Europe Orthopaedic Implants Market - By Type (Joint Reconstruction Implants, Trauma Implants, Spinal Implants, Dental Implants, Orthobiologics, Cranio-Maxillofacial (CMF) Implants,...... Others), By Application (Neck Fracture, Spine Fracture, Hip Replacement, Shoulder Replacement, Others), By Procedure (Open Surgery, Minimally Invasive Surger, Others), By Material (Metallic Biomaterials, Polymeric Materials, Ceramic Biomaterials, Natural Biomaterials), By End User (Hospitals, Ambulatory Surgery Centers, Orthopaedic Specialty Clinics, Trauma & Emergency Care Facilities), and Others Read more

- Healthcare

- Sep 2025

- 165

- PDF, Excel, PPT

Market Insights & Analysis: Europe Orthopaedic Implants Market (2025-30):

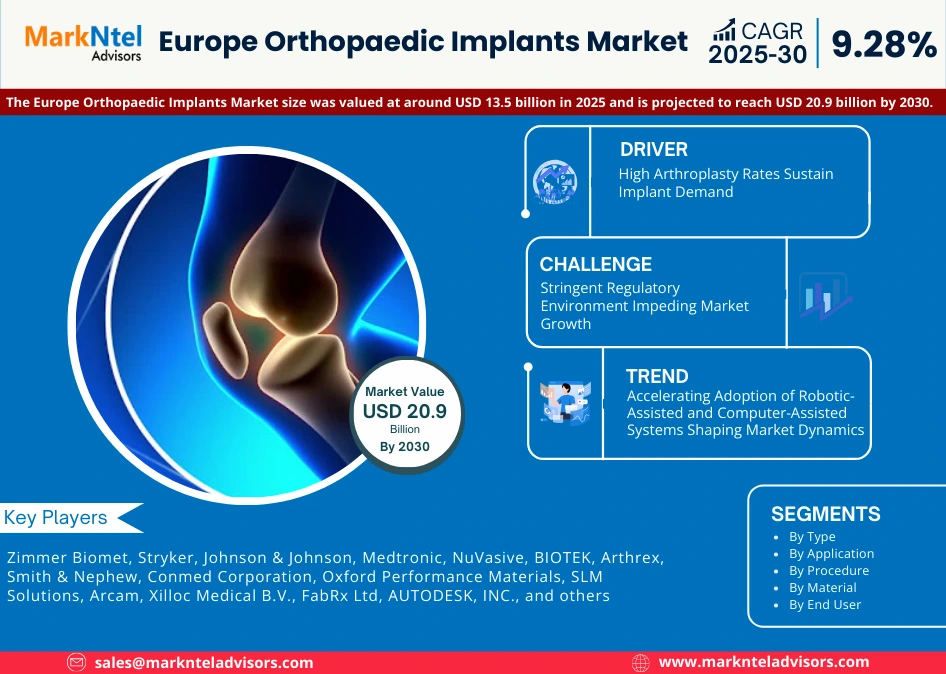

The Europe Orthopaedic Implants Market size was valued at around USD 13.5 billion in 2025 and is projected to reach USD 20.9 billion by 2030. Along with this, the market is estimated to grow at a CAGR of around 9.28% during the forecast period, i.e., 2025-30.

Various factors are attributed to the growing market. As more individuals in Europe are actively participating in sports activities, this has resulted in an increase in sports-related injuries, creating demand for orthopedic procedures and implants. Also, the demand for smart orthopedic solutions is increasing rapidly due to the adoption of digital and connected implants, paired with data services that align with European Health Data Space requirements. Moreover, various patients in the European region now require revision surgeries due to implant longevity. This has further pushed the market of revision orthopedic implants towards growth. Apart from this, the market is shifting from traditional product-only sales to integrated product plus data/service bundles while offering enhanced patient outcomes and ongoing care. Furthermore, the fragmented procurement and reimbursement systems across Europe necessitate flexible product and pricing strategies. This opens new opportunities for specialized orthopedic offerings like 3D-printed joint implants, robotic-assisted joint reconstruction systems, and smart implants with embedded sensors, along with others.

The growing number of sports activities among various people in Europe has increased the incidence of sports-related injuries. Around 6.2 million people in Europe are admitted annually who need hospital treatment for sports-related injuries. Out of them, around 402,000 cases (7%) require further treatments that involve orthopedic implants as well. Team ball sports account for 42% of all hospital-treated sports injuries, with 71% of these linked to football. As these injuries often require surgical intervention ranging from ligament reconstructions to knee and hip replacements, the demand for Orthopaedic implants continues to grow.

Moreover, Digital and connected orthopaedic implants are becoming more important in Europe due to the change in health data rules. As of January 2025, the European Health Data Space requires health systems to share electronic health records in a standard format and allows their reuse for research and monitoring. This gives an advantage to Orthopaedic implants that can provide reliable digital data. Also, the European Commission activated EUDAMED UDI & device registration rules in 2024 (Regulation EU 2024/1860) that expand traceability to the legacy devices. This has resulted in the increasing demand in hospitals for implants with strong digital identification features, including orthopaedic implants. National joint registries further add to this trend, with the UK registry passing 4 million procedures in 2024, and Sweden continues to publish detailed implant data through its Swedish Knee Arthroplasty Register and the Swedish Hip Arthroplasty Register.

Also, there is an increasing demand for revision orthopedic implants in Europe due to the prosthetics from the 1990s-2000s reaching their 15-25-year lifespan. As of 2023, 5,783 knee revisions were recorded by the National Joint Registry, along with a total of 47,090 revisions of hip replacement and 443 revisions in the elbow, confirming the clear uptick in revision procedures. Also, the National Arthroplasty Register in Sweden logs around 2,400 hip revisions and about 1,000 knee revisions every year, demonstrating persistent demand for corrective surgery. These growing numbers of revision orthopaedic implants are also the result of implant wear, failure, and issues like infection or loosening that are common in long-term joint replacements. With a shift towards modern implants from legacy devices, the growth of revision orthopedic implants will continue to rise during the forecast period.

Europe Orthopaedic Implants Market Scope:

| Category | Segments |

|---|---|

| By Type | Joint Reconstruction Implants, Trauma Implants, Spinal Implants, Dental Implants, Orthobiologics, Cranio-Maxillofacial (CMF) Implants, Others |

| By Application | Neck Fracture, Spine Fracture, Hip Replacement, Shoulder Replacement, Others |

| By Procedure | Open Surgery, Minimally Invasive Surger, Others |

| By Material | Metallic Biomaterials, Polymeric Materials, Ceramic Biomaterials, Natural Biomaterials |

| By End User | Hospitals, Ambulatory Surgery Centers, Orthopaedic Specialty Clinics, Trauma & Emergency Care Facilities), and Others |

Europe Orthopaedic Implants Market Driver:

High Arthroplasty Rates Sustain Implant Demand- Europe records some of the world’s highest arthroplasty volumes, which creates a steady baseline demand for orthopaedic implants. In Germany, over 2,29,551 knee replacements were performed in 2023, making them the most common inpatient surgeries. The UK National Joint Registry has logged more than 4 million hip and knee procedures since its creation, confirming the scale of implant use. Population ageing is expanding this candidate pool further, as by 2050, over 33% of the EU population will be over 65, sharply increasing the risk of degenerative joint disease, while further increasing arthroplasty rates. Alongside ageing, unintentional injuries, especially falls, in older adults, also sustain implant demand in Europe. The average fallers prevalence among European older adults is around 30% which creates a heavy risk for joint breakage, hence, creating the demand for orthopaedic implants in the country.

- Market Segmentation

- Introduction

- Market Definition

- Research Process

- Assumptions

- Executive Summary

- Europe Orthopedic Implants Market Trends & Insights

- Europe Orthopedic Implants Market Dynamics

- Growth Drivers

- Challenges

- Europe Orthopedic Implants Market Hotspot & Opportunities

- Europe Orthopedic Implants Market Supply Chain Analysis

- Europe Orthopedic Implants Market Regulation & Policy

- Europe Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type

- Joint Reconstruction Implants-Market Size & Forecast 2020-2030F, USD Million

- Trauma Implants-Market Size & Forecast 2020-2030F, USD Million

- Spinal Implants-Market Size & Forecast 2020-2030F, USD Million

- Dental Implants-Market Size & Forecast 2020-2030F, USD Million

- Orthobiologics-Market Size & Forecast 2020-2030F, USD Million

- Cranio-Maxillofacial (CMF) Implants-Market Size & Forecast 2020-2030F, USD Million

- Others-Market Size & Forecast 2020-2030F, USD Million

- By Application

- Neck Fracture -Market Size & Forecast 2020-2030F, USD Million

- Spine Fracture-Market Size & Forecast 2020-2030F, USD Million

- Hip Replacement-Market Size & Forecast 2020-2030F, USD Million

- Shoulder Replacement-Market Size & Forecast 2020-2030F, USD Million

- Others-Market Size & Forecast 2020-2030F, USD Million

- By Procedure

- Open Surgery-Market Size & Forecast 2020-2030F, USD Million

- Minimally Invasive Surgery-Market Size & Forecast 2020-2030F, USD Million

- Others-Market Size & Forecast 2020-2030F, USD Million

- By Material

- Metallic Biomaterials-Market Size & Forecast 2020-2030F, USD Million

- Polymeric Materials-Market Size & Forecast 2020-2030F, USD Million

- Ceramic Biomaterials-Market Size & Forecast 2020-2030F, USD Million

- Natural Biomaterials-Market Size & Forecast 2020-2030F, USD Million

- By End User

- Hospitals-Market Size & Forecast 2020-2030F, USD Million

- Ambulatory Surgery Centers -Market Size & Forecast 2020-2030F, USD Million

- Orthopaedic Specialty Clinics-Market Size & Forecast 2020-2030F, USD Million

- Trauma & Emergency Care Facilities-Market Size & Forecast 2020-2030F, USD Million

- Others-Market Size & Forecast 2020-2030F, USD Million

- By Country

- France

- Germany

- Spain

- Italy

- Benelux

- Scandinavia

- UK

- Others

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Type

- Market Size & Analysis

- France Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type - Market Size & Forecast 2020-2030, USD Million

- By Application - Market Size & Forecast 2020-2030, USD Million

- By Procedure- Market Size & Forecast 2020-2030, USD Million

- By Material- Market Size & Forecast 2020-2030, USD Million

- By End User- Market Size & Forecast 2020-2030, USD Million

- Market Size & Analysis

- Germany Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type - Market Size & Forecast 2020-2030, USD Million

- By Application - Market Size & Forecast 2020-2030, USD Million

- By Procedure- Market Size & Forecast 2020-2030, USD Million

- By Material- Market Size & Forecast 2020-2030, USD Million

- By End User- Market Size & Forecast 2020-2030, USD Million

- Market Size & Analysis

- Spain Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type - Market Size & Forecast 2020-2030, USD Million

- By Application - Market Size & Forecast 2020-2030, USD Million

- By Procedure- Market Size & Forecast 2020-2030, USD Million

- By Material- Market Size & Forecast 2020-2030, USD Million

- By End User- Market Size & Forecast 2020-2030, USD Million

- Market Size & Analysis

- Italy Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type - Market Size & Forecast 2020-2030, USD Million

- By Application - Market Size & Forecast 2020-2030, USD Million

- By Procedure- Market Size & Forecast 2020-2030, USD Million

- By Material- Market Size & Forecast 2020-2030, USD Million

- By End User- Market Size & Forecast 2020-2030, USD Million

- Market Size & Analysis

- Benelux Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type - Market Size & Forecast 2020-2030, USD Million

- By Application - Market Size & Forecast 2020-2030, USD Million

- By Procedure- Market Size & Forecast 2020-2030, USD Million

- By Material- Market Size & Forecast 2020-2030, USD Million

- By End User- Market Size & Forecast 2020-2030, USD Million

- Market Size & Analysis

- Scandinavia Orthopedic Implants Market Outlook, 2020-2030F

- Market Size & Analysis

- By Revenues (USD Million)

- Market Share & Analysis

- By Type - Market Size & Forecast 2020-2030, USD Million

- By Application - Market Size & Forecast 2020-2030, USD Million

- By Procedure- Market Size & Forecast 2020-2030, USD Million

- By Material- Market Size & Forecast 2020-2030, USD Million

- By End User- Market Size & Forecast 2020-2030, USD Million

- Market Size & Analysis

- Europe Orthopedic Implants Market Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- Zimmer Biomet

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Stryker

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Medtronic

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- NuVasive

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- BIOTEK

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Arthrex

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Smith & Nephew

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Conmed Corporation

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- DePuy Synthes.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- SLM Solutions

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Arcam

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Xilloc Medical B.V.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- FabRx Ltd

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- AUTODESK, INC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Zimmer Biomet

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

FILL THE FORM TO INQUIRE BEFORE BUYING THIS REPORT

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now