Southeast Asia Warehouse Automation Market Research Report: Forecast (2026-2032)

Southeast Asia Warehouse Automation Market - By Component (Hardware, Software, Services), By Automation Type (Automated Storage and Retrieval Systems (AS/RS), Autonomous Mobile Rob ... ots (AMRs), Automated Guided Vehicles (AGVs), Conveyor & Sortation Systems, Robotic Picking & Palletizing, Automated Packing & Labeling, Warehouse Management Systems (WMS / WES / WCS), Automated Identification Systems (RFID / Barcode / Vision), Automated Packaging Systems, Drones & Vision Inspection Automation), By End-Use Industry (Retail & E-commerce, Logistics Service Providers (3PL / 4PL), Manufacturing, Food & Beverage, Healthcare & Pharmaceuticals, Automotive & Industrial, Electronics & High-Tech, Cold Chain Specialists, Government / Defense Logistics, Warehouse Property Developers), and others Read more

- Buildings, Construction, Metals & Mining

- Feb 2026

- Pages 165

- Report Format: PDF, Excel, PPT

Southeast Asia Warehouse Automation Market

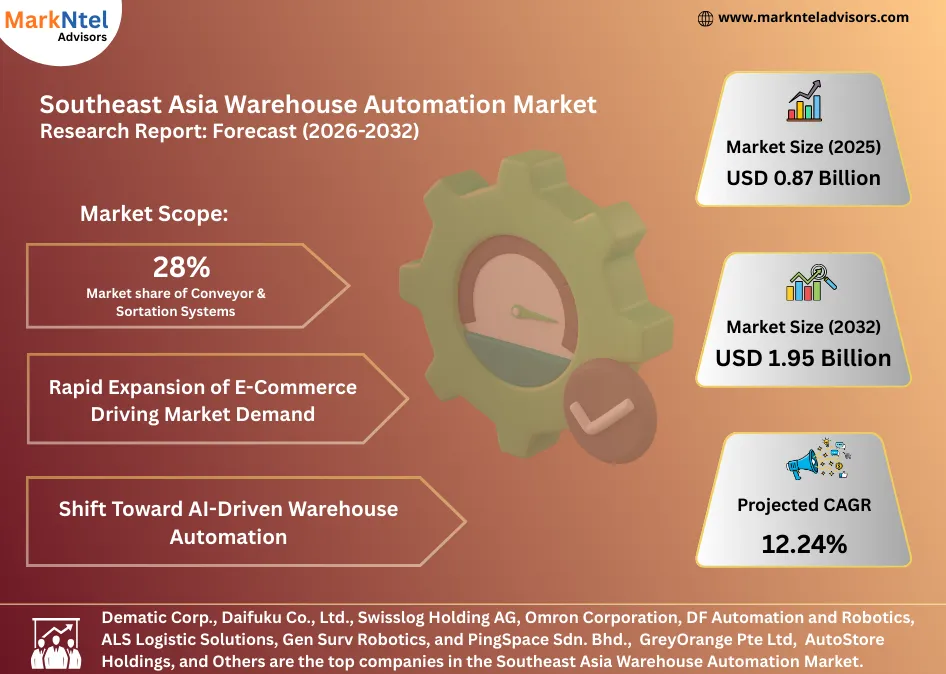

Projected 12.24% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2025)

USD 0.87 Billion

Market Size (2032)

USD 1.95 Billion

Base Year

2025

Projected CAGR

12.24%

Leading Segments

By Automation Type: Conveyor & Sortation Systems

Southeast Asia Warehouse Automation Market Report Key Takeaways:

- Market size was valued at around USD 0.87 billion in 2025 and is projected to reach USD 1.95 billion by 2032. The estimated CAGR from 2026 to 2032 is around 12.24%, indicating strong growth.

- Indonesia holds the largest market share of about 30% in the Southeast Asia Warehouse Automation Market in 2025.

- By Automation Type, the Conveyor & Sortation Systems segment represented a significant share of about 28% in the Southeast Asia Warehouse Automation Market in 2025.

- By End-Use Industry, the Logistics Service Providers (3PL/4PL) segment seized about 32% share in the Southeast Asia Warehouse Automation Market in 2025.

- Leading Warehouse Automation Companies in the Southeast Asia Market are Sun & Siasun Robot Co., Ltd.., Quicktron, Geek+, Vanderlande Industries, Dematic, Daifuku Co., Ltd., Swisslog Holding AG, Omron Corporation, DF Automation and Robotics, ALS Logistic Solutions, Gen Surv Robotics, PingSpace Sdn. Bhd., System Logistics Asia, GreyOrange, Locus Robotics, HAI Robotics, Honeywell Intelligrated, AutoStore, KNAPP AG, Murata Machinery, Ltd., Toyota Material Handling, KION Group, ABB, Yaskawa Electric Corporation, Godrej Consoveyo Logistics, Toshiba, SSI Schaefer, Honeywell, Siemens, Others,

Market Insights & Analysis: Southeast Asia Warehouse Automation Market (2026-32):

The Southeast Asia Warehouse Automation Market size is valued at approximately USD 0.87 billion in 2025 and is projected to reach USD 1.95 billion by 2032. Along with this, the market is estimated to grow at a CAGR of around 12.24% during the forecast period, i.e., 2026-32.

The market growth reflects a fundamental restructuring of Southeast Asia’s logistics backbone as trade volumes, e-commerce intensity, and manufacturing dispersion expand simultaneously. According to ASEAN Secretariat data, intra-ASEAN merchandise trade exceeded USD3.8 trillion in 2023, with inland logistics parks and urban fulfillment centers.

This volume pressure is being actively converted into automation demand through policy alignment. In the Singapore Budget 2024, the government allocated approximately USD 44 million to the National Robotics Program to accelerate the translation of robotics R&D capabilities into real-world applications in sectors including manufacturing, logistics, and facilities management. Similarly, according to Malaysia’s investment performance data, NIA-aligned approvals totaling USD30.8 billion in the first nine months of 2025 supported technology-driven sectors , including digitalization initiatives and logistics infrastructure essential for automated warehousing and distribution.

Additionally, in 2024, Thailand’s Board of Investment reported the digital sector attracted USD2.5 billion in investment applications, driven by data centers and cloud services projects . As these investments scale, automation economics become increasingly compelling. According to Singapore Economic Development Board data, automated warehouses deliver labor productivity improvements. These quantifiable gains underpin the market trajectory, as automation transitions from optional efficiency enhancement to operational necessity.

Southeast Asia Warehouse Automation Market Recent Developments:

- 2025: Dematic launched its next-generation Silky Crossbelt sorter across Southeast Asia to boost flexible logistics sorting efficiency tailored to regional requirements, supporting the growth of e-commerce and smart fulfillment operations.

- 2025: Daifuku expanded intralogistics innovation in Thailand with locally manufactured AS/RS and automation systems, enhancing storage efficiency and supporting exports to Singapore, Malaysia, and Vietnam.

Southeast Asia Warehouse Automation Market Scope:

| Category | Segments |

|---|---|

| By Component | Hardware, Software, Services |

| By Automation Type | Automated Storage and Retrieval Systems (AS/RS), Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Conveyor & Sortation Systems, Robotic Picking & Palletizing, Automated Packing & Labeling, Warehouse Management Systems (WMS / WES / WCS), Automated Identification Systems (RFID / Barcode / Vision), Automated Packaging Systems, Drones & Vision Inspection Automation |

| By End-Use Industry | Retail & E-commerce, Logistics Service Providers (3PL / 4PL), Manufacturing, Food & Beverage, Healthcare & Pharmaceuticals, Automotive & Industrial, Electronics & High-Tech, Cold Chain Specialists, Government / Defense Logistics, Warehouse Property Developers |

Southeast Asia Warehouse Automation Market Driver:

Rapid Expansion of E-Commerce Driving Market Demand

Rapid growth in e-commerce across Southeast Asia is the most influential driver transforming logistics expansion into sustained warehouse automation investment. Government and institutional data indicate that Southeast Asia now has over 460 million internet users, with e-commerce adoption rising fastest in Indonesia, Malaysia, the Philippines, Vietnam, and Thailand, where online retail participation has expanded sharply since 2023. According to national digital economy assessments, Malaysia and Singapore report e-commerce penetration rates exceeding 70% of internet users, while Vietnam and the Philippines continue to post double-digit annual growth in online buyers, expanding daily order volumes beyond seasonal peaks.

As penetration deepens, fulfilment demand shifts from episodic to continuous. This structural change increases SKU diversity, smaller order sizes, and higher order frequency, placing sustained pressure on warehouse throughput and accuracy. Government logistics agencies in Malaysia and the Philippines have highlighted that rising last-mile volumes are compressing fulfilment timelines, forcing warehouses to process more orders within shorter operational windows. Under these conditions, manual sorting and picking models struggle to scale efficiently, increasing reliance on conveyor-based sortation, automated storage, and software-driven inventory control.

The driver is further amplified by cross-border e-commerce. ASEAN trade facilitation reforms and digital customs platforms have increased small-parcel flows between Singapore, Malaysia, Thailand, and Vietnam, turning regional distribution centres into transhipment-heavy nodes. As delivery commitments tighten across borders, logistics operators increasingly deploy automation to absorb volume growth without proportional labour expansion.

Southeast Asia Warehouse Automation Market Trend:

Shift Toward AI-Driven Warehouse Automation

A major trend shaping Southeast Asia’s warehouse automation market is the move away from fixed, hardware-heavy systems toward AI-orchestrated, software-centric warehousing. Instead of relying on rigid conveyor layouts, warehouses increasingly deploy autonomous mobile robots (AMRs) coordinated by centralized warehouse execution software that dynamically assigns tasks based on real-time order demand and congestion.

This shift accelerated during 2024–2025, as leading automation providers expanded AI-enabled platforms in the region. For instance, GreyOrange scaled deployments of its AI-driven robot orchestration software across Southeast Asian fulfillment centers in 2024 , enabling flexible picking and sorting without structural redesign. Similarly, Locus Robotics expanded its AMR fleet management platform in Asian countries during 2024, allowing warehouses to scale robot fleets up or down based on daily volume fluctuations. HAI Robotics also increased adoption of its goods-to-person robotic systems in Singapore and Malaysia in 2024, integrating AI-based storage optimization. These adoptions are actively increasing the market growth.

Southeast Asia Warehouse Automation Market Opportunity:

Rising Government Incentives

Government incentives & Industry 4.0 grants act as a cohesive, policy-driven growth engine for the Southeast Asia warehouse automation market by directly linking national productivity goals with logistics modernization. Instead of treating warehousing as a downstream activity, governments increasingly position automated intralogistics as a core enabler of industrial competitiveness.

For instance, Singapore integrates warehouse automation into its productivity agenda through Enterprise Singapore’s Enterprise Development Grant, which can co-fund up to 70% of qualifying project costs for automation and digital transformation . This reduces capital intensity for SMEs and encourages early adoption of AS/RS, robotics, and WMS platforms within distribution centers supporting manufacturing and trade.

Similarly, Thailand aligns logistics automation with its Thailand 4.0 strategy. For instance, the Thailand Board of Investment offers corporate income tax exemptions of up to eight years for automation and smart-factory projects, motivating manufacturers and 3PLs to integrate automated warehousing alongside production upgrades. Likewise, Malaysia’s Industry4WRD policy provides automation grants and tax allowances that explicitly recognize intralogistics efficiency as a productivity multiplier.

Additionally, Indonesia’s Making Indonesia 4.0 roadmap includes super-deduction tax incentives of up to 300% for technology training and R&D, strengthening the skills and systems needed to operate automated warehouses. Collectively, these coordinated incentives lower adoption barriers, accelerate ROI, and structurally expand demand for warehouse automation across Southeast Asia.

Southeast Asia Warehouse Automation Market Challenge:

High Upfront Costs Hindering Market Growth

Market growth is hindered by the high upfront capital requirement, which disproportionately affects small and mid-sized logistics operators. Deploying warehouse automation is not limited to purchasing equipment; it requires simultaneous investment in automated storage systems, conveyor and sortation lines, robotics, warehouse execution software, and supporting electrical and IT infrastructure. Warehouse automation costs vary widely. Basic systems can start around USD50,000, while larger, integrated systems for storage, robotics, and conveyors can reach into the millions of dollars, reflecting substantial upfront capital investment.

This cost pressure is intensified by the structure of Southeast Asia’s logistics sector, where a large share of operators is asset-light and margin-sensitive. Government logistics reviews from Indonesia, Vietnam, and the Philippines highlight that many warehouses were originally designed for manual handling, making automation retrofits technically complex and financially demanding. As a result, automation projects often require longer commissioning periods and higher contingency budgets, increasing financial risk.

Southeast Asia Warehouse Automation Market (2026-32) Segmentation Analysis:

The Southeast Asia Warehouse Automation Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as;

Based on Automation Type:

- Automated Storage and Retrieval Systems (AS/RS)

- Autonomous Mobile Robots (AMRs)

- Automated Guided Vehicles (AGVs)

- Conveyor & Sortation Systems

- Robotic Picking & Palletizing

- Automated Packing & Labeling

- Warehouse Management Systems (WMS / WES / WCS)

- Automated Identification Systems (RFID / Barcode / Vision)

- Automated Packaging Systems

- Drones & Vision Inspection Automation

Conveyor & Sortation Systems dominate this market with a market share of about 28% because they directly address the region’s parcel intensity, hub-and-spoke logistics model, and port-centric trade flows, where fast, rule-based sorting is mission-critical. For instance, Southeast Asia’s e-commerce and express-parcel networks generate extremely high daily parcel volumes that must be sorted within tight cut-off windows.

In Singapore, the Infocomm Media Development Authority and SingPost have highlighted large-scale deployment of automated parcel sorters to handle rising cross-border and domestic deliveries efficiently, reflecting the centrality of conveyor-based sortation in national logistics infrastructure. Similarly, Indonesia’s state postal and courier operators have expanded automated sorting lines to manage surging last-mile and inter-island parcel flows, where manual handling is no longer viable.

Moreover, export and port-linked warehouses further reinforce dominance. Vietnam’s container throughput has grown steadily alongside electronics and apparel exports, increasing demand for conveyorized pallet and carton handling in port-adjacent distribution centers. Likewise, airports such as Thailand’s Suvarnabhumi rely on automated sortation to process time-sensitive air cargo efficiently.

Based on End-User:

- Retail & E-commerce

- Logistics Service Providers (3PL / 4PL)

- Manufacturing

- Food & Beverage

- Healthcare & Pharmaceuticals

- Automotive & Industrial

- Electronics & High-Tech

- Cold Chain Specialists

- Government / Defense Logistics

- Warehouse Property Developers

Logistics Service Providers (3PL/4PL) dominate warehouse automation adoption in Southeast Asia because the region’s supply chains are highly outsourced, cross-border in nature, and volume-concentrated, which structurally places automation investment decisions with logistics specialists rather than individual manufacturers or retailers. As trade lanes span multiple countries and service-level expectations tighten, shippers increasingly rely on 3PLs to deliver speed, accuracy, and cost efficiency at scale.

For instance, Southeast Asia’s trade and e-commerce flows are progressively consolidated into centralized logistics hubs managed by large service providers. In Singapore, PSA and state-linked logistics operators have expanded automated inland container depots and distribution facilities to support transshipment and regional distribution, embedding conveyor, sortation, and yard automation as core infrastructure rather than optional upgrades. This centralization concentrates throughput in 3PL-operated facilities, naturally accelerating automation uptake.

Similarly, in Thailand, Thailand Post has deployed automated parcel-sorting systems at major logistics centers to manage rising domestic and cross-border parcel volumes driven by e-commerce, illustrating how national logistics operators shoulder automation investments to meet delivery commitments. For instance, Vietnam’s Vietnam Post and Viettel Post have expanded automated sortation and conveyor systems at national hubs as express volumes grow, reinforcing that throughput and accuracy accountability sit with logistics providers. Likewise, Indonesia’s national logistics blueprint explicitly promotes large, automated logistics centers operated by 3PLs to reduce persistently high domestic logistics costs.

Southeast Asia Warehouse Automation Market (2026-32): Regional Projection

Indonesia’s dominance with a market share of about 30% in this market is fundamentally driven by scale, where rising digital consumption directly translates into automation necessity rather than optional efficiency. As Southeast Asia’s largest e-commerce economy, Indonesia recorded an estimated USD52.9 billion in e-commerce transaction value in 2023 , generating sustained, high-frequency order volumes that strain manual warehousing models and elevate demand for automated sorting, storage, and picking systems.

This demand pressure is structurally reinforced by government-led logistics reform. Indonesia’s National Logistics Ecosystem (NLE) integrates ports, customs, freight forwarders, and digital clearance systems, and by late 2024 had expanded to 46 seaports and six airports, reducing dwell times and enabling faster cargo turnover . As logistics velocity improves, warehouse operators are compelled to adopt automation to prevent inland bottlenecks from offsetting port-side efficiency gains. These facilities, often multi-story due to land constraints around Greater Jakarta, are structurally dependent on AS/RS, conveyor-sortation systems, and autonomous mobile robots to maximize throughput and space utilization.

Gain a Competitive Edge with Our Southeast Asia Warehouse Automation Market Report:

- Southeast Asia Warehouse Automation Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- Southeast Asia Warehouse Automation Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Southeast Asia Warehouse Automation Market Policies, Regulations, and Product Standards

- Southeast Asia Warehouse Automation Market Trends & Developments

- Southeast Asia Warehouse Automation Market Dynamics

- Growth Factors

- Challenges

- Southeast Asia Warehouse Automation Market Hotspot & Opportunities

- Southeast Asia Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- Hardware

- Robots (AMRs, AGVs, SCARA/Delta Arms)

- Conveyors & Sorters

- AS/RS Cranes & Shuttles

- Sensors & Scanners

- PLC / Controls

- Software

- WMS / Warehouse Execution Software

- Warehouse Control Systems

- Fleet / Robot Orchestration

- Analytics & Optimization

- Services

- Installation & Integration

- Maintenance & Support

- Training & Consulting

- Custom Engineering

- Hardware

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- Automated Storage and Retrieval Systems (AS/RS)

- Autonomous Mobile Robots (AMRs)

- Automated Guided Vehicles (AGVs)

- Conveyor & Sortation Systems

- Robotic Picking & Palletizing

- Automated Packing & Labeling

- Warehouse Management Systems (WMS / WES / WCS)

- Automated Identification Systems (RFID / Barcode / Vision)

- Automated Packaging Systems

- Drones & Vision Inspection Automation

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- Small Warehouses (Below 10,000 sq. meters)

- Medium Warehouses (10,000–50,000 sq. meters)

- Large Warehouses (Above 50,000 sq. meters)

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Retail & E-commerce

- Logistics Service Providers (3PL / 4PL)

- Manufacturing

- Food & Beverage

- Healthcare & Pharmaceuticals

- Automotive & Industrial

- Electronics & High-Tech

- Cold Chain Specialists

- Government / Defense Logistics

- Warehouse Property Developers

- By Country

- Philippines

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Singapore

- Rest of Southeast Asia

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Philippines Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Thailand Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Vietnam Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Malaysia Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Singapore Warehouse Automation Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Component- Market Size & Forecast 2022-2032, USD Million

- By Automation Type- Market Size & Forecast 2022-2032, USD Million

- By Warehouse Scale- Market Size & Forecast 2022-2032, USD Million

- By End-Use Industry- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Southeast Asia Warehouse Automation Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Sun & Siasun Robot Co., Ltd..

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Quicktron

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Geek+

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Vanderlande Industries

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Dematic

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Daifuku Co., Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Swisslog Holding AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Omron Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- DF Automation and Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ALS Logistic Solutions

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Gen Surv Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- PingSpace Sdn. Bhd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- System Logistics Asia

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- GreyOrange

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Locus Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- HAI Robotics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell Intelligrated

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AutoStore

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KNAPP AG

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Murata Machinery, Ltd.

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toyota Material Handling

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- KION Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- ABB

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Yaskawa Electric Corporation

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Godrej Consoveyo Logistics

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Toshiba

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SSI Schaefer

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Honeywell

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Siemens

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Sun & Siasun Robot Co., Ltd..

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now