UAE Gaming Market Research Report: Trends, Forecast & Opportunities (2026-2032)

By Type (Normal Gaming, Esports Gaming), By Device Type (Mobile Gaming, PC Gaming, Console Gaming), By Platform (Online Gaming, Offline Gaming), By Game Genre (Action & Adventure, ... Sports & Racing, Strategy, Role-Playing, Casual & Puzzle, Shooter, Simulation, Others), By Players Engaged (Single Player, Multi-Player), By Age Group (Upto 18 Years, 19 to 35 Years, Above 35 Years), By Player Type (Male Gamers, Female Gamers), By Technology (Cloud Gaming, VR / AR Gaming, Blockchain / Web3 Gaming, Social Gaming, iGaming & Online Betting), By Revenue Model (In-Game Purchases, Game Purchases, Advertising Revenue, Subscriptions, Sponsorship & Media Rights), and others Read more

- ICT & Electronics

- Feb 2026

- Pages 144

- Report Format: PDF, Excel, PPT

UAE Gaming Market

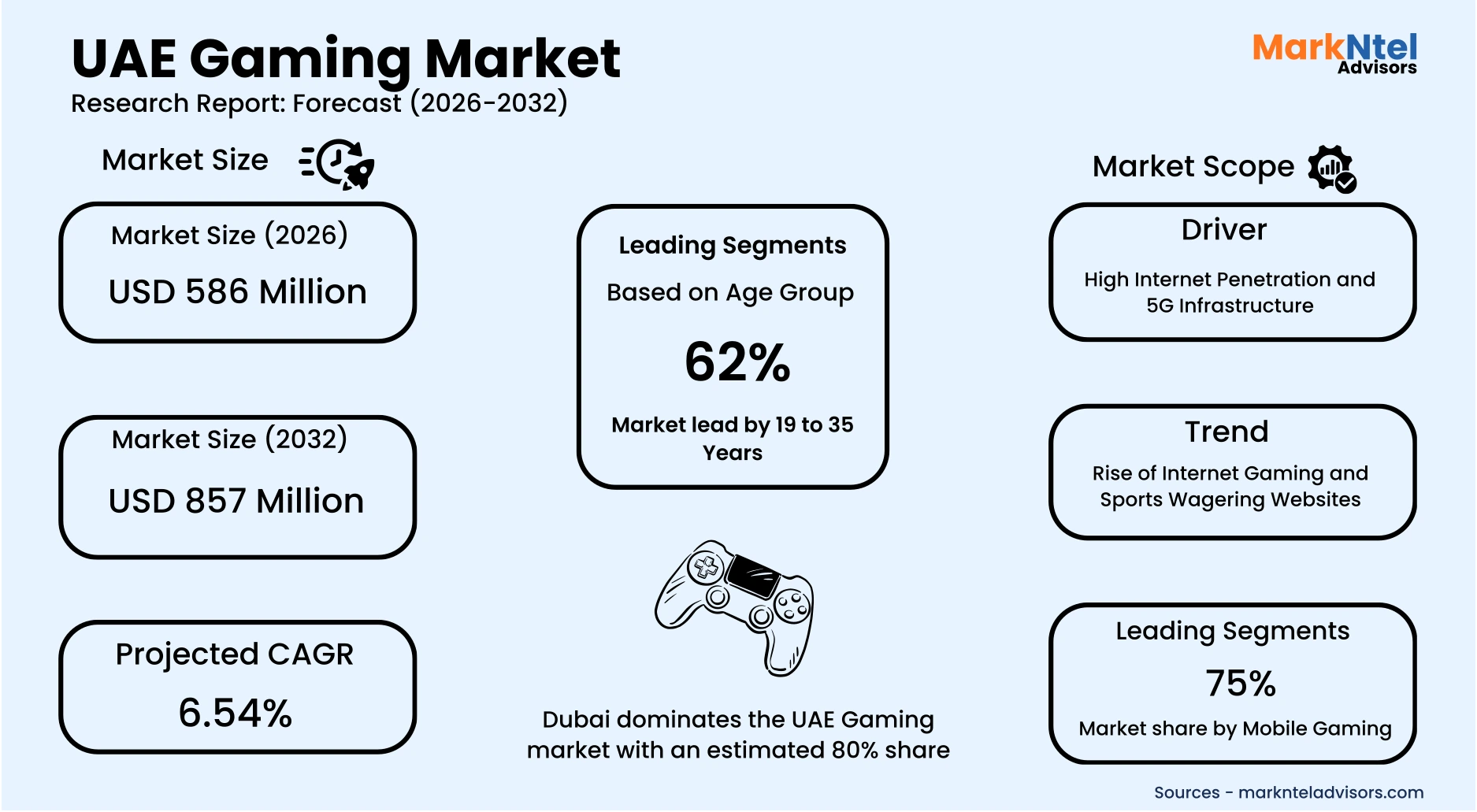

Projected 6.54% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 586 Million

Market Size (2032)

USD 857 Million

Base Year

2025

Projected CAGR

6.54%

Leading Segments

By Age Group: 19 to 35-year

UAE Gaming Market Report Key Takeaways:

- The UAE Gaming market size was valued at USD 550 million in 2025 and is projected to grow from USD 586 million in 2026 to USD 857 million by 2032, exhibiting a CAGR of 6.54% during the forecast period.

- Dubai holds the largest market share of about 80% in the UAE Gaming Market in 2026.

- By device type, the mobile gaming segment represented a significant share of about 75% in the UAE Gaming Market in 2026.

- By platform, the online gaming segment presented a significant share of about 90% in the UAE Gaming Market in 2026.

- By age group, the 19 to 35-year segment presented a significant share of about 62% in the UAE Gaming Market in 2026.

- Leading gaming companies in the UAE Market are Juego Studios Private Limited, Cubix, Exverse Ltd., Big Immersive FZ LLC, Tencent Holdings Ltd., Electronic Arts Inc., Sony Group Corporation, Microsoft Corporation, Apple Inc., Google LLC, NetEase Inc., Ubisoft Entertainment, Activision Blizzard, Roblox Corporation, and Others.

Market Insights & Analysis: UAE Gaming Market (2026-32):

The UAE Gaming Market size was valued at approximately USD 550 million in 2025 and is projected to grow from USD 586 million in 2026 to USD 857 million by 2032. Along with this, the market is estimated to grow at a CAGR of around 6.54% during the forecast period, i.e., 2026-32.

The UAE Gaming Market is projected to expand steadily, driven by widespread high-speed internet and 5G adoption, alongside the expansion of regulated online gaming and sports wagering platforms across the country.

The country has consistently ranked first worldwide in Fibre-to-the-Home (FTTH) penetration, reaching 99.3% coverage, according to the FTTH Council. This marks the eighth consecutive year of global leadership and reflects near-universal access to high-speed fixed broadband. Such extensive fibre deployment ensures ultra-low latency, high bandwidth reliability, and stable connectivity critical technical requirements for competitive multiplayer gaming, real-time streaming, and cloud-based platforms.

In the mobile segment, the UAE also ranked first globally in 5G network speeds, recording median download speeds exceeding 557.63 Mbps. By late 2023, 5G coverage had reached approximately 97–98% of the population, including major cities and key highway corridors. This high level of coverage enables seamless mobile gaming, high-definition live streaming, and participation in large-scale esports tournaments without performance constraints.

Connectivity development extends nationwide. For example, the UAE’s fibre infrastructure now spans more than 14.5 million kilometers, connecting 2.88 million homes across all Emirates. Moreover, by mid-2024, the country reported approximately 21.1 million active mobile subscriptions in a population of around 10 million, equating to a mobile penetration of nearly 200% . This high device density significantly expands the addressable market for mobile-first and cloud-enabled gaming services.

Regulatory modernization is progressing alongside infrastructure readiness. The structured expansion of licensed online gaming and sports wagering platforms demonstrates the establishment of formal oversight, enhanced consumer protection standards, and transparent licensing mechanisms. This controlled regulatory environment increases investor confidence and facilitates the entry of international operators while maintaining compliance and responsible participation.

Looking ahead, future spectrum investments are expected to further strengthen network capacity. The UAE has allocated the 600 MHz and 6 GHz frequency bands, planned for operational rollout during 2025–2026, to support advanced mobile communications and prepare for next-generation applications.

Additionally, the Telecommunications and Digital Government Regulatory Authority has unveiled a national 6G roadmap targeting deployment around 2030, alongside ongoing investments in submarine cable systems to enhance international bandwidth resilience and reduce latency .

The UAE’s combination of near-universal fiber penetration, global 5G speed leadership, expanding spectrum capacity, and evolving regulatory frameworks establishes a highly resilient and future-ready digital ecosystem. These structural advantages are expected to sustain long-term expansion of high-performance gaming, cloud platforms, and immersive digital entertainment across the country.

UAE Gaming Market Recent Developments:

- 2025: Grand Theft Auto V (GTA 5) was officially released in the UAE, twelve years after its global debut, following approval under the region’s updated regulatory framework. The title carries a 21+ age rating, reflecting new content standards established by local authorities to govern mature game distribution.

- 2025: The UAE Lottery introduced a new daily draw game called Pick 4, expanding its portfolio of regulated gaming offerings. The launch aims to enhance player engagement and diversify entertainment options within the federally authorized lottery framework, aligning with broader efforts to modernize and expand the UAE’s licensed gaming ecosystem.

UAE Gaming Market Scope:

| Category | Segments |

|---|---|

| By Type | (Normal Gaming, Esports Gaming), |

| By Device Type | (Mobile Gaming, PC Gaming, Console Gaming), |

| By Platform | (Online Gaming, Offline Gaming), |

| By Game Genre | (Action & Adventure, Sports & Racing, Strategy, Role-Playing, Casual & Puzzle, Shooter, Simulation, Others), |

| By Players Engaged | (Single Player, Multi-Player), |

| By Age Group | (Upto 18 Years, 19 to 35 Years, Above 35 Years), |

| By Player Type | (Male Gamers, Female Gamers), |

| By Technology | (Cloud Gaming, VR / AR Gaming, Blockchain / Web3 Gaming, Social Gaming, iGaming & Online Betting), |

| By Revenue Model | (In-Game Purchases, Game Purchases, Advertising Revenue, Subscriptions, Sponsorship & Media Rights), |

UAE Gaming Market Driver:

High Internet Penetration and 5G Infrastructure

The UAE’s gaming market is fundamentally supported by universal digital access and advanced telecommunications infrastructure, creating an exceptionally strong foundation for online and cloud-based gaming growth. According to World Bank development indicators, 100% of the UAE population was using the internet in 2024, reflecting complete digital penetration and a fully connected consumer base. This universal access eliminates entry barriers for online multiplayer platforms, esports participation, and digital content distribution, significantly strengthening demand potential across demographics.

Mobile infrastructure further reinforces this advantage. The UAE has achieved 100% mobile network coverage, alongside approximately 97% 5G coverage across populated areas, positioning the country among the world’s most digitally connected economies . High-speed 5G connectivity supports ultra-low latency performance, enabling seamless real-time gameplay, cloud streaming, and cross-device gaming experiences critical for competitive and immersive environments.

The country’s forward-looking approach is evident in its investment in next-generation technologies. In 2025, the UAE conducted the Middle East’s first 6G trial, achieving peak speeds of 145 Gbps in collaboration with New York University Abu Dhabi. This milestone highlights preparedness for bandwidth-intensive applications such as advanced cloud gaming, AI-driven interactive platforms, and immersive virtual environments.

Near-universal internet access, comprehensive 5G deployment, and early-stage 6G experimentation collectively position the UAE as a highly future-ready gaming market. This robust connectivity ecosystem is expected to sustain long-term expansion and technological advancement across the sector.

UAE Gaming Market Trend:

Rise of Internet Gaming and Sports Wagering Websites

The UAE gaming sector is entering a new regulatory phase as the country transitions from strict prohibition toward a controlled and licensed commercial gaming ecosystem. A pivotal milestone occurred in 2023 with the establishment of the General Commercial Gaming Regulatory Authority (GCGRA), the UAE’s first federal body tasked with overseeing commercial gaming, online betting, and lotteries. The authority was created to ensure strong governance, responsible gaming practices, and consumer protection while supporting the nation’s broader economic diversification and tourism strategies.

The creation of a centralized regulator has laid the foundation for a transparent licensing framework that can attract international operators and create a structured digital wagering environment. This policy shift reflects the UAE’s long-term strategy to expand entertainment offerings and develop new non-oil revenue streams through regulated gaming.

Momentum accelerated in 2025 when the GCGRA issued the first license for an internet gaming and sports wagering platform, Play971, officially introducing regulated online betting and casino-style gaming services in the UAE. This landmark licensing marks the beginning of a formal digital wagering ecosystem governed by compliance standards and consumer safeguards.

The creation of a national regulator and the licensing of the first online wagering platform signal a major policy transformation. As the regulatory framework expands, the UAE is expected to attract global gaming operators and unlock new digital revenue streams, significantly accelerating the long-term growth of the UAE gaming market.

UAE Gaming Market Opportunity:

Gaming Tourism and Mega-Events

The UAE is increasingly leveraging esports festivals and international gaming events to strengthen its position as a global gaming tourism hub. Large-scale gaming festivals are evolving into powerful drivers of visitor spending, international participation, and cross-industry revenue generation across hospitality, retail, and entertainment. A strong example is the Dubai Esports and Games Festival (DEF), which has emerged as a flagship initiative supporting Dubai’s digital economy and tourism ambitions.

In 2024, the festival attracted over0,000 visitors across a 17-day programme and awarded more than USD 54,000 in prize money. The event demonstrated growing public engagement and the ability of gaming festivals to generate visitor traffic and local economic activity.

Momentum accelerated further in 2025, when the festival expanded significantly, engaging 3.8 million gamers across 90+ tournaments, showcasing 130+ game titles, and distributing USD 190,000 in prizes. The event also brought together 2,000 industry professionals from 70 countries, reinforcing the UAE’s growing role as an international esports and gaming destination .

The rapid expansion of gaming festivals and global participation signals strong long-term tourism potential. As event scale and international visibility continue to grow, gaming tourism is set to become a key catalyst for sustained revenue growth in the UAE gaming market.

UAE Gaming Market Challenge:

Talent and Development Ecosystem Gaps

Despite strong policy support and rising investment, the UAE gaming market faces structural constraints linked to talent availability and ecosystem depth. Under the Dubai Future Foundation’s Dubai Program for Gaming 2033, authorities reported that Dubai hosts more than 350 gaming-related companies, of which only around 260 are game development studios (2025). This highlights a relatively limited base of core development entities compared to the sector’s expansion ambitions.

To address ecosystem gaps, the government announced the formation of a dedicated gaming committee in 2024 to support professional development and attract global expertise. However, broader labor market data underscores the scale of the challenge. According to national workforce projections cited in 2025, the UAE will need to add approximately 1 million workers by 2030 to meet digital economy demands, including AI, software engineering, and advanced technical roles critical to gaming development.

Without accelerated talent development and deeper localization of production capabilities, the UAE gaming market may face constraints in scaling indigenous content creation. Persistent skill gaps could slow innovation, increase operational costs, and moderate long-term market competitiveness.

UAE Gaming Market (2026-32) Segmentation Analysis:

The UAE Gaming Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the country level. Based on the analysis, the market has been further classified as;

Based on Device Type:

- Mobile Gaming

- PC Gaming

- Console Gaming

The mobile gaming segment dominates the UAE Gaming market, accounting for approximately 75% of the market size, driven by advanced digital infrastructure and widespread smartphone adoption.

The UAE consistently ranks among the highest globally in mobile and internet penetration, supported by nationwide 5G deployment and high-speed fiber connectivity. This technological foundation enables seamless gameplay, low latency, and efficient in-app transactions, reducing the need for dedicated gaming hardware such as consoles or high-specification PCs.

The market’s demographic structure further strengthens mobile gaming leadership. A young, digitally connected population with high disposable income demonstrates strong engagement with multiplayer, competitive, and socially integrated mobile titles. The accessibility of smartphones lowers entry barriers, allowing both casual and core gamers to participate without significant upfront investment.

Moreover, mobile esports tournaments and gaming festivals increasingly feature smartphone-based titles, reinforcing competitive gaming culture and expanding audience reach. Integration with digital wallets and secure online payment systems also supports monetization growth.

Given continuous advancements in 5G infrastructure, cloud integration, and device performance, mobile gaming is expected to retain its dominant position. Its scalability, cost efficiency, and infrastructure compatibility make it the primary engine of user acquisition and revenue expansion within the UAE gaming ecosystem.

Based on Age Group:

- Upto 18 Years

- 19 to 35 Years

- Above 35 Years

The 19 to 35-year segment dominates the UAE Gaming market, accounting for about 62% of the total market size, primarily due to its high digital engagement, economic participation, and strong alignment with emerging gaming formats. This cohort represents a substantial share of the country’s working-age and university population, characterized by advanced technological literacy and consistent access to high-speed connectivity and smart devices.

Individuals within this age group demonstrate strong adoption of console, PC, and mobile gaming platforms, as well as growing interest in cloud-based and cross-platform experiences. Their familiarity with digital ecosystems enables higher participation in online multiplayer games, esports tournaments, live-streamed gaming content, and subscription-based gaming services.

Unlike younger age groups, this segment typically possesses independent income, enabling discretionary spending on premium game titles, in-game purchases, hardware upgrades, and gaming accessories.

Moreover, gaming for this demographic extends beyond entertainment to include social interaction, competitive engagement, and community participation. The integration of gaming with digital payments, streaming platforms, and immersive technologies further strengthens their spending intensity and engagement levels.

Given their purchasing power, platform diversity, and adaptability to evolving gaming technologies, the 19–35 segment remains the principal revenue contributor. Their sustained demand for innovative, competitive, and socially connected gaming experiences positions them as the core driver of long-term market expansion in the UAE gaming industry.

UAE Gaming Market (2026-32): Regional Projection

Dubai dominates the UAE Gaming market with an estimated 80% share, driven by structured policy intervention, infrastructure readiness, and long-term economic planning. A defining milestone was the launch of the Dubai Future Foundation’s Dubai Program for Gaming 2033, a strategic initiative designed to position Dubai among the world’s leading gaming hubs. The program reflects a clear economic vision to increase the gaming sector’s contribution to Dubai’s GDP by USD 1 billion and generate 30,000 new jobs by 2033.

This initiative goes beyond promotional support and focuses on ecosystem building, attracting international gaming studios, nurturing startups, strengthening digital infrastructure, and expanding talent development pathways. By integrating gaming into the broader digital economy and innovation agenda, Dubai is aligning the sector with future-facing industries such as AI, Web3, and immersive technologies.

The scale of employment targets and GDP contribution underscores Dubai’s long-term commitment to institutionalizing gaming as a core creative and technology industry rather than a niche entertainment segment.

Through structured investment, job creation targets, and GDP-linked outcomes, Dubai has positioned itself as the central growth engine of the UAE gaming market. This proactive strategy strengthens its competitive edge and reinforces its leadership within the regional gaming landscape.

Gain a Competitive Edge with Our UAE Gaming Market Report:

- UAE Gaming Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- UAE Gaming Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- UAE Gaming Market Policies, Regulations, and Product Standards

- UAE Gaming Market Trends & Developments

- UAE Gaming Market Dynamics

- Growth Factors

- Challenges

- UAE Gaming Market Hotspot & Opportunities

- UAE Gaming Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Type- Market Size & Forecast 2022-2032, USD Million

- Normal Gaming

- Esports Gaming

- By Device Type- Market Size & Forecast 2022-2032, USD Million

- Mobile Gaming

- PC Gaming

- Console Gaming

- By Platform - Market Size & Forecast 2022-2032, USD Million

- Online Gaming

- Offline Gaming

- By Game Genre- Market Size & Forecast 2022-2032, USD Million

- Action & Adventure

- Sports & Racing

- Strategy

- Role-Playing

- Casual & Puzzle

- Shooter

- Simulation

- Others

- By Players Engaged- Market Size & Forecast 2022-2032, USD Million

- Single Player

- Multi-Player

- By Age Group- Market Size & Forecast 2022-2032, USD Million

- Upto 18 Years

- 19 to 35 Years

- Above 35 Years

- By Player Type- Market Size & Forecast 2022-2032, USD Million

- Male Gamers

- Female Gamers

- By Technology - Market Size & Forecast 2022-2032, USD Million

- Cloud Gaming

- VR / AR Gaming

- Blockchain / Web3 Gaming

- Social Gaming

- iGaming & Online Betting

- By Revenue Model- Market Size & Forecast 2022-2032, USD Million

- In-Game Purchases

- Game Purchases

- Advertising Revenue

- Subscriptions

- Sponsorship & Media Rights

- By Region - Market Size & Forecast 2022-2032, USD Million

- Abu Dhabi & Al Ain

- Dubai

- Sharjah & Northern Emirates

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Mobile Gaming Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Device Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Game Genre- Market Size & Forecast 2022-2032, USD Million

- By Players Engaged- Market Size & Forecast 2022-2032, USD Million

- By Age Group- Market Size & Forecast 2022-2032, USD Million

- By Player Type- Market Size & Forecast 2022-2032, USD Million

- By Technology - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE PC Gaming Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Device Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Game Genre- Market Size & Forecast 2022-2032, USD Million

- By Players Engaged- Market Size & Forecast 2022-2032, USD Million

- By Age Group- Market Size & Forecast 2022-2032, USD Million

- By Player Type- Market Size & Forecast 2022-2032, USD Million

- By Technology - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Console Gaming Market Outlook, 2022-2032

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Outlook

- By Device Type- Market Size & Forecast 2022-2032, USD Million

- By Platform - Market Size & Forecast 2022-2032, USD Million

- By Game Genre- Market Size & Forecast 2022-2032, USD Million

- By Players Engaged- Market Size & Forecast 2022-2032, USD Million

- By Age Group- Market Size & Forecast 2022-2032, USD Million

- By Player Type- Market Size & Forecast 2022-2032, USD Million

- By Technology - Market Size & Forecast 2022-2032, USD Million

- By Revenue Model- Market Size & Forecast 2022-2032, USD Million

- By Region - Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- UAE Gaming Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Juego Studios Private Limited

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Cubix

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Exverse Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Big Immersive FZ LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Tencent Holdings Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Electronic Arts Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Sony Group Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Microsoft Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Apple Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Google LLC

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- NetEase Inc.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ubisoft Entertainment

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Activision Blizzard

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Roblox Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Juego Studios Private Limited

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now