China Water and Wastewater Treatment Technology Market Research Report: Forecast (2026-2032)

China Water and Wastewater Treatment Technology Market - By Treatment Technology Physical & Mechanical Treatment Technologies, (Screening systems, Grit removal systems, Oil–water s ... eparation technologies, Sedimentation and clarification systems, Filtration systems), Chemical Treatment Technologies (Coagulation systems, Flocculation systems, pH control and neutralization systems, Chemical oxidation systems, Disinfection systems), Biological Treatment Technologies (Activated sludge systems, Biofilm-based treatment systems, Membrane bioreactor systems, Biological nutrient removal systems), Advanced & Resource Recovery Technologies (Membrane separation technologies, Zero liquid discharge systems, Nutrient recovery technologies, Metal recovery technologies), By System / Solution Architecture (Centralized treatment systems, Decentralized treatment systems, Modular treatment systems, Packaged treatment units), By End-User Municipal Sector (Urban wastewater utilities, Rural wastewater systems), Industrial Sector (Food and beverage industry, Chemical industry, Oil and gas industry, Pulp and paper industry, Pharmaceutical and healthcare industry, Aquaculture and poultry industry), By Treatment Stage (Preliminary treatment, Primary treatment, Secondary treatment, Tertiary treatment, Water reuse and reclamation), By Digital & Control Technologie (Process automation systems, Monitoring and sensing systems, Data analytics and optimization platforms), and others Read more

- Environment

- Jan 2026

- Pages 138

- Report Format: PDF, Excel, PPT

China Water and Wastewater Treatment Technology Market

Projected 5.43% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 18.91 Billion

Market Size (2032)

USD 27.38 Billion

Base Year

2025

Projected CAGR

5.43%

Leading Segments

By End User: Municipal Sector

China Water and Wastewater Treatment Technology Market Report Key Takeaways:

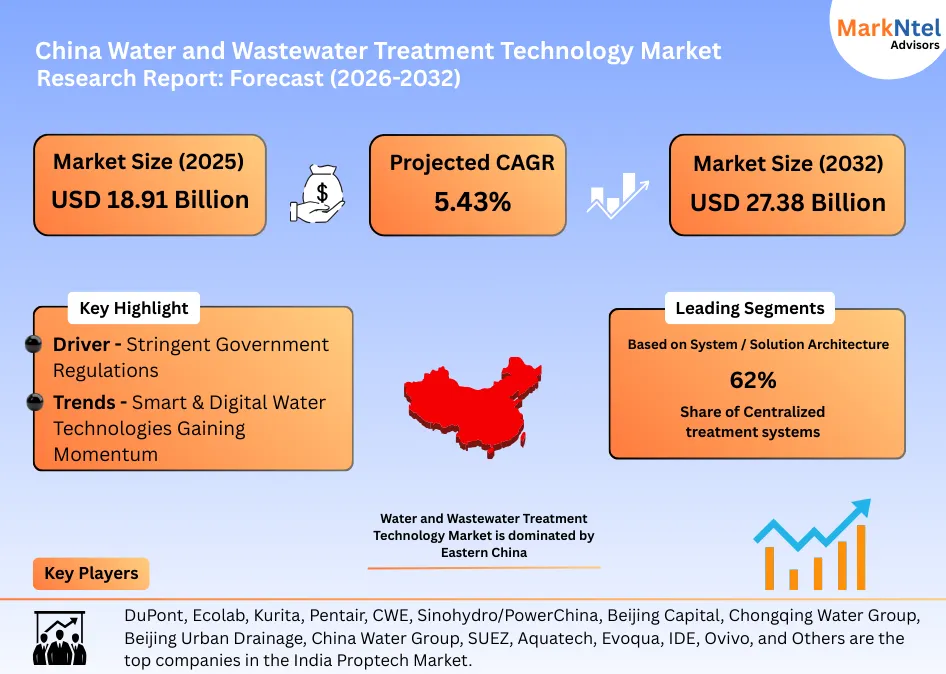

- The China Water and Wastewater Treatment Technology Market size was valued at around USD 18.91 billion in 2025 and is projected to reach USD 27.38 billion by 2032. The estimated CAGR from 2026 to 2032 is around 5.43%, indicating strong growth.

- By system/solution architecture, the centralized treatment systems represented 62% of the China Water and Wastewater Treatment Technology Market size in 2025.

- By end user, the municipal sector represented 48% of the China Water and Wastewater Treatment Technology Market size in 2025.

- By treatment technology, the biological treatment segment holds around 45% of the China Water and Wastewater Treatment Technology Market in 2025.

- The leading Water and Wastewater Treatment Technology companies in China are DuPont, Ecolab, Kurita, Pentair, CWE, Sinohydro/PowerChina, Beijing Capital, Chongqing Water Group, Beijing Urban Drainage, China Water Group, SUEZ, Aquatech, Evoqua, IDE, Ovivo, Xylem, Shanghai Kaiquan, OriginWater, Anhui Zhonghuan, Anhui Huaqi, Anhui Guozhen, Jiangsu Yihuan, Jiangsu Tianyu, Jingjin, BEWG, and others.

Market Insights & Analysis: China Water and Wastewater Treatment Technology Market (2026- 2032):

The China Water and Wastewater Treatment Technology Market size was valued at around USD 18.91 billion in 2025 and is projected to reach USD 27.38 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.43% during the forecast period, i.e., 2026-32. The China Water and Wastewater Treatment Technology Market is positioned for sustained expansion supported by regulatory enforcement, infrastructure modernization, and accelerating digital transformation. National policy focus has shifted from capacity creation alone toward quality-driven, technology-enabled water governance, increasing long-term demand for advanced treatment systems, smart monitoring platforms, and low-carbon solutions.

Government-led river and lake restoration programs covering more than 2,500 major water bodies are intensifying requirements for wastewater collection, industrial park treatment upgrades, and nutrient load reduction. These initiatives extend beyond municipal boundaries, drawing industrial and agricultural wastewater streams into formal treatment networks and raising adoption of advanced biological, membrane-based, and digital control technologies. At the same time, China’s objective to achieve at least 95 % sewage treatment coverage in county-level cities and expand reclaimed-water use in water-stressed regions continues to unlock multi-year investments in pipelines, treatment plants, and reuse infrastructure.

Technology adoption is becoming a defining feature of the market. Smart water platforms integrating AI-based analytics, real-time sensors, and automated dispatch systems are increasingly deployed at the city level, as exemplified by Fuzhou City’s platform connecting 3,000+ monitoring points, enabling AI-driven wastewater management and early-warning control. Industry exhibitions held in China during 2025, such as the WATERTECH CHINA 2025 expo in Shanghai, also demonstrate strong engagement with emerging technologies and innovation in wastewater treatment.

In addition, continued policy backing, digital water governance, and low-carbon treatment mandates are expected to shift demand toward intelligent, resilient, and resource-efficient wastewater technologies, supporting steady market growth and deeper technology penetration across urban and industrial systems.

China Water and Wastewater Treatment Technology Market Recent Developments:

- December 2025: The Asian Development Bank (ADB) and China Water Affairs Group (CWA) signed a USD 150 million financing package to modernize wastewater infrastructure in Ningxiang City, including a new 100,000 m³/day smart wastewater plant and updates to existing facilities, boosting treatment capacity and asset resilience.

- May 2025: Veolia finalized a USD 1.75 billion acquisition of the remaining 30 % stake in Water Technologies & Solutions (WTS) from CDPQ, gaining full ownership. This strategic move strengthens its global water treatment tech business, supporting advanced solutions applicable in China’s industrial and municipal wastewater sector.

China Water and Wastewater Treatment Technology Market Scope:

| Category | Segments |

|---|---|

| By Treatment Technology | Physical & Mechanical Treatment Technologies, (Screening systems, Grit removal systems, Oil–water separation technologies, Sedimentation and clarification systems, Filtration systems), Chemical Treatment Technologies (Coagulation systems, Flocculation systems, pH control and neutralization systems, Chemical oxidation systems, Disinfection systems), Biological Treatment Technologies (Activated sludge systems, Biofilm-based treatment systems, Membrane bioreactor systems, Biological nutrient removal systems), Advanced & Resource Recovery Technologies (Membrane separation technologies, Zero liquid discharge systems, Nutrient recovery technologies, Metal recovery technologies |

| By System / Solution Architecture | Centralized treatment systems, Decentralized treatment systems, Modular treatment systems, Packaged treatment units |

| By End-User | Municipal Sector (Urban wastewater utilities, Rural wastewater systems), Industrial Sector (Food and beverage industry, Chemical industry, Oil and gas industry, Pulp and paper industry, Pharmaceutical and healthcare industry, Aquaculture and poultry industry |

| By Treatment Stage | Preliminary treatment, Primary treatment, Secondary treatment, Tertiary treatment, Water reuse and reclamation |

| By Digital & Control Technologie | Process automation systems, Monitoring and sensing systems, Data analytics and optimization platforms), and others |

China Water and Wastewater Treatment Technology Market Drivers:

Stringent Government Regulations

China’s regulatory framework for water pollution prevention has become a foundational driver of wastewater treatment market growth. At the heart of this effort is the Water Pollution Prevention and Control Law, which mandates strict controls on pollutant discharge and strengthens enforcement mechanisms. Under this law, all entities discharging wastewater must obtain a pollutant discharge license and ensure effluent quality meets national or local discharge standards before release; violations can lead to fines, production suspension, or closure.

The State Council’s environmental targets emphasize expanding sewage infrastructure. For example, in 2025, China aims to increase daily sewage treatment capacity by 12 million m³ and expand sewage networks by 45,000 km, reflecting aggressive regulatory and infrastructure enforcement. According to the State Council’s guidelines, achieving a ≥95 % sewage treatment rate in county-level areas is a core policy target for improving compliance and environmental outcomes.

In addition, local governments can impose stricter local discharge limits than the national baseline, enabling provinces and cities to tailor regulations to water quality needs.

During the 15th Five-Year Plan (2026–2030), China is expanding its surface water monitoring network to include over 200 additional tributaries and small water bodies, enhancing compliance monitoring and creating demand for advanced treatment technologies over the long term.

Overall, these layered regulatory requirements from national discharge standards and licensing to expanded monitoring and local stricter limits compel municipal and industrial players to adopt modern wastewater treatment systems. This regulatory pressure ensures sustained demand for advanced treatment technologies, driving long-term growth in the China water and wastewater treatment technology market.

China Water and Wastewater Treatment Technology Market Trends:

Smart & Digital Water Technologies Gaining Momentum

A major trend shaping China’s water sector is the adoption of smart and digital water technologies, driven by high-level government policy and national strategic planning. In 2023, the Central Committee of the Communist Party of China and the State Council issued the Digital China Construction Overall Layout Plan, which explicitly calls for building a “digital twin” water governance system as part of a (smart water conservancy) framework. This integrates IoT, big data, AI, and cloud computing with traditional water management, enabling real-time monitoring, early warnings, and intelligent decision support for flood control, water allocation, and water quality control.

Under this initiative, China’s Ministry of Water Resources has advanced 94 digital twin construction tasks for water resource management, covering key river basins, reservoirs, and hydraulic infrastructure. By consolidating real-time data from tens of thousands of monitoring stations, including 53,000 precipitation and 25,000 hydrological stations, digital twins allow authorities to simulate scenarios, forecast risks, and optimize treatment and distribution operations without physical intervention.

This governmental push aligns with broader digital transformation goals for 2025 and beyond, guiding investments in water management systems that lower leakages, enhance operational efficiency, and cut costs through predictive analytics. As digital platforms become embedded in water infrastructure planning and regulation, smart water technologies will increasingly replace manual processes, accelerating the adoption of automated wastewater treatment controls and network optimization tools across cities and industrial zones nationwide.

Overall, the state-led smart water agenda is turning water utilities and regulators toward data-driven, intelligent management, making smart & digital water technologies a structural trend and long-term growth driver in China’s water and wastewater treatment market.

China Water and Wastewater Treatment Technology Market Challenges:

High Capital & Operating Costs Hindering Market Growth

High capital and operational costs continue to challenge China’s water and wastewater treatment sector. Modernizing municipal plants to meet stricter effluent standards, including nutrient removal, tertiary filtration, and low-carbon compliance, requires significant infrastructure upgrades, such as expanded treatment capacity and upgraded pipelines. The Ministry of Housing and Urban-Rural Development (MOHURD) and National Development and Reform Commission (NDRC) highlight that these upgrades increase operational complexity, energy consumption, and chemical usage, creating sustained pressure on plant budgets.

Operational challenges are exacerbated by limited fee recovery. In 2025, a wastewater treatment company in Linying County, Henan Province, reported delayed sewage fee payments of USD 78 million, forcing legal action to recover costs and maintain operations. Such cases highlight the gap between treatment expenses and collected revenues, underscoring the reliance on local government subsidies for operational continuity.

As China implements more stringent water quality standards and advanced treatment technologies, capital-intensive upgrades and recurring operational costs will remain a barrier. Strengthening cost recovery, dynamic pricing, and fiscal support mechanisms is crucial to ensure sustainable expansion and modernization of wastewater infrastructure nationwide.

China Water and Wastewater Treatment Technology Market (2026-32) Segmentation Analysis:

The China Water and Wastewater Treatment Technology Market Report and Forecast 2026-2032 offers a detailed analysis of the market based on the following segments:

Based on System / Solution Architecture:

- Centralized treatment systems

- Decentralized treatment systems

- Modular treatment systems

- Packaged treatment units

Centralized treatment systems dominate the market with a 62% share due to their ability to handle large volumes of wastewater efficiently, making them ideal for urban and industrial hubs. These systems benefit from economies of scale, lower per-unit treatment costs, and easier compliance with stringent government effluent standards. Centralized plants also allow integration of advanced treatment technologies, including biological nutrient removal, membrane filtration, and digital monitoring, which improves operational efficiency and ensures high-quality discharge.

Moreover, ongoing investments under national plans, such as upgrading pipelines and expanding treatment capacity, further strengthen the adoption of centralized solutions across China’s growing urban centers.

Based on End User:

- Municipal Sector

- Urban wastewater utilities

- Rural wastewater systems

- Industrial Sector

- Food and beverage industry

- Chemical industry

- Oil and gas industry

- Pulp and paper industry

- Pharmaceutical and healthcare industry

- Aquaculture and poultry industry

The municipal sector is the largest end-user in the China Water and Wastewater Treatment Technology Market, accounting for 48% of total demand. This dominance is driven by increasing urban populations and rapid urbanization, which significantly raise domestic wastewater generation and necessitate large-scale treatment infrastructure. Municipal systems require robust wastewater collection, treatment, and discharge solutions that can efficiently handle high volumes while meeting stringent environmental standards. The sector typically integrates a combination of physical, chemical, and biological treatment technologies along with process automation and monitoring systems to optimize operations, ensure consistent treatment quality, and reduce operational inefficiencies.

In addition, government policies and regulations promoting urban sanitation, public health protection, and sustainable water management create continuous demand for municipal wastewater infrastructure. As urban centers expand and discharge standards tighten, the municipal sector is expected to remain the key driver of market growth, supporting the adoption of advanced treatment technologies and efficient operational solutions.

China Water and Wastewater Treatment Technology Market (2026-32): Regional Projection

The China Water and Wastewater Treatment Technology Market is dominated by Eastern China, including provinces such as Jiangsu, Zhejiang, Guangdong, and Shandong. These regions lead due to high urbanization rates, dense populations, and extensive industrial and municipal infrastructure requiring advanced wastewater treatment solutions. The presence of large urban centers and industrial hubs drives demand for centralized and technologically advanced treatment plants.

Additionally, stringent local government regulations on water pollution control and water reuse incentivize the adoption of modern physical, chemical, biological, and digital treatment technologies. Eastern China also attracts substantial public and private investments in wastewater infrastructure, enabling the deployment of smart monitoring systems and energy-efficient solutions. The combination of high wastewater volumes, regulatory enforcement, and financial capacity makes Eastern China the most significant regional market, accounting for a major share of national water and wastewater treatment technology adoption, and positioning it as a key driver for market growth over the coming decade.

Gain a Competitive Edge with Our China Water and Wastewater Treatment Technology Market Report:

- China Water and Wastewater Treatment Technology Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- China Water and Wastewater Treatment Technology Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Demand Side Analysis

- Current Water & Wastewater Treatment Infrastructure

- Urban Municipal Infrastructure

- Rural & Small Town Installations

- Industrial Treatment Infrastructure

- Existing Capacity (MLD / BGD)

- Demand Analysis

- Water Consumption Trends (Municipal & Industrial)

- Wastewater Generation Patterns

- Regulatory Compliance Demand (effluent standards)

- Drivers of New Capacity Demand

- Future CapEx & Planned Projects

- Government Planned Investments

- Provincial & City Level CapEx Plans

- Corporate / Industrial Planned CapEx

- PPP & Private Participation Projects

- Forecast of Infrastructure Expansion (2025–2035)

- Demand Forecast

- Installed Capacity Forecast

- Treatment Technology Adoption Forecast

- Regional Demand Forecast

- Current Water & Wastewater Treatment Infrastructure

- China Water and Wastewater Treatment Technology Market Policies, Regulations, and Product Standards

- China Water and Wastewater Treatment Technology Market Supply Chain Analysis

- China Water and Wastewater Treatment Technology Market Trends & Developments

- China Water and Wastewater Treatment Technology Market Dynamics

- Growth Drivers

- Challenges

- China Water and Wastewater Treatment Technology Market Hotspot & Opportunities

- China Water and Wastewater Treatment Technology Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Billion)

- Market Share & Outlook

- By Treatment Technology- Market Size & Forecast 2022-2032, USD Billion

- Physical & Mechanical Treatment Technologies

- Screening systems

- Grit removal systems

- Oil–water separation technologies

- Sedimentation and clarification systems

- Filtration systems

- Chemical Treatment Technologies

- Coagulation systems

- Flocculation systems

- pH control and neutralization systems

- Chemical oxidation systems

- Disinfection systems

- Biological Treatment Technologies

- Activated sludge systems

- Biofilm-based treatment systems

- Membrane bioreactor systems

- Biological nutrient removal systems

- Advanced & Resource Recovery Technologies

- Membrane separation technologies

- Zero liquid discharge systems

- Nutrient recovery technologies

- Metal recovery technologies

- Physical & Mechanical Treatment Technologies

- By System / Solution Architecture- Market Size & Forecast 2022-2032, USD Billion

- Centralized treatment systems

- Decentralized treatment systems

- Modular treatment systems

- Packaged treatment units

- By End-User - Market Size & Forecast 2022-2032, USD Billion

- Municipal Sector

- Urban wastewater utilities

- Rural wastewater systems

- Industrial Sector

- Food and beverage industry

- Chemical industry

- Oil and gas industry

- Pulp and paper industry

- Pharmaceutical and healthcare industry

- Aquaculture and poultry industry

- Municipal Sector

- By Treatment Stage- Market Size & Forecast 2022-2032, USD Billion

- Preliminary treatment

- Primary treatment

- Secondary treatment

- Tertiary treatment

- Water reuse and reclamation

- By Digital & Control Technologie - Market Size & Forecast 2022-2032, USD Billion

- Process automation systems

- Monitoring and sensing systems

- Data analytics and optimization platforms

- By Region

- Eastern China

- Central China

- Northern China

- Western China

- By Company

- Company Revenue Shares

- Competitor Characteristics

- By Treatment Technology- Market Size & Forecast 2022-2032, USD Billion

- Market Size & Outlook

- China Physical & Mechanical Treatment Technologies Market Outlook, 2022-2032

- Market Size & Analysis

- Market Share & Analysis

- By System / Solution Architecture- Market Size & Forecast 2022-2032, USD Billion

- By End-User Category- Market Size & Forecast 2022-2032, USD Billion

- By Treatment Stage- Market Size & Forecast 2022-2032, USD Billion

- By Digital & Control Technologies- Market Size & Forecast 2022-2032, USD Billion

- China Chemical Treatment Technologies Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Billion)

- Market Share & Analysis

- By System / Solution Architecture- Market Size & Forecast 2022-2032, USD Billion

- By End-User Category- Market Size & Forecast 2022-2032, USD Billion

- By Treatment Stage- Market Size & Forecast 2022-2032, USD Billion

- By Digital & Control Technologies- Market Size & Forecast 2022-2032, USD Billion

- Market Size & Analysis

- China Biological Treatment Technologies Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Billion)

- Market Share & Analysis

- By System / Solution Architecture- Market Size & Forecast 2022-2032, USD Billion

- By End-User Category- Market Size & Forecast 2022-2032, USD Billion

- By Treatment Stage- Market Size & Forecast 2022-2032, USD Billion

- By Digital & Control Technologies- Market Size & Forecast 2022-2032, USD Billion

- Market Size & Analysis

- China Advanced & Resource Recovery Technologies Market Outlook, 2022-2032

- Market Size & Analysis

- Market Revenues (USD Billion)

- Market Share & Analysis

- By System / Solution Architecture- Market Size & Forecast 2022-2032, USD Billion

- By End-User Category- Market Size & Forecast 2022-2032, USD Billion

- By Treatment Stage- Market Size & Forecast 2022-2032, USD Billion

- By Digital & Control Technologies- Market Size & Forecast 2022-2032, USD Billion

- Market Size & Analysis

- China Water and Wastewater Treatment Technology Market Key Strategic Imperatives for Success & Growth

- Competition Outlook

- Company Profiles

- DuPont

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Ecolab

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Kurita

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Pentair

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- CWE

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Sinohydro/PowerChina

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Beijing Capital

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Chongqing Water Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Beijing Urban Drainage

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- China Water Group

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- SUEZ

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Aquatech

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Evoqua

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- IDE

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Ovivo

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Xylem

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Shanghai Kaiquan

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- OriginWater

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Anhui Zhonghuan

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Anhui Huaqi

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Anhui Guozhen

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Jiangsu Yihuan

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Jiangsu Tianyu

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Jingjin

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- BEWG

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- DuPont

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now