Southeast Asia Color Cosmetics Market Research Report: Trends & Forecast (2026-2032)

By Product Type (Face, Lip, Eye, Nail Cosmetics, Others), By Distribution Channel (Offline Retail, Online Retail, Direct Selling), By Price Product (Mass-Market Products, Prestige ... Premium Products), By Product Formulation (Powder, Cream, Gel, Stick, Liquid), By Value -Proposition (Long Wear, Hydrating, Matte, Natural Finish, Buildable), and others Read more

- FMCG

- Feb 2026

- Pages 280

- Report Format: PDF, Excel, PPT

Southeast Asia Color Cosmetics Market

Projected 7.08% CAGR from 2026 to 2032

Study Period

2026-2032

Market Size (2026)

USD 4.63 Billion

Market Size (2032)

USD 6.98 Billion

Base Year

2025

Projected CAGR

7.08%

Leading Segments

By Price Product: Mass-Market Products

Southeast Asia Color Cosmetics Market Report Key Takeaways:

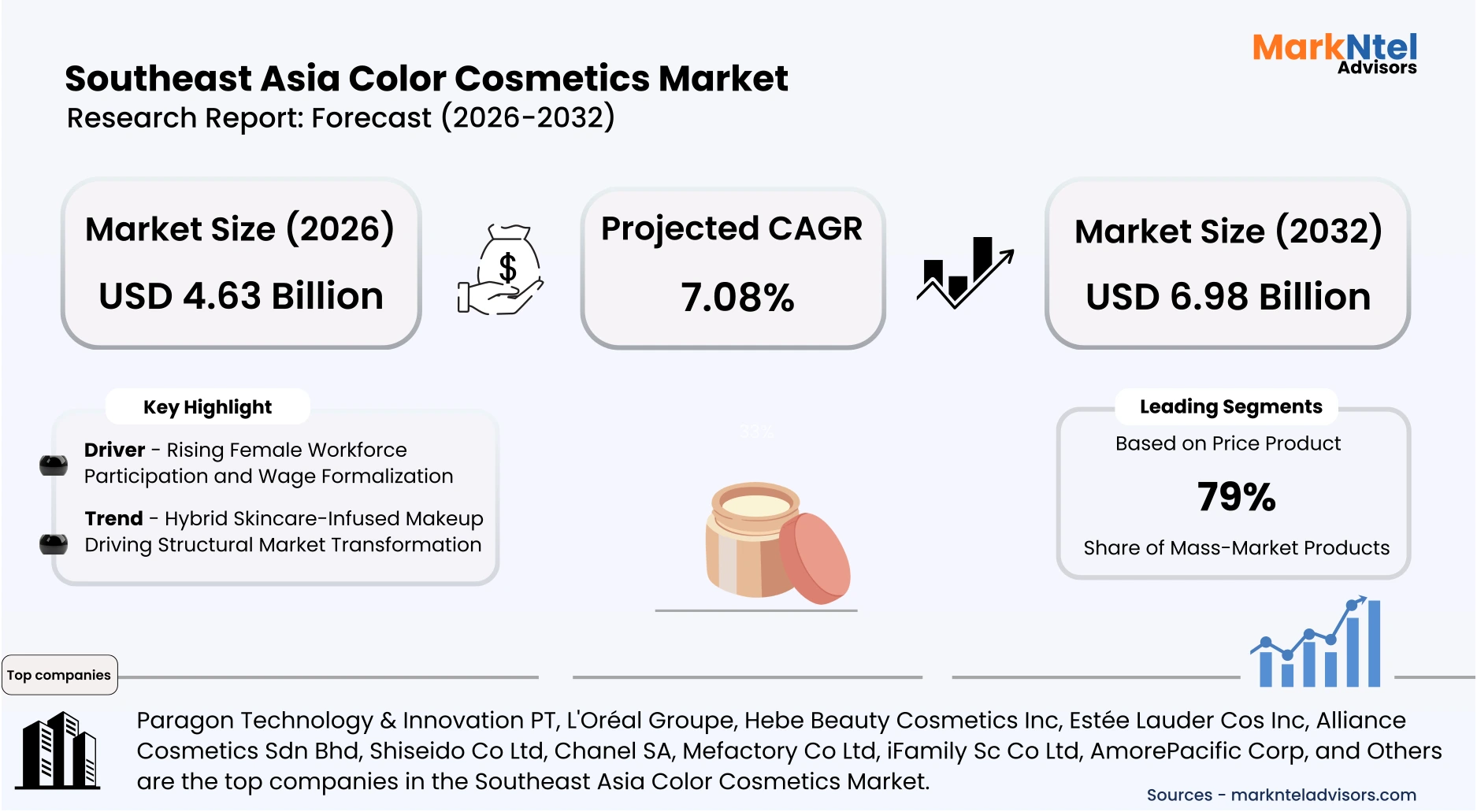

- Southeast Asia Color Cosmetics Market size was valued at USD 4.21 billion in 2025 and is projected to grow from USD 4.63 billion in 2026 to USD 6.98 billion by 2032, exhibiting a CAGR of 7.08% during the forecast period.

- By Product type, the Lip products represented a significant share of about 40% in the Southeast Asia Color Cosmetics Market in 2026.

- By Distribution Channel, the Online retail segment represented a significant share of about 39% in the Southeast Asia Color Cosmetics Market in 2026.

- By Price Product, the Mass-market products presented a significant share of about 79% in the Southeast Asia Color Cosmetics Market in 2026.

- Leading cosmetics companies in the Market are Paragon Technology & Innovation PT, L'Oréal Groupe, Hebe Beauty Cosmetics Inc, Estée Lauder Cos Inc, Alliance Cosmetics Sdn Bhd, Shiseido Co Ltd, Ever Bilena Cosmetics Inc, Natura &Co, Face Party Inc, SSUP Group, Giffarine Group of Cos, Chanel SA, Mefactory Co Ltd, iFamily Sc Co Ltd, AmorePacific Corp, and Others.

Market Insights & Analysis: Southeast Asia Color Cosmetics Market (2026-32):

The Southeast Asia Color Cosmetics Market size was valued at USD 4.21 billion in 2025 and is projected to grow from USD 4.63 billion in 2026 to USD 6.98 billion by 2032, exhibiting a CAGR of 7.08% during the forecast period. i.e, 2026-2032.

Industry-led expansion is currently bolstered by the Ministry of Health in Vietnam, which issued a circular to modernize the cosmetic notification process via the National Public Service Portal. These digital infrastructure improvements simplify market access for international brands, ensuring that product registrations align with the ASEAN Cosmetic Directive. Future market prospects remain positive as regional governments integrate beauty manufacturing into their long-term industrial competitiveness frameworks to drive consistent volume growth.

Economic and demographic factors, particularly the rise of a digitally savvy middle class, have shifted demand toward high-performance products across diverse end-user segments. Residential consumers in the Philippines are increasingly utilizing live-stream shopping, a trend supported by the Philippine E-commerce Roadmap 2022–2027, which aims to enhance digital trust and infrastructure . National publications, including The Philippine Star and BusinessWorld, report that the Chamber of Cosmetics Industry of the Philippines, Inc. projects double-digit expansion in both retail value and sales volume for 2025, indicating sustained momentum across the country’s cosmetics and personal care sector. These national development programs foster a resilient ecosystem where both local startups and global conglomerates can scale operations efficiently.

Regulatory frameworks are becoming more specialized, with Indonesia’s BPJPH mandating that all cosmetic products must obtain halal certification by October 17, 2026, under Government Regulation No. 42 of 2024. This policy serves as a critical industry-led factor, as it necessitates manufacturing investments in halal-compliant production lines to serve the region's largest consumer base. Companies like Wardah and the Martha Tilaar Group are leading localization strategies to meet these stringent quality standards while catering to ethical consumerism . Such initiatives ensure that the market size continues to expand through higher compliance-led consumer confidence and localised supply chain integration.

In late 2025, the Thailand Board of Investment (BOI) allocated approximately USD 153 million to a new funding scheme aimed at strengthening industrial human capital in advanced biotechnology . This investment supports the development of eco-friendly formulations, allowing manufacturers to adopt energy-efficient technologies and sustainable packaging solutions to meet international export standards.

Southeast Asia Color Cosmetics Market Recent Developments:

- 2025: DOWSIL™ FC-5012 ID Resin Gum A new formulation ingredient unveiled at in-cosmetics Asia 2025in Bangkok, Thailand, which is designed to improve color cosmetic performance with enhanced sebum and water repellency and better rub resistance, enabling brands to formulate longer-lasting makeup.

- 2025: Paragon unveiled Light+ by Wardah, a new halal beauty brand targeted at Gen Z consumers, blending skincare and makeup features tailored for youth lifestyles, a strategic product innovation for local market growth.

Southeast Asia Color Cosmetics Market Scope:

| Category | Segments |

|---|---|

| By Product Type | (Face, Lip, Eye, Nail Cosmetics, Others), |

| By Distribution Channel | (Offline Retail, Online Retail, Direct Selling), |

| By Price Product | (Mass-Market Products, Prestige Premium Products), |

| By Product Formulation | (Powder, Cream, Gel, Stick, Liquid), |

| By Value -Proposition | (Long Wear, Hydrating, Matte, Natural Finish, Buildable), |

Southeast Asia Color Cosmetics Market Driver:

Rising Female Workforce Participation and Wage Formalization

A principal structural driver of the Southeast Asia Color Cosmetics Market is the sustained rise in female labor force participation and wage formalization. The International Labor Organization reported in 2025 that female labor participation in Vietnam exceeds 69.13%, among the highest in the region. Concurrently, the Department of Statistics Malaysia recorded nominal wage growth above 3% in 2024, strengthening purchasing power. Formal employment expansion increases discretionary expenditure on personal appearance-related categories.

This workforce expansion has measurably influenced consumption intensity in urban centers. In Indonesia, the national minimum wage adjustments implemented in 2025 raised income thresholds for formal workers, according to the Ministry of Manpower. Greater financial independence has elevated repeat purchase frequency across daily-use cosmetics such as foundations and lip products. Corporate grooming norms in financial services and hospitality sectors further reinforce routine product usage. Consequently, demand growth reflects volumetric expansion rather than short-term pricing effects.

The driver’s durability stems from policy-backed gender inclusion strategies. The Philippine Commission on Women advanced its 2025 Gender Equality and Women’s Empowerment Plan to enhance workforce integration. Similarly, Thailand’s 2026 labor development programs prioritize female upskilling in service industries. These structural shifts enlarge the economically active female base, directly expanding the addressable consumer pool for color cosmetics. The sustained linkage between employment formalization and consumption patterns underscores its material contribution to long-term market growth.

Southeast Asia Color Cosmetics Market Trend:

Hybrid Skincare-Infused Makeup Driving Structural Market Transformation

The most significant trend reshaping the Southeast Asia color cosmetics market is the "skinification" of makeup, where consumers prioritize hybrid products that offer both aesthetic and dermatological benefits. This shift is driven by a post-pandemic emphasis on skin health, leading to high demand for foundations and lip products infused with active ingredients like hyaluronic acid and SPF. This behavior is particularly prevalent in tropical climates where consumers seek lightweight, breathable formulations that provide long-term protection against environmental stressors and digital blue-light exposure.

Structural changes are occurring across the value chain as manufacturers pivot from traditional color-only formulations to advanced "beauty-tech" and biotechnology-driven production methods. Major industry participants are now investing in R&D facilities that focus on "less is more" formulations, using fewer raw materials to achieve higher performance and safety standards. In the Philippines, recent collaborations in 2024 between local firms and South Korean dermatological labs have introduced plant-based stem cell makeup lines to the mass market . This trend is forcing distributors to rethink their inventory strategies, as high-SKU counts are being replaced by high-performance, multi-functional staples that command premium pricing.

This trend is expected to persist and influence long-term market evolution because it aligns with the broader global movement toward "clean" and "conscious" beauty. Government-led initiatives, such as Singapore’s ongoing support for biotechnology under its Research, Innovation, and Enterprise (RIE) plans, provide the infrastructure for sustainable ingredient sourcing . As of early 2026, consumer surveys indicate that over 60% of regional shoppers now check ingredient lists for skin-friendly properties before purchasing color cosmetics. This fundamental shift in consumer behavior ensures that future market growth will be dominated by brands that successfully merge the boundaries between traditional skincare and high-fashion color cosmetics.

Southeast Asia Color Cosmetics Market Opportunity:

Mobile-First Commerce & Digital Incentives Unlocking SME Expansion Potential

The expansion of digital trade infrastructure and social commerce platforms presents the most compelling opportunity for new entrants to achieve scalable growth without traditional retail overhead. In early 2026, the Philippines witnessed a surge in internet penetration, with 5G outdoor coverage reaching over 97% in the National Capital Region, facilitating seamless mobile-first shopping experiences. This technological shift allows emerging brands to bypass established distribution monopolies by utilizing live-streaming and influencer-led marketing to reach rural and underserved demographics directly. Consequently, digital connectivity acts as a structural equalizer, enabling smaller players to gain rapid market share through high-engagement, low-cost customer acquisition.

This opportunity translates into tangible market demand through the "platform convergence" trend, where social media, payment gateways, and logistics are integrated into a single user experience. According to 2025 e-commerce data, the Philippine online market reached immense heights, with beauty and personal care emerging as a top-performing category for digital transactions. New entrants can leverage this by launching "digital-native" brands that utilize real-time consumer data to iterate product formulations and marketing strategies more quickly than incumbents. The ability to offer niche, personalized products through these high-traffic digital corridors ensures a steady stream of demand from younger, tech-savvy consumer segments.

Smaller players are particularly advantaged by this environment because they possess the agility to adopt "clean beauty" and "halal-tech" innovations that resonate with modern values. While large incumbents face high costs in retooling massive supply chains, new entrants can build lean, specialized operations that comply with the latest 2026 Indonesian halal mandates from the start. Furthermore, government incentives for digital transformation in local businesses, such as those provided by the DTI in the Philippines, provide financial and technical support. These conditions allow emerging companies to differentiate themselves through authentic branding and ethical practices, effectively capturing the growing segment of conscious consumers.

Southeast Asia Color Cosmetics Market Challenge:

Rising Regulatory Compliance Burden & Entry Barriers

The Southeast Asia cosmetics market is witnessing a progressive tightening of regulatory enforcement and documentation standards, which is elevating structural entry barriers across the region. Although the ASEAN Cosmetic Directive aims to harmonize compliance requirements, national-level implementation and inspection intensity vary, increasing administrative complexity for multi-country operators.

Manufacturers are required to maintain comprehensive and audit-ready Product Information Files (PIFs), conduct periodic safety validations, ensure ingredient conformity with updated restricted substance lists, and manage timely product notification renewals. These obligations are increasing fixed compliance costs and lengthening product commercialization timelines.

The burden is particularly pronounced for small and mid-sized enterprises (SMEs), which often lack in-house regulatory expertise and structured compliance systems. As regulatory preparedness becomes a competitive differentiator, larger and well-capitalized players are better positioned to absorb rising compliance costs. Over time, this dynamic may contribute to gradual market consolidation and reduced agility among emerging brands.

Southeast Asia Color Cosmetics Market (2026-32) Segmentation Analysis:

Southeast Asia Color Cosmetics Market study of MarkNtel Advisors evaluates & highlights the major trends and influencing factors in each segment. It includes predictions for the period 2026–32 at the regional level. Based on the analysis, the market has been further classified as:

Based on Product Type:

- Face

- Lip

- Eye

- Nail Cosmetics

- Others

Lip products dominate the regional color cosmetics market by a market share of 40%, supported by structural consumption patterns and retail accessibility. Lipsticks, lip tints, balms, and glosses serve as entry-level beauty products across income groups due to their lower price points and high frequency of purchase. Rising female workforce participation and urbanization across Southeast Asia have reinforced daily-use demand for portable, quick-application formats. Additionally, regulatory harmonization under the ASEAN Cosmetic Directive facilitates faster product notification for standardized lip formulations, enabling quicker cross-border launches and distribution expansion.

Sustained dominance is further linked to investment flows and brand strategy. Both multinational and local players prioritize lip categories for innovation cycles, influencer collaborations, and limited-edition shade drops, given shorter development timelines and faster inventory turnover . E-commerce expansion and social commerce ecosystems amplify repeat purchases and shade experimentation, particularly among Gen Z consumers . Moreover, halal-certified and dermatologically tested lip variants are witnessing stronger traction in key Muslim-majority markets, reinforcing consistent demand across diverse consumer bases.

The region’s predominantly hot and humid tropical climate significantly influences product usage patterns and formulation preferences favor lightweight, transfer-resistant, and hydrating lip formats over heavier face products. High product trial rates , gifting culture, and impulse-driven retail behavior further support consistent volume momentum within the category. Combined with relatively accessible price points, streamlined regulatory pathways under ASEAN harmonization frameworks, rapid shade innovation cycles, and strong integration with digital and social commerce channels, lip cosmetics continue to demonstrate structural resilience and sustained commercial relevance across Southeast Asia.

Based on Price Product:

- Mass-Market Products

- Prestige Premium Products

The Mass-Market Products segment dominates the color cosmetics landscape in Southeast Asia, with a market share of 79%, catering to a vast and diverse demographic with a focus on affordability and accessibility. This segment’s leadership is sustained by the rapid expansion of modern retail channels, including pharmacies and hypermarkets, which prioritize high-volume, low-cost inventory. In 2024 and 2025, inflationary pressures led many consumers to seek "dupes" or cost-effective alternatives to luxury brands, further boosting the sales of mass-market lipsticks and eye palettes. This shift toward value-for-money products ensures that the mass-market segment captures the largest share of the growing middle-class and Gen Z consumer base.

Market drivers such as the growth of e-commerce platforms like Shopee and TikTok Shop have disproportionately benefited mass-market brands by providing them with a low-cost distribution network. Furthermore, local manufacturing investments in Indonesia and Vietnam have enabled mass-market players to reduce costs through localized supply chains and lower import duties. These strategies allow brands to maintain competitive pricing while adhering to the mandatory halal and safety regulations required for regional market entry.

Consumer demand within the mass-market segment is largely shaped by a preference for cost-effective offerings that balance price and quality for trendy, high-frequency purchases rather than long-term investment in single high-end products. This behavior is supported by the rapid turnover of digital beauty trends, which encourages consumers to experiment with different colors and formats at a lower financial risk. Government-led support for micro-SMEs in the Philippines and Malaysia also fosters a vibrant ecosystem of affordable local brands that compete effectively with global giants.

Southeast Asia Color Cosmetics Market (2026-32) Regional Analysis:

Indonesia stands as the largest and most dominant market for color cosmetics in Southeast Asia, outperforming its neighbors in terms of both demand concentration and adoption intensity. This regional leadership is anchored by a population of over 280 million, which provides a massive and growing consumer base for beauty and personal care products. Economic factors, such as the 5.0% GDP growth projected for 2025, have significantly increased the purchasing power of the urban middle class, particularly in major hubs like Jakarta and Surabaya. This industrial concentration has attracted major global manufacturers to establish local production facilities, ensuring a steady supply of innovative and culturally relevant cosmetic products.

The 2026 regulatory enforcement framework enhances entry barriers within the cosmetics segment, disproportionately benefiting incumbents with established compliance systems and localized operational footprints. This policy has not only protected the domestic market but has also positioned Indonesia as a global hub for halal beauty, attracting significant foreign investment in specialized manufacturing. Furthermore, the Indonesian government’s "Making Indonesia 4.0" initiative provides tax incentives and R&D support for companies adopting advanced digital and green technologies in their production lines.

The concentration of major industry players like Paragon Technology and Innovation (Wardah) has fostered a highly competitive yet innovative market landscape. These companies leverage a vast network of thousands of beauty advisors and a robust digital presence to maintain a dominant market share. According to official 2025 statistics, Indonesia's beauty and personal care market is the primary driver of regional growth, supported by a rapid shift toward sophisticated skincare-infused color cosmetics.

Vietnam, while smaller in population, has emerged as the most aggressive e-commerce-driven cosmetics market in the region. High livestream commerce adoption and strong Korean brand penetration have positioned Vietnam as a leading revenue contributor in online beauty transactions. Urban centers such as Ho Chi Minh City and Hanoi serve as innovation hubs where trend-sensitive Gen Z consumers rapidly adopt serum-based foundations, tint lip products, and lightweight hybrid formulations.

Gain a Competitive Edge with Our Southeast Asia Color Cosmetics Market Report:

- Southeast Asia Color Cosmetics Market Report by MarkNtel Advisors provides a detailed & thorough analysis of market size & share, growth rate, competitive landscape, and key players. This comprehensive analysis helps businesses gain a holistic understanding of the market dynamics & make informed decisions.

- This report also highlights current market trends & future projections, allowing businesses to identify emerging opportunities & potential challenges. By understanding market forecasts, companies can align their strategies & stay ahead of the competition.

- The Southeast Asia Color Cosmetics Market Report aids in assessing & mitigating risks associated with entering or operating in the market. By understanding market dynamics, regulatory frameworks, and potential challenges, businesses can develop strategies to minimize risks & optimize their operations.

*Reports Delivery Format - Market research studies from MarkNtel Advisors are offered in PDF, Excel and PowerPoint formats. Within 24 hours of the payment being successfully received, the report will be sent to your email address.

Frequently Asked Questions

- Market Segmentation

- Introduction

- Product Definition

- Research Process

- Assumptions

- Executive Summary

- Southeast Asia Color Cosmetics Market Policies, Regulations, and Product Standards

- Southeast Asia Color Cosmetics Market Trends & Developments

- Southeast Asia Color Cosmetics Market Dynamics

- Growth Factors

- Challenges

- Southeast Asia Color Cosmetics Market Hotspot & Opportunities

- Southeast Asia Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Face

- Lip

- Eye

- Nail Cosmetics

- Others

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- Offline Retail

- Online Retail

- Direct Selling

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- Mass-Market Products

- Prestige Premium Products

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- Powder

- Cream

- Gel

- Stick

- Liquid

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Long Wear

- Hydrating

- Matte

- Natural Finish

- Buildable

- By Country

- Indonesia

- Malayasia

- Singapore

- Thailand

- Vietnam

- Philippines

- Rest of Southeast Asia

- By Company

- Competition Characteristics

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Indonesia Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Malayasia Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Singapore Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Thailand Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Vietnam Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Philippines Color Cosmetics Market Outlook, 2022-2032F

- Market Size & Outlook

- By Revenues (USD Million)

- Market Share & Analysis

- By Product Type- Market Size & Forecast 2022-2032, USD Million

- By Distribution Channel- Market Size & Forecast 2022-2032, USD Million

- By Price Product- Market Size & Forecast 2022-2032, USD Million

- By Product Formulation- Market Size & Forecast 2022-2032, USD Million

- By Value -Proposition- Market Size & Forecast 2022-2032, USD Million

- Market Size & Outlook

- Southeast Asia Color Cosmetics Market Key Strategic Imperatives for Success & Growth

- Competitive Outlook

- Company Profiles

- Paragon Technology & Innovation PT

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- L'Oréal Groupe

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Hebe Beauty Cosmetics Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Estée Lauder Cos Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Alliance Cosmetics Sdn Bhd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Shiseido Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Ever Bilena Cosmetics Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Natura &Co

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Face Party Inc

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- SSUP Group

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Giffarine Group of Cos

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Chanel SA

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Mefactory Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- iFamily Sc Co Ltd

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- AmorePacific Corp

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Others

- Business Description

- Product Portfolio

- Collaborations & Alliances

- Recent Developments

- Financial Details

- Others

- Paragon Technology & Innovation PT

- Company Profiles

- Disclaimer

MarkNtel Advisors follows a robust and iterative research methodology designed to ensure maximum accuracy and minimize deviation in market estimates and forecasts. Our approach combines both bottom-up and top-down techniques to effectively segment and quantify various aspects of the market. A consistent feature across all our research reports is data triangulation, which examines the market from three distinct perspectives to validate findings. Key components of our research process include:

1. Scope & Research Design At the outset, MarkNtel Advisors define the research objectives and formulate pertinent questions. This phase involves determining the type of research—qualitative or quantitative—and designing a methodology that outlines data collection methods, target demographics, and analytical tools. They also establish timelines and budgets to ensure the research aligns with client goals.

2. Sample Selection and Data Collection In this stage, the firm identifies the target audience and determines the appropriate sample size to ensure representativeness. They employ various sampling methods, such as random or stratified sampling, based on the research objectives. Data collection is carried out using tools like surveys, interviews, and observations, ensuring the gathered data is reliable and relevant.

3. Data Analysis and Validation Once data is collected, MarkNtel Advisors undertake a rigorous analysis process. This includes cleaning the data to remove inconsistencies, employing statistical software for quantitative analysis, and thematic analysis for qualitative data. Validation steps are taken to ensure the accuracy and reliability of the findings, minimizing biases and errors.

4. Data Forecast and FinalizationThe final phase involves forecasting future market trends based on the analyzed data. MarkNtel Advisors utilize predictive modeling and time series analysis to anticipate market behaviors. The insights are then compiled into comprehensive reports, featuring visual aids like charts and graphs, and include strategic recommendations to inform client decision-making

We offer flexible licensing options to cater to varying organizational needs. Choose the pricing pack that best suits your requirements:

Buy Now