UAE Medical Consumables Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Healthcare Settings (Hospitals, Multispecialty Hospitals, Specialty Clinics, Others), By Usage (Surgical, Non-Surgical), By Division (Exam Gloves, Surgeons’ Gloves, Diagnostics ... Consumables, Anaesthesia Consumables, Advanced Wound Care, Vascular Access, Laboratory Consumables, Respiratory Consumables, EVS / Infection Control, Personal Protection (non-glove PPE), Urology, Personal Care, Primary + Preventive Care, SPT, Ready Care, Rehab & Fall Prevention, Medline Textiles), By Clinical Specialties (Cardiology, Gynecology, Urology, Orthopedics and Trauma, General Surgery and Laparoscopic Surgery, Nephrology and Dialysis, Oncology Medical and Surgical, Respiratory and Pulmonology, Gastroenterology, Vascular Surgery and Endovascular Procedures, Anesthesiology and Perioperative Care, Others), By Material (Disposable, Non-Disposable), and others Read more

- Healthcare

- Feb 2026

- Pages 130

- Report Format: PDF, Excel, PPT

UAE Medical Consumables Market

Projected 7.8% CAGR from 2026 to 2032

Study Period

2026-2032

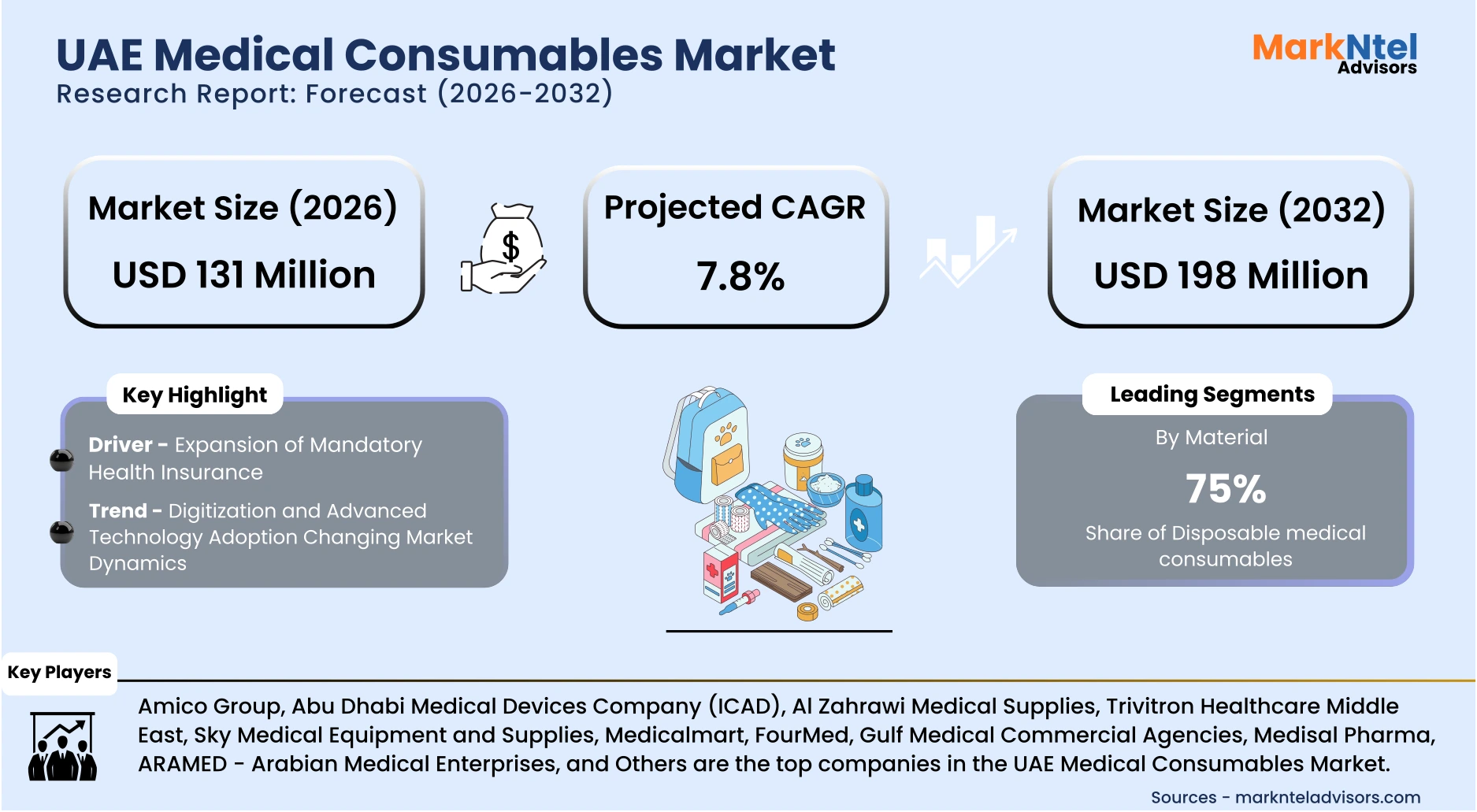

Market Size (2026)

USD 131 Million

Market Size (2032)

USD 198 Million

Base Year

2025

Projected CAGR

7.8%

Leading Segments

By Material: Disposable

UAE Medical Consumables Market Report Key Takeaways:

- Market size is valued at around USD 131 Million in 2026 and is projected to reach USD 198 Million by 2032. The estimated CAGR from 2026 to 2032 is around 7.8%, indicating strong growth.

- By Healthcare Settings, the Hospitals segment represented a significant share of about 67% in the UAE Medical Consumables Market in 2026.

- By material, the disposable segment presented a significant share of about 75% in the UAE Medical Consumables Market in 2026.

- Leading UAE Medical Consumables Companies in the UAE Market are Amico Group, Abu Dhabi Medical Devices Company (ICAD), Al Zahrawi Medical Supplies, Trivitron Healthcare Middle East, Sky Medical Equipment and Supplies, Medicalmart, FourMed, Gulf Medical Commercial Agencies, Medisal Pharma, ARAMED - Arabian Medical Enterprises, and Others.

Market Insights & Analysis: UAE Medical Consumables Market (2026-32):

The UAE Medical Consumables Market size is valued at around USD 131 Million in 2026 and is projected to reach USD 198 Million by 2032. Along with this, the market is estimated to grow at a CAGR of around 7.8% during the forecast period, i.e., 2026-32.

The UAE medical consumables market has demonstrated sustained expansion over the past decade, underpinned by consistent healthcare system upgrades and rising utilization of clinical services. This structural demand resilience has positioned medical consumables as a non-discretionary and steadily growing component of national healthcare expenditure.

Current market conditions are shaped by rapid institutional demand growth, particularly from public and private hospitals operating under expanded service mandates. In 2025, the UAE Ministry of Health and Prevention implemented updated infection prevention and control compliance frameworks aligned with WHO standards, increasing mandatory usage of single-use gloves, syringes, wound dressings, and sterilization products. Institutional end users, including tertiary hospitals and specialty centers, now account for the dominant share of consumption due to high patient throughput and regulatory compliance obligations. Commercial healthcare operators have also expanded outpatient and day-care procedures, reinforcing recurring consumable demand.

Regulatory and industrial policies continue to reinforce market expansion through localization and manufacturing incentives. The UAE’s Operation USD 300 billion industrial strategy, updated in 2025, prioritized domestic production of medical supplies under advanced manufacturing categories, offering financing access and procurement preference for locally produced consumables . UAE’s industrial ecosystem, supported by the National In-Country Value program, has attracted medical device manufacturing investments focused on consumables such as catheters and disposables. These initiatives have improved supply reliability while gradually reducing import dependency.

Looking ahead, market prospects remain favorable as demographic and infrastructure drivers converge. UN population projections updated in 2025 indicate continued population growth and a rising proportion of residents aged over 60 , directly increasing chronic care and surgical consumable usage. Ongoing hospital capacity expansions announced in Dubai and Abu Dhabi health authority capital plans for 2026 are expected to elevate procedural volumes. Together, institutional demand growth, regulatory enforcement, and domestic manufacturing support are set to sustain long-term expansion of the UAE medical consumables market.

UAE Medical Consumables Market Recent Developments:

- 2025: Borouge Plc unveiled Bormed™ LE6607-PH, the UAE’s first locally manufactured medical-grade low-density polyethylene (LDPE) engineered for healthcare applications. This polymer is used in sterile pharmaceutical and medical packaging such as blow-fill-seal bottles, ampoules, and other containers that are essential inputs for consumables manufacturing and aseptic production processes.

- 2026: In 2026, Abu Dhabi Biobank entered a strategic collaboration with AstraZeneca to advance precision medicine, biomarker discovery, and translational research. The partnership strengthens local genomic and diagnostic research capabilities, supporting increased use of specialized biospecimen collection systems, genetic testing kits, and laboratory consumables in advanced clinical and research workflows.

UAE Medical Consumables Market Scope:

| Category | Segments |

|---|---|

| By Healthcare Settings | (Hospitals, Multispecialty Hospitals, Specialty Clinics, Others), |

| By Usage | (Surgical, Non-Surgical), |

| By Division | (Exam Gloves, Surgeons’ Gloves, Diagnostics Consumables, Anaesthesia Consumables, Advanced Wound Care, Vascular Access, Laboratory Consumables, Respiratory Consumables, EVS / Infection Control, Personal Protection (non-glove PPE), Urology, Personal Care, Primary + Preventive Care, SPT, Ready Care, Rehab & Fall Prevention, Medline Textiles), |

| By Clinical Specialties | (Cardiology, Gynecology, Urology, Orthopedics and Trauma, General Surgery and Laparoscopic Surgery, Nephrology and Dialysis, Oncology Medical and Surgical, Respiratory and Pulmonology, Gastroenterology, Vascular Surgery and Endovascular Procedures, Anesthesiology and Perioperative Care, Others), |

| By Material | (Disposable, Non-Disposable), |

UAE Medical Consumables Market Driver:

Expansion of Mandatory Health Insurance

The most influential driver currently augmenting the UAE medical consumables market is the nationwide rollout and enforcement of mandatory health insurance coverage, which has structurally increased healthcare utilization rates and procedural volumes across multiple emirates. In 2025, the UAE Cabinet approved an extension of compulsory health insurance to private sector employees and domestic workers, providing standardized benefits and pricing, low annual premiums, and basic inpatient/outpatient coverage. This enables broad uptake of essential medical services such as consultations, lab tests, and inpatient care, making healthcare more accessible to workers previously uninsured in the Northern Emirates. This policy linkage between insurance and visa issuance has integrated a broader population into formal healthcare financing arrangements, significantly raising demand for insured clinical services and associated consumables.

This expansion has measurably impacted demand patterns within hospital and outpatient care settings. Mandatory coverage has reduced direct cost barriers for many residents, enabling earlier engagement with routine check-ups, diagnostics, and therapeutic interventions. In the Northern Emirates, healthcare providers reported up to a 25% increase in hospital patient volumes following the mandatory insurance rollout, with notable growth in outpatient visits and minor procedures previously deferred due to cost constraints. Such utilization directly correlates with higher per-service consumable usage, including sterile disposables, procedural kits, and diagnostic supplies.

The nature of this driver goes beyond short-term adoption or pricing effects, as it structurally alters the volume of services consumed by enrolled individuals. Insurance-linked demand, particularly for preventive care and early diagnosis, requires repeated use of medical consumables for both inpatient and outpatient episodes. Government-mandated coverage standards, including minimum benefits for inpatient and outpatient care, ensure consumables remain a recurring cost rather than a one-off purchase, anchoring long-term demand growth.

Furthermore, the broadening of coverage to include dependents and workers in the Northern Emirates has expanded the insured population base, leading to more predictable and frequent clinical encounters. This expanded base reduces variability in demand forecasts for consumables and enables healthcare institutions to scale procurement and inventory planning accordingly. As coverage enforcement continues and insurance uptake rises, the structural increase in service utilization continues to drive consistent year-on-year growth in consumable demand across the UAE medical consumables market.

UAE Medical Consumables Market Trend:

Digitization and Advanced Technology Adoption Changing Market Dynamics

A major structural trend reshaping the UAE medical consumables market is the digitization of healthcare delivery and the adoption of advanced technologies across hospital systems and outpatient facilities. Hospitals and healthcare networks in the UAE are increasingly integrating digital health platforms, electronic records, AI diagnostics, and robotics into everyday operations, moving care delivery toward data-driven precision and operational efficiency. Digital transformation enhances patient triage, optimizes clinical workflows, and supports predictive planning, all of which indirectly elevate the importance of consumable supply reliability and inventory responsiveness.

The shift to smart hospital ecosystems is supported by national innovation strategies and digital health roadmaps that prioritize interoperability, real-time data access, and technology-enabled care pathways. For instance, Burjeel Hospital and Mediclinic City Hospital use AI-driven diagnostic platforms to improve imaging analysis, while Cleveland Clinic Abu Dhabi applies predictive analytics for workflow optimization. Rashid Hospital incorporates AI imaging tools for rapid cardiovascular and neurological assessment. Government-linked systems such as DHA’s virtual health assistant and Abu Dhabi’s Smart Healthcare Platform further support automated scheduling, real-time monitoring, and proactive risk profiling, creating an environment where consumable demand becomes more predictable, standardized, and integrated within digital care pathways .

Parallel to hospital digitization, the uptake of robotic and minimally invasive surgical technologies continues to accelerate. Emirati hospitals are expanding the use of robotics to enhance precision, reduce recovery times, and support complex procedures that traditionally required larger surgical teams. This evolution toward precision care increases the consumption of specific disposable items tied to advanced procedures, such as laparoscopic kits and related sterile consumables, reinforcing structurally higher demand in specialized clinical settings.

These technology-driven shifts are underpinned by broader digital infrastructure developments, including nationwide efforts to unify electronic health records and real-time clinical data exchange, that improve resource visibility, inventory optimization, and operational coordination. As digital and smart systems become embedded across the UAE healthcare ecosystem, they are expected to sustain and structurally elevate medical consumables demand by aligning procurement with digital care pathways and performance metrics.

UAE Medical Consumables Market Opportunity:

Expansion of Ambulatory and Minimally Invasive Care Settings

The central pillar supporting expansion in the UAE medical consumables sector lies in the rapid growth of ambulatory surgery centers (ASCs) and minimally invasive care procedures, which structurally increase demand for high-turnover consumable products. For example, in 2024, Burjeel Holdings inaugurated a State of the Art Day Surgery Center in Al Dhahir, Al Ain, a facility designed to deliver comprehensive outpatient surgical services and minimize prolonged inpatient stays, illustrating tangible investment and capacity expansion in the ambulatory surgery space in the UAE. This growth underscores a broader shift toward outpatient and day-care surgical models that consume significant quantities of sterile disposables and procedural kits.

Regulatory and operational environments support this transition. Healthcare facility portfolios in urban centers such as Dubai include 58 day-care surgery centers that expand access to elective procedures, reducing inpatient admissions while increasing throughput of ambulatory interventions. These settings inherently require frequent use of consumables like surgical drapes, sterile gloves, single-use instruments, and wound care products due to stringent infection-control protocols and rapid turnover between cases.

At the same time, the increasing adoption of minimally invasive procedures across UAE hospitals is contributing to higher consumable usage, as these techniques rely heavily on single-use and procedure-specific disposable products. and outpatient facilities are performed using minimally invasive techniques, accelerating the adoption of related disposables such as endoscopes, insufflation tubing, and laparoscopic accessory kits. This shift aligns with patient preferences for shorter recovery times and lower complication risks, expanding the total addressable demand for consumables beyond traditional surgical settings.

From a supplier perspective, ambulatory and minimally invasive care pathways offer predictable, high-frequency consumable demand with relatively standardized product requirements, enabling new entrants to scale efficiently through framework agreements and volume contracts. As the UAE healthcare system continues to evolve toward outpatient-centric service delivery, the expansion of ambulatory and minimally invasive care presents a durable and scalable growth opportunity in the medical consumables market.

UAE Medical Consumables Market Challenge:

Complex Regulatory Compliance & Conformity Assessment Requirements

The most critical challenge facing the UAE medical consumables market is the increasing complexity of regulatory compliance and conformity assessment requirements. In 2025, the UAE introduced expanded medical device classification and post-market surveillance obligations under updated national regulations aligned with international risk-based frameworks. These changes require manufacturers and distributors to maintain detailed technical documentation, clinical performance evidence, and ongoing vigilance reporting. For consumables with high product turnover, these obligations significantly increase the administrative and operational burden.

This challenge measurably impacts market participants through longer approval timelines and higher compliance costs. Regulatory updates introduced from 2026 have increased the stringency of conformity assessment reviews for certain categories of medical consumables, with greater emphasis on certification requirements and periodic compliance verification. Smaller suppliers and import-dependent distributors face delays in product registration and re-registration, limiting their ability to respond quickly to procurement cycles. Public healthcare buyers have reported temporary supply constraints when products fail to meet updated documentation thresholds.

The regulatory burden materially restricts market expansion by raising entry barriers and discouraging portfolio diversification. As per OECD regulatory policy (2024), the compliance-intensive markets disproportionately affect small and medium enterprises, reducing competitive intensity. In the UAE context, frequent regulatory updates require continuous investment in quality management systems and regulatory expertise. While these measures strengthen patient safety and product reliability, they also slow time-to-market and increase fixed costs, constraining scalability and dampening short-term market participation for emerging players.

UAE Medical Consumables Market (2026-32) Segmentation Analysis:

The UAE Medical Consumables Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

By Healthcare Settings:

- Hospitals

- General Hospitals

- Specialty Hospitals

- Multispecialty Hospitals

- Specialty Clinics

- Others

Hospitals represent the largest and most dominant healthcare setting within the UAE medical consumables market with 67% market share. In 2024, the total number of hospital admissions across the UAE reached 526,451 cases, representing a 10.7% year-on-year increase compared with 2023, reflecting growing reliance on hospital-based care. These activities require continuous and high-volume use of medical consumables, including sterile disposables, diagnostic supplies, and infection-control products, resulting in structurally higher procurement levels compared with other care settings.

Hospital dominance is reinforced by the UAE’s healthcare infrastructure concentration. Government health statistics indicate that tertiary and multi-specialty hospitals in Abu Dhabi and Dubai deliver a broad range of complex services, including trauma care, oncology, cardiovascular treatment, and advanced surgery. Such services are inherently consumable-intensive, as they rely on single-use products to maintain sterility, patient safety, and clinical efficiency. In contrast, specialty clinics and outpatient centers typically handle lower-complexity cases with less frequent consumable turnover.

Additionally, hospitals are the primary beneficiaries of public healthcare funding and insurance-based reimbursement systems, enabling predictable procurement cycles and bulk purchasing of consumables. Public hospitals and large private hospital networks operate under standardized protocols and infection-control requirements , further cementing hospitals as the leading end-user segment for medical consumables across the UAE healthcare ecosystem.

By Material:

- Disposable

- Non-Disposable

Disposable medical consumables constitute the leading material segment in the UAE with 75% market share due to their integral role in infection prevention and standardized clinical workflows. In 2025, the UAE Ministry of Climate Change and Environment reinforced national waste segregation and biohazard handling protocols, indirectly favoring single-use products designed for safe disposal after patient contact. These regulatory expectations have accelerated healthcare providers’ preference for disposable gloves, syringes, drapes, and wound-care items, which reduce cross-contamination risks and simplify compliance with hygiene mandates.

Procurement and supply-chain dynamics further strengthen disposable material dominance. In recent years, Abu Dhabi has strengthened centralized healthcare procurement mechanisms through coordinated purchasing platforms and framework-based contracting models designed to improve supply continuity and cost efficiency for essential medical products. These arrangements support aggregated demand and standardized specifications, which are particularly well-suited to disposable medical consumables. Single-use products further benefit from scalable manufacturing processes and relatively short production lead times, enabling suppliers to respond more efficiently to fluctuations in clinical demand across healthcare facilities . This operational flexibility aligns with the UAE healthcare system’s emphasis on resilience and continuity, particularly during periods of peak patient inflow or public health surveillance.

End-user demand patterns in clinical settings may favor disposable materials over reusable alternatives in certain use cases. Academic lifecycle and operational efficiency literature from the mid-2020s indicates that single-use consumables can help limit sterilization requirements and reduce equipment turnaround times, which may support smoother clinical workflows where throughput pressures are high. Healthcare facilities increasingly value time efficiency and predictable performance over long-term reuse economics. Additionally, disposable products support consistent clinical outcomes by eliminating variability associated with repeated sterilization. These combined regulatory, operational, and utilization factors firmly position disposable materials as the dominant segment within the UAE medical consumables market.

UAE Medical Consumables Market (2026-32) Regional Analysis:

Abu Dhabi represents the largest and most dominant regional market for medical consumables in the UAE due to the highest concentration of healthcare infrastructure in the UAE, underpinned by extensive ongoing investment in hospital construction and modernization. Abu Dhabi hosts over 65 hospitals with more than 8,900 inpatient beds, along with 770+ clinics and over 1,500 medical centres, reflecting its role as the country’s largest hub for advanced clinical services. High inpatient capacity and procedure volumes with major facilities like the Cleveland Clinic Abu Dhabi and SEHA hospital networks translate into consistently elevated consumption of surgical, diagnostic, and patient-care consumables . The region’s strong fiscal capacity supports continuous procurement without disruption.

Regulatory and policy advantages further reinforce Abu Dhabi’s leadership position. The Department of Health–Abu Dhabi implemented updated value-based procurement guidelines in 2025, emphasizing quality assurance, traceability, and supplier reliability in consumables sourcing. These standards encourage long-term supply contracts and favor vendors capable of meeting strict compliance and volume requirements. Additionally, local industrial policies support domestic medical manufacturing clusters in designated economic zones, improving supply security and reducing lead times for consumable products.

Abu Dhabi exhibits comparatively stronger healthcare utilization levels than other emirates, supported by population concentration and a higher density of healthcare institutions. In recent years, official statistics showed the emirate hosting the highest number of inpatient admissions and surgical procedures nationwide, directly translating into higher per-capita consumables usage. The presence of internationally accredited hospitals and government-funded specialty centers increases adoption intensity for high-quality, single-use products. These combined economic strength, regulatory clarity, and concentrated healthcare demand firmly establish Abu Dhabi as the leading regional market for medical consumables in the UAE.

Gain a Competitive Edge with Our UAE Medical Consumables Market Report:

- The UAE Medical Consumables Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The UAE Medical Consumables Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- UAE Medical Consumables Market Policies, Regulations, and Product Standards

- UAE Medical Consumables Market Trends & Developments

- UAE Medical Consumables Market Dynamics

- Growth Factors

- Challenges

- UAE Medical Consumables Market Hotspot & Opportunities

- UAE Medical Consumables Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- Hospitals

- General Hospitals

- Specialty Hospitals

- Multispecialty Hospitals

- Specialty Clinics

- Others

- Hospitals

- By Usage- Market Size & Forecast 2022-2032, USD Million

- Surgical

- Non-Surgical

- By Division- Market Size & Forecast 2022-2032, USD Million

- Exam Gloves

- Surgeons’ Gloves

- Diagnostics Consumables

- O.R. Consumables (non-glove)

- Anaesthesia Consumables

- Advanced Wound Care

- Vascular Access

- Laboratory Consumables

- Respiratory Consumables

- EVS / Infection Control

- Personal Protection (non-glove PPE)

- Urology

- Personal Care

- Primary + Preventive Care

- SPT

- Ready Care

- Rehab & Fall Prevention

- Medline Textiles

- Others / Misc.

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- Cardiology

- Gynecology

- Urology

- Orthopedics and Trauma

- General Surgery and Laparoscopic Surgery

- Nephrology and Dialysis

- Oncology Medical and Surgical

- Respiratory and Pulmonology

- Gastroenterology

- Vascular Surgery and Endovascular Procedures

- Anesthesiology and Perioperative Care

- Others

- By Material- Market Size & Forecast 2022-2032, USD Million

- Disposable

- Non-Disposable

- By Region- Market Size & Forecast 2022-2032, USD Million

- Abu Dhabi

- Dubai

- Sharjah

- Northern Emirates

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Healthcare Settings- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Disposable Medical Consumables Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Non-Disposable Medical Consumables Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Usage- Market Size & Forecast 2022-2032, USD Million

- By Division- Market Size & Forecast 2022-2032, USD Million

- By Clinical Specialties- Market Size & Forecast 2022-2032, USD Million

- By Material- Market Size & Forecast 2022-2032, USD Million

- By Region- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Medical Consumables Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Amico Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Abu Dhabi Medical Devices Company (ICAD)

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Al Zahrawi Medical Supplies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Trivitron Healthcare Middle East

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sky Medical Equipment and Supplies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medicalmart

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- FourMed

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gulf Medical Commercial Agencies

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Medisal Pharma

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ARAMED - Arabian Medical Enterprises

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Amico Group

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now