Spain OTC Drugs Market Research Report: Size, Share, Trends & Forecast (2026-2032)

By Product Type (Analgesics, Cold & Cough Remedies, Digestive & Intestinal Remedies, Skin Treatment, Vitamins & Minerals, Hand Sanitizers, Eye Care), By Distribution Channel (Pharm ... acies/Drugstores, Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Others), By End User (Commercial, Non-Commercial), and others Read more

- Healthcare

- Feb 2026

- Pages 120

- Report Format: PDF, Excel, PPT

Spain OTC Drugs Market

Projected 5.24% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 2.31 billion

Market Size (2032)

USD 2.94 billion

Base Year

2025

Projected CAGR

5.24%

Leading Segments

By Product Type: Cold & Cough Remedies

Spain OTC Drugs Market Report Key Takeaways:

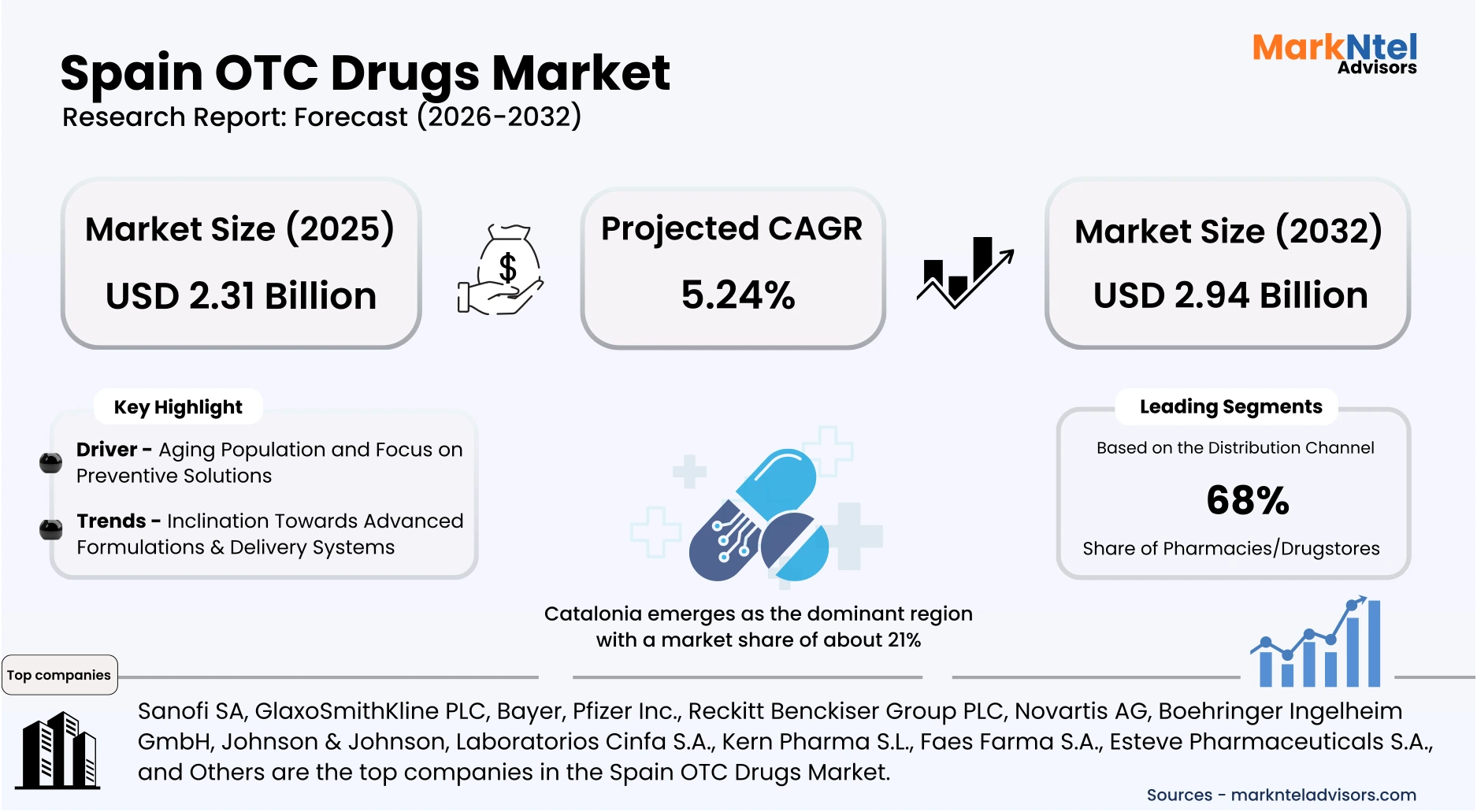

- Market size was valued at around USD2.31 billion in 2025 and is projected to reach USD2.94 billion by 2032. The estimated CAGR from 2026 to 2032 is around 5.24%, indicating strong growth.

- The Catalonia region holds the largest market share of about 21% in the Spain OTC Drugs Market in 2025.

- By Product Type, the Cold and Cough Remedies segment represented a significant share of about 32% in the Spain OTC Drugs Market in 2025.

- By Distribution Channel, the Pharmacies & drugstores segment presented a significant share of about 68% in the Spain OTC Drugs Market in 2025.

- Leading OTC Drugs Companies in the Spain Market are Sanofi SA, GlaxoSmithKline PLC, Bayer, Pfizer Inc., Reckitt Benckiser Group PLC, Novartis AG, Boehringer Ingelheim GmbH, Johnson & Johnson, Laboratorios Cinfa S.A., Kern Pharma S.L., Faes Farma S.A., Esteve Pharmaceuticals S.A., and Others.

Market Insights & Analysis: Spain OTC Drugs Market (2026-32):

The Spain OTC Drugs Market size is valued at around USD2.31 billion in 2025 and is projected to reach USD2.94 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 5.24% during the forecast period, i.e., 2026-32.

The Spain OTC Drugs Market continues to evolve steadily, supported by strong healthcare infrastructure, expanding consumer awareness, and the growing preference for self-medication. Pharmacies remain the primary distribution channel, as Spanish law permits non-prescription medicine sales mainly through authorized outlets. According to the Spanish Ministry of Health (Ministerio de Sanidad), the value of pharmacy-led OTC sales reaches several billion dollars each year, reflecting the high level of consumer trust in professional guidance and product safety. The country’s pharmaceutical base is also a major growth driver.

Moreover, Catalonia stands out as Spain’s leading production hub, accounting for nearly half of the national drug manufacturing capacity. It contributes tens of billions of dollars annually to the overall pharmaceutical output, while Madrid remains a key center for corporate, regulatory, and healthcare operations, sustaining strong domestic demand for OTC products.

Furthermore, seasonal changes play an important role in shaping market dynamics. During winter, cases of flu and respiratory infections rise sharply, boosting sales of cold, cough, and flu remedies. However, once the season passes, demand tends to fall, creating inventory and supply challenges for pharmacies and manufacturers. Looking ahead, the market is expected to remain resilient, supported by rising health consciousness, the expansion of online pharmacy services under strict regulations, and continuous innovation in vitamins, analgesics, and self-care solutions. Spain’s OTC industry thus reflects a mature, regulated, and consumer-trusted healthcare environment poised for long-term, stable revenue growth.

Spain OTC Drugs Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Analgesics, Cold & Cough Remedies, Digestive & Intestinal Remedies, Skin Treatment, Vitamins & Minerals, Hand Sanitizers, Eye Care), |

| By Distribution Channel | (Pharmacies/Drugstores, Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Others), |

| By End User | (Commercial, Non-Commercial), |

Spain OTC Drugs Market Driver:

Aging Population and Focus on Preventive Solutions

Spain’s aging population has become one of the most influential drivers of the OTC drugs market. According to Eurostat (2024), more than 20% of Spain’s population is aged 65 years or older, placing it among the oldest societies in the European Union. This demographic change has created rising demand for self-care and preventive health products, as elderly consumers increasingly prefer non-prescription medicines to manage mild or recurring conditions such as joint pain, digestive issues, colds, or sleep disturbances.

The Spanish Ministry of Health (Ministerio de Sanidad) continues to promote preventive healthcare and responsible self-medication to reduce pressure on the public healthcare system. This aligns with older individuals’ growing interest in maintaining independence and managing chronic symptoms safely at home. As a result, OTC categories such as pain relievers, vitamins, and digestive remedies have seen steady year-round demand. The combination of an aging society and a preventive-care mindset, therefore, remains a structural and long-term growth driver for Spain’s OTC Drugs Market.

Rising Investments Strengthening Spain’s OTC Drugs Market

Rising domestic and international investments are one of the strongest drivers of Spain’s OTC drugs industry, reinforcing its industrial and innovation capacity. According to the Spanish Federation of Pharmaceutical Industries (Farmaindustria), the country’s pharmaceutical sector has attracted investments exceeding USD9.7 billion over the past three years, reflecting growing confidence in Spain’s healthcare ecosystem . The government’s Pharmaceutical Industry Strategy 2024-28 aims to modernize production facilities, strengthen local supply chains, and expand R&D focused on self-care and preventive health products. Major global firms such as Bayer, Sanofi, and Cinfa have recently expanded or upgraded plants across Catalonia and Navarra, improving OTC production efficiency, thus driving the market size & volume.

Spain OTC Drugs Market Trend:

Inclination Towards Advanced Formulations & Delivery Systems

In this market, the adoption of advanced formulations and delivery systems is rapidly gaining importance. For reference, Bayer AG announced in 2023 that it had invested approximately USD166 million to boost production capacity in Spain for soft-gel capsules used in analgesic, digestive, and dermatological OTC/consumer-health products. These soft-gel capsules offer improved bioavailability and faster symptom relief compared with standard tablets.

Meanwhile, Spain continues to regulate the online sale of non-prescription medicines through licensed pharmacies under Royal Decree 870/2013, which helps the safe adoption of newer formulations in digital channels. As consumers in Spain increasingly seek convenient, rapid-acting self-care solutions, companies are responding with innovations such as orodispersible tablets, combination therapy formats, and once-daily soft-gel capsules. This trend not only enhances user experience but also strengthens the OTC self-medication ecosystem in Spain.

Growth of Natural, Herbal, and Clean-Label OTC Products

The rising demand for natural, herbal, and clean-label OTC products is transforming Spain’s over-the-counter drug industry. Consumers are increasingly choosing plant-based medicines and supplements that are perceived as safer, more sustainable, and aligned with preventive health habits. The Spanish Agency for Medicines and Health Products (AEMPS) has also established clear regulations for traditional herbal medicines, ensuring product safety and quality.

Pharmacies, which account for nearly three-quarters of supplement and herbal product sales in Spain, now dedicate more space to plant-based cough syrups, digestive aids, and immunity boosters. This strong preference for natural and clean-label products is positively reshaping Spain’s OTC drugs market, combining wellness, sustainability, and consumer confidence into a long-term growth trend.

Spain OTC Drugs Market Challenge:

Seasonal Nature of Demand Hindering Market Growth

A major challenge in Spain’s OTC Drugs Industry is the sharp decline in demand for cold, cough, and flu products after seasonal peaks. According to data from the Instituto de Salud Carlos III (ISCIII), weekly influenza incidence during the 2023–24 winter season reached over 380 cases per 100,000 inhabitants, but dropped by a significant fraction by late spring. This steep fall directly impacts pharmacy sales, especially for decongestants, lozenges, and fever medicines, leading to excess inventory and reduced cash flow in off-season months. Pharmacies often struggle to manage shelf life and storage costs for unsold stock, since most OTC respiratory products have fixed expiry dates.

Additionally, manufacturers face production slowdowns and forecasting difficulties, as demand fluctuates sharply within a few months each year. The imbalance between high winter demand and low summer sales thus creates significant operational inefficiencies and financial strain across Spain’s OTC distribution chain.

Spain OTC Drugs Market (2026-32) Segmentation Analysis:

The Spain OTC Drugs Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the Spain level. Based on the analysis, the market has been further classified as;

Based on Product Type

- Analgesics

- Cold & Cough Remedies

- Digestive & Intestinal Remedies

- Skin Treatment

- Vitamins & Minerals

- Hand Sanitizers

- Eye Care

- Others (Sleep Aids, Wound Care, etc.)

The Cold & Cough Remedies segment holds a dominant position in Spain’s OTC drugs industry by holding a market share of about 32% due to the country’s high seasonal incidence of respiratory infections and growing self-medication culture. Respiratory tract infections remain among the top causes for outpatient consultations each winter, ranging from 3 to 5 million reported influenza-like illness cases annually . Similarly, the Instituto de Salud Carlos III notes frequent surges in common cold and flu cases during winter peaks, driving strong pharmacy sales of decongestants, antihistamines, and throat lozenges.

Additionally, Spain’s easy pharmacy access and awareness campaigns promoting self-care contribute to the high demand for OTC cold and cough medications. The segment’s consistent year-round consumption, especially during flu seasons, makes it a core revenue contributor in Spain’s OTC drugs market, surpassing other categories such as digestive or skin-care treatments in overall sales.

Based on the Distribution Channel

- Pharmacies/Drugstores

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Others

Pharmacies & drugstores are the leading distribution channels in Spain’s OTC Drugs Market, holding a market share of about 68%, driven by strong regulation, accessibility, and consumer trust. For instance, Spain has around 22,000 registered pharmacies, giving it one of the highest pharmacy densities in Europe. Spanish law allows the sale of most OTC medicines only through licensed pharmacies, ensuring product safety and professional supervision.

Pharmacies also play a key advisory role, guiding consumers in self-medication and proper drug use. Although online platforms and supermarkets are slowly expanding, their share remains limited due to regulatory restrictions and consumer preference for professional service. Therefore, pharmacies clearly dominate Spain’s OTC market, combining legal authority, accessibility, and public confidence.

Spain OTC Drugs Market (2026-32): Regional Projection

- In Spain’s OTC Drugs Market, Catalonia emerges as the dominant region with a market share of about 21% due to its strong pharmaceutical manufacturing base, advanced research infrastructure, and export capacity. According to the Spanish Ministry of Industry, Trade and Tourism and Farmaindustria, Catalonia hosts over 45% of Spain’s pharmaceutical production units, with around 79 of the country’s 173 manufacturing plants located there. The region contributes nearly one-third of Spain’s total pharmaceutical turnover, driven by its biotechnology and chemical hubs in Barcelona and Tarragona. Additionally, Catalonia accounts for a major share of national pharmaceutical exports and employs the largest share of industry professionals in Spain.

- Consequently, Catalonia’s superior production capacity, strong industrial ecosystem, and consistent R&D investment make it the leading regional contributor to Spain’s OTC drugs manufacturing and supply network.

Gain a Competitive Edge with Our Spain OTC Drugs Market Report

- Spain OTC Drugs Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Spain OTC Drugs Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Spain OTC Drugs Market Regulations, Policies & Standards

- Spain OTC Drugs Market Trends & Developments

- Spain OTC Drugs Market Pricing Analysis

- Spain OTC Drugs Market Strategic Insights

- Spain OTC Drugs Market Dynamics

- Growth Drivers

- Challenges

- Spain OTC Drugs Market Hotspots & Opportunities

- Spain OTC Drugs Market Value Chain Analysis

- Spain OTC Drugs Market Outlook, 2022- 2032F

- Market Size & Analysis

- Market Revenues (USD Million)

- Market Share & Analysis

- By Product Type

- Analgesics- Market Size & Forecast 2022-2032, USD Million

- Cold & Cough Remedies- Market Size & Forecast 2022-2032, USD Million

- Digestive & Intestinal Remedies- Market Size & Forecast 2022-2032, USD Million

- Skin Treatment- Market Size & Forecast 2022-2032, USD Million

- Vitamins & Minerals- Market Size & Forecast 2022-2032, USD Million

- Hand Sanitizers - Market Size & Forecast 2022-2032, USD Million

- Eye Care- Market Size & Forecast 2022-2032, USD Million

- Others (Sleep Aids, Wound Care, etc.)- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel

- Pharmacies/Drugstores- Market Size & Forecast 2022-2032, USD Million

- Supermarkets/Hypermarkets- Market Size & Forecast 2022-2032, USD Million

- Convenience Stores- Market Size & Forecast 2022-2032, USD Million

- Online Retail- Market Size & Forecast 2022-2032, USD Million

- Others- Market Size & Forecast 2022-2032, USD Million

- By End User

- Commercial- Market Size & Forecast 2022-2032, USD Million

- Non-Commercial- Market Size & Forecast 2022-2032, USD Million

- By Region

- Andalusia

- Catalonia

- Madrid

- Valencia

- Galicia

- Castile and León

- Basque Country

- Canary Islands

- Rest of Spain

- By Competitors

- Competition Characteristics

- Market Share & Analysis

- By Product Type

- Market Size & Analysis

- Spain Commercial OTC Drugs Market Outlook, 2022- 2032F

- Market Size & Analysis

- Market Revenues (USD Million)

- Market Share & Analysis

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Spain Non-Commercial OTC Drugs Market Outlook, 2022- 2032F

- Market Size & Analysis

- Market Revenues (USD Million)

- Market Share & Analysis

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By End User- Market Size & Forecast 2022-2032, USD Million

- Market Size & Analysis

- Spain OTC Drugs Market Key Strategic Imperatives for Growth & Success

- Competitive Outlook

- Company Profiles

- Sanofi SA

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- GlaxoSmithKline PLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Bayer

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Pfizer Inc.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Reckitt Benckiser Group PLC

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Novartis AG

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Boehringer Ingelheim GmbH

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Johnson & Johnson

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Laboratorios Cinfa S.A.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Kern Pharma S.L.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Faes Farma S.A.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Esteve Pharmaceuticals S.A.

- Business Description

- Product Portfolio

- Strategic Alliances or Partnerships

- Recent Developments

- Financial Details

- Others

- Others

- Sanofi SA

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now