US Diagnostic Labs Market Research Report: Forecast (2026-2032)

US Diagnostic Labs Market - By Test Type (Pathology, Radiology & Imaging), By Pathology Test Type (Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopatholo ... gy & Cytopathology, Molecular Diagnostics, Genetic Testing), By Radiology Type (X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others), By Service Delivery Mode (Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units), By Disease Type (Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others), By End-User (Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions), and others Read more

- Healthcare

- Feb 2026

- Pages 135

- Report Format: PDF, Excel, PPT

US Diagnostic Labs Market

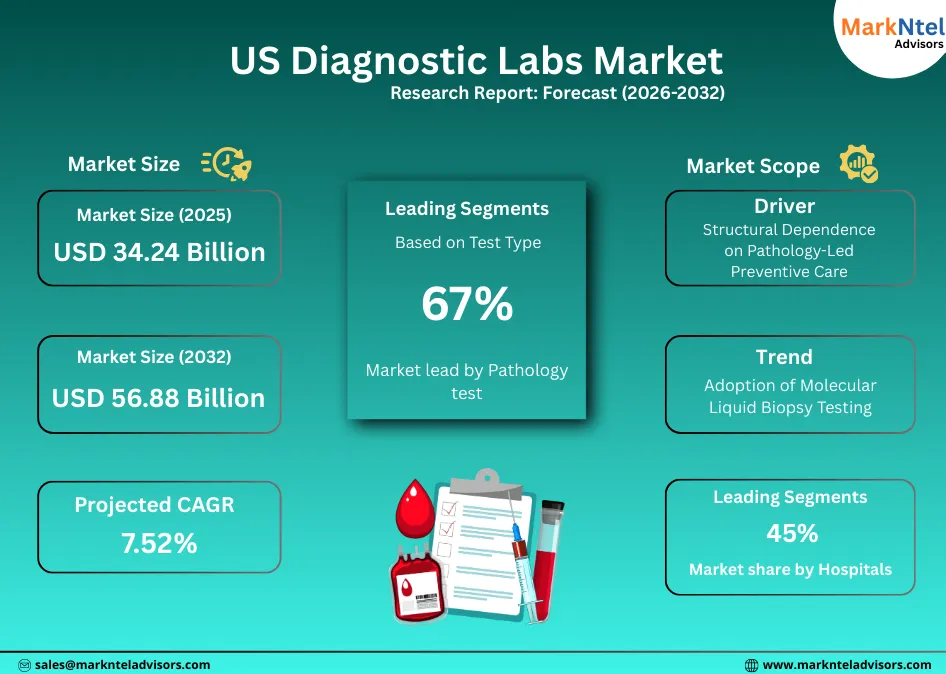

Projected 7.52% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 34.24 Billion

Market Size (2032)

USD 56.88 Billion

Base Year

2025

Projected CAGR

7.52%

Leading Segments

By End-User: Hospitals

US Diagnostic Labs Market Report Key Takeaways:

- Market size was valued at around USD34.24 billion in 2025 and is projected to reach USD56.88 billion by 2032. The estimated CAGR from 2026 to 2032 is around 7.52%, indicating strong growth.

- By Test Type, the Pathology segment represented a significant share of about 67% in the US Diagnostic Labs Market in 2025.

- By End-User, Hospitals seized a significant share of about 45% in the US Diagnostic Labs Market in 2025.

- Leading Diagnostic Labs Companies in the US Market are Labcorp, Quest Diagnostics, Mayo Clinic Laboratories, ARUP Laboratories, Bio-Reference Laboratories, Kaiser Permanente Laboratories, Cleveland Clinic Laboratories, Northwell Health Labs, Ascension Clinical Laboratories, Intermountain Healthcare Laboratories, Exact Sciences, Guardant Health, Myriad Genetics, Ambry Genetics, and Others.

Market Insights & Analysis: US Diagnostic Labs Market (2026-32):

The US Diagnostic Labs Market size was valued at around USD34.24 billion in 2025 and is projected to reach USD56.88 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 7.52% during the forecast period, i.e., 2026-32.

Market expansion is driven by the structural dependence of the US healthcare system on laboratory-led clinical decision-making, preventive screening, and chronic disease monitoring. Diagnostics form the backbone of care delivery across inpatient, outpatient, and employer-sponsored healthcare frameworks.

Market dynamics are shaped by disease burden and testing intensity. According to the US Centers for Disease Control and Prevention, nearly 129 million Americans live with at least one chronic condition, while over 42% of adults have multiple chronic diseases, necessitating repeated pathology testing. Additionally, the Centers for Medicare & Medicaid Services reports that laboratory services represent one of the highest-volume reimbursed outpatient services, reinforcing stable revenue generation.

Additionally, according to the National Institutes of Health (NIH), in 2024, the agency invested approximately USD30 billion in medical research, supporting laboratory research programs, facility upgrades, and biomedical infrastructure nationwide, thereby strengthening long-term diagnostic and pathology capacity across the United States , with diagnostics accounting for a significant share. Likewise, AI-enabled pathology, high-throughput analyzers, and digital workflows have reduced cost-per-test while increasing processing capacity.

Moreover, manufacturing and infrastructure expansion further support growth. In 2024, the Biden–Harris Administration committed USD51 million to a Central Indiana Tech Hub, strengthening biotechnology innovation, workforce development, and demonstration facilities, which indirectly support future diagnostic laboratory expansion and skilled talent availability. Similarly, in 2024, Novartis announced a USD23 billion U.S. investment plan, including biologics and research facility expansion in North Carolina, reinforcing large-scale laboratory, analytical testing, and quality-control infrastructure growth . These greenfield developments strengthen logistics resilience, turnaround times, and nationwide testing scalability, anchoring long-term market growth.

US Diagnostic Labs Market Recent Developments:

- 2025 : Quest Diagnostics formed a joint venture with Corewell Health to build and operate a 100,000 sq. ft. laboratory in Michigan, expected to open in Q1 2027, strengthening regional diagnostic capacity while Quest manages both existing and new laboratory operations.

- 2026 : Labcorp announced the construction of a new central laboratory facility in Brownsburg, Indiana, aimed at expanding testing capacity, improving turnaround times, and strengthening nationwide diagnostic infrastructure through long-term operational investment.

US Diagnostic Labs Market Scope:

| Category | Segments |

|---|---|

| By Test Type | Pathology, Radiology & Imaging |

| By Pathology Test Type | Clinical Chemistry, Hematology, Immunology & Serology, Microbiology, Histopathology & Cytopathology, Molecular Diagnostics, Genetic Testing |

| By Radiology Type | X-Ray, Ultrasound, CT Scan, MRI, Mammography, PET-CT, Nuclear Imaging, Others |

| By Service Delivery Mode | Walk-in Testing, Home Sample Collection, Mobile Diagnostic Units |

| By Disease Type | Infectious Diseases, Oncology, Diabetes & Endocrinology, Cardiology, Neurology, Nephrology, Gastroenterology, Gynecology & Obstetrics, Respiratory Disorders, Orthopedics, Others |

| By End-User | Hospitals, Physician Clinics, Independent Diagnostic Centers, Corporate & Preventive Health Programs, Government & Public Healthcare Institutions |

US Diagnostic Labs Market Driver:

Structural Dependence on Pathology-Led Preventive Care

The market growth is driven by the reliance of the healthcare system on pathology-led preventive and chronic care diagnostics. According to the CDC, 38.4 million Americans have diabetes, 116 million have hypertension, and 94 million exhibit elevated cholesterol levels, all requiring routine blood and biochemical testing. These conditions demand recurring diagnostics rather than episodic imaging.

Additionally, federal screening mandates reinforce pathology demand. The US Preventive Services Task Force expanded recommendations for colorectal cancer, lipid disorders, hepatitis C, and prediabetes screening between 2023 and 2025. Similarly, Medicare reimbursement schedules show pathology tests generate significantly higher annual claim volumes than radiology procedures, ensuring consistent lab utilization.

Moreover, according to the US Centers for Disease Control and Prevention, about 7 in 10 US adults aged 50–75 are up to date with recommended colorectal cancer screening, underscoring broad participation in routine preventive diagnostics . These accelerate clinical adoption of advanced pathology tests, strengthen diagnostic accuracy, and expand test menus, cementing pathology as the dominant testing modality.

US Diagnostic Labs Market Trend:

Adoption of Molecular Liquid Biopsy Testing

Molecular liquid biopsy adoption is emerging as a transformative trend in the US Diagnostic Labs Market because it enables non-invasive cancer detection and monitoring through blood-based genetic analysis. Unlike traditional tissue biopsies, liquid biopsies detect circulating tumor DNA (ctDNA) and other tumor indicators in blood, allowing clinicians to identify actionable mutations, monitor minimal residual disease, and personalize therapy decisions with less patient risk. The US Food and Drug Administration (FDA) has approved next-generation sequencing liquid biopsy tests such as the FoundationOne® Liquid CDx test, which detects multiple cancer-related genomic alterations to guide treatment decisions. Such regulatory clearances validate clinical utility and broaden adoption in oncology care pathways.

Clinical use is supported by broader investment and technological maturation. In 2025, Roche Diagnostics received FDA approval for a ctDNA-based liquid biopsy test for non-small cell lung cancer , expanding liquid biopsy applications in targeted therapy selection and reflecting the rising standardization of these assays.

US Diagnostic Labs Market Opportunity:

Centralized Mega-Labs and Employer Health Screening Expansion

A major revenue-generating opportunity in the US Diagnostic Labs Market lies in the expansion of centralized laboratories supported by regional outreach networks, as large payers and healthcare institutions increasingly seek scalable, cost-efficient testing models. According to the Centers for Medicare & Medicaid Services, Medicaid spending reached USD 931.7 billion in 2024 , illustrating the scale of public healthcare funding that underpins clinical services, including outsourced laboratory diagnostics across hospital and community settings.

This opportunity is reinforced by structural shifts toward laboratory consolidation. According to the US Government Accountability Office, clinical laboratory outsourcing and consolidation can meaningfully improve turnaround times and reduce per-test operational costs, prompting hospitals and health systems to move high-volume diagnostics to centralized laboratories while retaining clinical oversight.

Employer-sponsored preventive healthcare further strengthens demand visibility. According to the US Bureau of Labor Statistics, in March 2025, 72% of private-industry workers had access to employer-provided medical care benefits, while 45% actively participated, reinforcing consistent utilization of annual pathology-based preventive screenings such as blood chemistry, lipid panels, and metabolic tests. These factors are contributing to the potential market growth.

US Diagnostic Labs Market Challenge:

Capital-Heavy Infrastructure & Skilled Workforce Shortage

High capital intensity remains a structural challenge for diagnostic laboratories, particularly as the market shifts toward automation and advanced molecular testing. According to the US Department of Health and Human Services, capital expenditure constitutes one of the largest fixed cost components for clinical laboratories due to investments in high-complexity testing infrastructure. Advanced molecular analyzers, automation systems, and digital pathology platforms typically require multi-million-dollar installations, creating entry and scaling barriers for small and mid-sized laboratories.

This financial pressure is compounded by persistent workforce shortages. According to the American Society for Clinical Pathology, vacancy rates for medical laboratory technologists exceeded 28% in 2024, with the most acute gaps observed in molecular diagnostics, cytogenetics, and histopathology. Limited availability of skilled personnel increases wage inflation, prolongs onboarding timelines, and restricts laboratories’ ability to expand test menus or operate high-throughput platforms efficiently.

Regulatory compliance further elevates operational risk and cost exposure. According to the Office of Inspector General, audits related to CLIA compliance, billing accuracy, and healthcare data security continue to identify widespread deficiencies across diagnostic providers. These findings often result in corrective action mandates, operational disruptions, and financial penalties, reducing margin flexibility and delaying expansion initiatives. Together, high capital requirements, workforce scarcity, and regulatory burden create a compounded challenge that disproportionately impacts smaller laboratories and slows overall market scalability.

US Diagnostic Labs Market (2026-32) Segmentation Analysis:

The US Diagnostic Labs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Test Type:

- Pathology

- Radiology & Imaging

Pathology test dominates the US Diagnostic Labs Market with a market share of about 67% because these are essential across preventive care, chronic disease monitoring, and treatment management, generating far higher volumes than episodic radiology procedures.

Clinical chemistry and hematology represent the largest pathology sub-segments, encompassing routine panels such as basic metabolic, liver function, lipid profiles, and Complete Blood Count (CBC) tests. Clinical literature indicates hundreds of millions of CBCs are performed yearly in the US, reflecting their central role in monitoring conditions like diabetes, heart disease, and anemia. These tests are repeated frequently over a patient’s lifetime, unlike individual imaging studies.

Immunology and serology tests further contribute to volume, driving large-scale screening for infectious and autoimmune disorders at community and hospital levels. Microbiology testing supports infection diagnosis and antibiotic stewardship programs, requiring repeated cultures and sensitivity analyses.

Based on End-User:

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

Hospitals hold the largest market share of about 45% because they sit at the center of acute care, chronic disease management, and high-complexity testing that cannot be shifted to decentralized settings. According to the American Hospital Association, the US had over 6,100 hospitals in 2024, collectively delivering inpatient, emergency, surgical, and intensive-care services that require continuous, on-site diagnostic support.

Additionally, hospitals lead the adoption of advanced diagnostics. Academic medical centers and large hospital systems are primary users of genetic testing, histopathology, and precision diagnostics, driven by oncology programs and transplant services. Because hospitals combine patient volume, clinical complexity, reimbursement scale, and regulatory capability, they remain the largest and most influential end-use segment in the US Diagnostic Labs Market.

Gain a Competitive Edge with Our US Diagnostic Labs Market Report:

- US Diagnostic Labs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- US Diagnostic Labs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- US Diagnostic Labs Market Policies, Regulations, and Product Standards

- US Diagnostic Labs Market Trends & Developments

- US Diagnostic Labs Market Dynamics

- Growth Factors

- Challenges

- US Diagnostic Labs Market Hotspot & Opportunities

- US Diagnostic Labs Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Pathology

- Radiology & Imaging

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- Clinical Chemistry

- Hematology

- Immunology & Serology

- Microbiology

- Histopathology & Cytopathology

- Molecular Diagnostics

- Genetic Testing

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- X-Ray

- Ultrasound

- CT Scan

- MRI

- Mammography

- PET-CT

- Nuclear Imaging

- Others

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- Walk-in Testing

- Home Sample Collection

- Mobile Diagnostic Units

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- Infectious Diseases

- Oncology

- Diabetes & Endocrinology

- Cardiology

- Neurology

- Nephrology

- Gastroenterology

- Gynecology & Obstetrics

- Respiratory Disorders

- Orthopedics

- Others

- By End-User- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- Physician Clinics

- Independent Diagnostic Centers

- Corporate & Preventive Health Programs

- Government & Public Healthcare Institutions

- By Region- Market Size & Forecast 2022-2032, USD Million

- Northeast

- South Atlantic

- Pacific

- West South Central

- East North Central

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Test Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Pathology Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Radiology & Imaging Labs Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Pathology Test Type- Market Size & Forecast 2022-2032, USD Million

- By Radiology Type- Market Size & Forecast 2022-2032, USD Million

- By Service Delivery Mode- Market Size & Forecast 2022-2032, USD Million

- By Disease Type - Market Size & Forecast 2022-2032, USD Million

- By End-User- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- US Diagnostic Labs Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Labcorp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quest Diagnostics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mayo Clinic Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ARUP Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Bio-Reference Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Kaiser Permanente Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cleveland Clinic Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Northwell Health Labs

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ascension Clinical Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Intermountain Healthcare Laboratories

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Exact Sciences

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Guardant Health

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Myriad Genetics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ambry Genetics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Labcorp

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now