Size & Outlook

- Global Additive Manufacturing in Aerospace & Defense Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- 3D Systems, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EnvisionTEC GmbH

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- EOS GmbH Electro Optical Systems

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The ExOne Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Stratasys Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SLM Solutions Group AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Renishaw plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ultimaker B.V.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Optomec, Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Prodways Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Höganäs AB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- General Electric Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- The Boeing Company

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Airbus SE

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Lockheed Martin Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Northrop Grumman Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- BAE Systems plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Safran SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Rolls-Royce Holdings plc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell International Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Moog Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- 3D Systems, Inc.

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now